Alphabet shares are one of the most widely used tools in UK owner-managed business tax planning. They allow different shareholders to receive different levels of dividend income, which can reduce the household's overall tax bill significantly. Used carefully, the structure is legitimate. Used loosely, it attracts HMRC challenge under the settlements legislation, the employment income rules, and in some cases both at once. This guide explains how alphabet shares work, where the legal risks lie, when the Arctic Systems protection applies (and when it does not), and what to consider instead when the structure looks shaky.

What Are Alphabet Shares and Why Are They Used?

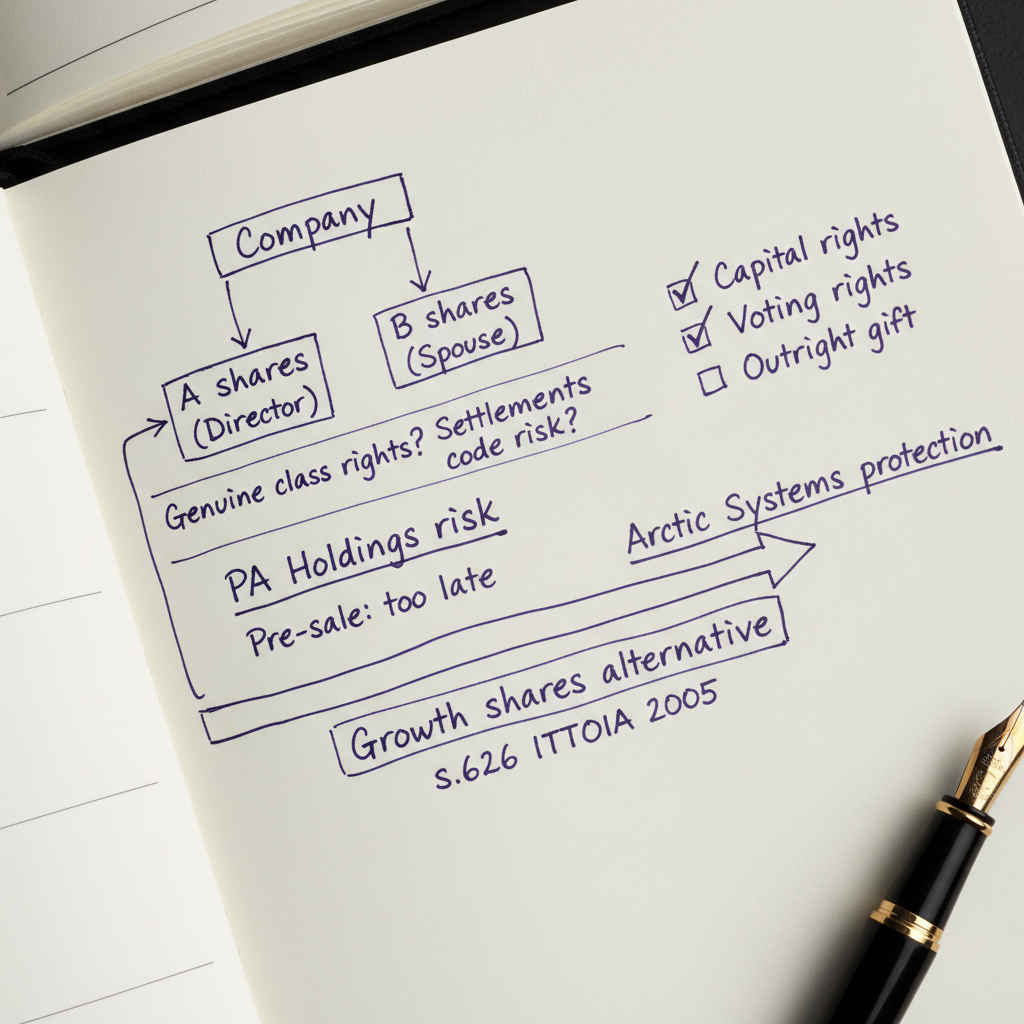

Alphabet shares are separate classes of ordinary shares carrying different rights to dividends. A typical structure has A ordinary shares held by the founder or director, B ordinary shares held by a spouse or civil partner, and C ordinary shares held by a business partner or family member. Each class can receive dividends in different amounts, at different times, or not at all, depending on what the board declares.

The tax appeal is clear. If one shareholder pays income tax at 45% and another pays at 20% (or has unused personal allowance), the same company profit produces a materially smaller combined tax bill if it is distributed to the lower-rate holder. Used in a genuine business context, this is legitimate tax planning. The difficulty arises when the reality of who does the work, who takes the risk, and who the income really belongs to diverges from what the share register suggests.

The Genuine Separate Class Requirement Under Company Law

Before getting to the tax analysis, there is a company law point that is often skipped. Under s.629 of the Companies Act 2006, shares form a class only if the rights attached to them are not in all respects uniform with the rights attached to shares in another class. Alphabet shares must have genuinely different rights baked into the articles of association.

Identical articles with different letter labels do not create separate classes for company law purposes. The articles need to specify the dividend rights that attach to each class: which class can receive a dividend, on whose resolution, in what proportions, and subject to what limitations. A blanket discretion for directors to pay different dividends to different shareholders, without the underlying class rights being properly set out, creates a fragile structure. HMRC has relied on this point in enquiries to argue that the "different" shares are not different at all and that the dividend carries the character of a salary top-up.

The risk is no longer only that loosely labelled shares fail. The High Court in Gu v Whibberley [2025] EWHC 1816 (Ch) considered a shareholder's claim that they had been unfairly treated on dividends paid across alphabet shares, which is exactly the argument that the shares were never genuinely separate classes at all. The case turned on its own facts, but it is a clear warning that even commonly used "pari passu save as to dividends" drafting, where the board simply has discretion over each letter, can be challenged at the company law level. If the class distinction collapses, so does the tax basis for paying different dividends. The practical answer is to have a corporate solicitor draft articles that give each class genuinely distinct rights, not just a different letter and a discretion.

The Settlements Code: Why the Tax Label Is Not the Whole Story

The settlements legislation is in Part 5 Chapter 5 of ITTOIA 2005. Section 620 defines a "settlement" broadly: it includes any disposition, trust, covenant, agreement, arrangement, or transfer of assets. The definition is wide enough to catch a gift of shares between family members, including spouses.

Where a settlement exists, s.624 provides that the income of that settlement is treated as the settlor's income if the settlor retains an interest in the settled property. This is the provision HMRC relies on most often to challenge alphabet share income-splitting arrangements where the underlying value or control over income remains with the director.

The practical problem is this: if a director transfers B shares to their spouse with no real capital or voting rights, simply to divert dividends, HMRC will argue the arrangement is a settlement, the director is the settlor, and the dividend income should be taxed as the director's income rather than the spouse's.

A separate but related risk arises from the PA Holdings litigation (PA Holdings Ltd v HMRC [2011] EWCA Civ 1414). In that case the Court of Appeal held that payments structured as dividends to employees were in substance earnings, subject to income tax and National Insurance as employment income. Where alphabet share dividends are paid in substitution for a salary or bonus, or are closely linked to an individual's personal revenue generation, that characterisation risk is real. The label "dividend" does not override the substance test. If your structure has an HMRC enquiry into your share structure already in progress, the period before any formal exchange of information is the most important time to take specialist advice.

The New Reporting Regime: HMRC Can Now See the Pattern

The biggest practical change for alphabet shares has nothing to do with case law. From the 2025/26 tax year, every director of a close company must disclose extra information on their self-assessment tax return: the company's name and registered number, the amount of dividend income received from it, and the percentage of share capital held. Where the holding changed during the year, the figure reported is the highest percentage held at any point. These rules were brought in by the Income Tax (Additional Information to be included in Returns) Regulations 2025.

This matters because, until now, HMRC could not easily tell whether a director's dividends were proportionate to their shareholding. It can now cross-reference the two. A director who holds a small percentage of the shares but receives a large dividend is exactly the pattern that the settlements legislation is aimed at, and that pattern is now visible on the face of the return. The requirement to report the highest holding during the year also closes off the trick of reducing a holding just before the year end. Combined with the annual employment-related securities return, HMRC has, for the first time, a near-complete picture of how owner-managed businesses are paying their people.

The takeaway is not that alphabet shares no longer work. It is that arrangements where the dividend looks out of step with the shareholding are now far more likely to be picked up. A structure that reflects genuine commercial reality has nothing to fear from better data. A structure that does not is now much more exposed.

When Arctic Systems Protects Spousal Dividend Splitting

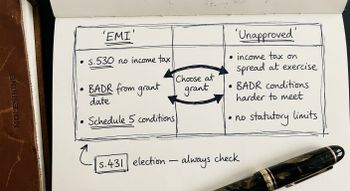

The leading case on spousal alphabet shares is Jones v Garnett [2007] UKHL 35, commonly known as Arctic Systems. The House of Lords held that the arrangement was a settlement under the predecessor legislation, but that the outright gift exception (now in s.626 ITTOIA 2005) applied to protect the wife's dividend income.

The outright gift exception saves income from the settlor charge where one spouse makes an outright gift to the other, provided the gift does not carry a right to income arising from employment or services rendered by the donor. The Arctic Systems protection depends on the shares being real shares with genuine capital rights and voting rights. A share carrying only a right to participate in dividends, with no capital value and no vote, is much more vulnerable to HMRC's argument that it is substantially a right to income from the donor's services.

In our experience, the key facts are: whether the shares have economic substance beyond the dividend stream (capital entitlement on a winding up, voting rights, genuine participation in a sale); whether the spouse paid something for the shares, even a nominal amount; whether the dividend paid to the spouse is grossly disproportionate to any contribution the spouse makes to the business; and whether the pattern of dividend payments tracks the director's personal revenue almost exactly.

The Arctic Systems protection is real and available to the right structure. It is not a blanket cover for any arrangement framed as a spousal dividend split. The facts matter, and HMRC applies a realistic, substance-over-form approach.

School Fees Planning via Grandparent Settlements

A related application of the alphabet share structure is grandparent school fees planning. The model involves grandparents subscribing for shares in a family company with their own capital, receiving dividends from those shares, and using those dividends to fund grandchildren's school fees.

HMRC's Spotlight 62, published in June 2023, targets arrangements where the return on the grandparent's shares is grossly disproportionate to the subscription price, or where the arrangement is structured so that the income effectively flows to a minor child. HMRC's stated view is that the scheme does not work, on the basis that the parent or company owner is the effective settlor and the grandparent is acting as a conduit. Where the grandparent has used their own capital, subscribed at a proper price reflecting the shares' value, and receives a proportionate return on that investment, the structure is more defensible. Where the capital is effectively lent, cycled back, or the subscription price bears no relation to market value, HMRC will argue the arrangement is a settlement by the working family member and tax the income accordingly.

The minor children rule under s.629 ITTOIA 2005 adds another layer: income of a settlement paid to an unmarried minor child of the settlor is taxed as the settlor's income. This catches arrangements where parents use a grandparent vehicle to route income to their own children, and the grandparent is acting as a conduit rather than a genuine investor.

The ERS Overlay in Employment Contexts

Where alphabet shares are issued in an employment context, the Employment-Related Securities (ERS) regime under Part 7 ITEPA 2003 applies. Following the Supreme Court's decision in HMRC v Vermilion Holdings Ltd [2023] UKSC 37, the ERS deeming provisions are a bright-line rule. If a person is an employee (or will become one), and securities are acquired in circumstances connected with that employment, the ERS regime applies regardless of the actual facts.

The practical consequence: where a director or employee receives shares in a company that employs them, any under-value acquisition of those shares is an employment income event. The characterisation of subsequent dividends under the settlements code is a separate, additional question. Both the ERS charge on acquisition and the settlements charge on income can apply simultaneously, and often do.

The settlements code and the ERS regime are independent charging provisions. An alphabet share structure that escapes one can still be caught by the other. The analysis must cover both before the shares are issued, not after HMRC raises the question.

The Pre-Sale Gifting Trap

One of the most significant errors in practice is gifting alphabet shares to a family member while a sale of the business is being discussed. In that situation, the shares are likely to be "readily convertible assets" under the employment income rules, meaning any discount from market value on the transfer triggers PAYE and National Insurance rather than a CGT charge.

More fundamentally, once heads of terms are signed (and arguably before, if a sale is actively in contemplation), the minority discount that would ordinarily apply to a small holding collapses. A notional purchaser knows the company is about to be sold at a known price. The timing of any gift must be well ahead of any sale process, when the minority discount is real and the readily convertible asset provisions have not been engaged.

What to Do Instead

Alphabet shares are not always wrong. A carefully structured arrangement with genuinely different class rights, proper articles, a spouse or civil partner with real economic exposure to the shares, and dividend levels that reflect commercial reality, can be defensible under Arctic Systems and the outright gift exception.

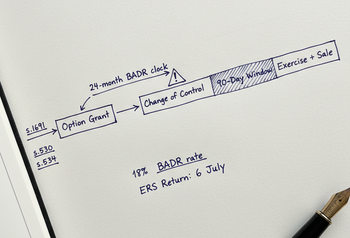

Where the structure is being driven primarily by income-splitting with no other economic rationale, two alternatives are usually preferable. Growth shares issued to a family member at a genuinely low value (reflecting the hurdle that makes them worth little on issue), with a proper option-pricing valuation and a s.431(1) ITEPA 2003 election signed within 14 days, give the family member a clean CGT stake in future upside with no settlements exposure. For employing family members, paying a market salary and keeping all shares in one class is often simpler, more defensible, and creates less due-diligence friction on a future sale.

We work with accountants and financial advisers on owner-manager structuring across the equity lifecycle, from initial incorporation through to exit planning. If an existing structure has alphabet shares and a sale or investment round is on the horizon, now is the time to review it.

Frequently Asked Questions

Are alphabet shares illegal in the UK?

No. Alphabet shares are a legitimate company law mechanism under s.629 CA 2006 for creating different classes of shares with different rights. The tax risk arises when the structure is used to divert income in a way that engages the settlements legislation under ITTOIA 2005, or when dividends are paid that are effectively salary in a different form.

Does the Arctic Systems case mean my spouse's alphabet share dividend is safe?

Not automatically. Jones v Garnett [2007] UKHL 35 held that the outright gift exception in s.626 ITTOIA 2005 protected a spousal share gift, but the shares in that case had genuine capital value and voting rights. If the shares held by your spouse are dividend-only rights with no real economic substance beyond the income stream, the Arctic Systems protection is much weaker. The facts of each structure need to be reviewed individually.

Can HMRC reclassify alphabet share dividends as employment income?

Yes, in some circumstances. Following PA Holdings Ltd v HMRC [2011] EWCA Civ 1414, dividends paid as a substitute for salary or bonus, or closely linked to an individual's employment performance, can be recharacterised as employment income and subjected to PAYE and National Insurance. The risk is highest where the dividend varies in line with personal revenue generation or replaces a conventional remuneration structure.

What is the settlements code and why does it matter for alphabet shares?

The settlements legislation in Part 5 Chapter 5 ITTOIA 2005 allows HMRC to treat the income of a "settlement" as the settlor's income rather than the recipient's. Section 620 defines a settlement widely, and a transfer of shares to a family member with the primary purpose of reducing a tax bill can fall within it. Where it applies, the dividends received by the spouse, civil partner, or other family member are taxed as if they remained the director's income.

Do I have to report dividends from my own company to HMRC?

Yes, if it is a close company and you are a director. From the 2025/26 tax year, directors of close companies must report on their self-assessment return the company name and registered number, the dividend income received from it, and the highest percentage of share capital they held during the year. This was introduced by the Income Tax (Additional Information to be included in Returns) Regulations 2025. It lets HMRC compare dividend income against shareholding, which makes disproportionate alphabet share dividends much easier to spot.

What is the s.629 CA 2006 separate class problem?

Section 629 of the Companies Act 2006 requires that different share classes must have genuinely different rights. If A, B, and C shares all have identical articles except the letter, they may not constitute separate classes at law. HMRC and the courts look at the substance of the rights, not the label. A poorly drafted alphabet structure can collapse to a single class, removing the basis for differential dividend payments entirely.

What are the main alternatives to alphabet shares for income splitting?

The main alternatives are: growth shares issued to a family member at an independently valued low price (with a s.431(1) ITEPA 2003 election signed within 14 days), which convert future appreciation into a CGT gain rather than income; paying a market salary to a spouse or family member who works in the business, which is deductible and straightforward; and in appropriate circumstances, a properly structured equal-shareholding arrangement where both parties have genuine economic exposure.

When should I review an existing alphabet share structure?

Review it immediately if a sale is in contemplation, if the company has received an HMRC enquiry or compliance check, if family circumstances have changed, or if the dividend pattern has become disconnected from commercial reality. The further the structure drifts from the facts that supported it at the outset, the greater the risk on any challenge.

To discuss whether your current share structure is defensible, or to consider a restructure ahead of a sale or further investment round, contact us. We advise owner-managers and their professional advisers across the full equity lifecycle.