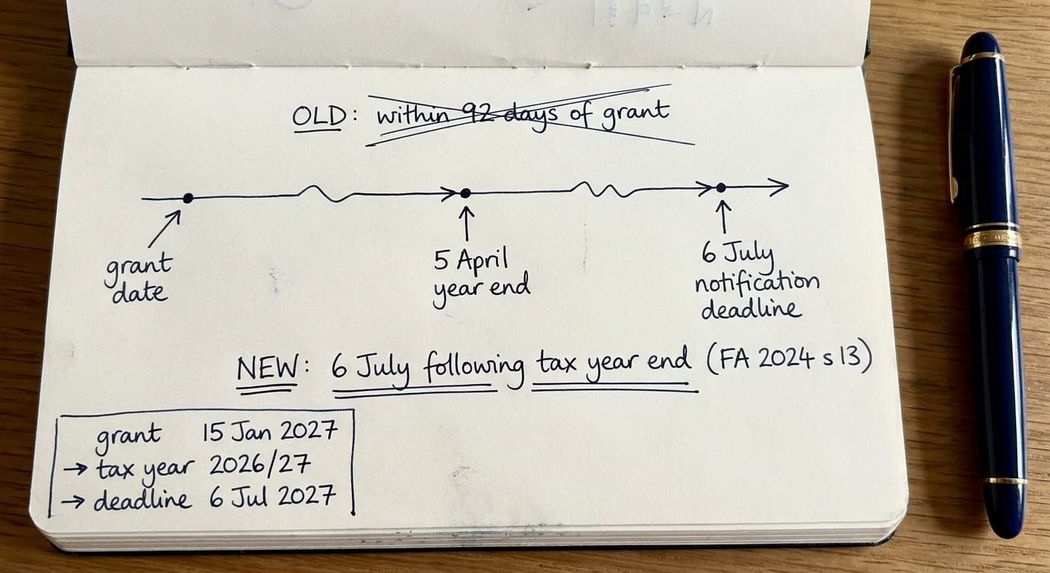

For EMI options granted on or after 6 April 2024, the company has until 6 July following the end of the tax year of grant to notify HMRC. The old "within 92 days of grant" rule has been abolished by Finance Act 2024 s 13. Miss the new deadline and the options stop being qualifying EMI options. The tax advantages are lost and cannot be put back.

Contents

- What is the EMI notification deadline under FA 2024?

- What did the 92-day rule say and why was it changed?

- How do you work out the 6 July deadline for a specific grant?

- What happens if you miss the 6 July deadline?

- Does the 6 July rule apply to replacement options?

- What are the common errors I see in practice?

- What is changing again in April 2027?

- Frequently asked questions

- About Steve Livingston FCA

What is the EMI notification deadline under FA 2024?

For an EMI option granted on or after 6 April 2024, the company must notify HMRC of the grant on or before 6 July following the end of the tax year in which the option was granted. Notification is made through the Employment Related Securities online service on HMRC's portal.

The change moves EMI notification onto an annual cycle that aligns with the existing ERS annual return, which is itself due by 6 July each year. The notification of grant and the annual return now share one deadline and one portal.

For grants made before 6 April 2024, the old "within 92 days of grant" rule continues to apply to those historic grants. The change is not retrospective.

What did the 92-day rule say and why was it changed?

Until 6 April 2024, the company was required to notify HMRC of an EMI grant within 92 days of the date of grant. That meant a separate compliance event for every single grant, regardless of how small or how routine. Many companies missed the deadline. Many advisers tracked it badly. Some specialists ran a permanent risk register of pending 92-day clocks.

The change in Finance Act 2024 s 13(2) replaced the words "within 92 days after the date of the grant of the option" with "on or before 6 July following the end of the tax year in which the option was granted". This was part of a broader, multi-year EMI simplification package, which also included the complete removal of the requirement for employees to sign a physical working time declaration back in April 2023.

The policy intention was to reduce the administrative burden on growth-stage companies running EMI schemes. In practice the change has done so, but it has also created a window of confusion. Many of the practitioner notes, online guides, and template files still in circulation continue to cite the 92-day rule. Anything written before late 2024 needs to be treated with caution.

How do you work out the 6 July deadline for a specific grant?

There are three steps.

- identify the tax year of grant. The UK tax year runs from 6 April to 5 April. So a grant on 1 March 2027 falls in tax year 2026/27. A grant on 15 May 2027 falls in tax year 2027/28.

- find the end of that tax year. For 2026/27 that is 5 April 2027. For 2027/28 that is 5 April 2028.

- apply the deadline. Notification is due on or before 6 July following the year end. So a 2026/27 grant is notified by 6 July 2027. A 2027/28 grant is notified by 6 July 2028.

| Grant date | Tax year | Year end | Notification deadline |

|---|---|---|---|

| 15 January 2027 | 2026/27 | 5 April 2027 | 6 July 2027 |

| 10 April 2027 | 2027/28 | 5 April 2028 | 6 July 2028 |

| 1 September 2027 | 2027/28 | 5 April 2028 | 6 July 2028 |

A practical observation. For a grant made early in a tax year (April, May, June) the window is now over 14 months. For a grant made late in a tax year (February, March) the window is around four to five months. The headroom is bigger than the old 92-day window in every case, but the discipline of getting it into the diary is what catches people out.

What happens if you miss the 6 July deadline?

If a qualifying EMI option is not notified to HMRC by the deadline, paragraph 44(2) of Schedule 5 ITEPA 2003 treats the option as not being an EMI option. The tax-advantaged treatment is lost. On exercise, the gain is generally taxed as employment income, with PAYE and NIC due where the option is over readily convertible shares.

This is not a position that can be tidied up retrospectively. There is no late notification facility for EMI in the way that there is for some other compliance failures. Once 6 July passes, the option is no longer EMI for tax purposes, even if every other condition was met perfectly.

That is why the deadline matters even when the grant looks routine. The cost of a missed notification on a senior hire's EMI award can run well into six figures of avoidable income tax and NIC, on a transaction that everybody assumed was complete the day the option deeds were signed.

For founders and finance directors, the practical fix is to put the 6 July notification date in the diary the moment a grant is made, and to confirm the ERS return has been filed before the deadline.

What are the common errors I see in practice?

Three keep coming up.

- Citing the old 92-day rule. This is everywhere. Template engagement letters, draft option agreements, in-house compliance calendars and online practitioner guides. Anything dated before late 2024 should be assumed to be wrong until checked against the current rule.

- Confusing the 6 July deadline with the 90-day AMV validity window. These are two completely separate clocks. The 90 days is the window during which an HMRC-agreed actual market value remains valid for executing the option deeds (counted from the date HMRC writes back confirming the valuation). The 6 July is the notification of grant, due in the tax year cycle after the grant has actually been made. Confusing the two leads to either rushing the grant (under the misapprehension that there is a 92-day clock) or missing the notification (under the assumption that 90 days inside the AMV window is the only deadline that matters).

- Treating the notification as optional or curable. It is neither. The deadline is statutory. There is no late-notification facility. The only thing that closes the position once the deadline has passed is to remove the option from EMI treatment, accept the loss of tax advantage, and look at what other share scheme route might salvage the position.

What is changing again in April 2027?

The government has signalled that the EMI notification of grant requirement will itself be removed from April 2027, leaving only the annual ERS return to capture EMI grants. If that goes ahead as currently signalled, the position from 6 April 2027 will be that there is no separate notification at all. The annual ERS return becomes the single touchpoint.

That is the direction of travel. It is not yet enacted. Until the legislation lands, the 6 July rule under FA 2024 s 13 remains in force for all EMI grants from 6 April 2024 onwards.

If you are planning grants close to April 2027, confirm the position at the time and do not assume the requirement has already gone.

Frequently asked questions

What is the deadline to notify HMRC of an EMI option grant?

For grants on or after 6 April 2024, it is 6 July following the end of the tax year of grant. The legal basis is paragraph 44(1) of Schedule 5 ITEPA 2003 as amended by Finance Act 2024 s 13(2). For grants made before 6 April 2024, the old "within 92 days of grant" rule continues to apply to those historic grants.

Where do you notify HMRC of an EMI grant?

Through HMRC's Employment Related Securities online service, the same portal used for the annual ERS return. The notification of grant and the annual return now share one deadline and one channel.

What happens if the EMI notification is filed late?

Paragraph 44(2) of Schedule 5 ITEPA 2003 treats the option as not being an EMI option from the start. The tax-advantaged treatment is lost. On exercise, the gain is taxed as employment income, with PAYE and NIC where the shares are readily convertible. There is no late-notification facility.

Does the 6 July rule apply to existing EMI options?

No. The change applies to grants on or after 6 April 2024. EMI options granted before 6 April 2024 sit under the old 92-day rule. In practice, those grants have either been notified long ago or have already lost EMI status.

Is the 6 July deadline the same as the ERS annual return deadline?

Yes. Both are 6 July following the end of the tax year. The deliberate alignment is the policy point of the change. One portal, one date, one compliance event per year.

Does the working time declaration still need to be obtained before grant?

No. The requirement to sign a physical working time declaration was completely abolished on 6 April 2023. The working time condition itself hasn't changed - the employee must still genuinely meet the threshold (25 hours a week or 75% of their working time) - but the administrative burden of chasing and storing a signed paper declaration has been permanently removed.

What is the AMV 90-day window and how does it differ from the 6 July deadline?

The AMV 90-day window is the period for which an HMRC-agreed actual market value remains valid for granting EMI options. It runs from the date HMRC issues its valuation confirmation letter, and the option deeds must be executed within that 90-day window. The 6 July deadline is a separate annual notification of grants made during the previous tax year. The two clocks are unrelated.

Get specialist help with EMI grant timing and notification

EMI is a powerful relief, but the compliance cost of getting the timing wrong is disproportionate to the work involved in getting it right. Most of the EMI mistakes I see are basic timing or notification slips on schemes that were otherwise well designed.

If you are planning EMI grants, restructuring options through a share exchange, or unsure whether a historic grant was notified correctly, get in touch. I work with founders and finance teams directly, and with accountants and professional advisers on a referral basis for EMI scheme design, valuation submissions, and HMRC SAV correspondence.

This is a highly complex technical area so none of the above should be interpreted as professional advice.