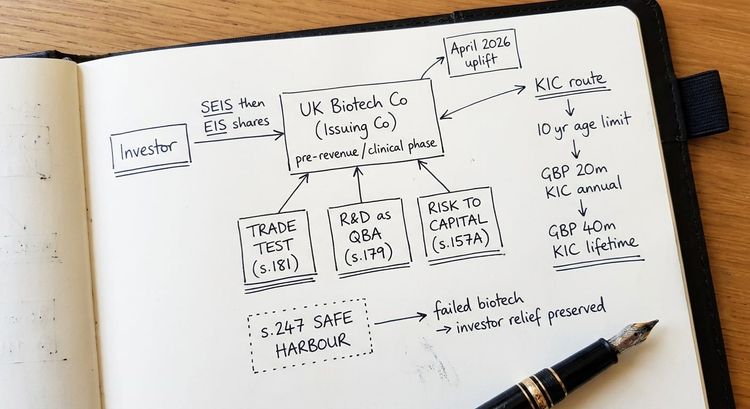

SEIS and EIS for Loss-Making Biotech: A UK Funding Guide

How SEIS and EIS apply to UK loss-making biotech. Trade test, R&D as qualifying activity, KIC status, April 2026 EIS uplift and loss relief on failure.

13 hours ago