A sale of the company is the moment EMI options are designed for. Done correctly, option holders pay capital gains tax at the BADR rate on the entire uplift from grant date to sale. Done incorrectly, the income tax exemption on exercise disappears, BADR is lost, and the ERS reporting obligation is missed. I am Steve Livingston FCA, and this article sets out what happens to EMI options on a trade sale, step by step.

Contents

- What happens to EMI options when your company is acquired?

- The 90-day rule: the most important deadline on a trade sale

- BADR on EMI shares: the special rules under TCGA 1992 s.169I

- Cash sales versus share-for-share exchanges: two different outcomes

- Replacement options: when the acquirer keeps the scheme alive

- Discounted options: the income tax exposure at exercise

- What to file: ERS annual return obligations after exit

- FAQ

What happens to EMI options when your company is acquired? {#what-happens}

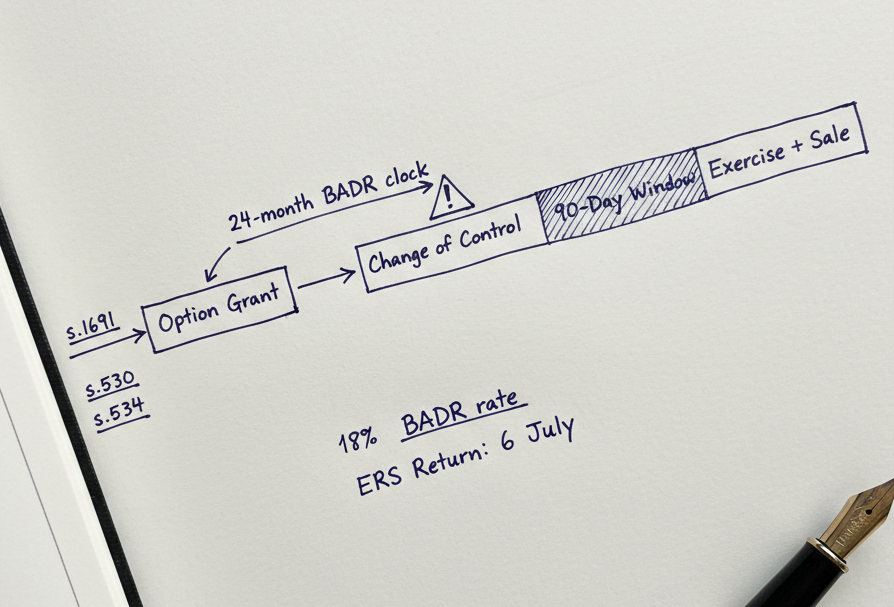

When a company with outstanding qualifying EMI options is acquired, several things happen simultaneously. The change of control is a disqualifying event under ITEPA 2003 s.534. A disqualifying event does not automatically destroy the income tax advantages of the option, but it starts a clock. From the moment the acquiring company obtains control, option holders have 90 days to exercise and retain their EMI income tax relief.

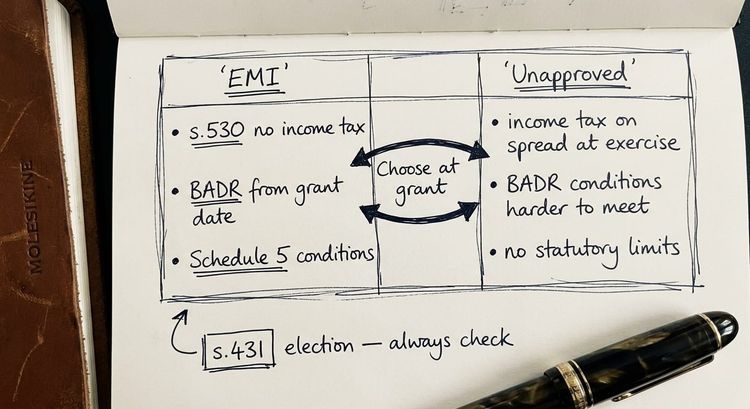

If the option is exercised within 90 days, and was granted at or above the agreed market value, no income tax arises on exercise under ITEPA 2003 s.530. The option holder acquires shares at the grant-date price, sells them at the completion price, and the entire gain between those two values sits in the capital gains tax regime, usually qualifying for the Business Asset Disposal Relief rate.

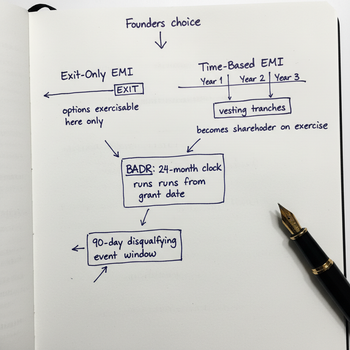

This is why most EMI schemes are structured as exit-only: the option becomes exercisable on a change of control, the holder exercises immediately before or at completion, and the shares are sold in the same transaction. The whole event is clean.

The 90-day rule: the most important deadline on a trade sale {#90-day-rule}

A change of control triggers a disqualifying event under ITEPA 2003 s.534. Once the acquiring company has obtained control, the 90-day clock begins. Option holders who exercise within 90 days retain the EMI income tax exemption in full, meaning no income tax arises on the exercise of a full-value option (one granted at or above grant-date market value).

Option holders who miss the 90-day window face the consequences in ITEPA 2003 s.532. The income tax charge is calculated on the "post-event gain" (the increase in share value between the disqualifying event and the date of exercise). That amount is treated as employment income, subject to income tax and potentially PAYE and national insurance if the shares are readily convertible assets at that point.

The practical point is that in a straightforward cash acquisition, the 90-day rule rarely causes problems: the option is exercised at completion and the shares are immediately sold. The risk arises when there is a delay between signing and completion, when consideration is deferred or structured as an earn-out, or when the transaction involves a share-for-share exchange without replacement options being offered.

For a detailed explanation of how disqualifying events arise in other contexts, including what HMRC can challenge, see our guide to EMI scheme disqualifying events.

BADR on EMI shares: the special rules under TCGA 1992 s.169I {#badr}

Business Asset Disposal Relief on EMI shares operates under a materially different set of rules from BADR on ordinary shares. The specific provisions are TCGA 1992 s.169I(7A)-(7R), introduced by FA 2013 and preserved since.

The two most important differences are these.

First, there is no minimum shareholding requirement. Ordinary BADR requires the seller to hold at least 5% of the ordinary share capital and voting rights. EMI option holders are exempt from this test entirely. A holder of 1% of the shares can qualify for BADR on the full gain.

Second, the 24-month ownership period for BADR can be satisfied by reference to the grant date of the option, not the date of exercise. Provided the option was granted at least 24 months before the date of disposal, the time-period condition is met, even where the shares were only acquired on the day of the sale.

The other BADR conditions still apply. The company must be a qualifying trading company (or holding company of a trading group) throughout the relevant period. The option holder must be an employee or officer of the company throughout. If either condition is not met, BADR falls away and the gain is taxed at the standard CGT rate: 18% (for basic-rate taxpayers) or 24% (for higher-rate taxpayers) in 2026/27.

The BADR rate on qualifying EMI share disposals is 18% for 2026/27 (up from 14% in 2025/26, following the changes in Autumn Budget 2024). The lifetime limit remains £1 million of qualifying gains per individual. Gains above that threshold are taxed at the standard CGT rate.

Key takeaway: EMI option holders can access BADR on a trade sale without satisfying the 5% shareholding test, provided the option was granted at least two years before the disposal and the company and employment conditions are met throughout. Gains beyond the £1 million lifetime limit are taxed at the standard CGT rate.

Cash sales versus share-for-share exchanges: two different outcomes {#cash-vs-shares}

The tax treatment of EMI options on a trade sale differs depending on the structure of the consideration.

Cash acquisition: Options are exercised at or just before completion. The holder pays the exercise price, acquires shares, and immediately sells them to the acquirer for cash. The income tax exemption under s.530 applies (assuming a full-value option exercised within 90 days). The gain is in CGT and BADR applies if conditions are met. Payment of the exercise price is typically funded from the sale proceeds, so there is no cash requirement on the option holder.

Share-for-share exchange where the acquirer is an eligible EMI company: Options need not be exercised at all. Under ITEPA 2003 Sch 5 paras 39-43, the option holder may instead release the old option in exchange for a replacement option over shares in the acquiring company. If a valid replacement option is granted within six months of the change of control, the new option inherits the grant date of the original (Sch 5 para 41(5)(b)). The BADR clock continues to run from the original grant. This is the structure known as "rollover through replacement options", covered separately in our article on preserving EMI through restructuring.

Share-for-share exchange where the acquirer is not eligible for EMI: The replacement option route is closed. The acquiring company may be too large, listed, or carry on excluded activities. In this situation, the option holder must exercise within 90 days of the change of control to retain EMI relief. The shares received in exchange are subject to CGT on disposal under the general CGT rules. TCGA 1992 ss.135-136 may treat the share exchange as not a disposal for CGT purposes, deferring any gain until the replacement shares are sold. The CGT deferral and the EMI income tax exemption are distinct questions. The income tax exemption on exercise is governed by the 90-day window, not by the CGT treatment of what is received.

Replacement options: when the acquirer keeps the scheme alive {#replacement}

If the acquirer is itself an eligible EMI company and is acquiring 100% of the target, it may offer replacement options to existing EMI option holders. The mechanics are in ITEPA 2003 Sch 5 paras 41-43.

The replacement option must be granted within six months of the acquiring company obtaining control (Sch 5 para 42). At the moment the new option is granted, the total market value of the shares subject to the new option must equal the total market value of the shares under the old option immediately before the release (Sch 5 para 43(6)). The acquiring company must satisfy the independence and trading activities requirements. The option holder must be an eligible employee in relation to the acquiring company.

Where these conditions are met, the replacement option is treated for all EMI purposes as if it had been granted on the date of the original option. The income tax advantages carry forward. The BADR clock runs from the original grant date.

Where conditions are not met (the acquiring company is listed, or too large, or carries on excluded activities), the replacement option route is not available. If that is the case and the option holder does not exercise within 90 days of the change of control, the income tax exemption is lost on the post-event growth.

This is a planning point that often arises too late. The question of whether the acquirer can offer valid replacement options should be part of the transaction due diligence, not something resolved on the day before exchange.

Discounted options: the income tax exposure at exercise {#discounted}

Not all EMI options are granted at full market value. Where the exercise price is set below the agreed market value at the date of grant, the option is a "discounted option". On exercise, an income tax charge arises under ITEPA 2003 s.531 on the lesser of (a) the amount of the discount (the difference between market value at grant and the exercise price) and (b) the excess of the market value at exercise over the exercise price.

Where the company is about to be sold, the shares are readily convertible assets (RCAs) and the income tax charge is subject to PAYE and national insurance contributions under the restricted chargeable assets rules.

The capital gain is still calculated in the usual way, but the base cost includes both the exercise price paid and the amount charged to income tax. The BADR CGT rate still applies to the remaining gain, provided all conditions are met.

One practical consideration: where the valuation agreed with HMRC's Shares and Asset Valuation office was not the actual unrestricted market value, there is a risk that HMRC challenges the discount calculation. For EMI options where the exercise price was agreed with HMRC SAV, a review of the agreed value before exercise is advisable. Our guide to HMRC valuation for EMI schemes explains the process.

What to file: ERS annual return obligations after exit {#filing}

The exercise of EMI options on a trade sale creates reporting obligations that must be met by 6 July following the end of the tax year in which the exercise occurs.

The company (or its successor) must submit an annual Employment Related Securities (ERS) return via HMRC's online ERS service. The return must capture all option exercises during the year, including the exercise date, exercise price, market value at exercise, number of shares, and whether the exercise was within 90 days of a disqualifying event.

If the company is acquired and ceases to have a UK payroll immediately, the obligation to file still falls on the employer company as it was at the date of exercise. In practice, this means the target company's directors or its advisors must ensure the return is filed before the 6 July deadline. Missing the deadline carries a penalty of £100 for late filing. If the return remains outstanding after 3 months from the filing date, a further £300 penalty is charged. If it remains outstanding after 6 months, a further £300 is charged. Beyond 9 months, HMRC may additionally impose a daily penalty of £10 for any period it specifies by notice (Sch 5 para 57B, ITEPA 2003).

Where the acquisition is completed close to the 6 July deadline, this obligation can fall through the gaps in the transaction process. It should be explicitly allocated to a responsible party in the sale and purchase agreement or in the post-completion timetable.

FAQ {#faq}

Do EMI option holders have to exercise their options when the company is sold?

Not automatically. Whether an option holder must exercise depends on the option agreement. Most exit-only EMI schemes make the option exercisable on a change of control and include drag-along provisions. If the acquirer offers valid replacement options over its own shares, option holders may instead release their current options and receive new ones. In a straightforward cash acquisition, exercise at or before completion is the standard approach.

What is the 90-day rule for EMI options on a trade sale?

A change of control is a disqualifying event under ITEPA 2003 s.534. Option holders who exercise within 90 days of the disqualifying event retain the EMI income tax exemption under ITEPA 2003 s.530. Option holders who miss the 90-day window face an income tax charge on the post-event gain under ITEPA 2003 s.532.

Can EMI option holders claim BADR without holding 5% of the company?

Yes. The special EMI BADR provisions in TCGA 1992 s.169I(7A)-(7R) remove the minimum shareholding test. A holder of any size stake can claim BADR on EMI shares, provided the option was granted at least 24 months before the disposal, the company meets the qualifying trading company test throughout, and the option holder is an employee or officer throughout.

What happens to EMI options on a share-for-share exchange where the acquirer is a large listed company?

The replacement option route under ITEPA 2003 Sch 5 paras 39-43 is not available if the acquirer is not eligible for EMI (for example, because it is listed, too large, or carries on excluded activities). Option holders must exercise within 90 days of the change of control to preserve the EMI income tax exemption. The capital gains treatment of any shares received depends on whether TCGA 1992 s.135 or s.136 applies to defer CGT on the share exchange.

What ERS returns are required after a company sale?

The company must file an annual ERS return by 6 July following the end of the tax year in which options were exercised. The return is submitted via HMRC's online ERS service and must include all exercise events during the year, with details of exercise dates, prices, market values and whether the 90-day window applied. Missing the deadline attracts financial penalties.

Does BADR still apply if a disqualifying event occurred before the sale?

BADR can still apply after a disqualifying event, provided the option is exercised within 90 days of that event. Where options were exercised late (beyond 90 days), income tax arises on the post-event growth, but the gain from grant date to the disqualifying event remains in the CGT regime and may still qualify for BADR, subject to the usual conditions being met at the relevant dates.

What is the BADR CGT rate on EMI shares in 2026/27?

The BADR rate on qualifying EMI share disposals in 2026/27 is 18%, following the changes introduced in Autumn Budget 2024. The rate was 14% in 2025/26 and 10% in earlier years. The first £1 million of qualifying BADR gains per individual is taxed at the BADR rate; gains above that are taxed at the standard CGT rate.

What to do next

EMI options on a trade sale require careful sequencing: exercise timing relative to the 90-day window, confirmation that BADR conditions are met, assessment of whether the acquirer can offer replacement options, and ERS reporting once the transaction is complete.

If you are advising on a transaction where EMI options are in issue, or if you have a client who has recently received an approach, get in touch before the transaction structure is agreed. The planning points (particularly whether the acquirer qualifies for the replacement option route) are most effective when addressed early.

For professionals with clients holding EMI options in companies approaching a sale or investment round, our dedicated adviser service provides specialist support across the full EMI lifecycle.

Contact us to discuss a specific situation.

Steve Livingston is a Fellow of the Institute of Chartered Accountants in England and Wales. IP Tax Solutions Ltd provides specialist advisory on EMI schemes, SEIS/EIS structuring, and innovation tax across the UK.