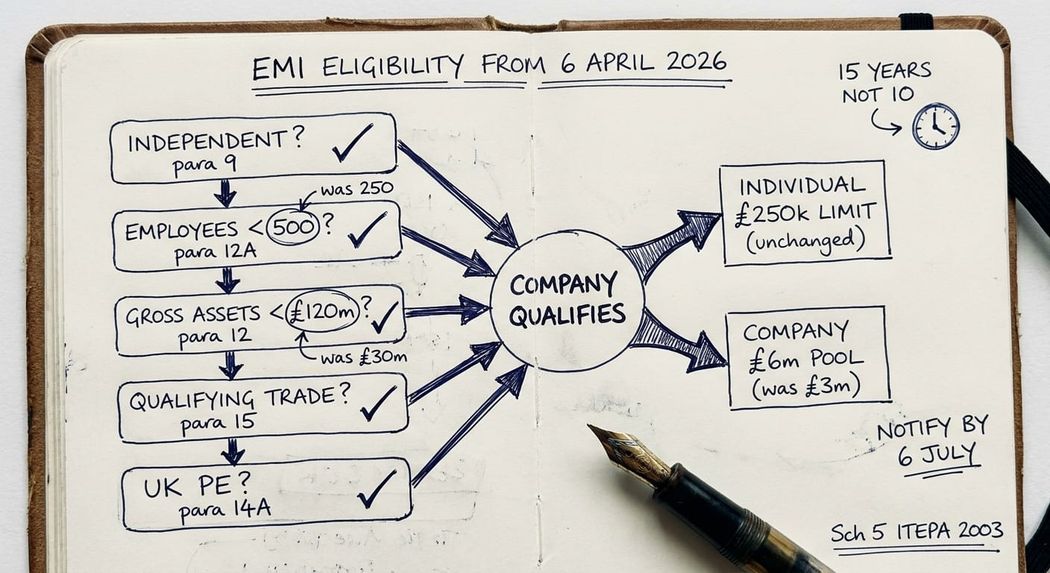

The expansion of Enterprise Management Incentives (EMI) announced at Autumn Budget 2025 and enacted in Finance Act 2025-26 is the most significant change to the regime in over a decade. From 6 April 2026, the headline company-side "gates" moved sharply upwards to accommodate a broader range of high-growth businesses.

In our experience, these new limits will pull a significant tranche of mid-market companies - especially scaling life sciences, defence, and software businesses - into the EMI net for the first time. They also provide a "rescue" route for companies that had previously aged out of EMI and switched to less tax-efficient unapproved or growth share schemes.

What Changed on 6 April 2026?

Four numerical changes sit at the heart of the EMI expansion, with effect for options granted on or after 6 April 2026:

| Requirement | Old Limit (Pre-April 2026) | New Limit (Post-April 2026) | Statutory Reference |

| Employee Headcount | < 250 FTE | < 500 FTE | Para 12A Sch 5 |

| Gross Assets | £30 Million | £120 Million | Para 12 Sch 5 |

| Total Unexercised Options | £3 Million | £6 Million | Para 7 Sch 5 |

| Exercise Window | 10 Years | 15 Years | s.529 / Para 36 Sch 5 |

The 15-Year Exercise Window & Transitional Provisions

Options granted on or after 6 April 2026 must be capable of exercise within fifteen years to maintain tax advantages.

Important Note for Existing Options: While Finance Act 2025-26 transitional provisions allow the 15-year window to apply to "live" options granted before April 2026, this is not an automatic statutory override of your existing legal contracts. Companies wishing to extend the life of older options will likely need to formally amend their option agreements to reflect the new term; otherwise, the options will still lapse based on their original 10-year contractual expiry.

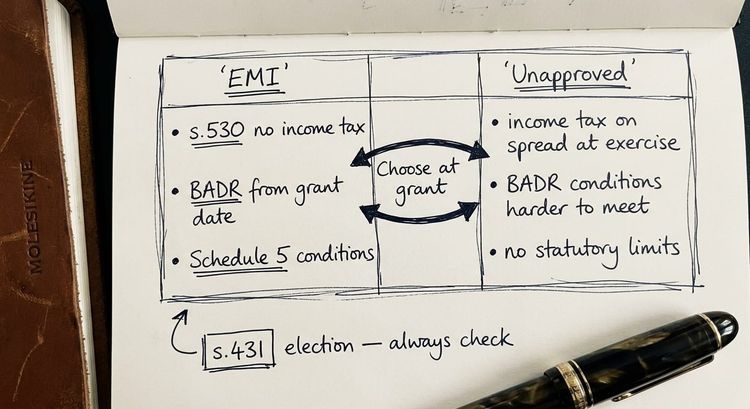

The Individual £250,000 Limit Has Not Changed

This remains the most common point of confusion. The individual financial limit is unchanged.

- An employee may not hold unexercised qualifying EMI options over shares with a total market value (measured at grant) of more than £250,000.

- CSOP options held by the same employee count towards this limit.

- Once the £250,000 ceiling is reached, no further qualifying EMI options can be granted to that employee for three years from the date of the last qualifying grant.

While the company-wide ceiling now has more headroom (£6m), the £250,000 cap remains the binding constraint for senior-hire equity packages.

What Did Not Change: The "Fixed" Conditions

The headline numbers changed, but the structural "integrity tests" of Schedule 5 ITEPA 2003 remain intact. You must still verify:

- Independence: The company must not be a 51% subsidiary or under the control of another company. Corporate parents generally kill EMI eligibility.

- Qualifying Subsidiaries: All subsidiaries must be qualifying subsidiaries (usually 51% or more, with stricter rules for property management).

- Trading Activities: The company must carry on a qualifying trade. Excluded activities (financial services, property development, etc.) must not make up more than 20% of the overall business.

- UK Permanent Establishment: The company (or a qualifying subsidiary) must have a fixed place of business in the UK.

- Employee Commitment: Optionholders must work at least 25 hours per week or 75% of their working time for the company.

- No Material Interest: An individual cannot hold more than 30% of the ordinary share capital and still qualify for EMI.

How EMI Interacts with Other Reliefs

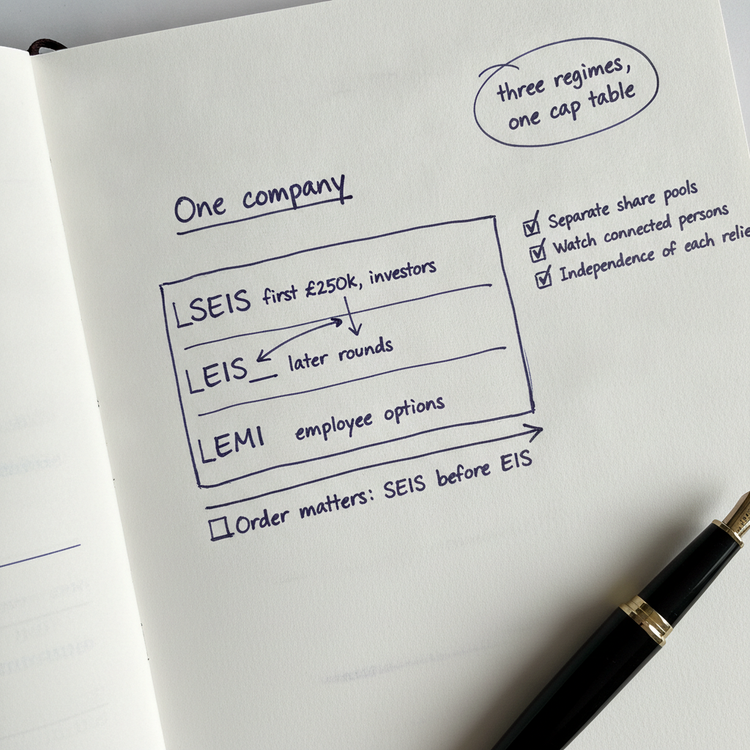

EMI and SEIS/EIS

An EMI optionholder who later acquires shares on exercise does not typically receive SEIS or EIS income tax relief on those shares.

The primary blocker is the "connected persons" rule: because EMI optionholders are, by definition, employees or directors, they are connected to the company for SEIS/EIS purposes. This disqualifies them from relief unless they meet the narrow "Business Angel" exception for unremunerated directors. However, the company can still raise SEIS/EIS investment from external investors alongside an EMI scheme.

EMI and R&D Tax Credits

An R&D-intensive company can run an EMI scheme without affecting its R&D tax credit position. The corporation tax deduction available on exercise of an EMI option is separate from the staffing-cost line in the R&D claim.

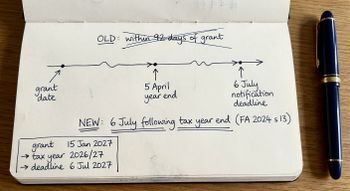

Notification and Reporting: The "Trap"

The expansion did not relax notification requirements. You must notify HMRC of a grant by 6 July following the end of the tax year in which the grant occurred.

Given the higher valuations and larger headcounts now in scope, we expect HMRC to be increasingly vigilant regarding these filings. Late notification results in the total loss of EMI tax advantages, effectively turning the options into "unapproved" schemes with full Income Tax and NIC exposure on exercise.

When EMI is Still Not the Right Answer

Even with the expansion, EMI is not a "catch-all":

- Non-Employees: Consultants and NEDs cannot receive EMI options (use unapproved schemes instead).

- Corporate Parents: If your company is a subsidiary of a US or European parent, you are ineligible (consider a "Phantom" or CSOP structure).

- High-Equity Founders: Those holding >30% cannot participate (consider growth shares or rachets).

Next Steps

If your company previously failed the old thresholds, we recommend a fresh eligibility audit. The jump to 500 employees and £120m in assets is a game-changer for the UK mid-market.

Contact Steve Livingston FCA at IP Tax Solutions for a detailed review of your scheme design, valuation submissions and notification compliance.

This is a highly complex technical area so none of the above should be interpreted as professional advice.