Most companies that receive an unfavourable outcome from an HMRC R&D tax credit enquiry accept it without challenge. That is often a mistake. HMRC enquiry officers make errors of judgement. They can misapply the DSIT Guidelines. They can conflate scientific uncertainty with commercial uncertainty. They may disallow costs on grounds that do not withstand scrutiny. The statutory appeal process exists precisely for these situations, and it works.

This article explains your rights when HMRC rejects or significantly reduces an R&D tax credit claim, the options available at each stage, and how to give yourself the best prospect of a successful outcome.

When Does an HMRC R&D Enquiry Lead to a Formal Decision?

An HMRC R&D enquiry typically opens with a compliance check letter. What triggers an HMRC R&D tax credit enquiry can range from a high claim value to inconsistencies in the Additional Information Form. The enquiry proceeds through correspondence, and sometimes an in-person or video meeting, before HMRC reaches a view.

HMRC communicates that view as a formal decision in one of two ways, depending on whether the tax year is still open for a standard enquiry:

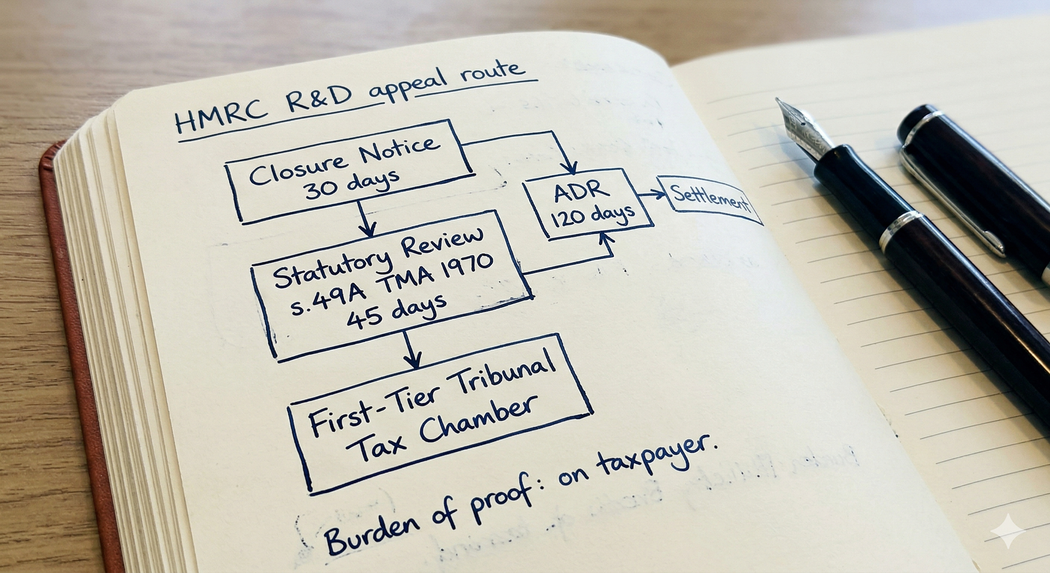

- For active enquiries (within the normal time window): HMRC will issue a closure notice under FA 1998, Sch 18, para 32. This formally ends the active enquiry and amends the company tax return as HMRC sees fit.

- For closed tax years (outside the normal time window): If HMRC believes tax was understated for a previous year that is no longer within the active enquiry period, they will issue a discovery assessment under FA 1998, Sch 18, para 41. This assesses the additional tax HMRC believes is due, based on conditions regarding non-disclosure or careless/deliberate behaviour.

The clock for an appeal starts from the date of the closure notice or discovery assessment letter. You have 30 days to lodge a formal appeal. Missing that deadline does not automatically end your right to appeal, but you will need HMRC's agreement (or tribunal permission) to appeal late. Do not let 30 days pass without taking action.

Your Statutory Right to Appeal

Under FA 1998, Sch 18, para 34, a company has the right to appeal against an amendment made by a closure notice. The same right applies to assessments. The appeal must be notified to HMRC in writing within 30 days.

On receipt of your notice of appeal, HMRC will offer one of three options:

- Settlement by agreement (s.54 TMA 1970): HMRC withdraws or modifies its position and you accept the revised figure.

- Statutory review: An independent HMRC officer reviews the decision (see below).

- Referral to the First-Tier Tribunal (Tax Chamber): The appeal proceeds to an independent judicial body.

You do not have to choose immediately, and the three options are not mutually exclusive at the early stages. In practice, most disputes go through an initial period of negotiation, then either settle or proceed to review or tribunal.

How to Request a Statutory Review

A statutory review is an internal HMRC process under s.49A-49I TMA 1970. An officer who was not involved in the original enquiry reviews the decision. The review is independent in name and in practice often produces a different outcome where the original officer applied the wrong legal test or weighed the facts incorrectly.

Key points:

- You must request the review within 30 days of receiving HMRC's offer of review (or you can request one yourself when you notify your appeal).

- HMRC must complete the review within 45 days, though this can be extended by agreement.

- The reviewer can uphold, vary, or cancel the decision.

- A statutory review does not prevent you from going to tribunal if the outcome remains unsatisfactory.

In our experience, statutory reviews are most effective where the original officer has clearly misapplied the DSIT Guidelines, particularly on the "scientific or technological uncertainty" test. A fresh pair of eyes, approaching the claim without the original officer's preconceptions, can reach a materially different conclusion.

Alternative Dispute Resolution: A Faster, More Collaborative Route

Alternative Dispute Resolution (ADR) is available at any point in an R&D dispute, including during an open enquiry, after a closure notice and before or alongside a tribunal appeal. HMRC's ADR service uses an independent HMRC facilitator whose role is to help both parties reach a mutually acceptable outcome.

ADR is not arbitration. The facilitator does not impose a decision. Both parties must agree any settlement. But the process is confidential and in complex R&D cases it provides an opportunity to engage directly with the substantive arguments without the formality and cost of tribunal proceedings.

HMRC's published target for ADR resolution is 120 days. In practice this varies, but ADR is usually faster and less expensive than a full tribunal hearing. It is particularly well-suited to cases where the dispute turns on the interpretation of facts rather than a pure point of law.

To apply for ADR, use HMRC's online application form on GOV.UK (search "use alternative dispute resolution to settle a tax dispute"). You can make the application yourself or through a specialist adviser.

Taking Your Case to the First-Tier Tribunal (Tax Chamber)

If statutory review and ADR do not resolve the dispute, the next step is the First-Tier Tribunal (Tax Chamber), governed by the Tribunal Procedure (First-tier Tribunal) (Tax Chamber) Rules 2009. The tribunal is independent of HMRC and of the courts. It is presided over by a tax judge and in technically complex cases a specialist tax member.

Cases are categorised by complexity and amount at stake. Most R&D disputes are categorised as "standard" or "complex" cases, which means directions hearings, skeleton arguments, witness statements, and a formal oral hearing.

Key takeaway: The burden of proof at tribunal lies with the taxpayer. You must demonstrate, on the balance of probabilities, that your claim is correct. HMRC does not have to prove it is wrong. This makes preparation the single most important determinant of success.

The hearing proceeds with opening submissions, evidence and cross-examination. HMRC's officer will be cross-examined on the grounds for the enquiry outcome. Your technical expert (and often the company's own employees) will give evidence on the nature of the R&D work.

What the Tribunal Looks for in R&D Tax Credit Appeals

The tribunal's primary task is to apply the law to the facts. In practice, most R&D disputes focus on two questions:

First, does the work constitute R&D under the DSIT Guidelines? The 2023 DSIT Guidelines (which replaced the earlier BIS Guidelines and apply to accounting periods beginning on or after 1 April 2023) define R&D by reference to scientific or technological advancement and scientific or technological uncertainty. The tribunal scrutinises whether the company was genuinely seeking to advance the state of knowledge or capability in the field, and whether a competent professional in the field would have considered the uncertainty to be genuine and non-trivial.

Second, do the claimed costs constitute "qualifying expenditure"? This is where precise record-keeping is critical. The Additional Information Form submitted with your claim is central here: HMRC and the tribunal will test the costs claimed against the narrative in that form.

Case law is developing. The tribunal has found in taxpayers' favour in cases where HMRC applied an overly narrow reading of "uncertainty" (treating commercial uncertainty as sufficient grounds to deny relief without proper analysis of the technical position). It has also found against taxpayers where the claimed work amounted to routine adaptation of existing methods.

If your case involves allegations beyond a straightforward technical disagreement, for example questions about the integrity of the claim itself, the legal landscape is different. A fraud allegation in the context of an R&D enquiry is a serious matter with different procedural consequences, and it requires specialist advice from the outset.

When to Settle and When to Fight

Not every adverse HMRC decision should be taken to tribunal. The cost, management time, and litigation risk must be weighed against the amount in dispute and the strength of your case. As a broad guide:

- Settle where HMRC's position has at least some merit, the amount in dispute is modest relative to the cost of litigation, or the company cannot confidently document the technical uncertainty through contemporaneous records.

- Fight where HMRC has clearly misapplied the legal test, the amount is material, your technical evidence is strong, and you have (or can obtain) credible expert witness testimony.

HMRC's Litigation and Settlement Strategy (LSS) requires HMRC to pursue cases only where it has a reasonable prospect of success. Where you have a genuinely strong technical case and can demonstrate that through expert evidence, HMRC will often settle rather than proceed to a hearing. The threat of a well-prepared tribunal case is itself a negotiating tool.

One practical consideration: if HMRC has offered a partial concession at review stage, accepting it and appealing only the remaining point is sometimes more cost-effective than fighting the whole decision from scratch.

Frequently Asked Questions

How long does an R&D tax credit appeal take?

A statutory review takes up to 45 days. ADR typically resolves within 120 days. A First-Tier Tribunal hearing for a standard or complex R&D case takes 12 to 24 months from the date of listing, depending on tribunal availability and case management directions. Early, well-documented preparation shortens the effective timeline.

Can I appeal if I missed the 30-day deadline?

Yes, but you will need HMRC's agreement or the tribunal's permission. The tribunal applies the overriding objective (fairness, proportionality) when deciding whether to extend time. A late appeal is not impossible, but the longer you wait, the harder it becomes. If you have missed the deadline, take specialist advice immediately.

What evidence does the tribunal want to see in an R&D appeal?

Contemporaneous technical records are the most powerful evidence: meeting notes, design specifications, test logs, version control histories and project documentation created at the time the R&D was conducted. Retrospective summaries carry less weight. Expert witness evidence from a qualified scientist or engineer in the relevant field is often decisive in close cases.

Does HMRC always send a specialist to tribunal?

In complex R&D appeals, HMRC is represented by counsel (a barrister) and often produces its own technical expert. You should expect a professionally prepared opposition. Attending tribunal without specialist representation in a contested R&D case is rarely advisable.

What happens if I lose at the First-Tier Tribunal?

You can appeal to the Upper Tribunal on a point of law (not on findings of fact). From the Upper Tribunal, a further appeal to the Court of Appeal is possible, also on a point of law. Appeals beyond the First-Tier Tribunal are costly and reserved for cases where there is a genuine, arguable legal question of wider significance.

Is ADR confidential?

Yes. What is said during HMRC ADR discussions is "without prejudice" and cannot be used in tribunal proceedings if the ADR does not result in a settlement. This is an important protection: you can make concessions in ADR discussions without those concessions being cited against you later.

Can I claim costs if I win at tribunal?

The First-Tier Tribunal has limited power to award costs in tax cases. Costs are generally only awarded where a party has acted unreasonably in bringing or conducting proceedings. Winning on the merits does not automatically entitle you to a costs order. The Upper Tribunal has somewhat broader discretion on costs.

Next Steps

If HMRC has issued an unfavourable decision on your R&D tax credit claim, the 30-day appeal window is running from the date of that letter. The most important thing you can do right now is take specialist advice, gather your contemporaneous technical records, and understand whether your position on the R&D qualifying conditions is defensible.

IP Tax Solutions acts for companies facing HMRC enquiries and adverse outcomes at every stage, from initial review up to tribunal representation. If you want to understand whether an appeal is worth pursuing, contact us or prepare properly for your next engagement with HMRC using our meeting guide.

Steven Livingston LLB FCA is principal of IP Tax Solutions Ltd, a boutique tax advisory practice specialising in R&D tax relief, SEIS/EIS, Patent Box and EMI schemes. He has represented clients across the full range of HMRC R&D enquiry outcomes, from closure by negotiation up to tribunal proceedings.