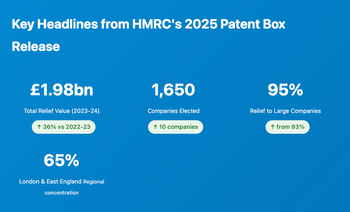

Executive Summary: The Great R&D Consolidation

HMRC's September 2025 R&D tax credit statistics reveal a fundamental restructuring of UK innovation support. This is the first complete tax year reflecting the April 2023 reforms - reduced SME rates, enhanced RDEC rates and mandatory Additional Information Forms for all claims.

🔑 The Defining Moment: RDEC Overtakes SME

For the first time in the scheme's history, RDEC relief (£4.41bn, up 36%) has surpassed SME scheme relief (£3.15bn, down 29%). This £1.26bn gap represents not growth, but consolidation - claim volumes have collapsed 26% while total relief remains flat. The remaining claims are 33% larger on average and concentrated amongst companies with robust compliance infrastructures.

The statistics tell two parallel stories: a compliance victory for HMRC, with fraudulent and erroneous claims substantially reduced, and an accessibility crisis for SMEs and first-time innovators who are being systematically priced out of the system.

The Numbers in Detail: Unpacking the £7.6bn

Total relief has remained remarkably stable at £7.6bn (down just 2% from £7.7bn), but this headline figure masks dramatic underlying shifts. The composition of relief has fundamentally changed, with RDEC now accounting for 58% of total relief compared to 42% just two years ago.

| Tax Year | SME Relief (£m) | RDEC Relief (£m) | Total Relief (£m) | Total Claims | Avg Claim |

|---|---|---|---|---|---|

| 2016-17 | £2,265 | £2,225 | £4,490 | 53,015 | £85k |

| 2017-18 | £2,740 | £2,415 | £5,150 | 62,290 | £83k |

| 2018-19 | £3,510 | £2,800 | £6,310 | 74,535 | £85k |

| 2019-20 | £4,185 | £2,710 | £6,890 | 84,005 | £82k |

| 2020-21 | £4,200 | £2,655 | £6,855 | 87,180 | £79k |

| 2021-22 | £4,620 | £2,980 | £7,600 | 83,220 | £91k |

| 2022-23 | £4,440 | £3,245 | £7,690 | 63,780 | £121k |

| 2023-24 | £3,145 | £4,405 | £7,555 | 46,950 | £161k |

The data reveals three distinct phases:

- 2016-17 to 2020-21: Steady growth in both schemes, with SME relief climbing from £2.3bn to £4.2bn

- 2021-22 to 2022-23: First signs of decline as compliance measures introduced, claims fell 23%

- 2023-24: Full impact of reforms, with SME relief down 29% and RDEC up 36%

SME vs RDEC: The Historic Crossover

SME Scheme: The 31% Collapse

The SME scheme experienced its most severe contraction on record:

- 36,885 claims – down 31% from 53,150 in 2022-23

- £3.15bn relief – down 29% from £4.44bn in 2022-23

- 20,865 credit claims and 16,020 deduction claims

- 3,990 R&D intensive SME claims (11% of SME credits) retaining the 14.5% rate

⚠️ The SME Deterrent Effect

The combination of reduced enhancement rates (from 130% to 86%), lower credit rates (from 14.5% to 10%) and mandatory Additional Information Forms has created what experts call a "compliance cliff." For many smaller innovators, the administrative cost of claiming now exceeds the benefit, effectively pricing them out of the system entirely.

RDEC Scheme: The 36% Surge

The RDEC scheme's growth tells a more complex story:

- 10,065 claims – down 5% from 10,620 in 2022-23

- £4.41bn relief – up 36% from £3.24bn in 2022-23

- £3.61bn from large companies (3,335 claims averaging £1.08m each)

- £795m from SMEs (6,730 claims averaging £118k each)

The RDEC rate increase from 13% to 20% represents a 54% increase in credit value. However, this was partially offset by the Corporation Tax rise to 25%, which reduced net RDEC payouts for profitable companies.

R&D Expenditure: The £46.1bn Reality Check

While relief and claims fell, qualifying R&D expenditure remained remarkably stable at £46.1bn (down just 1%). This critical finding suggests UK companies are still investing heavily in innovation, but access to tax relief has become significantly more challenging.

Critical Finding: The Expenditure-Relief Gap

69% of all qualifying R&D expenditure (£31.6bn) now comes through the RDEC scheme, dominated by large companies and restricted SMEs. This means the majority of UK R&D spend is concentrated in established corporations rather than smaller, high-growth innovators traditionally seen as the engine of breakthrough innovation.

Regional Analysis: The London Effect Intensifies

Regional concentration remains stark and has worsened. Three regions account for 64% of all relief claimed, with London alone capturing nearly one-third of total support.

⚠️ Regional Disparity Crisis

London's average claim of £205k is 156% higher than Wales (£80k) and 138% higher than the North East (£86k). The capital captures 31% of all relief despite representing just 24% of claims. This concentration directly contradicts the government's levelling-up agenda and suggests R&D relief is reinforcing rather than reducing regional economic inequality.

Sector Analysis: Three Industries Dominate

Three sectors continue to dominate the R&D landscape, collectively accounting for 71% of all relief and 72% of all claims.

The Tech SME Squeeze

Information & Communication—traditionally dominated by tech SMEs—saw the steepest decline at -13.8%. This sector historically relied on the SME scheme's generous rates and lighter compliance burden. The reforms have disproportionately impacted software, digital and IT services companies, many of which were claiming smaller amounts (£15k-£50k) that are no longer economically viable.

Cost Band Analysis: The Disappearing Small Claim

The cost band distribution reveals the scheme's dramatic structural shift towards larger claims.

⚠️ The £15,000 Compliance Cliff

Claims under £15,000 have been decimated. Just 7% of total relief now goes to claims under £50k (which represent 61% of all claims), while 43% of relief goes to claims over £1m (just 3% of claims). The smallest 20% of claims by value account for less than 1% of total relief—suggesting many micro-innovators have been priced out entirely.

First-Time Claimants: The Innovation Pipeline Crisis

The decline in first-time applicants represents perhaps the most concerning trend in the data, as it suggests the scheme is failing to attract new innovators - the lifeblood of the UK's innovation ecosystem.

Critical statistics:

- First-time SME applicants fell 45% in 2022-23 to just 7,230

- This is the lowest level since 2013-14

- Represents a 67% collapse from the 2018-19 peak of 21,945

- Four consecutive years of declining first-time applicants

- Just 0.42% of newly registered companies now make first-time R&D claims (vs 2-3% historically)

What This Means for Your Business

The 2023-24 statistics reveal a fundamentally restructured R&D tax credit landscape. Whether you can successfully claim depends increasingly on your size, resources and ability to navigate complex compliance requirements.

For SMEs: Navigate Carefully or Miss Out

Key Takeaways:

- Compliance is non-negotiable: Expect to invest significantly in professional support for a compliant claim

- Claims under £20,000 may not be viable: Calculate whether the net benefit justifies the cost and risk

- Document everything: Start contemporaneous record-keeping from day one of your R&D project

- Check R&D intensity: If loss-making with R&D ≥30% of spend (from April 2024), you may qualify for ERIS at 27%

- Don't miss advance notification: First-time claimants must notify HMRC within 6 months of period end

Should SMEs Still Claim?

Absolutely - if you're doing genuine R&D and can prepare a compliant claim. The support remains substantial:

- Merged scheme (from April 2024): £20 credit per £100 R&D spend

- ERIS (from April 2024): £27 credit per £100 R&D spend

For a company spending £500,000 on qualifying R&D, that's £100,000 (merged scheme) or £135,000 (ERIS) in tax relief—still highly significant.

Need Expert Guidance on R&D Tax Credits?

The data shows successful claims now require strategic planning and expert compliance support. We help established companies investing £500k+ in R&D maximise relief whilst minimising enquiry risk.

Our approach: Partner-led service (work directly with Steve Livingston LLB FCA) • Former Big 4 expertise without bureaucracy • Strategic multi-year planning, not one-off claims

Book Your R&D Strategy ConsultationConclusion: A Watershed Moment for UK R&D Support

The 2023-24 statistics mark a fundamental inflection point for R&D tax credits. The scheme has successfully reduced fraud and error, consolidated support amongst larger claimants and maintained total relief at £7.6bn. But this success comes at a cost: 26% fewer companies claiming, first-time applicants at decade lows, and systematic exclusion of smaller innovators.

The Three-Speed System

R&D tax credits now effectively operate at three speeds:

- High speed: Large companies and well-resourced SMEs with compliance infrastructure - thriving under enhanced RDEC rates

- Medium speed: Established SMEs with substantial R&D budgets (£100k+) - surviving but facing higher barriers

- Stalled: Micro-innovators, start-ups and first-time claimants - increasingly priced out by compliance costs

The merged scheme and ERIS (from April 2024) may address some concerns. The lower 30% ERIS threshold could support thousands more R&D-intensive start-ups. But unless compliance costs fall or support mechanisms improve for smaller claimants, the scheme risks becoming a support system for established innovation rather than a catalyst for breakthrough discoveries.

Data Source: All statistics from HMRC's official "Research and Development Tax Credits Statistics: September 2025" publication covering tax year 2023-24. Figures for 2023-24 are provisional and uplifted to account for late claims.

About the Author: Steve Livingston LLB FCA is a UK Chartered Accountant with 20+ years' experience advising high-growth companies on innovation tax relief. He previously held senior roles at KPMG and was a tax partner at Crowe UK before founding IP Tax Solutions in 2012.

© 2025 IP Tax Solutions Ltd | iptaxsolutions.co.uk