If HMRC has rejected your R&D tax credit claim, the decision is not the final word. There is a defined process to challenge it, and prospects of success are often better than companies assume, provided the response is structured properly and the evidence repositioned to address what HMRC has actually decided.

In our experience, rejections fall into three groups:

- technical disagreement (HMRC says the project does not meet the science or technology test),

- evidential failure (the documentation HMRC saw did not prove what it needed to prove), and

- procedural disqualification (a quirk of trading status, accounting basis, subsidy rules, or claim notification).

The route you choose, statutory review, Alternative Dispute Resolution (ADR), or First-tier Tribunal, depends on the diagnosis.

This article picks up where our earlier guide on how to respond to an HMRC R&D enquiry letter leaves off, focusing on what happens after HMRC issues a closure notice that refuses or amends the claim.

What "claim rejected" means in HMRC terminology

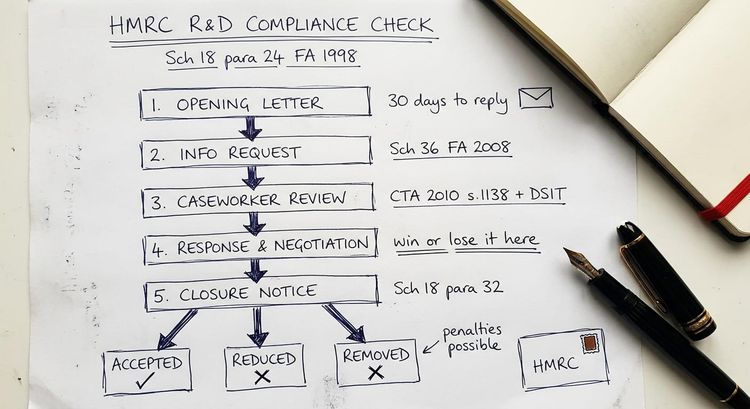

HMRC does not use the word "rejected" in formal correspondence. The decision arrives as a closure notice under paragraph 32, Schedule 18, Finance Act 1998 (ending the enquiry and amending your Corporation Tax return), an assessment to recover any payable credit already paid (often with interest and a Schedule 24 penalty), or a discovery assessment under paragraph 41, Schedule 18 if the rejection falls outside the normal enquiry window.

The terminology matters: the appeal route, time limits, and strategic options flow from which document you have received. The 30-day clock starts from the date of the document, not the date you received it. If you only have a draft closure notice or "view of the matter" letter, you are not yet at the rejection stage and a different response is appropriate.

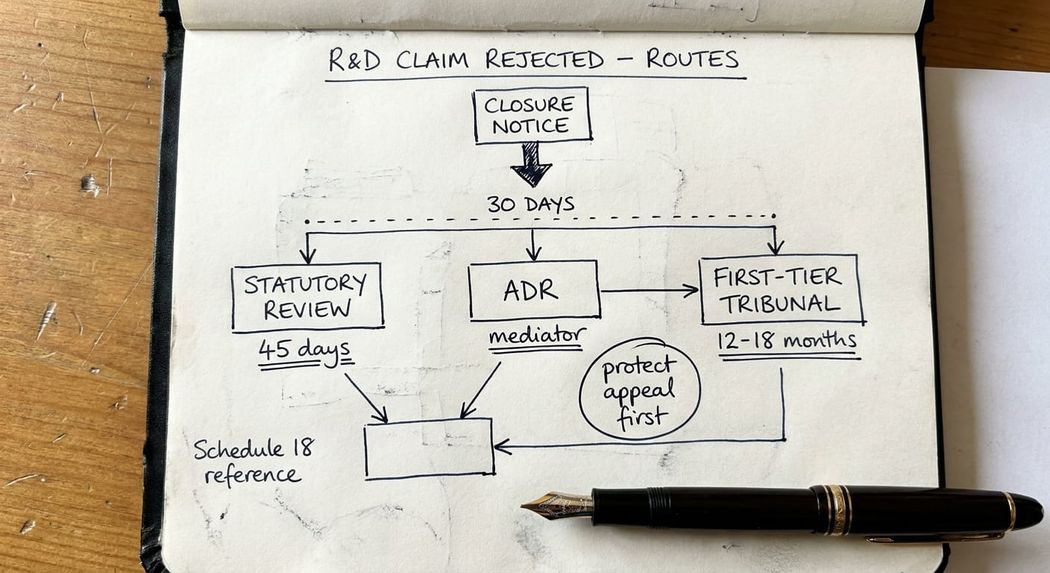

Key takeaway: A closure notice is not the end of the matter. You have a 30-day statutory window to appeal and three distinct routes (statutory review, ADR, or tribunal) to challenge the decision. The right route depends on whether the dispute is technical, evidential, or procedural.

The 30-day appeal window: what to do in the first week

Every closure notice or assessment carries a 30-day appeal period. Missing it is fatal in almost all circumstances. A late appeal is only accepted at HMRC's discretion or eventually the tribunal's, and the bar is high.

The first week after a rejection should cover four steps.

- Diary the deadline: calculate the 30-day point precisely. If the document is dated 15 June, the appeal must be in HMRC's hands by 15 July.

- Draft the appeal in writing: a short letter stating that the company appeals against the closure notice or assessment, identifying the document by reference and date, and stating the grounds in outline ("the company maintains the project meets the requirements of s.1138 CTA 2010 and the BEIS / DSIT Guidelines") is sufficient.

- Apply for postponement of tax: if the rejection produces a Corporation Tax liability or a clawback of credit, the tax becomes due 30 days after the assessment unless postponement is applied for at the same time as the appeal.

- Triage the closure notice: read it slowly. Highlight the specific paragraphs that drive the rejection. The grounds matter more than the conclusion, because each ground points to a different remedy.

The appeal letter goes to HMRC. It does not commit you to tribunal. It simply preserves your rights while you decide which route to take.

Route 1: Statutory review

A statutory review is conducted by HMRC's Legal Group (formerly the Solicitors Office and Legal Services team, renamed in January 2025). It is a fresh look at the case by someone who has not been involved in the enquiry. The reviewer examines the documentation, the technical reports, the correspondence, and the legislation, and either upholds the original decision or amends it. They produce a written conclusion within 45 days unless an extension is agreed.

Statutory review tends to work well when the dispute is legal or procedural, when the caseworker has misapplied a rule (for example, applying pre-April 2024 subcontractor rules to a post-April 2024 accounting period, or treating a customer payment as a subsidy in a way Stage One Creative Services and Collins Construction have now ruled against), or when the closure notice contains factual or arithmetical errors. It tends not to work well when the dispute is a head-on clash on whether the work was R&D: a paper-based review will rarely shift two competent professionals who honestly disagree unless new evidence is introduced. If the review upholds the original decision, you have 30 days from the conclusion letter to notify the appeal to the First-tier Tribunal.

Route 2: Alternative Dispute Resolution (ADR)

ADR is a facilitated conversation between the company, its advisers, and HMRC, led by a trained HMRC mediator who has not been involved in the enquiry. It is voluntary, free, and can be requested at any stage. It does not replace the appeal: you still need to lodge the formal appeal in time, but ADR runs in parallel.

ADR is particularly useful for R&D disputes because the process forces both sides to articulate the issues plainly. In a written enquiry, HMRC's questions and the company's answers can drift over months until both sides are responding to a moving target. ADR resets the conversation. The mediator asks "what is the actual disagreement here?" and that question, asked face to face, often surfaces the real point.

ADR works well where the technical disagreement is genuinely narrow but has been obscured by months of correspondence, where a competent professional is available to give live testimony to HMRC, and where the cost of litigation is disproportionate to the amount in dispute. HMRC caseworkers (particularly in the Individual Small Business Compliance unit) rarely take a meeting voluntarily, and ADR is one of the few ways to put the technical lead in the room. ADR cannot rewrite the law and the mediator does not adjudicate, but settlement, partial withdrawal of the rejection, or agreement on a smaller amended claim is common.

Route 3: First-tier Tribunal (Tax Chamber)

The First-tier Tribunal is the formal route. The recent case law shows that taxpayers do win, often on points HMRC had treated as settled. In the last two years the FTT has overturned HMRC's position on several R&D issues:

- Stage One Creative Services Ltd (TC09358, November 2024) and Collins Construction Ltd (TC09332, October 2024) rejected HMRC's expansive reading of the subsidy rules. Both confirmed that "standard commercial payments do not constitute a subsidy" within s.1138 CTA 2009.

- Get Onbord Ltd (TC09238, July 2024) confirmed that the burden of proof shifts based on which party provides the stronger evidence, not automatically on the taxpayer throughout. This matters when HMRC's position rests on bare assertion rather than positive evidence to the contrary.

- Realbuzz Group Ltd (TC09502, May 2025) prevented HMRC from reopening an earlier R&D claim outside the statutory enquiry window.

- H&H Scaffolding Ltd (TC09082, February 2024) held that rejection of a claim does not automatically warrant a carelessness penalty. A failed claim is not the same as a careless one.

The cases that fail at tribunal usually share the same shortcomings: insufficient documentary evidence, no competent professional testimony, advances that turn out to be routine and readily deducible, customer-funded work positioned as subsidised expenditure on the wrong analysis, or trading status that could not be established.

The economics need to be honest. A contested R&D appeal typically takes 12 to 18 months to list, with adviser and counsel fees for a one-day hearing running from £15,000 (plus VAT) to £40,000 (plus VAT). For sub-£50,000 disputes, the case for tribunal needs to be weighed against ADR and statutory review. For disputes north of £100,000, or where there is an ongoing reputational or future-claim issue, the tribunal route deserves serious consideration.

Why a second pair of eyes matters

The pattern we see most often, particularly when accountants ask us to take over a rejected claim, is that the closure notice has been written to the documentation HMRC actually saw, not the documentation that exists. Three or four months into an enquiry, things slip. Spreadsheets, project plans and procurement records that would have answered HMRC's question in three lines never made it into the response. By the closure notice stage, the case looks weaker on paper than it is in reality.

A specialist review at the appeal stage will re-diagnose the rejection against the legislation and the most recent case law, reconstruct the technical evidence so that the competent professionals who actually did the work are speaking, and build the bundle as if it were going to tribunal from day one. Even if the case settles at ADR or review, the discipline of preparing for tribunal lifts the quality of the response. This is the work IP Tax Solutions does for specialist HMRC R&D enquiry defence clients, including those introduced by accounting firms whose own teams have run the enquiry to closure notice.

Frequently Asked Questions

How long do I have to appeal an R&D tax credit claim rejected by HMRC?

You have 30 days from the date of the closure notice or assessment to lodge an appeal. The clock runs from the document's date, not the date you received it. A short letter to HMRC, identifying the decision and stating that the company appeals, is enough to preserve the position. Postponement of tax should be requested at the same time if a liability has crystallised.

What happens if HMRC rejects my R&D tax credit claim and I do nothing?

The closure notice or assessment becomes final after 30 days. The amended Corporation Tax position stands, any payable credit already received is recoverable as a debt, and HMRC can begin enforcement. You also lose the ability to challenge the decision other than through judicial review, which is narrow and rarely the right route. Lodging a protective appeal in time, even while you are still deciding strategy, is essential.

Can I get a second opinion on an R&D claim that HMRC has already rejected?

Yes, and we strongly recommend it before deciding the route. A specialist review can identify whether the closure notice has been written to weak documentation rather than the underlying facts, whether HMRC has misapplied the legislation, and whether new evidence from the technical leads can be properly introduced. The 30-day appeal window is short, so the review needs to be commissioned in the first week.

What is the difference between statutory review and ADR for an R&D claim rejected by HMRC?

Statutory review is a paper-based reconsideration by HMRC's Legal Group, conducted by someone independent of the original enquiry. It works best for legal or procedural disputes. ADR is a facilitated discussion led by a trained HMRC mediator. It works best when the parties have lost sight of the actual disagreement or when a competent professional needs to give live evidence. The two routes are not mutually exclusive.

Will HMRC charge a penalty if my R&D tax credit claim is rejected?

Not automatically. A rejected claim is not in itself a careless or deliberate inaccuracy. Schedule 24 Finance Act 2007 requires HMRC to establish behaviour, and the FTT confirmed in H&H Scaffolding that rejection alone does not warrant a carelessness penalty. Any penalty issued should be scrutinised separately and the reasonable-care defence considered.

Where to go next

If your claim has been rejected within the last 30 days, the priority is to lodge a protective appeal. After that, the diagnostic work decides the route. We act for companies whose accountants have asked us to take over and for founders / finance teams who want a specialist hand on the appeal. The work is led personally by Steve Livingston FCA. For a confidential review of your enquiry, contact us here and we will outline the realistic options within two working days.