Granting EMI options without first agreeing the share valuation with HMRC is one of the most common and costly mistakes companies make. HMRC's Shares and Assets Valuation (SAV) team exists specifically to assess these values, and in 2025 and 2026 they have become noticeably more aggressive in how they treat the discounts that practitioners apply.

This article explains how the EMI share valuation process works, what SAV is looking for, and how to present a submission that stands up to scrutiny.

What Is an Agreed Market Value for EMI Purposes?

Under the Enterprise Management Incentives regime, the exercise price of an EMI option must be set at or above the agreed market value (AMV) of the underlying ordinary shares at the date of grant. If it is set below the AMV, the option does not qualify for the capital gains treatment that makes EMI attractive. The employee instead faces income tax (and potentially National Insurance) on any gain attributable to the discount at the point of exercise.

The AMV is not simply the last round price. For most private companies, the shares being optioned are ordinary shares, which may sit behind a class of preferred shares held by venture capital or angel investors. The preferred shares typically carry rights (in particular, a liquidation preference) that makes the ordinary shares structurally inferior in economic terms. The AMV must reflect this inferiority.

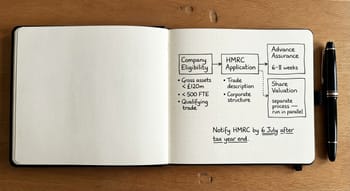

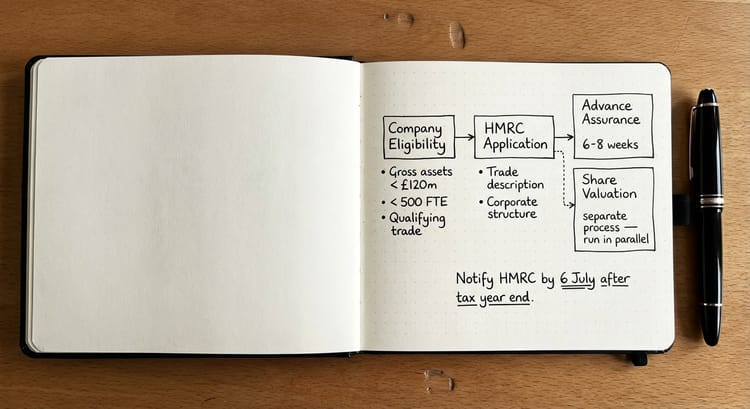

Companies apply to HMRC SAV using the Form Val231 process. Once submitted, SAV issues a letter either accepting the proposed value or inviting discussion. The agreed value is then fixed for a period, typically 90 days, within which the company must grant the options.

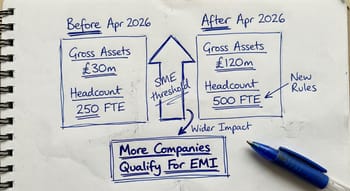

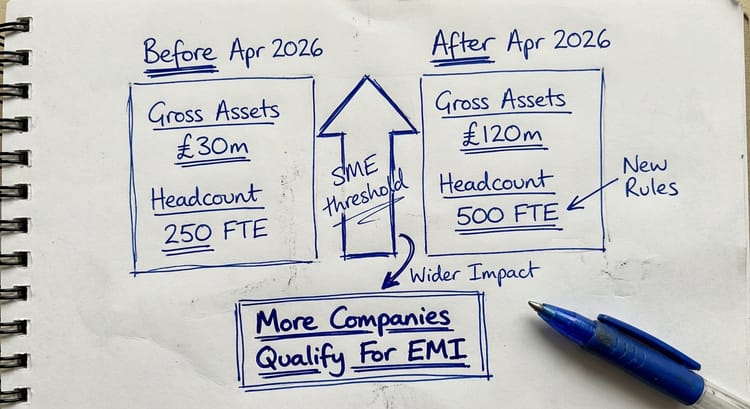

From 6 April 2026, the Finance Bill 2025-26 changes expand EMI eligibility materially. The gross assets limit increases from £30 million to £120 million, and the employee headcount limit rises from 250 to 500 full-time equivalents. This brings a significantly larger pool of VC-backed scale-ups into the scheme, and we expect SAV's workload to increase as a result.

How HMRC SAV Is Currently Approaching Valuations

Based on practitioner experience across the market in 2025 and early 2026, HMRC SAV has tightened its approach in several ways.

- For scale-ups, SAV is treating the most recent investment round price as its default starting point. Officers will ask the submitting party to justify any discount from that price rather than accepting a discounted value on its merits. This shifts the burden of proof in a way that was less marked in earlier years.

- Turnaround times have extended. Submissions on straightforward structures are taking six to eight weeks for an initial response. Complex capital structures, particularly those involving multiple share classes or preference stacks, are routinely taking eight to twelve weeks for an initial response.

- SAV is pushing agreed values higher than expected. Across the market, practitioners are finding that HMRC comes back with values above what the submission proposed, requiring negotiation. Discount levels above 50% are attracting heightened scrutiny, and anything above 75% requires unusually strong factual and mathematical support.

The practical implication is that companies should submit well in advance of their intended grant date and should build a robust technical case from the outset, not in response to a SAV challenge.

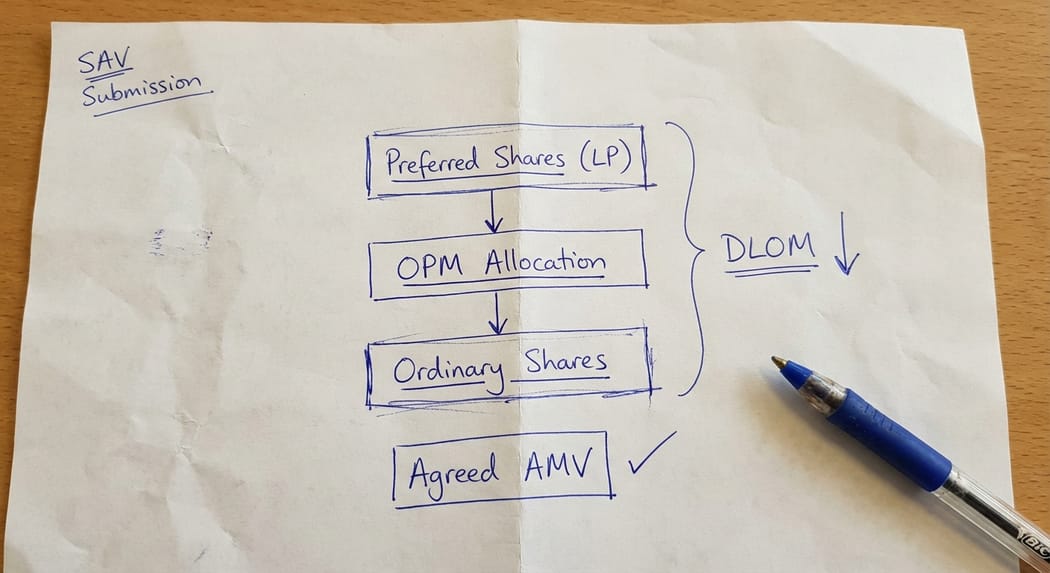

The Discount Framework: OPM, Structural Discount, and DLOM

For companies with a preferred and ordinary share structure, the valuation involves two distinct discount components applied sequentially.

The structural or minority discount reflects the economic inferiority of the ordinary shares. Where investors hold preferred shares with a liquidation preference, the ordinary shares only participate meaningfully in exit proceeds above the liquidation stack. The Option Pricing Model (OPM) quantifies this mathematically, treating each share class as an option over the company's equity value at different strike prices. The OPM allocates value across share classes based on their respective rights at various terminal enterprise values. The result, rather than a judgment call, is a mathematical output driven by the company's Articles, the liquidation preference amount, the time to exit, and the volatility of the company's equity value.

For a company with a 1x non-participating liquidation preference and a small ordinary shareholding, the combined structural and OPM discount commonly falls in the range of 40 to 65 percent from the implied ordinary share value on a notional fully-diluted basis.

The discount for lack of marketability (DLOM) is separate. This reflects the fact that private company shares have no ready market. A hypothetical arm's length buyer would pay less for shares they cannot easily sell. HMRC's own guidance at SVM110050 suggests a DLOM of 20 to 35 percent is appropriate for most private companies, with the level depending on the likely exit horizon and any specific transfer restrictions in the Articles.

These two discounts are applied sequentially, not additively. HMRC SAV's own guidance at SVM110050 gives worked examples of this approach. The DLOM addresses a risk that applies to any private company holding; the structural discount addresses the specific waterfall economics of this capital structure. They are conceptually distinct.

HMRC's SVM110050 Example 6 (Rosalind Ltd) explicitly endorses a "potentially significant discount" for a loss-making development company with a liquidation preference structure, and specifically approves the OPM methodology. This is the practitioner's strongest starting authority.

What HMRC SAV Checks in a Submission

A well-prepared valuation submission should address each of the following areas that SAV commonly examines.

The company's financial position. SAV will look at the most recent accounts, management accounts, and cash burn rate. A company whose enterprise value only marginally exceeds its liquidation preference stack is in a different position to one with substantial equity headroom. SAV is increasingly alert to submissions where the current EV is close to the liquidation preference threshold, because in that zone the preferred shares and ordinary shares have similar economics and the ordinary share discount is harder to justify.

The recency and relevance of the most recent investment round. The more recent the round, the harder it is to argue that the ordinary share value differs materially from the implied value in the round. SAV will use the post-money valuation from the most recent round as its starting reference. If the round was more than twelve months ago, there is more scope to argue that the cash burn and changing market conditions justify a departure from the round price.

The OPM parameters. SAV reviewers (many of whom have RICS valuation backgrounds) will engage on the specific inputs to any OPM model. The key variables are: the enterprise value, the liquidation preference amount, the risk-free rate, the time to exit, and the volatility assumption. Volatility is the most commonly challenged parameter. SAV may suggest a lower figure, which in most LP structures actually reduces the implied ordinary share value, so this challenge can sometimes be accommodated without material harm to the submission.

The DLOM level. SAV will challenge DLOM levels above 35 percent and will expect qualitative support for any level applied (transfer restrictions, absence of a secondary market, specific exit horizon evidence from investor documentation).

Common SAV Challenges and How to Respond

The most frequent objection is that the total discount (structural plus DLOM) is too high. The correct response is not to retreat immediately but to invite SAV to identify which component they consider excessive and to propose a specific parameter change. This reframes the negotiation around objective inputs rather than a global dispute about the final percentage.

Where SAV argues that the current EV is above the inflection point of the liquidation preference, making the preferred and ordinary shares economically equivalent, the response is to explain that the OPM is a probability-weighted model, not a spot calculation. If the company has a monthly cash burn and limited runway without further fundraising, material probability mass exists at enterprise values below inflection. The ordinary shares remain economically subordinate in expectation even if they would rank equally at today's spot valuation.

On case law, HMRC's own guidance at SVM113130 sets out a table of decided cases. Clark v Green (3.16% holding, 70% discount) is the outer boundary from reported decisions and provides useful support when deploying case law in a response letter. However, case law should be reserved for second-round correspondence rather than leading with it in the original submission.

The Agreed Value Process: From Submission to Notification

Once SAV accepts a value, the company has a fixed period (under paragraph 44 of Schedule 5 ITEPA 2003) within which options must be notified to HMRC after grant. Practitioners should build a realistic programme that allows the company to grant options before the agreed value expires.

If SAV does not accept the submitted value, they will issue a response letter proposing a higher figure or asking for further information. The company's agent responds, and a negotiation follows. In our experience, the process typically involves two to three rounds of correspondence before a value is agreed. Having a pre-built concession schedule (a range of parameter adjustments and their resulting AMVs) allows the agent to respond efficiently without needing to re-run the model at each stage.

Finance Bill 2025-26: What Changes from 6 April 2026

The Finance Bill 2025-26 changes two key eligibility thresholds for EMI from the start of the new tax year on 6 April 2026.

- The gross assets limit increases from £30 million to £120 million, and

- the employee headcount limit increases from 250 full-time equivalents to 500.

These changes are significant for scale-up businesses, particularly technology companies and life sciences companies, which frequently crossed the old thresholds before reaching the growth stage at which share options are most commercially useful.

The broader EMI qualifying conditions remain unchanged. Companies must carry on a qualifying trade (broadly, a commercial trade not consisting wholly or mainly of excluded activities), must be independent and must meet the permanent establishment condition. The individual options limits (£250,000 of unexercised options per employee and £3 million total outstanding) also remain unchanged.

For companies that previously fell outside EMI on grounds of size, the position from 6 April 2026 is worth reviewing. Companies that qualify for the first time will need to approach their advisers promptly if they intend to grant options in the 2026-27 tax year, because the SAV valuation process alone takes six to twelve weeks.

Key Takeaway

An EMI option is only as effective as the agreed share valuation that underpins it. A valuation submitted without OPM support, without a clear analysis of the liquidation preference waterfall, or without a properly segmented discount presentation is likely to be challenged by HMRC SAV. The cost of getting this wrong is not a revised valuation; it is an income tax charge on the option holder at exercise.

Frequently Asked Questions

Do I have to agree the EMI share valuation with HMRC before granting options?

You are not legally required to obtain an agreed value in advance, but it is strongly advisable. Without a prior agreement, the exercise price you set may be challenged by HMRC after the event, potentially resulting in an income tax charge on the employee at exercise. Applying to HMRC SAV for an agreed market value before grant eliminates this risk for a defined period.

How long does HMRC SAV take to agree an EMI share valuation?

Based on current experience across the market in 2026, straightforward submissions are receiving an initial response in six to eight weeks. Complex capital structures involving multiple share classes or a liquidation preference stack are typically taking eight to twelve weeks for an initial response, with further rounds of correspondence before agreement is reached. Companies should factor this timeline into their option grant programme.

What discount from the round price should I expect HMRC to accept?

There is no standard answer, because the appropriate discount depends on the specific capital structure, the company's financial position, and the time since the last investment round. For companies with a 1x non-participating liquidation preference and a small ordinary class, combined discounts of 50 to 70 percent from the implied ordinary share round price are generally achievable with a properly documented submission. Discounts above 75 percent require exceptional facts and strong OPM support.

What is the Option Pricing Model and why does HMRC accept it?

The OPM is a method of allocating equity value across different share classes by treating each class as holding a series of financial options at different strike prices. HMRC SAV explicitly endorses the OPM approach in its own guidance at SVM110050, Example 6 (the Rosalind Ltd example).

Can I use the same share valuation for both EMI and growth shares issued to founders?

No. The valuation basis differs between EMI (agreed market value of the share being optioned) and growth shares (market value of the growth share at issue, assessed by reference to its specific rights under the waterfall). Growth shares also involve a separate analysis of whether the issue price meets the unrestricted market value threshold for restricted securities purposes under Part 7 ITEPA 2003.

How do the Finance Bill 2025-26 changes affect EMI eligibility?

From 6 April 2026, the gross assets limit increases from £30 million to £120 million and the employee headcount limit increases from 250 to 500 full-time equivalents. Companies that previously fell outside EMI on grounds of size may now qualify. All other conditions (qualifying trade, independence, permanent establishment, individual option limits) remain unchanged.

What happens if HMRC SAV proposes a higher value than I submitted?

SAV issues a response letter setting out their proposed value and the basis for it. You can accept their proposal, negotiate by providing further information or alternative parameters, or in limited circumstances pursue an internal review. In practice, most submissions are resolved by negotiation rather than formal dispute. Having a concession schedule prepared before submission allows you to respond efficiently to SAV's counter-proposal without starting the analysis from scratch.

Working with IP Tax Solutions on EMI Valuations

EMI share valuation is a technical area where the quality of the submission directly determines the tax outcome for your employees. A poorly supported submission is challenged; a well-constructed one is accepted, usually with minor adjustments.

At IP Tax Solutions, we handle the full process: capital structure analysis, OPM modelling, preparation of the valuation report and cover letter to HMRC SAV and negotiation of the agreed value if SAV challenges the submission. We also coordinate with your company solicitors on the option documentation to ensure the granted options reflect the agreed terms.

If you are planning an EMI option grant, or if your company has recently become eligible following the Finance Bill 2025-26 changes, please contact us to discuss the valuation process and timescales.