Most EMI schemes are designed as exit-only. The option holder cannot exercise until the company is sold. That is the right default for most founder-led businesses, but it is not the right answer in every case. The choice between exit-only and time-based EMI has implications for cap table mechanics, BADR eligibility, disqualifying event exposure and the commercial dynamics with your key hires.

Contents

- What is exit-only EMI?

- What is time-based EMI?

- Why exit-only is the default for most companies

- When time-based vesting is worth considering

- The disqualifying event trap in exit-only schemes

- How BADR works for each structure

- The hybrid model: vesting schedule plus exit trigger

- A practical decision framework

- Frequently asked questions

What is exit-only EMI?

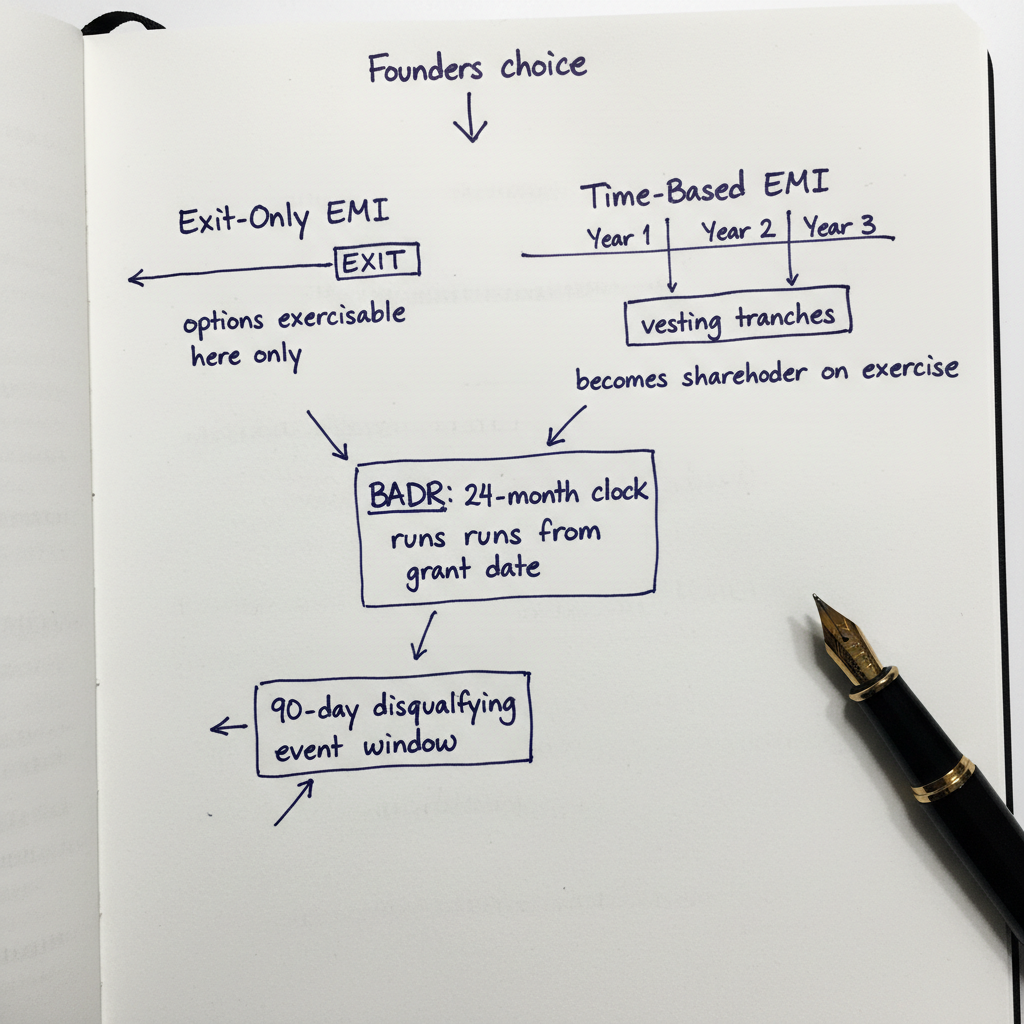

Exit-only EMI means the option can only be exercised on a defined exit event: typically a trade sale, a management buyout, or an initial public offering. Until that event happens, the option holder cannot convert their options into shares. They are not a shareholder. They hold a contractual right to acquire shares at a future point, but nothing more.

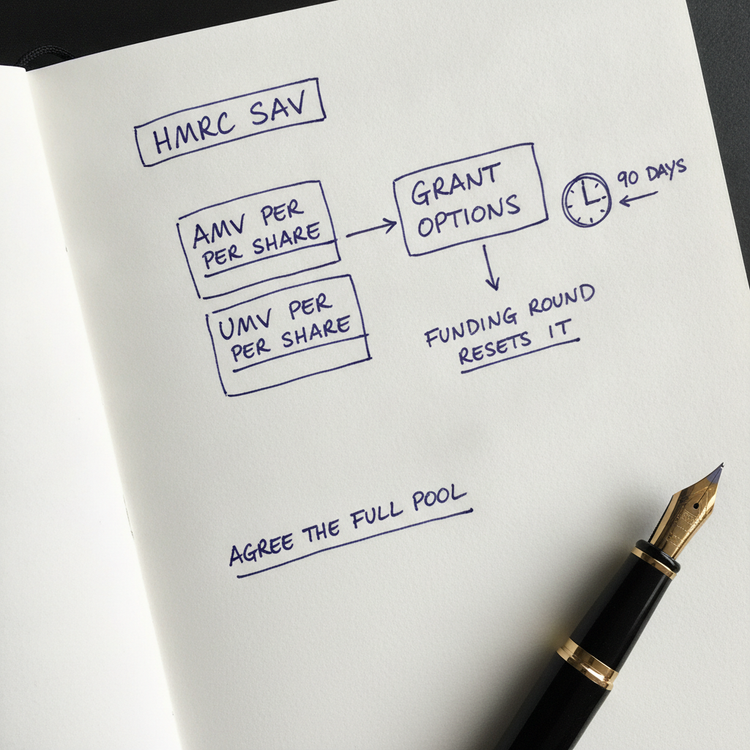

The exercise price is set at the agreed actual market value (AMV) at the date of grant, confirmed with HMRC's Shares and Assets Valuation (SAV) team where prior agreement has been sought. On exercise at the moment of sale, the option holder pays the grant-date AMV and simultaneously sells their shares as part of the wider transaction. The profit (sale price minus exercise price) is taxed as a capital gain, not as employment income.

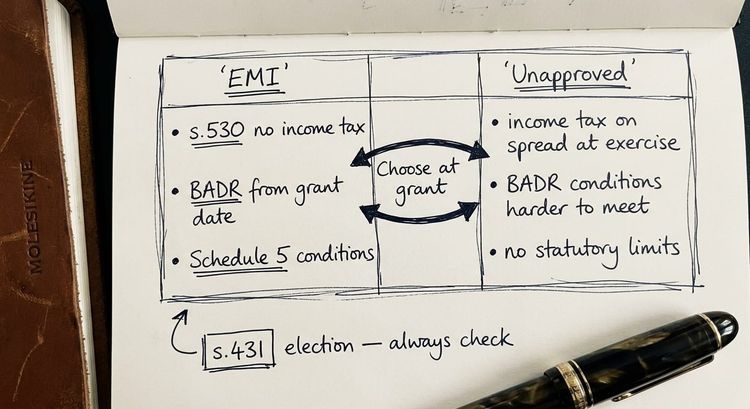

This is the structure most practitioners mean when they refer to "exit-only options" under Schedule 5 to the Income Tax (Earnings and Pensions) Act 2003 (ITEPA 2003).

What is time-based EMI?

Time-based EMI means the option vests in tranches over a defined period, typically monthly over three or four years, sometimes with a one-year cliff before any vesting begins. Once vested, the holder can exercise that portion of their option regardless of whether the company has been sold.

This means the option holder becomes a shareholder during the life of the company, before any exit. They hold actual shares with the rights and obligations that go with a minority holding.

The underlying tax treatment is the same: exercise at AMV triggers no income tax under section 530 ITEPA 2003, and the subsequent sale of shares is taxed as a capital gain. But the practical and commercial consequences of being a shareholder during the company's operating life are very different from holding an unexercised option.

Why exit-only is the default for most companies

Exit-only is the standard for a reason. It keeps the cap table clean.

Until the option is exercised, the holder is not a shareholder. The company does not need to address minority shareholder rights, pre-emption rights, tag-along provisions, or dividend entitlement in its Articles of Association or shareholders' agreement for holders who have not yet exercised. In practice that means no drag-along wrangling, no pre-emption notices on a secondary sale, no shareholder votes from a cohort of minority holders spread across the employee base.

There is also the practical matter of funding. The option holder can simply pay the exercise price out of their share of the sale proceeds. They do not need to fund the exercise out of personal cash before seeing a return - it is effectively a "cashless-exercise" dealt with my the lawyers on a sale. For a senior hire holding options over shares worth £200,000 to £400,000, the prospect of funding the exercise personally is a real commercial obstacle. Exit-only removes it entirely.

Exit-only options mean the holder does not become a shareholder until immediately before the sale of the company, and the company therefore avoids the complications and costs of changing its Articles or creating a shareholders' agreement to cover protective provisions for option holders.

For founder-led companies below £120m gross assets with fewer than 500 employees (the thresholds applicable from 6 April 2026 under the Finance Act 2025-26), exit-only is almost always the right starting point.

When time-based vesting is worth considering

There are specific situations where time-based vesting earns its place.

- Where talent retention in a competitive market depends on more than a future exit event. A senior technology hire may value the ability to exercise incrementally and become a genuine shareholder. The psychological difference between holding an unexercised option and holding real shares matters to some people more than the tax mechanics.

- Where the company is not planning a sale in the near term and the grant horizon is long. An option with a 15-year window (the maximum under s.529 ITEPA 2003 as amended by Finance Act 2025-26) is a long time to hold a right that cannot be exercised into anything. A time-based structure allows some value realisation before the window closes.

- Where the company intends to pay dividends during the option period and the holder wants to participate. Dividends are paid to shareholders, not to option holders. Time-based vesting and early exercise are the only route to dividend participation within an EMI structure.

In all three cases, the benefit must be weighed against the cost. The company will need to update its constitutional documents and shareholders' agreement to address the rights of employees who exercise early. That is not prohibitive, but it is a real cost and a real source of complexity, particularly when a clean SEIS or EIS structure is running alongside the EMI scheme.

The disqualifying event trap in exit-only schemes

This is the area where exit-only schemes most frequently create problems in practice.

Under s.535 ITEPA 2003, when an employee ceases to meet the employment requirement (broadly, ceasing to be employed by the relevant company or a qualifying subsidiary), a disqualifying event occurs. Where an option is exercised more than 90 days after a disqualifying event, modified tax consequences apply: the gain accrued up to the date of the disqualifying event is treated as employment income, and only the gain after that date falls within the capital gains regime.

For a time-based option, a leaver who has already vested their options can exercise within 90 days of leaving. The position is manageable. For an exit-only option (with no vested shares), there is nothing to exercise into if there is no pending sale. The 90-day window closes. When the exit eventually happens, the full disqualifying event consequences apply to the gain accrued up to the leaving date.

The practical fix is to include good leaver and bad leaver provisions within the option agreement itself. Good leavers (typically those leaving by reason of death, serious illness, or mutually agreed departure) are permitted to exercise their options within a defined window, or to retain their (vested) options as if still employed. Bad leavers (those dismissed for cause) have their options lapse. The board is commonly given a limited discretion to permit exercise in specific circumstances.

That discretion needs to be drafted carefully. HMRC's position (set out in Employee Related Securities Bulletin 49 and the Employee Tax Advantaged Share Scheme User Manual at section 54320) is that an unlimited discretionary power to permit exercise invalidates the EMI status. The discretion must be limited and specific. An adviser who has drafted EMI option agreements across multiple schemes will have standard wording that sits in the right place. An adviser working from a generic template may draft provisions that are either too wide (invalidating the option) or too narrow (failing to protect the leaver's position).

How BADR works for each structure

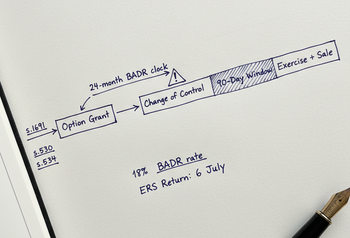

Business Asset Disposal Relief (formerly "Enterpreneur's Relief") is available on the sale of EMI shares without requiring the minimum 5% shareholding that applies to ordinary shareholders. For 2026/27 the BADR rate is 18% on gains up to £1m lifetime (formerly 14% for the tax year 2025/2026).

The critical point is when the 24-month clock starts. For EMI shares, the clock runs from the date of the option grant, not the date of exercise. An option holder who has held their options for at least 24 months before the sale qualifies for BADR on the gain, provided they also meet the employment or officer condition throughout that period.

For most exit-only schemes, where exercise and sale happen simultaneously at the exit event, the rule is straightforward: grant date plus 24 months, plus continuing employment throughout, equals BADR eligibility.

The hybrid model: vesting schedule plus exit trigger

The most widely used structure in practice sits between the two extremes. Options vest on a time-based schedule (monthly over three or four years, often with a one-year cliff) but can only be exercised on an exit event. Unvested options lapse on departure, subject to the board's good leaver discretion. Vested options held by a good leaver remain exercisable at exit.

This model gives the company the clean cap table of exit-only (no early exercise, no early minority shareholder rights) while providing the psychological incentive of a vesting schedule. The holder sees their options vest month by month. The progression is visible. But they cannot exercise until the company is sold.

From a tax perspective this remains exit-only: exercise happens at the point of sale, funded from proceeds, with the full gain taxed as CGT at BADR rates where the 24-month condition is met from the grant date.

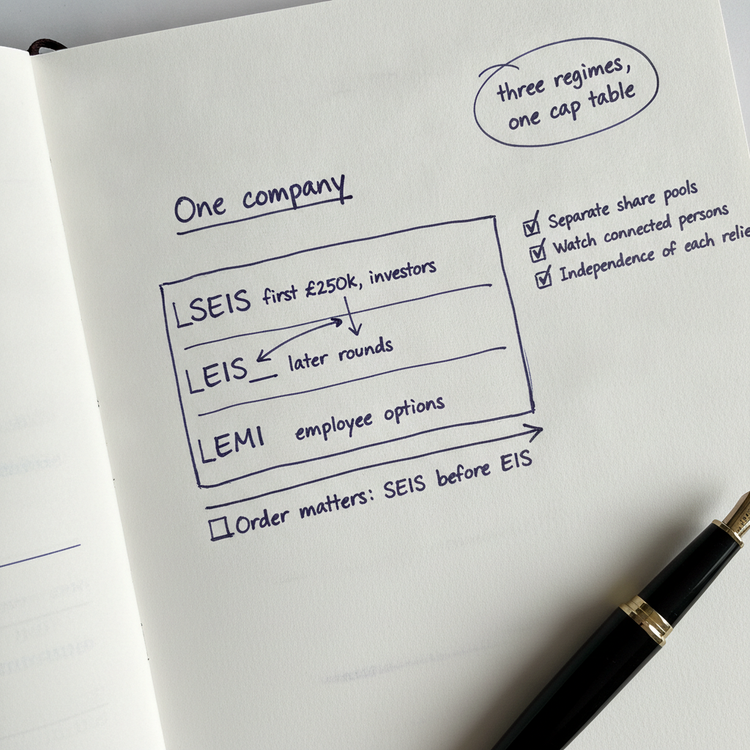

The hybrid is also the structure most compatible with SEIS and EIS investor expectations. Institutional angel investors who have taken SEIS or EIS relief are generally comfortable with a vesting-schedule plus exit-only structure. They are less comfortable with time-based exercise that places minority shareholders onto the cap table ahead of a funding round. If you are running SEIS or EIS alongside the EMI scheme, the hybrid is usually the answer that serves all parties.

A practical decision framework

For a founder deciding which structure to use, the starting questions are these.

- Do you want option holders to become shareholders before the company is sold? If no, use exit-only or hybrid. If yes, time-based with early exercise is the right structure, and you need to update your constitutional documents and shareholders' agreement accordingly.

- Will the company pay dividends during the option period? If yes, time-based exercise is the only route to give option holders dividend participation within an EMI structure.

- Is there a realistic exit within 15 years? For a company with no credible exit horizon over that window, a time-based structure may be the only practical way to give the holder something exercisable within a reasonable period.

- Are you running SEIS or EIS alongside the EMI scheme? If so, keep the cap table as clean as possible. Exit-only or hybrid is almost always the better answer.

- Are your option holders working in an advisory or part-time capacity? The EMI rules require the holder to commit 25 hours per week or 75% of their working time to the business. For part-time advisers, EMI eligibility may not be available at all, regardless of the exercise structure chosen. The structure question does not arise until eligibility is confirmed.

Key takeaway: Exit-only is the right default for most founder-led companies. It keeps the cap table clean, avoids minority shareholder complications and funds the exercise from sale proceeds. The choice shifts when early share ownership, dividend rights or a long grant horizon without a near-term exit are genuine priorities. Whichever structure you choose, the good/bad leaver provisions drafted into the option agreement itself are where the risk actually lives.

Frequently asked questions

What is the difference between exit-only EMI and time-based EMI?

Exit-only EMI means options can only be exercised on a defined exit event such as a trade sale or flotation. Time-based EMI vests over time and allows the holder to exercise and become a shareholder during the company's operating life, before any exit. Most founder-led companies use exit-only because it keeps the cap table clean until the point of sale and funds exercise from proceeds.

Can I have a vesting schedule on an exit-only EMI option?

Yes. The most common structure is a vesting schedule combined with an exit-only exercise trigger. Options vest monthly over three or four years with a one-year cliff, but can only be exercised when the company is sold. Unvested options typically lapse on departure unless the board exercises its good leaver discretion to accelerate vesting or permit retention.

Does BADR apply to EMI shares even without a 5% shareholding?

Yes. Finance Act 2013 removed the minimum shareholding requirement for EMI shares. Business Asset Disposal Relief is available regardless of the size of the holding, provided the option has been held for at least 24 months before disposal and the holder has met the employment condition throughout. The 24-month period runs from the option grant date, not the exercise date.

What happens to exit-only options when an employee leaves?

Typically, if an employee leaves and there is no pending exit, the options cannot be exercised during the 90-day window following the disqualifying event. When the exit eventually occurs, the modified income tax charge applies to the gain accrued from the leaving date. The solution is good/bad leaver provisions drafted into the option agreement, allowing the board to permit exercise within the 90-day window or to retain vested options for good leavers until the exit event.

Can I grant EMI options to a director who already holds shares in the company?

Yes, provided the director does not hold more than 30% of the ordinary share capital or 30% of the assets of a close company on a winding-up (the no material interest test in paragraph 28 of Schedule 5 ITEPA 2003). The exercise structure, whether exit-only or time-based, does not affect this eligibility test. Existing shares held before the grant are what count, not the options themselves.

How does the 15-year exercise window interact with exit-only options?

The option must be capable of exercise within 15 years of grant (formerly 10 years, until 5 April 2026). For exit-only options, the agreement must permit exercise within that window even if no exit has occurred. In practice this is achieved through a long-stop provision: if no sale or flotation has occurred by a specified date within the 15-year period, the board has a defined discretion to permit exercise. This provision should be included in all exit-only option agreements as standard.

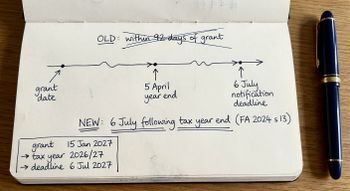

Does the choice of exit-only or time-based EMI affect the 6 July notification deadline?

No. The notification deadline (6 July following the end of the tax year of grant) applies to all qualifying EMI options regardless of whether they are exit-only, time-based or hybrid. The exercise conditions do not affect the notification obligation.

Work with Us

Exit-only versus time-based is one structural decision among several that need to be right before the option agreements are signed. Valuation, the 6 July notification timing, the interaction with existing SEIS or EIS investment, and the good/bad leaver provisions all determine whether the scheme delivers what it is meant to deliver at the exit event.

If you are a founder designing an EMI scheme from scratch, or an accountant advising a client on a scheme that has moved beyond the standard template, I would be glad to talk it through. The best starting point is the contact page. For professional advisers, the professionals page sets out how I work with accounting and law firms on complex EMI and equity structuring matters.

Steve Livingston FCA is the founder of IP Tax Solutions Ltd. He advises founders, directors and their advisers on EMI schemes, SEIS/EIS structuring, R&D tax credit defence and Patent Box across the UK.

This is a highly complex technical area so none of the above should be interpreted as professional advice.