R&D tax credits and UK defence procurement sit on top of each other in a way that catches out even experienced finance teams. The technical work qualifies. The claimant identity does not. Under the merged scheme that applies for accounting periods beginning on or after 1 April 2024, the procurement route - who contracted with whom, on what terms, and through what vehicle - is now decisive in fixing where the relief lands. Section 1133 CTA 2009 has put contractual intent at the centre of the test, and the procurement route in defence is unusually varied: direct MOD contracts, prime sub-contracts under DEFCON terms, DASA and SBRI Defence calls, Crown Commercial Service framework call-offs, and cross-border arrangements via Foreign Military Sales. Each routes the relief differently.

This guide sets out, by procurement vehicle, how the contracted-out R&D rules apply, where the "ineligible person" rule (commonly referred to as the irrelievable client exemption) in section 1042F CTA 2009 saves a claim, and how HMRC tests the procurement analysis when an enquiry opens. It is written for CFOs and finance directors at defence companies, and for the tax partners advising them.

Why the procurement route matters

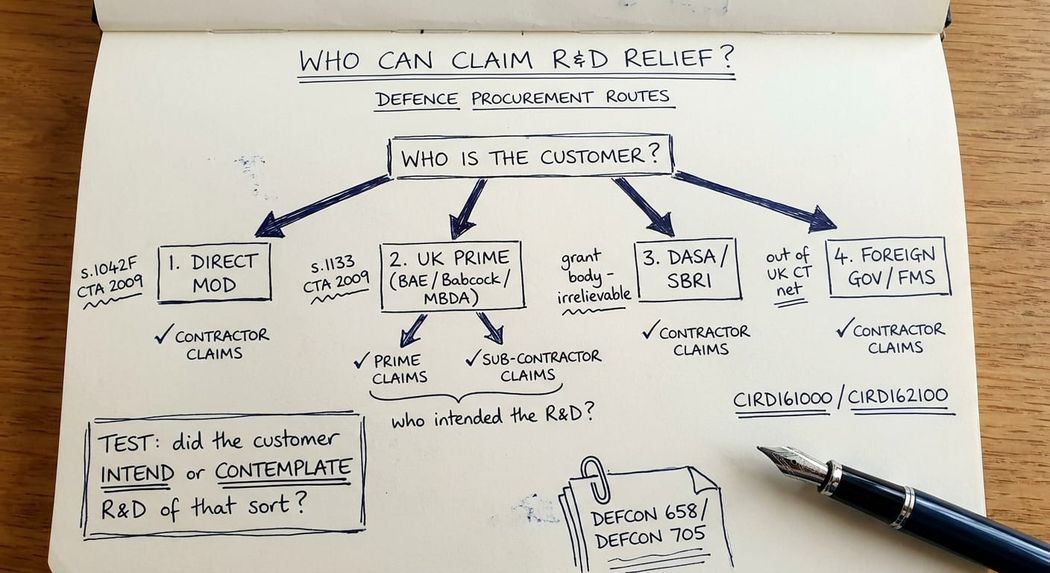

Most R&D claims do not need a procurement analysis. Defence claims do. The reason is that defence work is almost always done under a contract with a customer who is paying for the technical output.

Where that customer is the MOD, a foreign government, a UK prime contractor, or a grant-awarding body, the contracted-out R&D rules in section 1133 CTA 2009 ask whether that customer "intended or contemplated" R&D of the sort actually done.

- If the answer is yes: The customer claims (where it is in the charge to UK corporation tax) and the contractor cannot.

- If the customer is outside the UK corporation tax net: Where the customer is an "ineligible person" under section 1042F CTA 2009 (such as the MOD itself, a foreign government, or DASA), the rule lets the contractor claim notwithstanding the contract.

Two consequences follow.

- the procurement vehicle is part of the technical analysis, not an administrative footnote.

- the same R&D activity can produce different claimant outcomes depending on whether the contract sits with the MOD directly, a prime, a CCS framework call-off, or a DASA themed competition.

Finance teams that file the technical narrative without first documenting the procurement-route analysis lose claims that should have been winnable.

Direct MOD contracts and the irrelievable client rule

Where a defence company contracts directly with the Ministry of Defence, typically under the Single Source Contract Regulations or the Defence and Security Public Contracts Regulations 2011, the position is generally favourable. The MOD is a UK government department and is not within the charge to UK corporation tax. Even if the contract terms point to the MOD intending or contemplating R&D of the sort done, section 1042F CTA 2009 treats the MOD as an ineligible person (an irrelievable client). The contractor can claim notwithstanding the contracted-out point.

HMRC's example 12 at CIRD162100 puts this beyond doubt for direct contracts with a UK government department. The contractor would not have been able to claim if a UK trading customer had been on the other side of the contract, but because the MOD is not carrying on a chargeable trade, the contractor claims under the merged scheme RDEC, with ERIS available where the loss-making R&D-intensive SME conditions in CIRD123000 are met.

The same example flags the structural complication for defence: where a prime sits between the contractor and the MOD as a true intermediary on a "pass-through" basis (the R&D programme agreed between the contractor and the MOD, with the prime providing only a procurement service or contracting route), the contractor may still claim. The contracting analysis turns on whether the prime meets the conditions in section 1133(4) CTA 2009 as the party undertaking the obligations and the contracting party for the R&D work. If the prime does not, the R&D is contracted out by the MOD, section 1042F is met, and the contractor claims.

Single Source Contract Regulations contracts add a further layer. The cost-plus pricing regime, the regulated baseline profit rate, and the indexation of allowable costs all bear on the surrounding circumstances HMRC weighs at CIRD161000. Where the MOD has set the technical specification through the SSRO process and the contract carries firm-fixed-price R&D milestones, the inspector will read that as the MOD intending R&D of that sort. Where the contract is for delivery of capability with the contractor retaining design freedom and technical risk, the analysis points the other way.

Prime sub-contracts and DEFCON terms

The most common defence procurement route, and the one most likely to put a claim at risk, is the prime sub-contract. The defence company sits below a UK prime (BAE Systems, Babcock, Rolls-Royce, MBDA, Leonardo, Thales UK, QinetiQ) which has the head contract with the MOD or a foreign government. The sub-contract is usually written on standard commercial terms that flow down mandatory head-contract requirements, alongside bespoke schedules: DEFCON 658 covering cyber security and DEFCON 705 vesting foreground intellectual property in the customer.

Under section 1133 CTA 2009, the question is whether the prime intended or contemplated that R&D of the sort done would be conducted by the sub-contractor. CIRD161000 is clear that this requires a specific appreciation of the R&D, not mere awareness. Three contracting patterns recur:

- Detailed Engineering Specification: Handed down by the prime with a price reflecting the technical solution, this usually points to the prime as claimant.

- Performance Specification: Leaving the sub-contractor real design freedom, combined with the sub-contractor identifying and resolving unforeseen technological uncertainty on its own initiative, this can leave the sub-contractor as claimant by analogy with example 6 at CIRD162100.

- Research or Feasibility Scope: This unambiguously fixes the prime as claimant.

DEFCON 705 does not, on its own, decide the analysis. IP allocation is one of the surrounding circumstances at CIRD161000, alongside who priced the technical risk, who set the design route, who took the autonomy in execution, and who held the competent professional capability. A sub-contractor whose claim is anchored on autonomy, technical initiative, and self-funded technical risk - with the DEFCON 705 IP transfer acting as a contractual mechanic rather than a description of the R&D process - can hold the claim. A sub-contractor that has accepted a detailed prime specification and is delivering against it cannot.

DASA, SBRI Defence, Defence Innovation Loans and other innovation funding

UK government innovation funding routes for defence used to sit awkwardly with the old R&D rules, but the merged scheme has resolved most of the historical confusion. The Defence and Security Accelerator (DASA) themed and open calls, the Small Business Research Initiative (SBRI) defence competitions, the Defence Innovation Loan, Innovate UK programmes with a defence application, and the Defence Solutions Centre challenge competitions all flow through public bodies that are not within the charge to UK corporation tax.

Under the merged scheme, the analysis is straightforward. The contracted-out R&D test in section 1133 CTA 2009 is applied first. Where DASA or the relevant funder intended or contemplated R&D of the sort done (which is almost always the case for a competitive innovation award), the funder is the contracting party. Section 1042F CTA 2009 then applies because the funder qualifies as an ineligible person outside the charge to UK corporation tax. The defence company claims under the merged scheme RDEC, or ERIS where the conditions are met, on gross qualifying expenditure.

The legacy SME scheme treated the same money as subsidised expenditure and routed the claim through RDEC at the lower rate. From 1 April 2024, that cliff edge has gone. Two practical points still bite:

- The Contracting Counterparty: The contracting party must actually be the public body, not a commercial intermediary. Where DASA awards are managed through a delivery partner that contracts in its own name, the analysis must check whether that partner is itself an ineligible person.

- Transitional Provisions: Transitional provisions at CIRD165000 still need to be applied for accounting periods straddling 1 April 2024, as the position on grant funding for periods before that date is fundamentally different.

Crown Commercial Service frameworks and call-offs

Defence companies increasingly contract with public sector customers through Crown Commercial Service frameworks (the RM6 series, Digital Outcomes and Specialists, Cyber Security Services 3) and other framework arrangements. The framework agreement itself is not the contracting vehicle for the R&D. The call-off contract is. Each call-off must be analysed on its own terms.

Where the call-off is with the MOD or another central government department, the ineligible person analysis at section 1042F CTA 2009 applies just as it does for direct MOD contracts. Where the call-off is with a non-departmental public body, an arm's length body, or a UK trading customer, the analysis turns on whether that customer is within the charge to UK corporation tax. Most non-departmental public bodies are exempt; some commercial subsidiaries are not. The diligence required is the same as for any other contracting party: confirm the legal status of the call-off counterparty, confirm whether it is within the charge, and apply the contracted-out R&D test on the call-off scope.

A common error is to assume that a CCS framework places the contracting party on a known footing. It does not. The framework sets the terms; the call-off identifies the customer. The R&D analysis follows the call-off.

International contracts: foreign government, FMS and exports

Defence companies serving foreign customers face a different procurement landscape. Foreign Military Sales (FMS) contracts where the UK MOD is the buyer for onward sale to a foreign government, direct contracts with foreign defence ministries, NATO procurement vehicles, and contracts under government-to-government Memoranda of Understanding all need separate analysis.

Where the contracting party is a foreign government or a foreign defence ministry, that party is by definition outside the UK charge to corporation tax. Section 1042F CTA 2009 applies as they are an ineligible person, and the UK contractor claims, subject to the standard merged scheme conditions. The same outcome follows for NATO bodies and most multinational procurement vehicles. Where a UK prime sits between the foreign government and the UK contractor, the analysis reverts to the prime sub-contract pattern, with the additional question of whether the prime is itself contracting on a pass-through basis or as principal.

Export control regimes (the UK Strategic Export Controls regime, ITAR, EAR) do not bear directly on the R&D claim, but they do dictate the technical narrative. A claim involving ITAR-controlled technology cannot describe operational specifics in writing. The narrative must be calibrated to the same standard as for UK classified work, expressed at the level of technological uncertainty rather than project specifics.

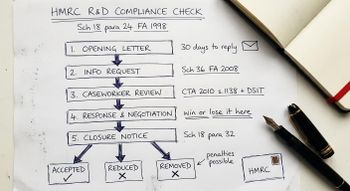

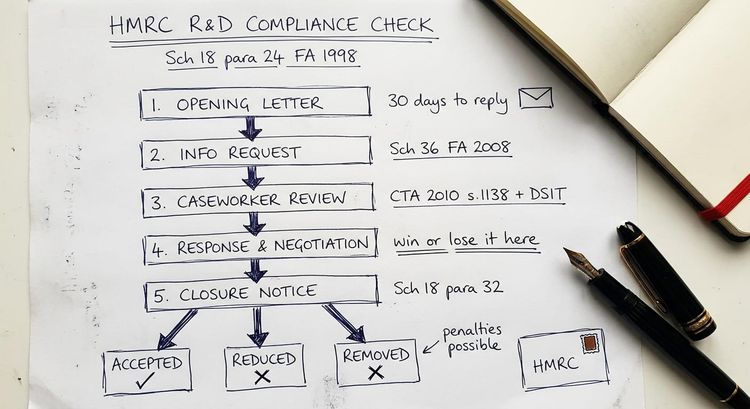

How HMRC tests the procurement route in an enquiry

Where HMRC opens an enquiry into a defence claim, the procurement-route analysis is usually the first substantive question.

- The first tranche typically asks for the underlying contract (or the grant offer letter and conditions where the work is grant-funded), the parties' identities, legal status, the scope of work, and the technical specification.

- The second tranche tests the contracted-out analysis: did the customer intend or contemplate R&D of that sort, and does section 1042F CTA 2009 apply?

- The third tranche tests the surrounding circumstances at CIRD161000, with particular attention to IP allocation, financial risk, autonomy, and decision-making.

The defensible position must be set up before the claim is filed. That means a written procurement-route analysis sitting alongside the technical narrative, identifying the contracting party, its status under section 1042F where relevant, the contracting route, and the conclusion on which party is the rightful claimant under section 1133 CTA 2009. Where this work has been done in advance and the file demonstrates it, the inspector usually accepts the position on the first or second exchange. Where it has not, the claim is exposed.

R&D tax credits and UK defence procurement turn on the contracting route as much as on the technical work. Document the procurement-route analysis before filing. The technical narrative tells HMRC what was done. The procurement analysis tells HMRC who is entitled to claim relief on it.

FAQ: R&D tax credits and UK defence procurement

Can a UK defence company claim R&D tax credits on a contract directly with the Ministry of Defence?

Yes, in most cases. The MOD is a UK government department and is not within the charge to UK corporation tax. Section 1042F CTA 2009 treats the MOD as an "ineligible person" (an irrelievable client), so the contractor can claim under the merged scheme RDEC notwithstanding the contracted-out R&D test in section 1133 CTA 2009. HMRC's example 12 at CIRD162100 confirms this position for direct contracts with a UK government department.

Does a DASA or SBRI Defence award stop a defence company from claiming R&D tax credits?

No. Under the merged scheme that applies from 1 April 2024, DASA awards, SBRI Defence funding, Defence Innovation Loans, and similar competitive innovation awards no longer reduce the claim through the old subsidised expenditure rules. The contracted-out R&D test in section 1133 CTA 2009 is applied first, and the funder is then treated as an ineligible person under section 1042F because it is not within the charge to UK corporation tax. The contractor claims on gross qualifying expenditure.

Who claims R&D tax credits on a sub-contract under DEFCON 705?

DEFCON 705 vests foreground IP in the customer but does not on its own decide the R&D claim. The question under section 1133 CTA 2009 is whether the prime intended or contemplated R&D of the sort actually done. Where the prime issued a detailed specification and priced for innovation, the prime usually claims. Where the sub-contractor identified and resolved unforeseen technological uncertainty on its own initiative, the sub-contractor may claim by analogy with Example 6 at CIRD162100. The IP allocation in DEFCON 705 is simply one of the surrounding circumstances HMRC weighs at CIRD161000, alongside autonomy, financial risk, and decision-making.

Does a Crown Commercial Service framework decide who claims R&D tax credits?

No. The framework agreement is not the contracting vehicle for the R&D; the call-off contract is. Each call-off must be analysed on its own terms: the identity and legal status of the customer, whether the customer is within the charge to UK corporation tax, and the contracted-out analysis under section 1133 CTA 2009. Most central government call-offs route into section 1042F CTA 2009, allowing the contractor to claim, but commercial intermediaries and trading subsidiaries can change the analysis.

Can a UK defence company claim R&D tax credits on a contract with a foreign government?

Yes. A foreign government is by definition outside the UK charge to corporation tax. Section 1042F CTA 2009 applies because they are an ineligible person, allowing the UK contractor to claim under the merged scheme RDEC (or ERIS where the loss-making R&D-intensive SME conditions are met). The same outcome usually follows for NATO bodies and direct contracts with foreign defence ministries. Where a UK prime sits between the foreign government and the contractor, the standard prime sub-contract analysis applies.

What evidence does HMRC ask for when it tests the procurement route in a defence R&D enquiry?

The first information request typically asks for the underlying contract or grant offer letter, the legal identity and status of the contracting party, the technical specification, and the technical narrative. The second tranche tests the contracted-out analysis under section 1133 CTA 2009 and whether section 1042F CTA 2009 applies. The third tranche evaluates the surrounding circumstances at CIRD161000. A written procurement-route analysis dated before the claim was filed is usually highly persuasive. For the wider enquiry process see our guide to how to respond to an HMRC R&D tax credit enquiry letter.

Where this leaves you

R&D tax credits and UK defence procurement reward finance teams that treat the contracting route as an integral part of the technical analysis. The merged scheme has not made defence procurement claims simpler. It has made them more procedural: identify the contracting party, fix its status under section 1042F CTA 2009, apply section 1133 CTA 2009 to the actual contract scope, and document the conclusion in writing before the technical narrative is finalised.

We work with defence companies and their tax partners on procurement-route analysis, technical narrative drafting, competent professional engagement, and HMRC enquiry defence. If you contract with the MOD, a prime, a foreign government, or through a CCS framework and would like a view on whether your R&D position is fully defensible before you file, please contact us for an initial conversation.

This is a highly complex technical area so none of the above should be interpreted as professional advice.