If HMRC's Venture Capital Reliefs (VCR) Team has refused your SEIS or EIS advance assurance application, the application itself is almost always the problem, not the underlying business. In my experience, the same handful of issues come up again and again, and most of them are fixable. This article sets out why advance assurance gets rejected, how to diagnose your own application, and how to rebuild it before you reapply.

I write this from the perspective of someone who has corresponded with the VCR Team for more than two decades, including on cases where assurance was first refused and then granted on a structured second submission. The aim here is to give you the diagnostic framework I use when a refusal letter lands on a founder's or accountant's desk.

What is SEIS/EIS advance assurance?

SEIS and EIS advance assurance is a non-statutory, discretionary opinion from HMRC's VCR Team on whether a proposed share issue would meet the conditions for tax relief. It is governed by VCM60000 of HMRC's Venture Capital Schemes Manual. It is optional, but most institutional and angel investors expect to see it before they commit funds.

Two points are worth holding in mind from the outset.

- advance assurance is not a formal clearance, so there is no statutory right of appeal against a refusal.

- the assurance only ever covers the specific share issue described in the application, not the company as a whole.

A refusal does not mean the company is permanently outside the schemes. It means HMRC was not satisfied, on the information provided, that the proposed share issue would qualify. That distinction is what creates the opportunity to fix the application and reapply.

Why HMRC's VCR Team rejects advance assurance applications

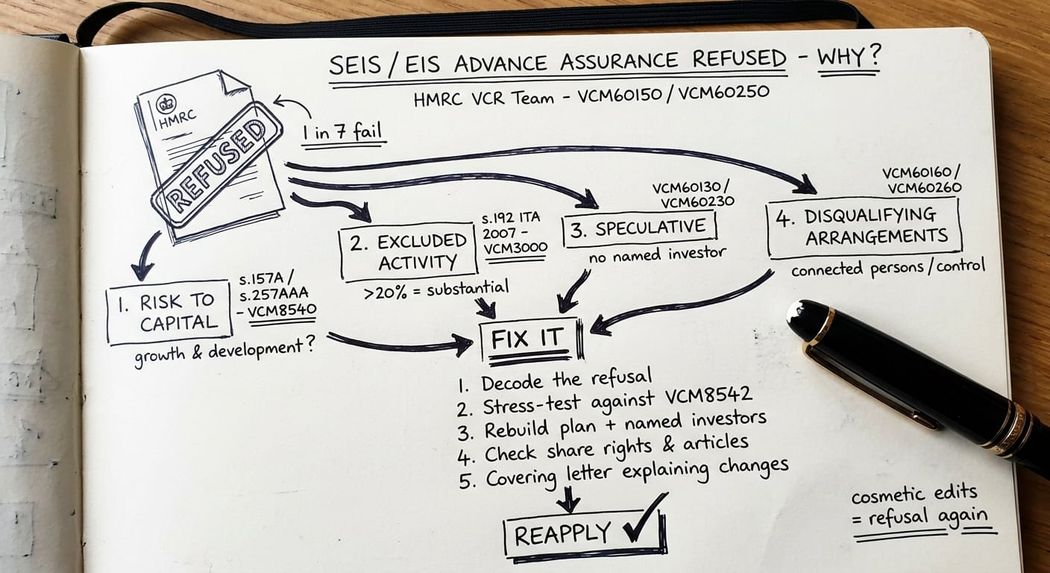

HMRC publishes a list of grounds for refusal at VCM60150 (EIS) and VCM60250 (SEIS). The list reads as a series of legal tests, but in practice the VCR Team is reaching one of three judgements when it issues a refusal.

- On the facts presented, one or more qualifying conditions cannot be met. The risk to capital condition in s.157A ITA 2007 (EIS) and s.257AAA ITA 2007 (SEIS) is the most common stumbling block here.

- The application is speculative or unsupported, often because the company has not yet engaged with named investors, or because the business plan is too thin.

- The application discloses arrangements that look like capital preservation, tax avoidance, or substantial excluded activities.

In 2024-25, HMRC processed 3,195 SEIS advance assurance applications and approved around 85 per cent. That means roughly one in seven applications failed at the first attempt. The pattern of refusals I see in practice is consistent, and the rest of this article walks through it.

The four root causes of advance assurance refusal

No.1: Risk to capital condition not satisfied

This is the most common reason for refusal, and it is the one most often misdiagnosed. The risk to capital condition has two limbs.

- The company must have objectives to grow and develop its trade over the long term, and

- the investment must carry a significant risk that the investor will lose more capital than they gain as a return.

Refusal letters on this ground usually flag one of three concerns:

- that the company looks like a special purpose vehicle for a single project rather than a long-term trade;

- that secured income streams or asset backing reduce investor risk; or

- that the marketing or share rights suggest capital preservation.

HMRC's guidance at VCM8540 makes clear that "growth and development" is assessed by reference to the company's circumstances, but the burden is on the applicant to evidence it.

The fix is to rewrite the use-of-funds and growth narrative against the VCM8542 factor list (employees, turnover, customer base, markets, brand) and to remove or restructure any feature that looks like a capital protection arrangement.

No. 2: Excluded activity (or substantial part)

The qualifying trade requirement bites where the company's activities fall within the excluded list at s.192 ITA 2007, applied to both EIS and SEIS by reference (s.257DA imports the EIS excluded activities into SEIS), as set out in VCM3000. Property-adjacent businesses, energy generation, asset leasing, financial services, royalty-based revenue models, and hospitality (including operating hotels or care homes) are the recurring problem areas.

The legislation accepts that excluded activities up to a "substantial part" of the trade are tolerated. HMRC ordinarily treats more than 20 per cent (by turnover or capital employed) as substantial, although this is a question of fact in each case.

The fix here is structural, not cosmetic. If the excluded activity is genuinely incidental, the application has to evidence that with figures. If it is core, the company will need to consider whether the qualifying activity can be carved out into a separate company or whether a restructuring before share issue is realistic.

No.3: Speculative or under-evidenced application

VCM60130 (EIS) and VCM60230 (SEIS) state that HMRC will not engage with speculative applications. In practice, this is the basis for refusing applications where the company has no named investor, no fund manager letter, no AIM Nomad, and no crowdfunding platform engagement. It is also the basis for refusing applications where the business plan reads as a pitch deck rather than a substantive document.

The supporting evidence HMRC expects is specific. Direct investor names and amounts. Letters or emails from intermediaries confirming the company has been accepted. A business plan with growth projections, employee numbers, and use of funds detail "of the kind any potential market investor or lender would expect to see," in HMRC's own words. If any of these are missing, the application is at risk.

No.4: Disqualifying arrangements and control concerns

VCM60160 (EIS) and VCM60260 (SEIS) list a set of structural indicators that the VCR Team treats as warning signs. They include voting control delegated outside scheme investors, the substantial use of subcontractors funded ahead of customer payment, intangible asset transactions involving connected parties, and marketing materials that promise low risk or capital preservation.

Connected persons issues sit alongside these. Where a director or substantial shareholder is also the proposed investor, or where group structures put control outside the company, the application can fail on the issuing company conditions in VCM13000 (EIS) and VCM34000 (SEIS) rather than on the disqualifying arrangements rule itself. The technical analysis is different. The fix usually is not.

Key takeaway: An advance assurance refusal is almost never about the company's commercial merits. It is about whether the application, on its face, satisfies HMRC that the share issue will meet the qualifying conditions. The same company, with a properly evidenced application, will often succeed on the second attempt.

How to fix the application

The mistake I see most often is companies and advisers reapplying with cosmetic changes. The VCR Team will read the second application against the first, and a thinly redrafted version will usually fail again. The fix has to be substantive.

I work through five steps when I take on a refused application.

- I read the refusal letter against VCM60150 or VCM60250 to identify which limb HMRC has actually relied on. The letter is often less specific than founders expect, so this step is partly inferential.

- I stress-test the company against the risk to capital factors at VCM8542 and the excluded activities tests at VCM3000.

- I rigorously review the business plan against each weakness identified, with figures, named investor evidence and a clear use-of-funds story.

- I check the share rights, articles, and any side arrangements for features that look like capital preservation.

- I draft a covering letter that walks the VCR Team through the changes, because a silent reapplication does not give the case officer the explanation they need.

HMRC's posture, in my reading of recent correspondence, is tighter and more evidence-driven than it was eighteen months ago.

When to instruct a specialist

Most refusals can be turned around with a careful rewrite. The cases that need specialist input are typically those involving group structures, mixed SEIS/EIS rounds, cross-border parents, connected persons issues, or borderline excluded activities. If the refusal letter raises risk to capital and the business is asset-heavy, project-based, or revenue-secured, the technical analysis is rarely something a generalist accountant will resolve unaided.

The cost of getting the second application right is meaningfully lower than the cost of losing the round, and substantially lower than the cost of issuing shares without assurance and being challenged later under the compliance statement process.

Frequently asked questions

Why was my SEIS or EIS advance assurance application rejected?

Advance assurance is most often rejected because the risk to capital condition is not satisfied, the company carries a substantial excluded activity, the application is speculative without named investors, or the structure suggests disqualifying arrangements. The refusal letter from HMRC's VCR Team will reference the specific concern.

Can I appeal an HMRC advance assurance refusal?

There is no statutory right of appeal against an advance assurance refusal because the service is non-statutory and discretionary. You can submit further information or reapply with a restructured application, but you cannot challenge the refusal through the tribunal system. If shares are subsequently issued and the compliance statement is rejected, that decision does carry appeal rights.

How long does it take to reapply for SEIS or EIS advance assurance?

HMRC aims to respond to advance assurance applications within 15 working days for standard cases and 40 working days for complex matters. A reapplication runs on the same timetable, but in my experience complex restructured cases tend toward the longer end.

Does an advance assurance refusal mean my company cannot use SEIS or EIS?

No. A refusal is not a determination that the company is permanently outside the schemes. It means HMRC, on the information provided, was not satisfied the proposed share issue would qualify. A restructured application, or a different share issue with different facts, can succeed.

What is the risk to capital condition and why does it cause so many refusals?

The risk to capital condition at s.157A ITA 2007 (EIS) and s.257AAA ITA 2007 (SEIS) requires that the company has long-term growth objectives and that the investment carries a significant risk of capital loss. It causes refusals because it is principles-based, fact-sensitive, and tested at the time of share issue. Companies with secured revenue, asset backing, or capital preservation features routinely fail it.

Can I issue shares without advance assurance if my application was rejected?

Yes. Advance assurance is optional. You can proceed to a share issue and submit a compliance statement on form SEIS1 or EIS1 instead. The risk is that the same concerns that drove the refusal will resurface when HMRC reviews the compliance statement, and at that stage a withdrawal of relief affects investors who have already committed.

Should I use the same adviser for the reapplication?

If the original application was prepared in-house or by a generalist, a specialist review is usually worth the investment. The refused application becomes part of the file the VCR Team reads when it considers the reapplication, so the second submission needs to engage with HMRC's reasoning, not work around it.

What to do next

If your SEIS or EIS advance assurance has been rejected, do not reapply on autopilot. Read the refusal letter carefully, identify which limb of VCM60150 or VCM60250 HMRC has relied on, and work back from there. The application that gets approved on the second attempt is rarely a tidied-up version of the first one. It is a substantively different document anchored in evidence.

If you would like a second opinion before you reapply, I am happy to read the refusal letter and the original application and give you a view. Most refusals can be turned around. My work can cover diagnosis and advice on next steps or a substantive response to HMRC on your behalf. Reach out to discuss your case.

This is a highly complex technical area so none of the above should be interpreted as professional advice.