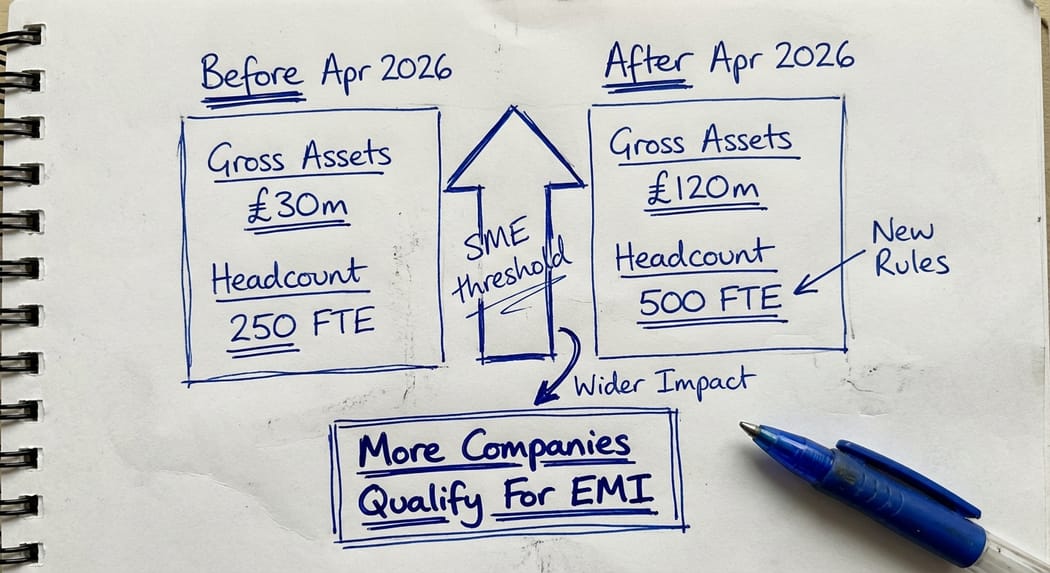

From 6 April 2026, the Enterprise Management Incentives scheme has become accessible to a materially larger pool of UK companies. The gross assets limit has risen from £30 million to £120 million and the employee headcount cap has moved from 250 to 500 full-time equivalent employees. If your company previously sat above one of those thresholds and ruled out EMI on that basis, the position needs to be reassessed today.

This article explains what has changed, how the qualifying conditions work in practice and what steps a company should take if it now qualifies for the first time.

What the EMI Scheme Offers

Before examining eligibility, it is worth being clear about what is at stake. EMI is the most tax-advantaged employee share option scheme available to qualifying UK companies. Options granted at or above unrestricted market value (UMV) can be exercised with no income tax and no National Insurance Contributions on exercise. On a disposal of the resulting shares, employees pay capital gains tax at 18% (on first £1m of lifetime gains) under Business Asset Disposal Relief, subject to a qualifying holding period.

For employers, there is typically no employer NIC exposure on exercise of qualifying options, and the company receives a corporation tax deduction equal to the spread between the exercise price and the market value at exercise.

The scheme is particularly powerful for growth companies where the share price is expected to rise significantly. Options granted today over shares worth £1 could be worth £10 on exit, with the full £9 gain taxed at 18% under Business Asset Disposal Relief, rather than income tax rates of up to 45%.

What Changed on 6 April 2026

Two of the three company-level tests have been relaxed:

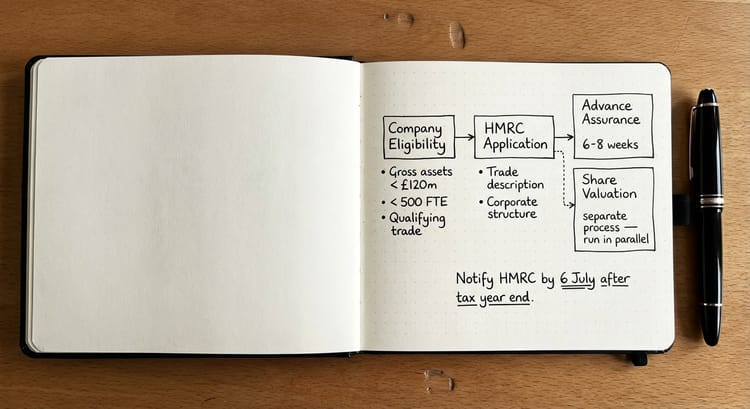

- Gross assets test: previously, the company's gross assets must not have exceeded £30 million at the time of grant. From 6 April 2026, that limit rises to £120 million

- Employee headcount test: previously, the company must have had fewer than 250 full-time equivalent employees. From 6 April 2026, that limit rises to 500 FTE.

These changes apply to options granted on or after 6 April 2026. Options granted before that date remain governed by the old thresholds for the purposes of qualifying at grant.

The third company-level test, the trading company condition (including the excluded activities rules), has not changed. A company must still be a qualifying trading company carrying on a qualifying trade, and must not have more than a "substantial" proportion of its activities in excluded areas such as property development, financial services, leasing or legal services.

How the Gross Assets Test Works in Practice

Gross assets is not the same as net assets. The test uses the total assets figure from the balance sheet, before deducting any liabilities. A company with £100 million of property, plant and equipment and £80 million of debt has gross assets of £100 million, not £20 million.

For groups, the test applies to the aggregate gross assets of the group (the issuing company and its subsidiaries, if any). If the company granting options is a subsidiary, its parent and all group members are included in the calculation.

The test is applied at the time of grant of each tranche of options. A company that exceeds the limit on the date options are granted does not qualify, even if it was below the limit a week earlier.

Under the revised limit, companies with gross assets up to £120 million now qualify. For many Series B and Series C-stage businesses that have raised significant capital and hold cash, IP assets or equipment against their balance sheets, this will bring EMI into reach for the first time.

How the Headcount Test Works in Practice

The employee headcount test uses full-time equivalent employees, not raw headcount. Part-time employees are aggregated on a pro-rata basis: two employees each working half-time count as one FTE. Employees on long-term sick leave or statutory leave continue to count.

The count includes all employees of the group, including those employed by subsidiaries. Directors who are also employees count. Self-employed consultants and agency workers do not count, provided they are genuinely not employees under the employment law test.

For groups, all members of the group are counted together. A company with 200 employees that has a subsidiary with 400 employees has 600 FTE in total and did not qualify before 6 April 2026 under the old 250 limit. Under the new 500 limit, it still does not qualify. The threshold applies to the group as a whole.

The revised limit of 500 FTE brings mid-sized technology businesses, professional services firms and manufacturing companies with multiple sites into scope. For companies that have grown through acquisition and as a result pushed above 250 FTE, this is a significant change.

The Conditions That Have Not Changed

Meeting the revised gross assets and headcount tests is necessary but not sufficient. The following conditions remain unchanged and must all be satisfied for options to qualify:

Trading company condition: the company must be carrying on a qualifying trade. Excluded activities include property development, financial activities, legal services, leasing, farming and certain energy activities. Where a company carries on a mix of qualifying and excluded activities, the excluded element must not be "substantial" in the context of its overall activities.

Independence: the company must not be a 51% subsidiary of another company, and must not be controlled by another company. This catches situations where a PE-backed company has technically ceded control to its investor.

Qualifying subsidiary condition: if the trade is carried on through subsidiaries, those subsidiaries must themselves be qualifying subsidiaries, broadly meaning the issuing company holds more than 50% of the ordinary share capital.

Individual qualifying conditions: employees receiving options must work at least 25 hours per week, or if less, at least 75% of their total working time, for the company or group. This is the working time requirement. It applies at the time of grant and must be maintained.

Grant limits: each employee may hold qualifying EMI options over shares with an unrestricted market value of no more than £250,000 at the date of grant. The total value of qualifying options outstanding across all participants must not exceed £6 million from 6 April 2026 (increased from the previous £3 million).

HMRC notification: each grant of options must be notified to HMRC through the Employment Related Securities (ERS) online service by 6 July following the end of the tax year in which the grant is made (for options granted on or after 6 April 2024). Missing this deadline means the options are not qualifying EMI options.

Key takeaway: the April 2026 changes significantly expand the company-level eligibility for EMI. But the trading company condition, the independence requirement, the working time rule and the grant limits remain unchanged. A company that now passes the gross assets and headcount tests still needs to satisfy all of the other conditions.

What to Do If Your Company Now Qualifies

If your company was previously excluded by the gross assets or headcount limit, the first step is to carry out a full eligibility review before granting any options. This should cover every condition in Schedule 5 ITEPA 2003, not just the two tests that have changed.

The most common areas where eligibility breaks down in practice are the excluded activities test, the independence condition and in complex group structures the qualifying subsidiary condition.

Once eligibility is confirmed, the practical next steps are:

- Agree a share valuation with HMRC: you are not obliged to obtain advance agreement on the value of the shares, but doing so protects both the company and the employee. The HMRC Shares and Assets Valuation (SAV) team will review a formal submission and if they agree will provide an agreed unrestricted market value that can be used for options granted within a specified window.

- Apply for advance assurance: separately from the valuation, companies can apply to HMRC for advance assurance that the company and the proposed share scheme qualify for EMI. This is not mandatory but gives comfort before options are granted. It is particularly useful where there is any doubt about the excluded activities position or the group structure. For a detailed walkthrough of the advance assurance process, see our guide to EMI advance assurance applications.

- Draft scheme documents: the option agreement and the scheme rules need to be carefully drafted. The terms must not fall outside the parameters set by Schedule 5 ITEPA 2003, including on good and bad leaver provisions.

- Notify HMRC by 6 July: for options granted on or after 6 April 2024, HMRC notification must be made by 6 July following the end of the tax year in which the grant is made (for example, options granted in the 2026-27 tax year must be notified by 6 July 2027). Build this into the implementation timeline from the outset.

Frequently Asked Questions

Does my company qualify for EMI options in 2026?

From 6 April 2026, a company qualifies for EMI if its gross assets do not exceed £120 million, it has fewer than 500 full-time equivalent employees across the group, it is a qualifying trading company, it is independent (not a 51%-owned subsidiary), and its trade does not consist substantially of excluded activities. All conditions must be met at the time each tranche of options is granted.

What are the new EMI gross assets and headcount limits from April 2026?

The gross assets limit has increased from £30 million to £120 million. The employee headcount limit has increased from 250 to 500 full-time equivalent employees. Both changes take effect for options granted on or after 6 April 2026.

How is gross assets calculated for the EMI scheme eligibility test?

Gross assets is the total assets figure from the company's balance sheet, before deducting liabilities. For groups, it is the aggregate gross assets of the issuing company and all of its subsidiaries. The test is applied at the date of each grant of options.

How is the 500 employee limit calculated for EMI from April 2026?

The 500 FTE limit uses full-time equivalent employees across the whole group. Part-time employees are counted on a pro-rata basis. Directors who are employees count. Self-employed consultants and agency workers do not count, provided they are genuinely not employed. The count is taken at the date of each grant.

Do I need HMRC advance assurance before granting EMI options?

Advance assurance is not a legal requirement, but it is strongly advisable where there is any uncertainty about the company's qualifying position, particularly regarding excluded activities or complex group structures. An EMI advance assurance application provides HMRC's confirmation that the company and proposed scheme qualify before any options are committed to employees.

Do the April 2026 changes affect options already granted?

No. Options granted before 6 April 2026 are assessed against the conditions at the time of grant. The new thresholds apply only to options granted on or after 6 April 2026. However, if a company holds an existing scheme and wishes to grant further options, the new limits apply to those new grants.

What other conditions must a company meet for EMI options to qualify?

Beyond the gross assets and headcount tests, the company must be a qualifying trading company with no substantial excluded activities, must be independent, must have only qualifying subsidiaries and must meet the group structure requirements. At the individual level, each employee must meet the working time requirement. The scheme must also stay within the £250,000 per employee and £6 million total outstanding limits (from 6 April 2026), and HMRC must be notified of each grant by 6 July following the end of the tax year in which the grant is made.

Taking the Next Step

The April 2026 changes bring a significant number of growth-stage UK businesses within reach of the EMI scheme for the first time. If your company has previously been excluded by the gross assets or headcount limits, now is the right time to assess whether you qualify under the revised thresholds.

In our experience, the companies best placed to act quickly are those that have already confirmed their trade qualifies and whose group structure is straightforward. For companies with complex preferred share structures, joint ventures or mixed trading activities, a careful legal and tax review of all conditions is essential before any options are granted.

If you would like to discuss whether your company now qualifies, or to understand the process from eligibility review through to HMRC advance assurance and share valuation, please get in touch.