Most SEIS and EIS rejections we see do not turn on the qualifying trade test, the gross assets test, or even the connected persons rules. They turn on the risk to capital condition. It is the gate every investment must pass and it is the one HMRC examines most carefully, both at advance assurance stage and on later compliance review. If you do not pass it, none of the other conditions matter.

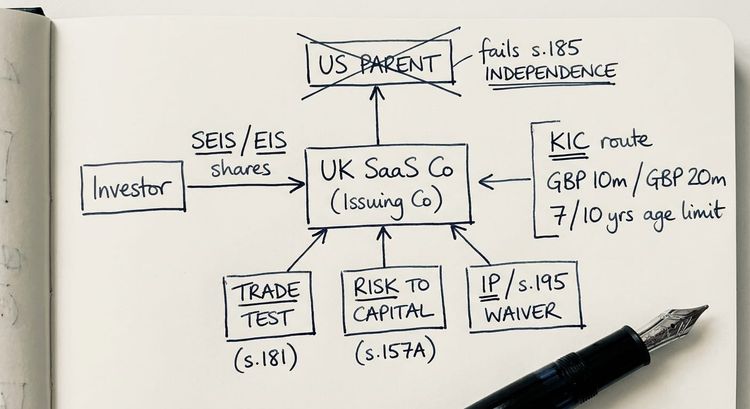

The risk to capital condition has been in force since 15 March 2018. It applies to SEIS, EIS and Venture Capital Trusts. It sits in s.157A ITA 2007 (EIS), s.257AAA ITA 2007 (SEIS) and s.286ZA ITA 2007 (VCTs), introduced by Finance Act 2018. HMRC's guidance is at VCM8500 to VCM8560. In our experience advising founders and accountants on advance assurance applications, this is where most submissions fall over and where the work to fix them is least understood.

This article sets out the two limbs HMRC actually tests, the factors that tip a borderline case one way or the other, and the practical steps to evidence the condition properly before you submit.

What is the risk to capital condition?

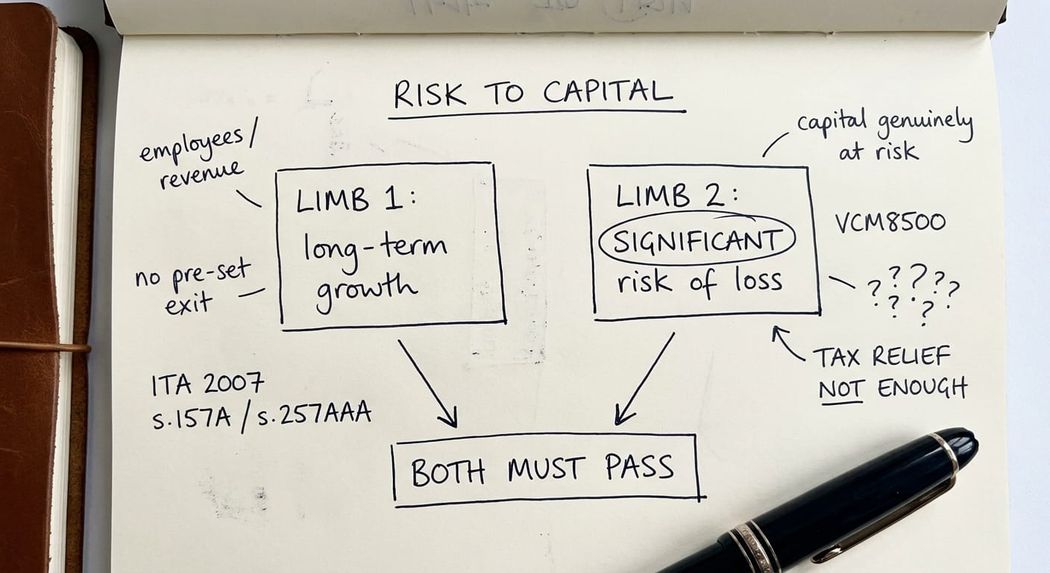

The risk to capital condition is a principles-based test that asks two questions about a SEIS or EIS share issue:

- Does the company have objectives to grow and develop its trade in the long term?

- Is there a significant risk that the investor will lose more capital than they gain as a return on the investment?

Both limbs must be satisfied. They are tested on the facts as they stand at the time the shares are issued, not later. HMRC evaluates the company in the round, looking at the prospective investment, the way it is being marketed, the company's commercial practices and any associated arrangements.

The condition was introduced because the generosity of the venture capital schemes had attracted "tax-motivated" structures. These were arrangements where the investor's capital was protected by assets, contracts, guaranteed income streams or pre-determined exit routes, and the tax relief delivered most of the return. Such arrangements often complied with the letter of the law as it stood, but they were contrary to the policy intent of SEIS, EIS and VCT. The risk to capital condition is the policy intent codified.

Crucially, there are no bright lines. HMRC has been explicit that no bright-line tests apply, precisely so the condition cannot be planned around.

Limb one: long-term growth and development

The first limb examines whether the company has objectives to grow and develop its trade over the long term. "Growth and development" is not statutorily defined. HMRC takes the ordinary meaning. Common indicators include increases in revenue, customer base or employee numbers, but the list is not exhaustive and the right indicators depend on the company's circumstances.

A company that automates and grows revenue while reducing headcount can still satisfy the condition. A company that grows employee count from one to two probably cannot, on that fact alone, rely on staff growth as evidence. The point is that the indicators must be commercially genuine and proportionate to the company's situation.

"Long term" is also undefined. The schemes are designed to encourage patient capital, and HMRC's view is that investors typically hold beyond the three-year minimum holding period. Any feature that suggests the company's existence might be compromised in order to deliver an investor exit at the end of the holding period weighs heavily against the long-term test.

Special purpose vehicles created to deliver a single project (build the asset, generate income, distribute and wind up) almost never satisfy the long-term limb. Where a parent company uses subsidiary SPVs as part of normal commercial practice, retains the capital in the group and reinvests profits to grow the group's trade, the parent may still qualify. Creative industries are a good example. A film or production parent with subsidiary SPVs for individual projects can pass the limb if the group is genuinely building lasting infrastructure.

What founders need to evidence here is a credible business plan that articulates growth ambitions extending beyond the holding period, with measurable metrics tied to the company's specific circumstances. "We will scale to £X revenue by year three" is not enough on its own. HMRC wants to see what the company will look like in year five or six.

Limb two: significant risk of loss of capital

The second limb tests whether, at the date of the share issue, there is a significant risk that the investor loses more capital than they gain as a net return.

"Net return" includes income (dividends, interest, fees), capital growth, and the upfront income tax relief itself. The presence of the income tax relief is part of the calculation. If the relief plus any contracted income or asset value gets the investor most of the way home, the risk of net loss is not significant and the limb fails.

"Significant risk" is not defined either. HMRC's position is that the assessment varies by company and by investor circumstances. The starting point is commercial failure risk. Risk of breaching the scheme's spending or qualifying trade conditions does not count as risk to capital, only commercial failure does.

In practice, this limb is most often failed by:

- Investments protected by income streams. Long-term customer contracts, pre-let property revenues, government-backed receipts. The closer the income looks to a pre-agreed yield, the harder the limb is to satisfy.

- Asset-backed structures. Where the company holds tangible assets that can be realised at or near book value if the venture fails, the loss exposure on the equity is reduced and the limb can fail.

- Limited-life vehicles. Companies set up with a known dissolution path, where the directors' job is to deliver and exit, not to keep building.

- Pre-determined exit arrangements. Side letters, put options, buy-back rights or marketing of a specific exit window all suggest the investor is buying a packaged return rather than equity in a growth business.

The condition assumes the company is genuinely trying to grow. Even legitimate growth companies carry meaningful risk because expansion can fail. The question is whether the structure being marketed has dampened that risk to the point where it is no longer significant.

The factors HMRC actually weighs

HMRC's published list of factors at VCM8542 is not exhaustive but is a useful checklist. None of them is determinative on its own, but they cluster.

- Number of employees and turnover. Growth must be demonstrable, proportionate, and pushed beyond the holding period. Stagnation at the end of year three is a red flag.

- Sources of income. Pre-investment income is fine in principle. Material assured income is not, particularly if it represents a significant proportion of forecast revenue.

- Assets. Assets used in the trade are unobjectionable. Assets that look like they are held mainly for disposal, or that secure the investment, are problematic.

- Subcontracting. A company that subcontracts most of its trading activity, holds assets, and has external parties making the commercial decisions starts to look like a shell. Genuine entrepreneurial direction is the antidote.

- Ownership and management. The schemes are intended for genuine entrepreneurs. Where the investor base is overwhelmingly composed of tax-advantaged scheme participants and the directors have been installed by promoters, capital preservation is the suspicion. Founders who hold significant equity, take real management decisions and operate independently of investors are the protection.

- Marketing. How the opportunity is sold matters. Investments marketed as low-risk, fixed-yield or short-duration almost certainly fail the limb. Marketing materials are routinely requested by HMRC during compliance review.

- Fragmentation. Splitting essentially the same activity across multiple companies to multiply the relief is a long-standing capital preservation pattern and HMRC looks for it. Closely aligned activities in different geographies, parallel SPVs, and shared promoter groups all attract scrutiny.

Key takeaway: the risk to capital condition is not satisfied by a single feature. It is satisfied by the overall commercial picture. The factors above are HMRC's lens; structuring decisions need to be tested against the whole list, not just the obvious ones.

How HMRC challenges the condition

The condition can bite at three points.

- At advance assurance. HMRC has stated explicitly that it will not give advance assurance for investments that "appear likely to fail" the risk to capital condition. Advance assurance refusals on this ground are common, and the reason given is often a brief boilerplate sentence. Pulling apart what HMRC is actually concerned about, and re-presenting the case with proper evidence, is the work.

- At compliance statement stage (SEIS1 or EIS1 submission). Even where advance assurance was given, the company must submit a compliance statement after issue, certifying that the conditions are met. HMRC reviews these on a risk-based basis. Where the issued shares, business activity or marketing has drifted from what was assured, the assurance no longer protects the company.

- On later compliance check or enquiry. HMRC can look back at investments years after issue. Tax relief can be revoked under ITA 2007 ss.208-244 (EIS) and the equivalent SEIS provisions if it later transpires that the condition was not met or that information given was misleading or incomplete.

We have represented clients in these post-issue reviews and the reality is that capital preservation indicators emerge from the evidence (marketing materials, board minutes, contracts) rather than the original application form.

The pattern is consistent: companies that received clean advance assurance and then drifted, particularly into asset-backed activity or guaranteed income, get caught at compliance review. The damage at that point is not just to the issuing company. The investors lose their relief and may face clawback assessments under s.235 ITA 2007 and the SEIS equivalents.

How to evidence the risk to capital condition properly

Evidence is the difference between a clean advance assurance and a refusal. Working through the cases we run, the items that need to be in the file before submission are:

- A board-adopted business plan with growth ambitions extending well beyond the holding period, with metrics tied to the company's circumstances and a credible path to delivering them.

- A clean explanation of why the company is genuinely high-risk, framed in commercial terms (technology risk, market risk, execution risk), not in tax terms.

- Marketing materials, term sheets and investor decks reviewed for any language suggesting low risk, capital protection, fixed yield or pre-defined exit. If any of that is present, fix it before HMRC sees it.

- Cap table and director shareholdings showing genuine entrepreneurial control. If founders have been diluted to nothing or are taking instructions from investor representatives, that needs explaining.

- A clear analysis of any income streams already in place, the proportion of forecast revenue they represent, and why they do not eliminate the equity risk.

- Where assets are held, an explanation of why they are held for trade purposes and not as security or for disposal.

- Where SPVs are involved, an explanation of why the SPV is part of normal commercial practice for the sector and how the parent group satisfies the long-term test.

- A note explaining any features that might look like capital preservation, with the commercial answer to each. HMRC reads the file looking for these features. Pre-empting them is more effective than waiting to be challenged.

In our experience, the difference between a successful application and a refusal often comes down to whether someone has thought about the case the way HMRC will think about it, before submission, and built the evidence to answer.

Frequently Asked Questions

What is the risk to capital condition for SEIS and EIS?

The risk to capital condition is a two-limbed test in s.157A ITA 2007 (EIS) and s.257AAA ITA 2007 (SEIS) that every SEIS or EIS share issue must pass. The company must have objectives to grow and develop its trade in the long term, and there must be a significant risk that the investor will lose more capital than they gain as a net return. Both limbs must be satisfied at the time the shares are issued.

When did the risk to capital condition come into force?

The condition was introduced by Finance Act 2018 and applies to SEIS and EIS investments made on or after 15 March 2018. It applies in the same way to Venture Capital Trust investments under s.286ZA ITA 2007.

Why does HMRC reject SEIS or EIS advance assurance applications on risk to capital grounds?

HMRC's published position is that it will not grant advance assurance where the investment appears likely to fail the risk to capital condition. The most common triggers are guaranteed or near-guaranteed income streams, asset-heavy balance sheets where the asset secures the investment, marketing of the opportunity as low-risk or fixed-yield, pre-determined exit arrangements, and limited-life or single-project vehicles. Cases are usually rescuable if the underlying trade is genuine and the application can be re-presented with proper evidence.

Does the risk to capital condition exclude any specific sectors?

No. The condition does not exclude sectors. HMRC has confirmed there are no bright-line industry exclusions. However, capital preservation indicators cluster in some sectors more than others, particularly property-adjacent trades, infrastructure with guaranteed revenues, and asset-backed structures. Sector context is a starting point, not a conclusion.

What is "capital preservation" in the context of SEIS and EIS?

Capital preservation describes arrangements where the tax relief delivers most of the investor's return while the capital itself is protected by assets, contracts, guaranteed income or pre-arranged exits. These structures may comply with the letter of the law on other conditions but are contrary to the policy intent of the schemes. The risk to capital condition was introduced to filter them out.

Can HMRC withdraw SEIS or EIS relief later if the risk to capital condition was not met?

Yes. HMRC can review compliance statements and the underlying facts after issue. If information given was misleading or incomplete, or if circumstances at the date of issue indicate the condition was not met, relief can be withdrawn under ITA 2007 ss.208-244 and the equivalent SEIS provisions. Investors can face assessments to claw back the relief they have received.

How do I evidence that the risk to capital condition is met?

Start with a board-adopted business plan showing long-term growth ambitions and credible metrics, ensure marketing materials do not describe the investment as low-risk or fixed-yield, document genuine entrepreneurial control by founders, explain any income streams or assets in commercial trade terms, and pre-empt any feature that could look like capital preservation. The point is to answer the questions HMRC will ask before they ask them.

Where this leaves you

If you are preparing a SEIS or EIS round, the risk to capital condition is the first thing to test, not the last. If your advance assurance has been refused on these grounds, the case is usually rescuable but only with a properly evidenced re-submission. If you have already issued shares and are now facing a compliance review, the evidence in the file is what matters; the original application form is not enough on its own.

We work with founders and their advisers on SEIS and EIS structuring, advance assurance applications, compliance statements and post-issue defence. If you want a view on whether your case will pass the condition before you submit, get in touch.

This is a highly complex technical area so none of the above should be interpreted as professional advice.