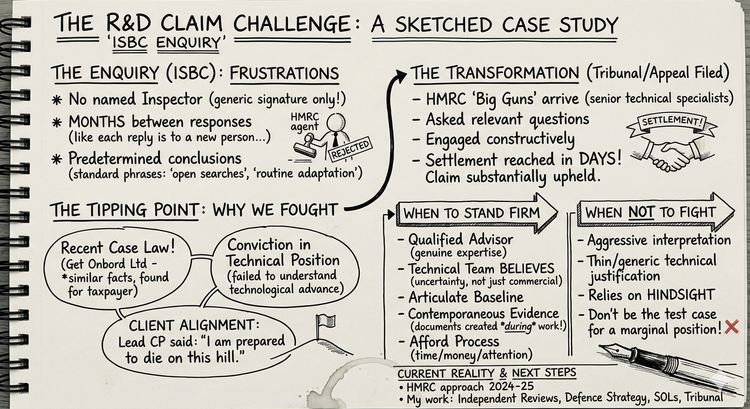

HMRC's compliance programme now subjects a significant proportion of R&D tax credit claims to scrutiny. According to HMRC's published statistics (September 2025), 46,950 claims were filed in 2023/24 - a 26 per cent fall from the previous year. Enquiry selection is no longer random. HMRC uses data analytics, agent risk profiles and the quality of your Additional Information Form to decide which claims to examine. Understanding the triggers is the first step to building a defensible claim.

Contents

- Why HMRC Opens R&D Enquiries

- How HMRC Selects Claims: Risk-Based Profiling

- The Additional Information Form: Your First Line of Risk

- Agent Risk: Who Prepared Your Claim?

- Technical Red Flags in R&D Claims

- Sector-Specific Patterns HMRC Targets

- What Happens Once Your Claim Is Selected?

- Frequently Asked Questions

Why HMRC Opens R&D Enquiries

HMRC's compliance programme for R&D tax credits has changed significantly since 2022. The mass-letter period, where HMRC wrote simultaneously to thousands of SME claimants, has given way to something more targeted and, in some respects, more consequential: data-driven, risk-based selection.

The figures from 2023/24 are instructive. According to HMRC's R&D Tax Credits Statistics (September 2025), 46,950 claims were filed - a 26% fall from 2022/23, driven largely by a 31% drop in SME scheme claims. HMRC does not publish the number of compliance checks in its September 2025 statistics; some industry commentary estimates around 9,700 checks, implying a rate of roughly 17% to 21%.

The reason HMRC continues to open so many enquiries is straightforward: the agency believes significant non-compliance persists in the system, including genuine errors, aggressive interpretations and in some cases fraud. The question for any company or accountant reviewing a claim is not whether HMRC enquiries happen, but whether a particular claim presents the risk signals that draw attention?

How HMRC Selects Claims: Risk-Based Profiling

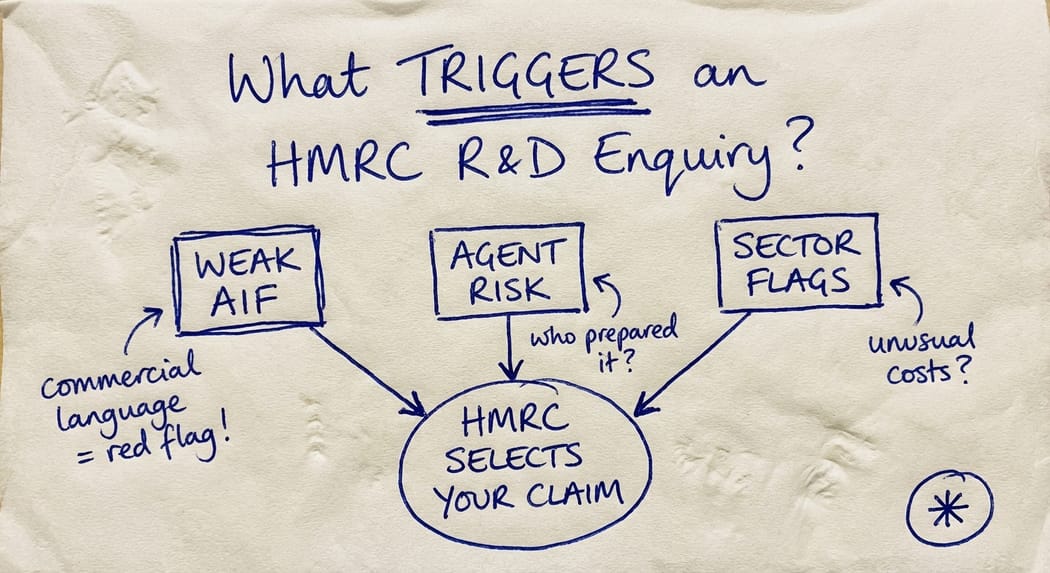

HMRC appears to use a combination of internal risk models, data-matching across its own systems and signals from the Additional Information Form (AIF) to identify which claims warrant closer examination.

Several patterns consistently appear in compliance selection.

First-time claimants attract scrutiny, particularly where the claim value is substantial. A company filing its first R&D claim for a significant sum, without a prior history of innovation activity visible to HMRC, raises an obvious question about why the activity is only appearing now.

Inconsistencies between the AIF and CT600 are a significant trigger. If the narrative in the AIF describes three projects but the expenditure figure in the tax return does not reconcile with the project scope described, HMRC's data-matching systems will flag it. Discrepancies between the AIF, the CT600 and payroll records are identifiable. Ensuring these figures reconcile exactly before submission is a basic but essential step.

Claims that appear disproportionate relative to company size or sector benchmarks also generate risk flags. A company with ten employees claiming that 80 per cent of payroll relates to qualifying R&D will draw scrutiny. HMRC holds sector and size benchmarks. Significant departures from those norms attract attention.

Amended returns that introduce R&D claims are another prompt for examination. HMRC is alert to the pattern of a company filing a standard corporation tax return, then amending it several months later to include a substantial R&D credit, particularly where no prior R&D activity had been declared.

The Additional Information Form: Your First Line of Risk

The AIF has been mandatory for all R&D claims since 8 August 2023. It is the single most important document in HMRC's initial assessment of a claim, and a weak AIF is probably the most common trigger for an enquiry opening.

HMRC's Guidelines for Compliance (GfC3, published October 2023 and updated January 2025) set out in detail what HMRC expects. A competent professional in the relevant field of science or technology should identify the specific scientific or technological advance the project sought to achieve, name the exact uncertainties the project was trying to resolve, and explain why those uncertainties were not readily deducible by a competent professional in the field.

Where the AIF reads as a product description rather than a technical narrative, where it uses commercial language rather than scientific or technological language, or where it fails to clearly distinguish business uncertainty from technological uncertainty, HMRC compliance officers have grounds to open an enquiry.

GfC3 was published precisely to address a persistent gap between what companies and advisers were submitting and what HMRC expected to receive. An AIF that satisfies the five mandatory questions superficially but does not demonstrate genuine technological advance will not withstand scrutiny.

Key takeaway: Treat the AIF as the primary defence document, not as an administrative requirement. The way it is drafted determines whether HMRC reads your claim as low risk or problematic from the outset.

Agent Risk: Who Prepared Your Claim?

This is a trigger that many companies do not anticipate. HMRC tracks which agents are preparing R&D claims and uses this information in its risk models. Agents associated with high volumes of rejected claims, enquiries or complaints see their clients' claims selected at higher rates.

The mandatory registration regime for all tax advisers interacting with HMRC is due to open in May 2026, with a deadline of August 2026 for existing agents. One consequence is a cleaner HMRC map of which agents are active in the R&D market. Agent registration data will, over time, feed into claim risk profiling more systematically.

If your claim was prepared by a volume claim preparer, a firm whose business model involves submitting large numbers of claims with standardised narratives, the risk of enquiry is meaningfully higher. I have represented clients whose claims were prepared by such firms and who found themselves in enquiry with inadequate documentation, poor technical narratives and agents who were unwilling or unable to assist with the defence.

For accountants referring R&D work, the quality and track record of the specialist you use matters not only for the client's outcome but for the risk profile attached to the claims you submit.

Technical Red Flags in R&D Claims

Beyond AIF quality and agent risk, HMRC compliance teams look for specific technical patterns that suggest a claim may be overstated or ineligible.

Broad project boundaries are a persistent problem. Companies often describe a commercial product development programme as the R&D project, when the qualifying activities are a subset of that programme. The DSIT Guidelines (introduced by Statutory Instrument 293 of 2023, applicable to periods beginning after 31 March 2023) are clear on this point: a project should encompass only the activities that serve to resolve scientific or technological uncertainty. The wider commercial project within which those activities sit does not become qualifying R&D simply because some part of it involved genuine uncertainty.

Routine optimisation described as qualifying R&D is another flag. The DSIT Guidelines state that improvements, optimisations, and fine-tuning which do not materially affect the underlying science or technology do not constitute work to resolve scientific or technological uncertainty. HMRC compliance officers are increasingly attentive to narratives that describe iterative software development or engineering refinement without identifying a genuine technical uncertainty that was not readily deducible.

Subcontractor and externally provided worker costs remain a high-scrutiny area, particularly under the merged scheme from April 2024. The question of who is the "decision maker" for the R&D, and whether the R&D has been "contracted out" to the claimant, requires careful analysis. Poor documentation of subcontract arrangements is a frequent trigger.

Overseas R&D costs claimed under the merged scheme require clear evidence that it was wholly unreasonable to perform the work in the UK. HMRC expects a documented analysis, not an assumption.

Sector-Specific Patterns HMRC Targets

Certain sectors consistently appear in HMRC's compliance activity, and this is not coincidental.

Software development claims have been under sustained scrutiny. The boundary between routine software development and genuine technological advance is genuinely difficult to draw in practice. HMRC's GfC3 guidance includes software-specific examples precisely because this is an area of persistent misapplication. A claim that describes agile development sprints without identifying the specific technological uncertainty being resolved is likely to face questions.

Construction and engineering claims have attracted attention where companies describe process improvements without demonstrating that the improvements involved resolving genuinely uncertain technological problems. Applying existing methods in a new context is not qualifying R&D under the DSIT Guidelines, even where the outcome is commercially significant.

Professional services companies claiming R&D credits for software or systems built to deliver their services have also been challenged. HMRC is sceptical where the claimed R&D relates closely to the company's core commercial activity, without a clear argument for why the development involved genuine technological advance rather than standard business system implementation.

If your company operates in any of these sectors, the technical narrative in your AIF needs to be more precise, not less.

What Happens Once Your Claim Is Selected?

Understanding what triggers an enquiry is useful. Understanding what follows is equally important.

HMRC's initial contact is typically a compliance check letter, which is informal and does not constitute a formal enquiry notice under paragraph 24, Schedule 18 FA 1998. The letter will request information and documentation relating to the claim.

How you respond to that first letter sets the tone for the entire process.

A weak or incomplete initial response frequently leads to escalation. HMRC may then raise a formal enquiry, request additional information, and bring in HMRC's own technical specialists to review the R&D activity. At that stage, the scope of the compliance check and the amount at risk can broaden significantly.

For more detail on the process and what to do when you receive a letter about your R&D claim, see my guide to responding to an HMRC R&D tax credit enquiry letter.

If you are considering whether to instruct a specialist, our R&D tax credit defence page explains how we approach these cases and what the process involves.

Frequently Asked Questions

Why did HMRC open an enquiry into my R&D claim?

HMRC selects R&D claims for compliance checks based on a combination of data-matching, risk profiling, and AIF quality assessment. Around 20% of claims are currently selected. Common reasons include: weak technical narratives in the AIF, inconsistencies between the AIF and CT600, first-time or unusually large claims, and claims prepared by agents with a higher risk profile. HMRC does not explain its selection criteria in the enquiry opening letter.

Does receiving an HMRC letter about my R&D claim mean HMRC thinks I have done something wrong?

Not necessarily. HMRC selects claims using risk models that flag patterns, not confirmed errors. A compliance check letter means your claim has been identified for review, not that HMRC has concluded it is incorrect. However, the compliance process is serious and needs to be handled carefully from the outset. Poorly prepared responses can significantly worsen the position.

What triggers an HMRC R&D tax credit enquiry more than anything else?

In my experience, the quality of the Additional Information Form is the single most consistent trigger. A narrative that uses commercial rather than technical language, draws project boundaries too broadly, or fails to identify specific technological uncertainties gives HMRC grounds to challenge the claim. Agent risk, where the claim was prepared by a firm with a poor compliance track record, is the second most significant factor.

Can HMRC open an enquiry into an old R&D claim?

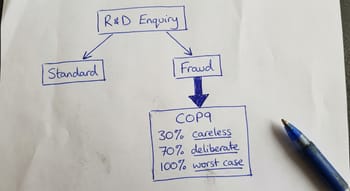

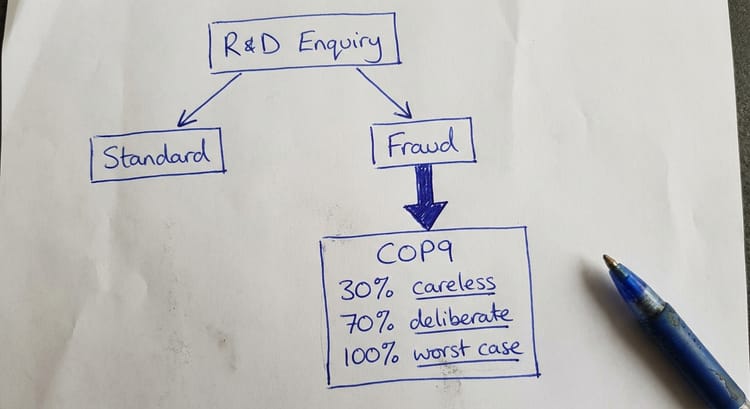

Yes. HMRC can open a formal enquiry within 12 months of the date the return was filed under paragraph 24, Schedule 18 FA 1998 (potentially longer if filed via an amended CT600 return). Where HMRC believes there is a loss of tax, it may issue a discovery assessment: four years from the end of the accounting period for careless error, six years for deliberate error. Claims where HMRC alleges fraud are subject to extended time limits.

How do I reduce the risk of an HMRC R&D enquiry?

The most effective steps are: ensure the AIF contains a technically precise narrative identifying specific scientific or technological advances and uncertainties; ensure the cost schedule reconciles exactly to the CT600 and underlying records; use a specialist with a credible compliance track record rather than a volume claim preparer; and retain contemporaneous technical documentation throughout the R&D process. A claim that is well-evidenced, technically precise, and internally consistent is materially less likely to be selected for examination.

What should I do if HMRC opens an enquiry into my R&D claim?

Take it seriously from the outset. The first response to HMRC often determines how the enquiry develops. If your claim was prepared by a generalist accountant or a volume specialist, consider instructing someone with specific R&D enquiry experience before responding. For claims involving fraud allegations, technical disputes about qualifying activities, or significant amounts, instruct a specialist before sending anything to HMRC.

Is an HMRC compliance check the same as a formal enquiry?

No, though the distinction is not always communicated clearly. A compliance check letter is informal. A formal enquiry opened under paragraph 24, Schedule 18 FA 1998 carries specific procedural rights and obligations on both sides, including the right to request a closure notice. Many R&D cases begin as informal compliance checks and escalate into formal enquiries when the initial response is insufficient. Understanding which you are dealing with is important from the start.

If HMRC Has Selected Your Claim

If HMRC has written to you about your R&D claim, the immediate priority is to understand precisely what the letter asks for and whether there is a legal basis for the information request. HMRC compliance letters vary considerably in scope and formality.

I am a specialist in R&D enquiry defence with 25 years in innovation tax, including training at a Big 4 firm and as a partner at mid-tier firm. I have defended R&D claims, including cases where fraud was alleged and where the original claim had been prepared by a volume specialist. The earlier specialist help is instructed, the more options remain available.

You can reach me at stevelivingston@iptaxsolutions.co.uk or through the contact form on this site.

Steve Livingston FCA is the founder of IP Tax Solutions, a specialist innovation tax advisory firm. He handles R&D tax credit defence, HMRC enquiry response, SEIS/EIS structuring, Patent Box computation and EMI scheme issues.