Aerospace R&D tax credits are routinely under-claimed by UK SMEs in the sector. The reason is not a lack of qualifying activity (most aerospace engineering firms have plenty). It is a combination of conservative tax preparation, a generalist accountant who treats the work as "just engineering", and a discomfort with the contracted-out R&D rules that govern Tier 1 prime supplier relationships with Airbus, Rolls-Royce, BAE Systems, GKN Aerospace, Leonardo, and the wider primes.

This guide is the sector-specific companion to our broader defence cluster. It sets out what qualifies as R&D for UK aerospace SMEs under the current statutory framework, where the qualifying activity boundaries actually sit, and how the merged scheme contracted-out R&D rules now allocate the claim across the aerospace supply chain. It is written for finance directors and CFOs at aerospace SMEs, and for tax partners advising them.

The R&D test applied to aerospace: same statute, sector-specific application

There is no separate aerospace R&D regime. For accounting periods beginning on or after 1 April 2024, the statutory framework is governed by Chapter 1A of Part 13 of the Corporation Tax Act 2009 (CTA 2009), which mirrors the definition of R&D found in Section 1138 of the Corporation Tax Act 2010. These definitions are read alongside the DSIT Guidelines (Statutory Instrument 293 of 2023). Earlier accounting periods are tested against the legacy SME or RDEC frameworks and the 2004 BIS Guidelines.

The four-part test, applied to aerospace work, requires that:

- The project must seek an advance in science or technology.

- The advance must be in overall knowledge or capability in the field, not just the claimant's own.

- The project must involve scientific or technological uncertainty that a competent professional in the field cannot readily deduce.

- The qualifying activities are those directly resolving the uncertainty, plus a defined list of qualifying indirect activities.

Aerospace engineering can meet this test routinely. The challenge is often not eligibility in principle. It is the specificity of the technical narrative, the contracting analysis, and the identification of where the genuine technological uncertainty sits within projects that are otherwise heavily engineered around mature airworthiness frameworks (CS-25, DEF-STAN 00-970, MIL-STD-810, RTCA DO-178C for software, DO-254 for hardware).

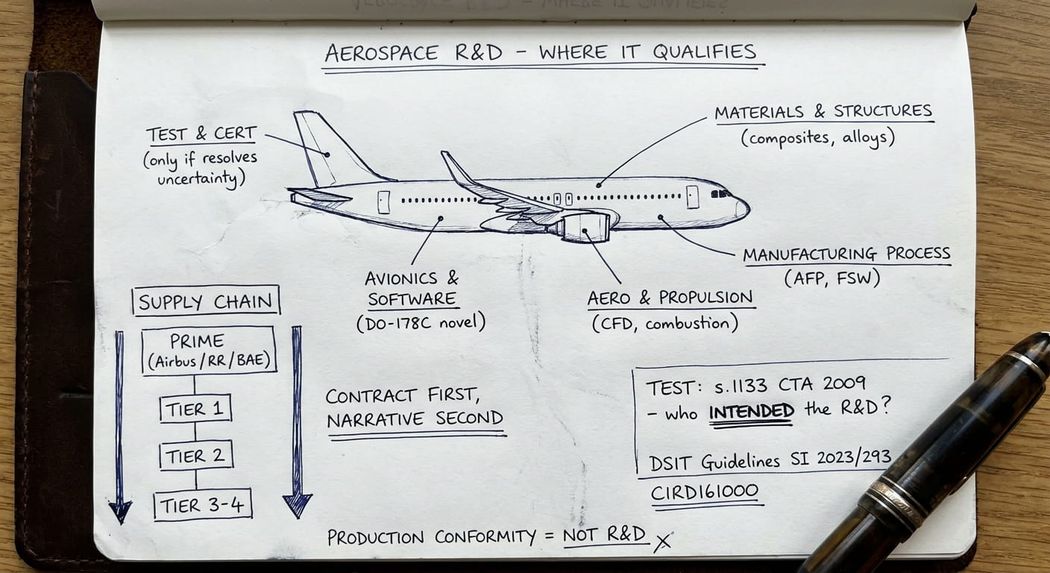

Aerospace qualifying activities: where R&D actually sits

In our experience, aerospace R&D claims fall into a recognisable set of patterns. Each pattern is rooted in genuine scientific or technological uncertainty, not in the routine execution of certification activity.

Materials and Structures

Work consistently qualifies where the project resolves uncertainty in composite layup behaviour, novel alloy performance under combined thermal and mechanical loading, additive manufacturing of safety-critical components, or bonded versus mechanically-fastened joint behaviour. The qualifying boundary sits at the point where uncertainty is resolved. Coupon and element testing that feeds back into design iteration qualifies (DSIT Guidelines paragraphs 33 and 39). Production qualification of an already-resolved design does not.

Aerodynamics and Propulsion

Work qualifies where the project addresses uncertainty in flow behaviour, combustion stability, propulsion integration, or noise and emissions performance. Wind tunnel work, CFD validation against test and design of experiments for novel configurations are routinely R&D. By contrast, parametric optimisation within a well-understood design space using validated tools is engineering, not R&D, even where it is technically demanding.

Avionics and Embedded Software

Work qualifies under paragraph 29 of the DSIT Guidelines where there is genuine system uncertainty: integration of new sensors with legacy buses, real-time data fusion under constrained latency, certification-bound software where the certification basis itself is novel, or autonomy and decision-support code where the underlying algorithms are not in the public domain. DO-178C compliance activity by itself is not R&D. DO-178C compliance of a system where the technological problem could not be readily deduced is.

Manufacturing Process Improvements

Work qualifies where novel processes (automated fibre placement, friction stir welding for aerospace primary structure, novel inspection methods, high-rate composite curing) are developed and the technological uncertainty is resolved through trials and iteration. The DSIT Guidelines at paragraph 9(d) explicitly accept that achieving the same effect by a fundamentally different method qualifies. Many aerospace manufacturing improvements meet this test even where the product itself is mature.

Test and Certification

Work that resolves uncertainty qualifies. Test and certification work that simply demonstrates compliance with a known acceptable means does not. This is the most frequently misread boundary in aerospace R&D claims and is a leading enquiry trigger.

What consistently fails to qualify: Production engineering once the design freeze is in place, conformity demonstration against a known certification basis, design or styling without scientific or technological uncertainty, and commercial activity (bid management, programme management, contractual negotiation).

The contracted-out R&D problem in aerospace supply chains

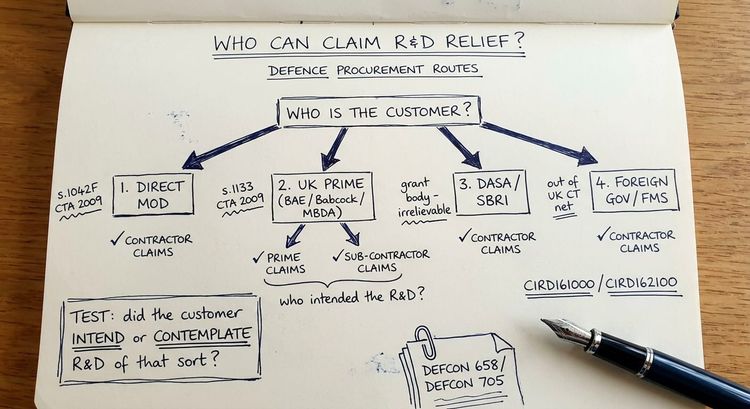

The aerospace supply chain is unusually layered, and the contractual analysis matters more here than in almost any other sector. Most UK aerospace SMEs sit at Tier 2, Tier 3, or Tier 4 in the supply chain to Airbus, Boeing, Rolls-Royce, GKN Aerospace, Safran, MBDA, Leonardo, Thales, GE Aerospace, Honeywell, Collins Aerospace, or to the major UK and US primes through framework agreements.

Under the merged scheme that applies for accounting periods beginning on or after 1 April 2024, the contracted-out R&D rules - set out in Section 1142A of the Corporation Tax Act 2009 - allocate the claim to the party that met the "intended or contemplated" test. The statutory framework looks at whether it is reasonable to assume that R&D of that description was intended or contemplated at the execution of the contract. The detailed application sits in HMRC's manual at CIRD161000 onwards and is highly fact-specific.

In aerospace, the practical pattern looks like this:

- Build-to-Print: Where a Tier 1 prime issues a detailed build-to-print drawing pack, the supplier is rarely the R&D claimant.

- Performance-Based Specs: Where the contract is performance-based and the supplier must resolve genuine technological uncertainty to meet it, owning the underlying design solution, the supplier is typically the claimant.

- Research & Feasibility Grants: Where the contract is a research or feasibility study funded via DASA, ATI, Clean Sky 2, or Horizon Europe pass-through, the supplier is typically the claimant. Crucially, under the merged scheme, grant funding no longer automatically restricts or bars the claim as it did under the legacy SME scheme; the primary test is strictly who contracted the work out under Section 1142A.

The mistake we see most often in aerospace SME claims is preparing the technical narrative first and reviewing the contract afterwards. The contract review must come first. Our manufacturing R&D tax credits specialist guide covers the same supply chain pattern in adjacent industrial sectors, and the analytical framework is identical.

The strongest aerospace R&D claims are the ones where the contract review, the technical narrative, and the cost basis have been built together from the outset. Retro-fitting a claim onto a contract you did not draft around the R&D test is where claims fail.Dual-use technology in aerospace: civilian and defence applications

Dual-Use Technology in Aerospace: Civilian and Defence Applications

A significant proportion of UK aerospace SME work is dual-use. Sensor technology, autonomy stacks, propulsion components, materials, and inspection systems often serve both civilian and defence customers, sometimes through the same engineering team and the same toolchain.

The R&D test does not change because the technology is dual-use. What changes is the documentation. A dual-use claim should be written around the specific scientific or technological uncertainty that arose in the development, not around the end customer. Where the same uncertainty was resolved across civilian and defence variants, that is one R&D project for tax purposes, even if it is two product lines commercially.

What HMRC scrutinises in aerospace R&D claims in 2026

Recent HMRC compliance practice has narrowed and deepened. While the total volume of blunt, automated enquiries has fallen from its peak, the depth, rigour, and technical competency of each enquiry have significantly increased. For aerospace-sector claims specifically, the questions HMRC asks most often are these:

- Who is the competent professional in this project, and what evidence is there of their direct involvement? Generic statements ("our engineering team includes Chartered Engineers") do not meet this test. HMRC expects named individuals with identifiable qualifications and contemporaneous involvement in the work.

- What was the state of overall knowledge in the field at project start? HMRC will challenge claims that simply assert novelty. Reasoned reference to public-domain literature, the prior art search, and the specific gap the project addresses is what holds up.

- For system integration claims, what is the system uncertainty under paragraph 29 of the DSIT Guidelines, and how is it more than routine integration of qualified parts? This is the single most contested area in aerospace claims because system integration sits at the boundary of qualifying and non-qualifying work.

- For dual-use claims, what was the specific uncertainty that distinguished R&D from product development? HMRC is sceptical of claims where the same technology is described as R&D in the corporation tax computation and as a mature product in concurrent marketing or investor materials.

- For contracted work, who instigated the R&D, and what does the contract actually say about technical risk, intellectual property ownership, and design responsibility under Section 1142A? This is where many Tier 2 and Tier 3 aerospace claims unwind.

- How have non-qualifying activities been excluded from the cost basis? Production, conformity demonstration, programme management, and commercial activity all need to be carved out cleanly, with a defensible methodology.

The Additional Information Form (AIF) remains central to enquiry triage. Weak AIF answers, generic technical narratives, or named competent professionals who are not identifiable in the company structure all raise the chance of an enquiry. If you receive an enquiry letter, our guide on how to respond to an HMRC R&D enquiry letter sets out the structured response approach, and our HMRC R&D enquiry defence service page covers the wider position.

Aerospace R&D Claim Cost Categories: Practical Notes

The merged scheme cost categories apply to aerospace claims without sector-specific modification, but a few industry-specific points are worth flagging:

| Cost Category | Aerospace Application & Boundaries |

| Consumables | The most contested category. Material consumed in iterative test articles qualifies. Material consumed in first-article-inspection demonstrators on a finalised design generally does not. Contemporaneous evidence (build records, design freeze documentation) is vital. |

| Externally Provided Workers (EPWs) | Costs from aerospace specialist contractors are frequently misallocated. The EPW test under Section 1128 CTA 2009 focuses on whether the worker is subject to supervision, direction, or control (SDC) by the claimant company. Many contractors meet this but are incorrectly claimed as subcontracted R&D, disrupting the Section 1142A analysis. |

| Software, Data & Cloud | Fully within scope. CFD licences, simulation cloud capacity, and CAD/CAM software used directly in qualifying activity are claimable, apportioned based on actual R&D usage versus standard operations. |

The practical takeaway for aerospace SME CFOs

If your company is a UK aerospace SME, three things move the needle on the value and the defensibility of your aerospace R&D tax credits claim:

- Review the customer contracts before the technical narrative is written. The contracted-out R&D position under Section 1142A CTA 2009 must be resolved upstream. Most failed aerospace claims fail because the contract did not support the position the narrative implied.

- Identify the technological uncertainty at the right level of granularity. Aerospace engineering is full of qualifying activity once you separate genuine uncertainty from compliance with a known certification basis. The DSIT Guidelines reward specificity; generic narratives are immediately flagged by HMRC.

- Document the competent professional involvement contemporaneously. Named engineers with identifiable qualifications, contemporaneous design reviews, and a clear chain of decision-making are the single most powerful evidence in an HMRC enquiry.

For aerospace SMEs operating across civilian and defence markets, or supplying defence primes through dual-use programmes, the contracting and dual-use analysis is where claim value is most often left on the table (and equally often exposed to challenge). A pre-submission review of the position by a specialist with direct HMRC enquiry defence experience is materially cheaper than defending a contested claim two years later.

If you want a view on whether your current aerospace R&D claim methodology is defensible, or if you are facing an HMRC enquiry into an aerospace claim already submitted, reach out for assistance.

Frequently asked questions

Can a UK aerospace SME claim R&D tax credits?

Yes. UK aerospace SMEs can claim R&D tax credits on the same statutory basis as any other sector, primarily under the merged scheme (Chapter 1A, Part 13, CTA 2009) for current accounting periods. The sector-specific issues are the contracted-out R&D analysis with Tier 1 primes, the boundary between R&D and certification activity, and the documentation of dual-use technology.

What aerospace activities qualify for R&D tax credits in the UK?

Aerospace activities that routinely qualify include materials and structures work resolving uncertainty in composites, alloys, additive manufacturing, or bonded joints; aerodynamics and propulsion work involving genuine flow or combustion uncertainty; avionics and embedded software with system uncertainty under paragraph 29 of the DSIT Guidelines; novel manufacturing processes; and test and certification work that resolves uncertainty rather than demonstrating compliance with a known acceptable means.

How do contracted-out R&D rules work for aerospace SMEs supplying primes like Airbus or Rolls-Royce?

Under the merged scheme, contracted-out R&D is allocated under Section 1142A of the Corporation Tax Act 2009 to the party that intended or contemplated that R&D would be required. In aerospace supply chains, build-to-print contracts generally allocate the claim to the customer, while performance-based contracts where the supplier owns the design solution generally allocate it to the supplier. Contract review must happen before the technical narrative is finalised.

Are aerospace certification activities (CS-25, DO-178C, DO-254) R&D for tax purposes?

Certification activity by itself is not R&D. However, where the certification basis is novel, or where the design being certified resolves genuine technological uncertainty that a competent professional could not readily deduce, the underlying engineering work qualifies. The certification artefacts themselves are evidence of the work, not R&D activity in their own right. This is one of the most common areas of HMRC challenge.

Can a UK aerospace SME claim R&D tax credits on dual-use technology serving both civilian and defence customers?

Yes. The end use of the technology, civilian or military, is not the R&D test. The test is whether the project sought an advance in science or technology and resolved uncertainty not readily deducible by a competent professional. Furthermore, under the merged scheme, taking on public grant funding (e.g., from DASA or Innovate UK) to develop this technology does not automatically bar the claim as it did under the legacy SME rules.

How does HMRC scrutinise aerospace R&D tax credit claims?

HMRC scrutiny focuses on identifying the named competent professional, establishing the state of overall knowledge in the field at project start, distinguishing system integration with genuine uncertainty from routine integration of qualified parts, examining the contracted-out R&D position under Section 1142A, and challenging the boundary between R&D and certification activity. The Additional Information Form (AIF) is the primary trigger document for enquiry selection.

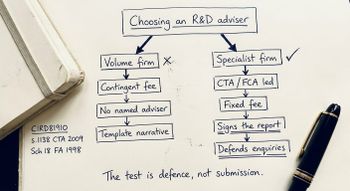

Should an aerospace SME use a generalist accountant or a specialist for R&D tax credits?

For straightforward aerospace claims with no contractual complexity, no dual-use position, and no prospect of HMRC challenge, a competent generalist accountant can prepare the claim. Where the claim involves Tier 1 prime contractor relationships, dual-use technology, material values, or any prior HMRC contact, a specialist with direct enquiry defence experience in the aerospace and defence sector is materially safer. The fee differential is small relative to the disallowance and penalty risk on a poorly defended claim.

Contact us for further assistance.

This is a highly complex technical area so none of the above should be interpreted as professional advice.