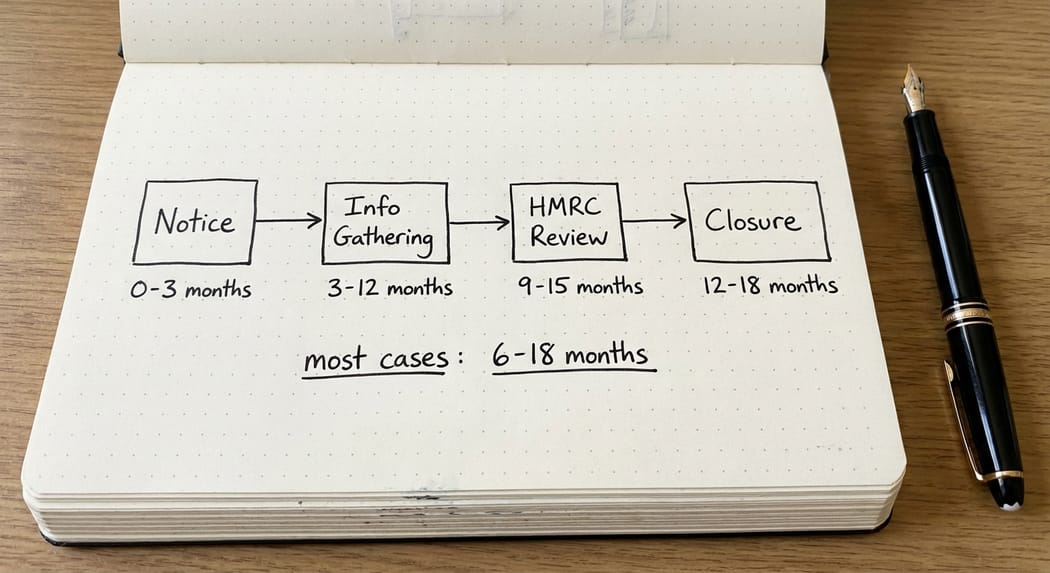

Most HMRC R&D tax credit enquiries run for 6 to 18 months from notice letter to closure. The timeline depends on claim complexity, how quickly you provide information, and whether HMRC finds issues that need deeper investigation. Understanding each stage helps you plan resources and manage stakeholder expectations.

Table of Contents

- Understanding the overall timeline

- Stage 1: Notice and Initial Response (Months 0-3)

- Stage 2: Information Gathering (Months 3-12)

- Stage 3: Closure and Settlement (Months 12+)

- What lengthens an enquiry

- What speeds it up

- Frequently Asked Questions

- When specialist input matters

Understanding the Overall Timeline

HMRC begins an enquiry by sending a notice letter. The clock starts there. From that moment to a final closure notice, you should expect between 6 and 18 months. Some cases close in under 6 months if they are straightforward and your documentation is complete. Others can run 2+ years if they are complex or if HMRC identifies potential fraud.

In our experience defending R&D enquiries, the single biggest variable is not the claim size but the quality of your original documentation. If your advisor prepared a thorough technical narrative with strong evidential backing and project timelines, the enquiry typically runs 6-18 months. If the claim was submitted without narrative or with vague descriptions of work, HMRC needs to dig deeper and the timeline stretches to 2+ years.

Stage 1: Notice and Initial Response (Months 0-3)

HMRC sends you a notice letter under Schedule 18, Finance Act 1998 (which governs enquiries into company tax returns). This letter does three things: it specifies the relevant accounting periods under enquiry, it tells you the deadline to respond (usually 30 days), and it tells you what information HMRC wants first.

HMRC issues what's called an information request (sometimes informally referred to as an additional information request). This is a list of specific questions or documents HMRC needs: technical specifications, project meeting minutes, cost allocations, evidence of novel technical uncertainty, subcontractor invoices or code samples etc.

Your response in these first 30-60 days is critical. If you push back on the scope or ask for extensions repeatedly, HMRC will view you as uncooperative. The enquiry timeline starts to stretch.

Instead, within 30 days, send HMRC a substantive response covering at least: the business context of your R&D work, a list of the qualifying projects, the names of the staff involved, and a timeline of work. Do not send everything you have. Send a structured, indexed bundle with a covering letter from your adviser.

After you respond, HMRC typically needs 30+ days to review your first submission and identify what else they need. That brings us to months 2-3 of the enquiry.

Stage 2: Information Gathering (Months 3-12)

This stage typically includes one or two rounds of information requests. HMRC sends one, you respond. HMRC sends a follow-up with clarification questions. This back-and-forth usually takes 3-12 months total.

The speed of your responses matters. If you take 30 days to answer every question, the enquiry stretches. If you ask for extensions, the enquiry stretches further.

If HMRC is satisfied, they issue a closure notice. You retain the relief. This happens at the fast end of a typical enquiry (3-12 months total).

If matters reach a dead-lock, it can be helpful to request a call with HMRC and the competent professionals from the claimant company. This can help overcome any misunderstandings and help accelerate matters. It can be the case that HMRC isn't willing to attend meetings, preferring to rely on written correspondence.

Stage 3: Closure and Settlement (Months 12+)

A closure notice under Schedule 18, Finance Act 1998 ends the enquiry. HMRC either:

- Accepts your claim in full (no change to the relief claimed)

- Accepts it in part (reduces the relief, you pay back some amount plus interest (and penalties))

- Rejects it (no relief, you repay everything plus interest and penalties)

After the closure notice, you have 30 days to appeal if you disagree. If you do appeal, the dispute typically moves to a Solicitors Office and Legal Services (SOLS) review.

If the SOLs review is unsuccessful, the next step is an appeal to the First Tier Tribunal (Tax Chamber), where proceedings can take a further 24 months+. But this is outside the HMRC enquiry timeline - the enquiry itself is closed.

What Lengthens an HMRC R&D Enquiry

Several factors reliably extend the timeline:

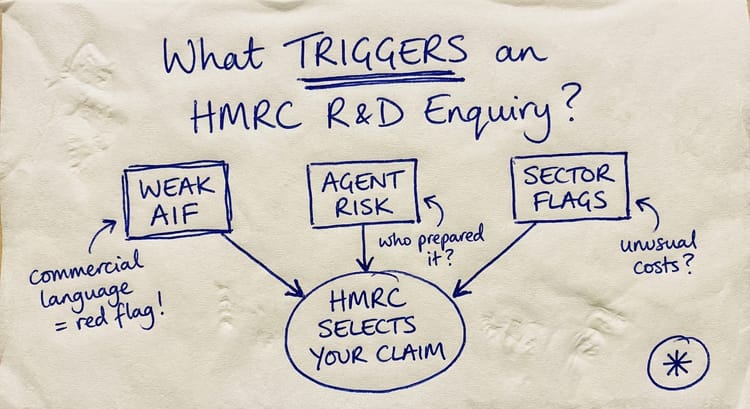

Missing or weak technical narrative. If your original claim had no technical narrative, or a vague one, HMRC needs to build one for you through questions.

Subcontracted R&D. If you subcontracted part of your R&D (to another company or to a freelancer), HMRC wants to verify the subcontractor's status and the nature of work. If the subcontract was not clearly documented, this becomes a stumbling block.

Overseas costs or team members. If you claimed costs for overseas development work, or if part of your team was based abroad, HMRC needs to verify that the qualifying activities were actually performed by your UK company or a connected company.

Staff turnover. If the people who did the work have left your company, HMRC cannot interview them directly. You then need contemporaneous documentation (emails, git commits, technical notes) to prove the work happened. If this documentation is incomplete, the enquiry stalls while you hunt for evidence.

System unavailability. If your original code repositories, project management systems, or email archives are no longer accessible, HMRC will want alternative proof (consultant reports, technical reviewers' notes, published patents or products). Gathering this takes time.

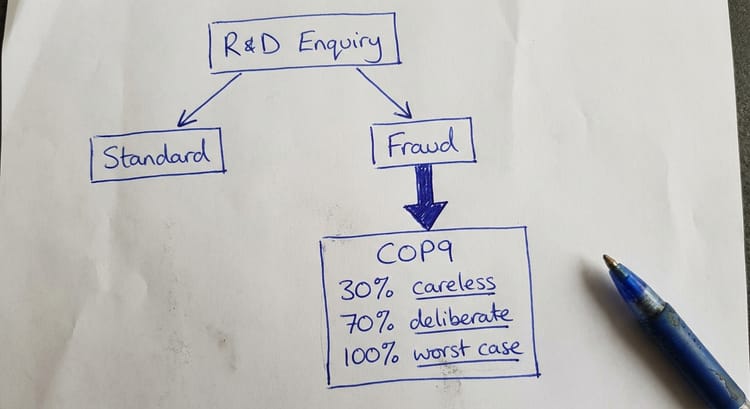

Suspected fraud. If HMRC identifies inconsistencies or what they perceive as deliberate misstatement, they may escalate the case to the Criminal Investigation Team or to Fraud Compliance. This can delay closure by 12-24+ months while the investigation runs in parallel.

What Speeds Up an HMRC R&D Enquiry

Conversely, these factors pull the timeline in:

Complete technical narrative in the original claim. If your claim included a well-written technical narrative explaining the novel technical uncertainties you faced, HMRC can verify your claim more quickly.

Clear cost allocation records. If you have timesheets, project timesheets, or clear cost allocation spreadsheets showing which staff worked on which qualifying projects, HMRC moves fast.

Cooperative approach from day one. If you appoint an adviser early (not after you receive the enquiry notice), and the adviser responds promptly to every question, HMRC perceives cooperation and moves forward.

Straightforward business model. If your R&D work is in-house development or process improvement with no subcontracting and no overseas costs, HMRC's review is simpler.

Expert defence from an experienced adviser. This is important: if you instruct an R&D specialist early, they can prepare your case professionally and challenge weak claims proactively. In our experience, a specialist adviser can save months on average because HMRC respects a structured, evidence-backed defence and doesn't need to ask as many follow-up questions.

Frequently Asked Questions

Can I speed up an HMRC enquiry by offering to repay some of the relief?

Technically yes, but it is not advisable. If you concede part of your claim to close the enquiry, HMRC will still issue a formal closure notice on the amount you accepted, and seek to apply penalties. The better approach is to defend your claim properly or, if you genuinely made an error, to correct it through a voluntary disclosure before the enquiry closes.

What happens if I miss a deadline to respond to HMRC?

HMRC can issue a formal information notice (under Schedule 36, Finance Act 2008) requiring a response within a set period. If you miss that deadline, HMRC can issue a closure notice on the basis of the information they have, which usually means they reject or heavily reduce your claim. Missing HMRC deadlines materially worsens your position. Ensure your adviser tracks deadlines diligently.

Can an HMRC enquiry be opened beyond the standard 12 month window?

For most claims, HMRC has a 12 month window to open an enquiry (from the date the claim was filed, longer if filed via an amended return). However, once an enquiry is open, there is no statutory time limit on how long HMRC can take to close it. HMRC can extend this 12 month period to 4 years if there is a "discovery assessment" and longer if there is fraud.

If HMRC finds no fault, do I still need to pay interest?

No. If HMRC closes the enquiry and confirms that your claim was correct, you owe no additional interest. Interest only runs on understatements. However, if HMRC identifies an understatement (i.e., you claimed too much relief), they assess interest from the original self-assessment due date to the date of the closure notice.

What if I receive a second enquiry notice on a different claim year?

HMRC can open separate enquiries into different years. If you received an enquiry into 2024 and then, while that is ongoing, receive a second enquiry into 2025, they are two separate enquiries. The timeline for each runs independently, though HMRC may want consistent information across both years. This does not automatically extend either enquiry, but it does mean you are managing two parallel processes.

Do I need a specialist if the enquiry is just into year 1 of a claim?

If HMRC has opened an enquiry, you almost certainly benefit from specialist advice. Even a "simple" first-year enquiry is a formal legal proceeding. The documentation you provide, and the tone of your response, set the precedent for how HMRC views subsequent years. Investing in specialist advice in year one typically saves money in years 2-3. A specialist can also review your claim for genuine errors before submitting the full response to HMRC, which can limit the scope of the enquiry.

When Specialist Input Matters

You should instruct an R&D specialist if any of these apply:

- You have received an HMRC enquiry notice and have not yet submitted your initial response

- Your original claim lacked a technical narrative or other key documentation

- HMRC has issued an additional information form and the questions indicate suspicion of fraud or non-qualifying activity

- Your R&D work involved subcontracting, overseas costs, or a complex cost allocation

- HMRC has indicated they may reduce the claim by a material amount, say 20%+

- You disagree with HMRC's assessment of what counts as qualifying activity

In these scenarios, specialist input from someone with HMRC R&D defence experience and track record makes a material difference to the outcome and often shortens the timeline by negotiating a settlement rather than contesting every point.

The average HMRC enquiry will cost you in terms of management time, distraction from your business, and the cost of your accountant's time. A specialist adviser adds cost upfront but typically pays for themselves through either securing more relief or closing the enquiry faster than it would otherwise run.

If you are facing an HMRC R&D enquiry, it is worth getting specialist input early. The timeline is long, and the quality of your defence in the first 6 months shapes the entire outcome. I handle R&D defence cases and HMRC enquiries. If you want to discuss your situation, reach out for a confidential conversation.