If HMRC has requested a meeting as part of an enquiry into your R&D tax credit claim, you need to treat it seriously. A poorly prepared meeting can result in concessions you did not intend to make, disallowed costs, or a settlement far below the value of your claim. This guide explains what HMRC is trying to achieve, what documentation you need, who should attend, and how to handle the meeting itself.

Contents

- What does an HMRC R&D meeting actually involve?

- How much time do you have to prepare?

- What documentation should you bring?

- Who should attend the meeting?

- What questions does HMRC typically ask?

- How to handle the meeting itself

- What happens after the meeting?

- When should you instruct a specialist before the meeting?

- Frequently asked questions

What does an HMRC R&D meeting actually involve?

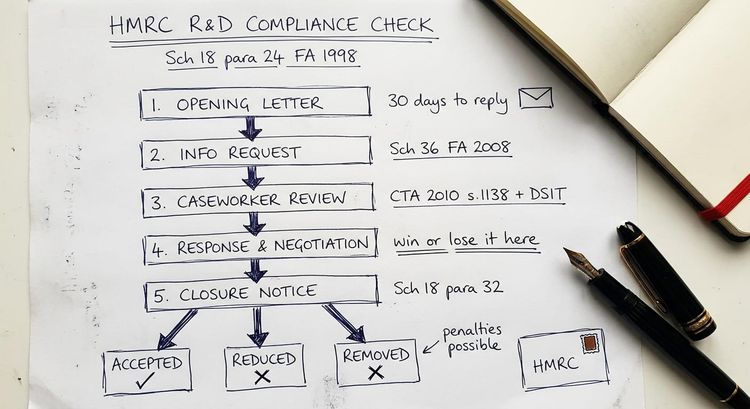

An HMRC meeting in the context of an R&D tax credit enquiry is a formal step in HMRC's compliance check process. HMRC opens these meetings under the powers in Schedule 36, Finance Act 2008, or as part of a self-assessment enquiry. In practical terms, it is an opportunity for the inspector to ask detailed technical and financial questions about your claim, assess the credibility of your technical narrative, and probe the evidence underpinning your cost calculations.

The meeting is not a casual conversation. HMRC officers at R&D specialist units (RIS teams) are trained to identify weaknesses in claims and to draw out admissions that can be used to disallow expenditure. Everything said in the meeting matters, and in some cases HMRC will ask for written confirmation of points discussed.

Understanding that this is an investigative process, not a collaborative one, is the first step in preparing effectively.

How much time do you have to prepare?

HMRC will normally give at least two to four weeks' notice of a meeting date, though the actual enquiry may have been open for several months before this point. In some cases, HMRC requests a meeting within a few weeks of issuing the initial enquiry letter.

If the timeframe is genuinely insufficient to prepare properly, you are entitled to request a postponement. HMRC is generally accommodating of reasonable requests, particularly if you can show that key individuals (such as the competent professional or technical lead) are unavailable. A short delay of two to three weeks is rarely refused.

Use every day of the notice period. The meeting date is a hard deadline. Scrambling for documentation in the final 48 hours is one of the most common reasons companies perform poorly.

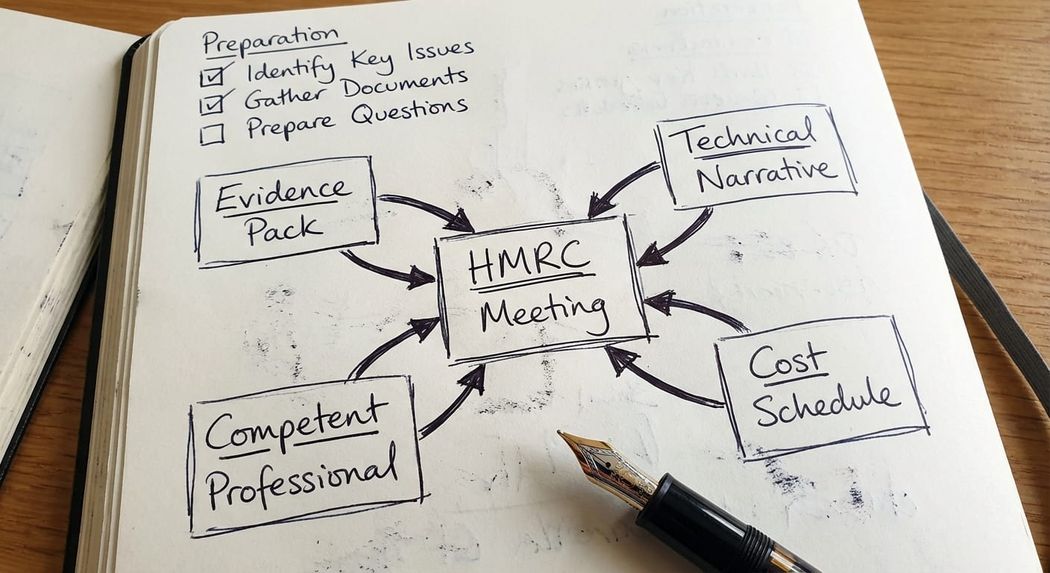

What documentation should you bring?

Your preparation should centre on assembling a comprehensive evidence pack. Based on what HMRC's GfC3 Guidelines for Compliance require claimants to demonstrate, the pack should include:

Technical documentation

- Project descriptions identifying the specific scientific or technological uncertainties being resolved, not merely what the company was trying to build commercially

- Evidence that a competent professional in the relevant field identified the qualifying activities: this means someone with genuine expertise, not just an interested director

- Technical records created during the project: design documents, test results, prototype iterations, lab notebooks, version control logs (for software), engineering drawings, or equivalent

- A clear statement of what was known in the field at the time the project started, and why the approach taken was not routine or readily deducible

Financial documentation

- A cost schedule mapping each claimed category of expenditure (staff, subcontractors, consumables, EPWs) to specific qualifying projects

- Payroll records and timesheets, or a credible time apportionment methodology with supporting rationale

- Subcontractor agreements and invoices, together with evidence of the actual R&D work performed (not just the invoice)

- Any cost-sharing arrangements, group recharges, or externally provided worker agreements

Claim documentation

- The additional information form submitted with the claim

- Any technical narrative or R&D report prepared at the time of the claim

- Previous years' claims if HMRC is reviewing more than one accounting period

The critical point is that documentation should have been created during or close to the time of the project. HMRC is alert to narratives written retrospectively to justify a claim that was prepared by a volume claim factory without proper technical input. If your documentation is weak, the meeting is not the moment to realise this.

Who should attend the meeting?

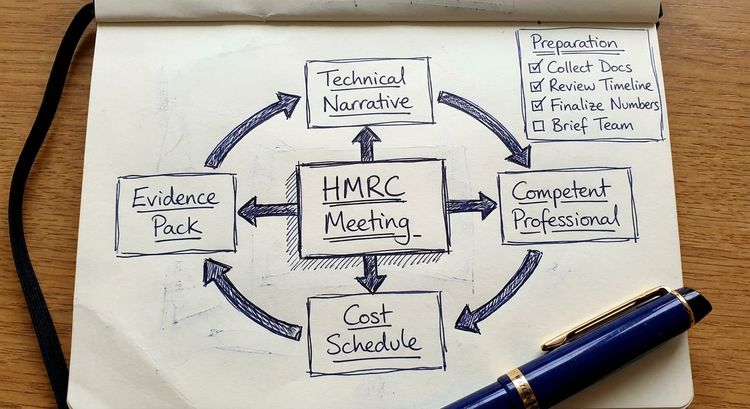

The choice of attendees is one of the most consequential preparation decisions. In my experience, the strongest meetings involve three categories of person: the competent professional, a financial representative / CFO/FD and (where the enquiry is complex) a specialist tax adviser.

The competent professional. This is the person who can speak with genuine technical authority about the qualifying projects: what the uncertainties were, why they were not routine, what was tried, what failed, and what ultimately worked or did not. HMRC's GfC3 guidelines set a high bar for what constitutes a competent professional. They must have relevant qualifications or experience, awareness of the field's current state of knowledge, and a track record in the area. A director with a general commercial understanding of the project is not sufficient.

A financial representative. Someone who can speak to how costs were identified, apportioned, and calculated. This is often the finance director or a senior member of the finance team.

A specialist adviser. If the enquiry involves technical disputes about qualifying activities, significant sums, or allegations of inaccuracy, having a specialist R&D tax adviser present is important. This is not the same as the accountant who prepared the claim. A specialist adviser can anticipate the direction of HMRC's questions, manage the pace of the meeting, and intervene when questions stray into territory that could generate unhelpful admissions.

Avoid sending anyone to the meeting who cannot speak authoritatively about the topics they may be asked about. A technical team member who is unprepared under pressure can cause significant damage.

What questions does HMRC typically ask?

HMRC's questions in an R&D meeting tend to follow a consistent pattern, focused on three areas:

Technical eligibility. HMRC will probe whether the work genuinely sought a scientific or technological advance. Expect questions such as: What was the state of knowledge in your field at the start of the project? Why was the solution not readily deducible? What specific uncertainties were you trying to resolve? What failed, and what did you learn? Who decided that this was R&D?

Competent professional. HMRC will want to understand who identified the qualifying activities and why they are qualified to do so. Expect questions about the technical background of the person named in the additional information form, their role in the project, and whether their assessment was contemporaneous.

Cost calculation. HMRC will scrutinise how staff time was apportioned, the basis for including subcontractor costs, and whether costs directly relate to qualifying activities. Expect questions about timesheets, project accounting systems and whether costs relate to the qualifying R&D or to the broader commercial project.

Key takeaway: HMRC is not trying to understand your technology. They are testing whether the evidence for your claim holds up under scrutiny. The questions are designed to find inconsistencies between your documentation, your additional information form and what your team say on the day.

How to handle the meeting itself

Several practical disciplines make a material difference to meeting outcomes.

Answer only what is asked. The most common mistake is volunteering information beyond the scope of the question. Keep answers focused and specific. If a question is unclear, ask for clarification before answering.

Do not concede without considering the implications. If HMRC suggests that certain activities or costs do not qualify, this does not need to be accepted in the room. A meeting is not a negotiation. You can note the point and agree to respond in writing after taking advice.

Take a note. Designate one attendee as note-taker. Record what HMRC officers say, what is agreed and what is left open. This record is important if there is later disagreement about what was said.

Manage technical questions through the competent professional. Direct HMRC's technical questions to the person who can genuinely answer them. If a question falls outside a particular attendee's expertise, it is better to say so than to speculate.

Do not bring draft documents. If you have internal documents that acknowledge weaknesses in a project or that describe activities in terms that do not match your claim, do not bring them to the meeting unless required. HMRC cannot demand documents in a meeting that have not been formally requested.

What happens after the meeting?

HMRC will typically write to you after the meeting summarising what was discussed and any points that remain open. This letter is important: it sets out HMRC's current position and often includes requests for further documentation.

Respond to post-meeting letters carefully. Errors or concessions in written responses after a meeting can be harder to walk back than positions taken verbally. If the meeting has gone well, HMRC may close the enquiry or indicate that only limited adjustments are required. If HMRC remains sceptical about specific projects or cost categories, there will be further correspondence.

Where HMRC issues a closure notice with amendments you disagree with, you have 30 days to appeal. The appeal options are internal HMRC review, ADR (alternative dispute resolution), or appeal to the First-tier Tribunal. Understanding how to respond to an initial HMRC enquiry letter is also covered in our guide to handling R&D tax credit enquiry correspondence.

When should you instruct a specialist before the meeting?

Preparing for an HMRC meeting without specialist input is high risk in several circumstances:

- The enquiry involves fraud allegations or assertions of inaccuracy

- The claim was prepared by a 'volume claim factory' without a proper technical narrative

- HMRC has already indicated which projects or cost categories it disputes

- The competent professional named in the claim is no longer available or was never genuinely qualified

- The amounts at stake are significant (typically above £50,000)

- HMRC's questions suggest they have a specific concern that goes beyond routine verification

A specialist can help structure the evidence pack, prepare the technical team for questioning, attend and manage the meeting, and handle post-meeting correspondence. Instructing a specialist at this stage is not an admission of weakness. It is prudent judgement. The cost of a poorly handled meeting is almost always greater than the cost of specialist support.

If you are at this stage in an R&D enquiry and want to understand your options, see how I approach R&D tax credit defence.

Frequently asked questions

Do I have to attend an HMRC meeting about my R&D claim?

HMRC cannot compel attendance at a meeting under normal enquiry powers. However, refusing a meeting is likely to slow the enquiry, create an adversarial dynamic and limit your ability to explain your position before HMRC reaches a view on the claim. In most cases, a well-prepared meeting accelerates resolution.

Can I bring my accountant to an HMRC R&D meeting?

Yes. You can bring any adviser you choose. However, the adviser you bring should have specific R&D tax experience and understand the technical aspects of your claim. A general practice accountant who prepared a straightforward claim is not ideally placed to defend the technical merits in a meeting with a HMRC officer.

What if HMRC asks questions I cannot answer on the day?

It is acceptable to say that you will take a question away and respond in writing. This is preferable to speculating or giving an answer that is later shown to be inaccurate. Note the question, confirm that you will respond by a specific date, and make sure you follow up promptly.

Can HMRC demand documents in the meeting?

HMRC can request documents under Schedule 36 powers, but formal document requests must be made in writing and cannot be demanded spontaneously in a meeting without the correct notice procedure. If HMRC asks informally in a meeting for documents you have not reviewed, you are entitled to consider the request and respond formally.

What if I disagree with HMRC's conclusions after the meeting?

If HMRC issues amendments to your claim that you consider incorrect, you have the right to appeal. The First-tier Tax Tribunal has jurisdiction over R&D disputes, and case law (including cases where HMRC has alleged inadequate technical uncertainty) is developing in this area. Early specialist involvement gives you more options.

How long does an HMRC R&D enquiry take after a meeting?

The meeting is rarely the final step. Post-meeting correspondence, further information requests, and negotiation over the scope of any adjustments typically take several months. The key variable is how well the meeting itself goes and how promptly both sides respond to correspondence.

What is a competent professional and why does HMRC care?

A competent professional, as defined in HMRC's GfC3 Guidelines for Compliance, is someone with genuine qualifications and experience in the relevant field of science or technology. They must be able to identify what constitutes an advance in the field and why the work was not routine. HMRC reduces claims to zero where no competent professional has been properly involved. This is one of the most significant points of vulnerability in R&D claims prepared without specialist oversight.

Get specialist advice before your HMRC meeting

If HMRC has requested a meeting about your R&D claim, the time to act is now, not after the meeting has taken place. I represent companies and their advisers at HMRC meetings, prepare evidence packs, and handle post-meeting correspondence. My background includes partnership at a Top 10 firm and 20+ years in corporate tax, including defending claims against fraud allegations up to tribunal.

Contact me to discuss your position before the meeting date. A short initial call costs nothing and can significantly change the outcome.

Steve Livingston LLB FCA

IP Tax Solutions Ltd

Tel: 0161 961 0096

stevelivingston@iptaxsolutions.co.uk