If HMRC has raised a fraud allegation against your R&D tax credit claim, you are facing something far more serious than a standard compliance check. A fraud allegation can expose the company to penalties of up to 200% of the underpaid tax, personal liability for directors and in extreme cases a criminal referral. The first step is to understand exactly what HMRC means by "fraud" and to appoint a specialist immediately.

Table of Contents

- What does HMRC mean by "fraud" in an R&D claim?

- How does a fraud allegation differ from a standard R&D enquiry?

- What powers does HMRC have when it suspects R&D fraud?

- What are the penalties if HMRC proves fraud in an R&D claim?

- Does a claim prepared by a third party protect you?

- How do you defend an HMRC fraud allegation on an R&D claim?

- When should you appoint a specialist?

- Frequently asked questions

What does HMRC mean by "fraud" in an R&D claim?

The word "fraud" is used loosely in practice, and the first thing I tell clients is to understand precisely what HMRC is alleging before responding to anything.

In a technical sense, HMRC uses the concept of fraud in two distinct ways in the R&D context. The first is the civil concept: a "deliberate inaccuracy" under Schedule 24 Finance Act 2007. This means that a company (or its adviser) made a false entry in the tax return knowing it was false, or was reckless as to whether it was false. The second, rarer meaning is a criminal allegation: that the company has committed fraud by false representation, typically contrary to the Fraud Act 2006.

The majority of what HMRC calls "fraud" in R&D claims falls into the civil category. A company may have claimed relief for activities that were not qualifying R&D under s.1138 CTA 2010 and the DSIT Guidelines, and HMRC's view is that this was done deliberately rather than through honest error. This distinction matters enormously because civil and criminal routes carry different powers, different burdens of proof and very different consequences.

For comprehensive guidance on R&D tax credit defence more generally, see my overview at R&D tax credit defence.

How does a fraud allegation differ from a standard R&D enquiry?

A standard R&D compliance check, opened under the enquiry provisions in Schedule 18 Finance Act 1998, is a factual review. HMRC asks questions about the technical activities, the qualifying costs and the methodology behind the claim. It is adversarial in tone but it is a civil process with clear procedural rules.

A fraud allegation is categorically different. When HMRC believes fraud may be involved, the case is typically referred to the Fraud Investigation Service (FIS), a specialist unit within HMRC that operates separately from the standard compliance teams. FIS has wider investigative powers and the ability to use Code of Practice 9 (COP9), which is HMRC's civil investigation of fraud procedure.

Under COP9, a company is given the opportunity to make a full and complete disclosure through the Contractual Disclosure Facility (CDF). Accepting the CDF means admitting deliberate wrongdoing in exchange for civil (rather than criminal) treatment. Rejecting the CDF, or failing to disclose fully, risks a criminal investigation.

If you have received a letter that refers to COP9 or the CDF, or that uses the phrase "suspected fraud", the normal process for how to respond to an HMRC R&D enquiry letter does not apply. You need specialist representation before responding to anything. See my guide on how to respond to an HMRC R&D enquiry letter for the standard enquiry process, but note that a COP9 referral is a separate and more serious matter entirely.

What powers does HMRC have when it suspects R&D fraud?

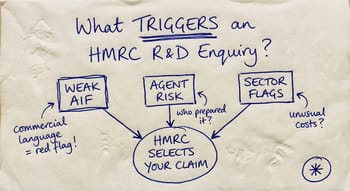

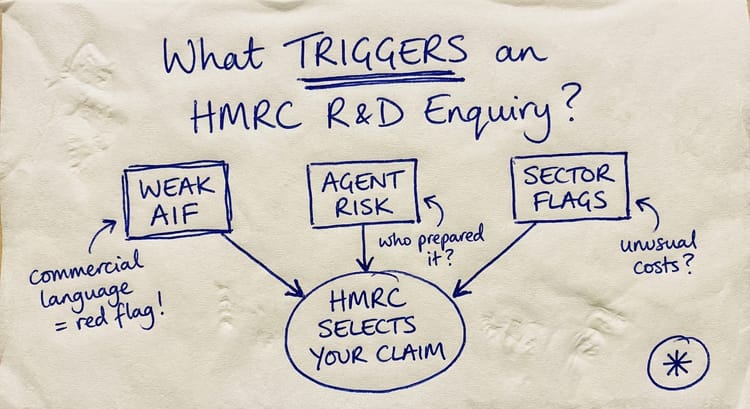

Understanding what triggers an HMRC R&D enquiry helps explain how a fraud case develops. In a fraud case, the investigative toolset is considerably wider.

Under a civil COP9 investigation, HMRC can:

- Issue formal information notices under Schedule 36 Finance Act 2008, requiring the production of documents and information with no right of appeal in most cases

- Apply for third-party information notices, allowing HMRC to approach banks, clients, or suppliers directly

- Inspect business premises, with or without notice, under appropriate authorisations

- Assess tax outside the normal four-year window: where deliberate behaviour is alleged, HMRC can go back 20 years (Schedule 18 FA 1998, paragraph 46, applying the extended time limit for deliberate conduct)

In criminal cases, powers extend further to include search warrants, arrest, and seizure of material under the Police and Criminal Evidence Act 1984 (as applied to HMRC).

The 20-year assessment window is the aspect that most clients find alarming. A company that has been claiming R&D relief for several years using the same methodology could theoretically face assessments covering every claim made since incorporation if HMRC characterises the behaviour as deliberate.

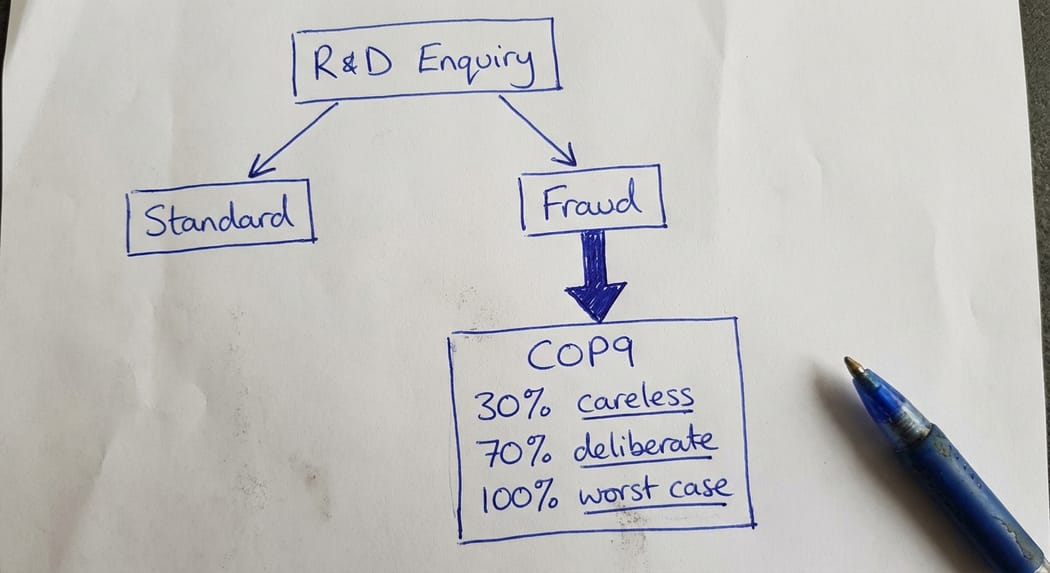

What are the penalties if HMRC proves fraud in an R&D claim?

The penalty regime under Schedule 24 Finance Act 2007 operates on a sliding scale based on the quality of the taxpayer's behaviour:

- Careless inaccuracy: 30% of the potential lost revenue, reduced to 0% where the taxpayer has taken reasonable care

- Deliberate inaccuracy: 70% of the potential lost revenue

- Deliberate and concealed inaccuracy: 100% of the potential lost revenue (Offshore: enhanced ranges by category, with Category 3 deliberate & concealed up to 200%.)

In addition to penalties, HMRC will seek repayment of the tax credits received, with interest running from the date of payment. For a company that received, say, £300,000 in payable R&D tax credits over three years of claims, the exposure can include the full repayment of those credits, a penalty of up to £210,000 on top, and interest. The total liability in serious cases can easily exceed the original benefit of the scheme.

The H&H Scaffolding Ltd case (TC09082, February 2024) provides useful guidance here. The Tribunal found that when HMRC determines an R&D claim does not qualify, that finding does not automatically mean the company has been careless. The company had taken reasonable care and the Tribunal declined to uphold the inaccuracy penalty. This is an important precedent: even where a claim fails on technical grounds, penalty exposure is a separate question that turns on the specific facts.

Does a claim prepared by a third party protect you?

This is one of the most common questions I receive, and the honest answer is: only partially, and less than most directors assume.

The HMRC Guidelines for Compliance (GfC3, published 31 October 2023 and updated 23 January 2025) are explicit on this point. HMRC states that the facts of an R&D claim always remain the company's responsibility, even where a professional adviser has been engaged. Only the business fully understands the work that was undertaken. A company cannot simply point to its agent and absolve itself of responsibility.

That said, the involvement of a professional adviser is relevant to the penalty assessment. A company that took reasonable steps to engage a qualified adviser, provided accurate information to that adviser, and reviewed the claim before submission is in a significantly stronger position than one that signed whatever was put in front of it. The question is whether the company discharged its own duty of care, not whether it delegated the preparation.

The proliferation of volume R&D claim factories between 2019 and 2023 has created a specific category of cases: companies that were cold-called, provided minimal information, and received exaggerated claims they did not fully understand. HMRC is pursuing these cases aggressively. If your claim was prepared by a firm you now have doubts about, get a specialist review before HMRC makes contact.

How do you defend an HMRC fraud allegation on an R&D claim?

The single most important thing you can do is appoint a specialist before making any response. Anything said to HMRC in the early stages of a fraud investigation can be used against you.

An effective defence in a fraud allegation has several components.

The first is an immediate technical review of the claim. This means going back to the underlying activities and asking whether they genuinely satisfied the DSIT Guidelines: was there a scientific or technological advance sought, was there a genuine technical uncertainty, and did the company's activities seek to resolve it? This is not a paper exercise. I need to speak with the people who actually did the work.

The second is a review of the documentation trail. What records existed at the time of the claim? What was submitted on the Additional Information Form? What instructions were given to the agent, and what did the agent actually record? Contemporaneous documentation is the single most powerful tool in an R&D fraud defence.

The third is a proper assessment of the penalty exposure. Not every technical failure represents deliberate behaviour. The Get Onbord Limited case (TC09238, July 2024) confirms that the burden of proof shifts depending on who has presented the stronger evidential base. Where a company can demonstrate it acted in good faith and took reasonable care, the penalty position can be significantly mitigated.

If a COP9 offer has been made, the decision whether to accept the Contractual Disclosure Facility is one of the most consequential decisions in the entire process. I would never advise accepting or rejecting the CDF without specialist input on the specific facts.

When should you appoint a specialist?

If any of the following apply, the matter has moved beyond what an in-house finance team or general practice accountant should handle:

- HMRC has used the words "fraud", "deliberate", or "suspected fraud" in any correspondence

- The case has been referred to the Fraud Investigation Service

- You have received a COP9 letter

- HMRC has made a discovery assessment going back more than four years

- Criminal investigators have made contact

The earlier a specialist is involved, the more options remain open. Once a response has been filed, a position has been taken, or an offer accepted, the room to manoeuvre is considerably reduced.

I have represented clients in R&D fraud allegations through to successful resolution, including defending a £200,000-plus claim against HMRC's fraud allegations. The outcome in each case has depended not on the size of the claim or the strength of HMRC's opening position, but on the quality of the technical and procedural defence put together from the outset.

If HMRC has raised a fraud allegation on your R&D claim, or if you are concerned about a claim made in previous years, contact me to discuss the specific facts.

Frequently asked questions

Has HMRC alleged fraud in my R&D claim, or just opened an enquiry?

The distinction matters and is not always clear from the correspondence. An enquiry letter opening under Schedule 18 FA 1998 is a standard compliance check. A COP9 letter is a fraud investigation. If HMRC's correspondence uses words like "suspected fraud", "deliberate", or refers to Code of Practice 9, you are in a fraud investigation. If the language is simply about "checking your claim" or "verifying information", you are more likely in a standard enquiry. When in doubt, instruct a specialist to review the correspondence before responding.

Can HMRC pursue directors personally for an R&D fraud allegation?

Yes. Where HMRC alleges that a director personally made or authorised a deliberate inaccuracy, HMRC can seek a Personal Liability Notice under Schedule 24 FA 2007 to transfer the penalty liability from the company to the individual. This is relatively uncommon but is used in the most serious cases, particularly where the company is unable to pay. Directors in companies under investigation should consider whether they need separate legal advice from the company's adviser.

How long does an HMRC R&D fraud investigation take?

Civil fraud investigations under COP9 typically take between 18 months and four years from the opening letter to a final settlement. The timeline depends on the complexity of the claim, the amount of documentation to review, and whether the matter progresses to the Tax Tribunal. Criminal investigations take longer still. This is not a process that resolves quickly, which is why early specialist involvement is so important.

What is the difference between an inaccuracy penalty and an HMRC fraud allegation in R&D?

An inaccuracy penalty under Schedule 24 FA 2007 is a civil penalty for a false entry in a tax return. The penalty rate depends on whether the behaviour was careless (30%), deliberate (70%), or deliberate and concealed (100%). An HMRC fraud allegation is the assertion that the inaccuracy was deliberate, meaning the higher penalty bands apply. In practice, when HMRC uses the word "fraud" in relation to an R&D claim, it typically means it is asserting a deliberate inaccuracy rather than making a criminal allegation, though the matter can escalate.

If my R&D claim was prepared by a specialist firm that has since closed, am I protected?

No. The company remains responsible for the accuracy of its tax return regardless of whether the adviser still exists. The closure of an agent does not transfer liability back to the agent or extinguish it. It does, however, affect the evidence available for a penalty mitigation argument. If the agent has gone into liquidation, you should preserve any correspondence and documentation you hold and seek specialist advice on reconstructing the technical case from the company's own records.

Can a fraud allegation on an R&D claim be appealed to the Tax Tribunal?

Yes. If HMRC issues a closure notice reducing or disallowing a claim, and imposes penalties, both the quantum of the reduction and the penalty can be appealed to the First-tier Tax Tribunal. The Tribunal is independent of HMRC and applies the law without deference to HMRC's position. Tribunal appeals in fraud cases are more complex than standard R&D appeals because penalty behaviour is a separate question from technical eligibility, and both issues may need to be addressed. Specialist representation is essential.

What to do next

If HMRC has raised a fraud allegation against your R&D tax credit claim, or if you have received a COP9 letter or a request from the Fraud Investigation Service, contact me to discuss the position.

The earlier I am involved, the better the outcome is likely to be.

Contact IP Tax Solutions to discuss your situation in confidence.