Enterprise Management Incentives (EMI) are one of the most tax-efficient ways for UK companies to reward and retain key employees. Before granting a single option, however, most advisers recommend obtaining EMI advance assurance from HMRC. This confirmation gives the company and its employees certainty that the scheme qualifies under Schedule 5 ITEPA 2003, before any options are on the table. Getting the application wrong can delay the entire process by months, or result in options being granted without the protection that advance assurance provides.

This guide sets out what HMRC actually checks during the advance assurance process, what a strong application contains, the common reasons HMRC refuses or raises queries, and how long you should expect to wait.

What Is EMI Advance Assurance?

EMI advance assurance is a written confirmation from HMRC that, based on the information provided, the company meets the qualifying conditions for the Enterprise Management Incentives scheme. It is not a legal requirement. You can grant EMI options without it. In practice, however, any adviser who does not recommend seeking advance assurance is taking a significant risk on their client's behalf.

The assurance is company-specific. It confirms that the employer qualifies under Schedule 5 ITEPA 2003, but it does not individually pre-approve each option agreement, each employee's terms, or the exercise price. It also does not override HMRC's right to open an enquiry after options have been granted. What it does do is give directors and employees confidence that the fundamental structure is sound before the company incurs the cost of legal documentation and before employees start planning their equity position.

Who Can Apply?

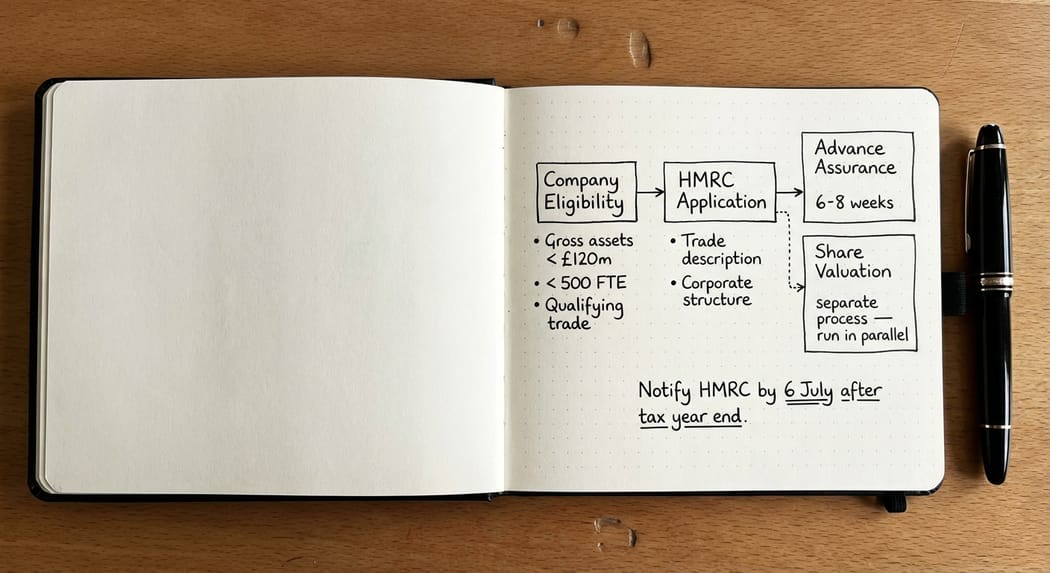

To obtain EMI advance assurance, the company applying must be a qualifying company under the EMI legislation. HMRC uses the advance assurance process to check the company against the main qualifying conditions. These are:

The trading requirement. The company must be an independent trading company, or the holding company of a qualifying group. "Trading" for EMI purposes is broadly defined but HMRC draws firm lines. Certain activities are categorically excluded.

Excluded activities. The legislation in Schedule 5 ITEPA 2003 sets out activities that disqualify a company or cause disqualification if they represent a "substantial" part of its business. The legislation does not define "substantial" numerically; HMRC applies a working guideline of more than 20 per cent of turnover, assets, or time, though this is practice rather than a fixed statutory threshold. Excluded activities include: dealing in land or property development, financial activities (banking, insurance, money lending, leasing), receipt of royalties or licence fees (unless arising from intangible assets created by the company), farming and market gardening, hotel and nursing home operations, and legal or financial services. Companies in these sectors routinely receive rejections or queries, and the advance assurance application must address them directly.

The gross assets test. The company's gross assets must not exceed £30 million at the time each option is granted (increasing to £120 million for grants made on or after 6 April 2026, under Finance Bill 2025-26). For advance assurance purposes, HMRC will check the latest available balance sheet figures and the trend.

The employee headcount test. The company must have fewer than 250 full-time equivalent employees at the date of each option grant (increasing to 500 FTE for grants made on or after 6 April 2026, under Finance Bill 2025-26). Part-time employees are counted on a pro-rata basis.

Independence. The company must not be a 51 per cent subsidiary of another company unless the parent itself qualifies as a trading company.

UK permanent establishment. The company must have a permanent establishment in the United Kingdom.

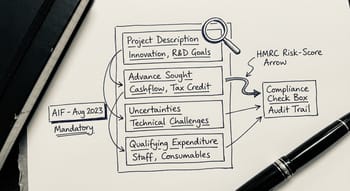

What to Include in Your EMI Advance Assurance Application

HMRC's standard guidance asks for specific information, and a weak application is the most common cause of delay. A strong application includes the following.

A description of the company's trade. This should be clear, specific, and honest. Vague descriptions ("technology company providing software solutions") give HMRC nothing to work with. Describe what the company actually does, how it generates revenue, what its customers buy, and whether any part of the business touches the excluded activities list. If there is any connection to property, finance, or IP licensing, address it head-on and explain why it does not meet the substantial-activity threshold.

The company's ownership structure. Include a corporate structure chart if the company has subsidiaries or is part of a group. HMRC needs to confirm independence and that the parent, if any, also meets the trading requirement.

Current financial position. Provide the most recent accounts or management accounts, including gross assets figures. If the company is approaching the applicable gross assets threshold (£30 million for grants before 6 April 2026, £120 million from 6 April 2026), HMRC will want to understand the position as of the planned grant date.

Employee headcount. Provide a headcount breakdown, distinguishing between full-time and part-time employees. State the anticipated headcount at the expected grant date if this differs materially from today.

The proposed option plan. Describe in outline the terms of the scheme: the total number of options to be granted, the proposed exercise price, the vesting schedule, and any performance conditions. Individual limits under the legislation are £250,000 per employee (based on unrestricted market value at the date of grant) and £3 million total EMI options outstanding across the company at any time.

Purpose of the options. HMRC expects options to be granted "for genuine commercial purposes." This is a conditions under the legislation that is sometimes overlooked. Confirm that the options are part of the company's recruitment and retention strategy and are not being used for a tax avoidance purpose.

Common Reasons HMRC Refuses or Queries an Application

In our experience, the majority of queries and refusals fall into a small number of categories.

Excluded activities. By far the most common. Companies that have any involvement in property, financial services, or IP licensing need to tread carefully. HMRC's starting point is often to query whether the activity is "substantial." If you have not pre-empted this in the application with specific data, you will receive a query letter asking for more information, and the clock restarts.

Group structure complexity. If the company has subsidiaries, or is itself a subsidiary, HMRC will want to trace the trading activity through the group. Applications that fail to provide a clear corporate structure chart almost always attract a query.

Gross assets above or near the threshold. Companies with gross assets approaching the applicable threshold (£30 million for grants before 6 April 2026, £120 million from 6 April 2026 under Finance Bill 2025-26) need to provide detailed balance sheet evidence (and in some cases projections). HMRC will not give advance assurance where it cannot determine from the application that the threshold is met.

Options not yet fully designed. Advance assurance applications submitted before the company has settled its option plan terms can result in an assurance that is too narrow to be useful, or a refusal on the grounds of insufficient information. The terms do not need to be final, but they do need to be clear enough for HMRC to assess.

EMI Advance Assurance and Share Valuation: Two Separate Processes

A point that causes significant confusion in practice: EMI advance assurance and EMI share valuation are entirely separate applications to HMRC, handled by different teams.

Advance assurance is handled by HMRC's EMI team and confirms the company qualifies. Valuation is handled by HMRC's Shares and Assets Valuation (SAV) team and confirms the unrestricted market value (UMV) of the shares at the date of grant, for income tax purposes.

Companies wishing to grant options at market value (so that employees have no income tax liability on exercise) need to obtain both. The valuation agreement is time-limited: it must be used within 90 days of HMRC's agreement. If the company does not grant options within that window, a fresh valuation will be required.

The two applications should run in parallel where possible, to avoid sequential delays. In our experience, the valuation process takes slightly longer, and if the company has a complex capital structure (multiple share classes, convertible instruments, preference shares with non-standard liquidation waterfalls), it can take considerably longer. Starting both applications simultaneously is almost always the right approach.

How Long Does EMI Advance Assurance Take?

HMRC's published target is to respond within 28 days. In practice, response times vary considerably. For straightforward applications from simple trading companies with clean structures, 4-6 weeks is achievable. For applications requiring further information, or where the trade description is ambiguous, response times of 3-4 months are not unusual.

Practical advice: submit the advance assurance application before legal drafting begins. If you wait until the option agreements are drafted to apply, a two-month delay from HMRC will delay the grant beyond the valuation window, requiring a fresh valuation. Plan the timeline from the outset.

What Happens After Advance Assurance Is Granted?

Advance assurance is not indefinite. It confirms the company's position as of the date of the application, based on the information provided. If material facts change (the company makes an acquisition, gross assets increase substantially, or the trade changes), the advance assurance cannot be relied upon and a fresh application may be needed.

After advance assurance is granted, the company must still:

- Grant options on terms that comply with the legislation (in particular, the individual and aggregate limits, the purpose requirement, and the requirement for a written option agreement)

- Notify HMRC of each EMI option grant on or before 6 July following the end of the tax year in which the option was granted, using HMRC's online ERS service (this deadline is absolute; late notification means the options are not qualifying EMI options)

- File an annual EMI return via the PAYE online service

The notification deadline (6 July following the end of the tax year in which the option was granted) is one of the most frequently missed requirements in the EMI process. It cannot be extended, it does not have a "reasonable excuse" carve-out, and missing it means the options lose their qualifying status entirely. That has significant tax consequences for the employees.

Key Takeaway

EMI advance assurance is one of the most straightforward things a company can do to protect its employee share scheme, but only if the application is prepared with care. A vague trade description, an unexplained group structure, or a failure to address excluded activities will cost you weeks of delay. Get the application right first time.

Frequently Asked Questions

Is EMI advance assurance compulsory?

No. You can grant EMI options without it. In practice, however, most advisers treat it as essential. Without advance assurance, the company and its employees are relying on their own assessment of the qualifying conditions, without HMRC confirmation. If HMRC later disagrees, the options are not qualifying and the income tax and NIC advantages are lost.

How long does EMI advance assurance last?

There is no fixed expiry date for EMI advance assurance. It confirms the company's position as of the application date. If material facts change (the trade evolves, gross assets increase, or the ownership structure changes), the advance assurance may no longer be reliable and a fresh application should be considered. In practice, most companies use the assurance within 12 months of receipt.

Can a subsidiary apply for EMI advance assurance?

A 51 per cent subsidiary cannot grant qualifying EMI options unless its parent is also a qualifying company. Where the group structure is eligible, advance assurance should be obtained at the level of the company actually granting the options, with full disclosure of the group structure in the application.

What is the difference between an EMI option and an unapproved option?

An EMI option is a qualifying option under Schedule 5 ITEPA 2003, granted by a company that meets the EMI conditions. Options granted by qualifying companies on qualifying terms receive significant tax advantages: no income tax on grant, income tax only on the gain above the agreed market value on exercise (and only if the exercise price is below market value), and capital gains treatment on disposal. An unapproved option is any option that does not meet those conditions. It is taxed as employment income on the full gain at exercise, with employer and employee NIC applying. The difference in tax cost can be substantial.

What individual limits apply to EMI options?

Each employee can hold qualifying EMI options over shares with an unrestricted market value of up to £250,000 at the date of grant. The total value of EMI options outstanding across the company at any time must not exceed £3 million. Options above these limits can still be granted, but the excess is treated as unapproved options.

Does HMRC charge for advance assurance?

No. The advance assurance application is free of charge. Any fees incurred are for professional adviser time in preparing the application, not for the HMRC process itself.

What happens if I miss the EMI notification deadline?

Missing the deadline for notifying HMRC of EMI option grants means those options are not qualifying EMI options. The notification must be made on or before 6 July following the end of the tax year in which the option was granted. Options notified late are treated as unapproved options from the date of grant. There is no provision in the legislation to extend or waive this deadline, and no "reasonable excuse" defence applies. This is one of the most serious compliance risks in the EMI process.

Talk to a Specialist Before You Apply

EMI advance assurance is a process that rewards thorough preparation. A clear, complete application prepared by an adviser who understands how HMRC reads these submissions will almost always result in a faster response and fewer queries than an application put together without specialist input.

At IP Tax Solutions, Steve Livingston FCA advises companies on the full EMI process, from initial eligibility assessment and advance assurance through to share valuation, option documentation review, and HMRC annual returns. If you are planning a new EMI scheme or reviewing an existing one, contact us directly: stevelivingston@iptaxsolutions.co.uk or 0161 961 0096.