To choose an R&D tax credit specialist UK firm properly, the test is not the brochure. It is whether the adviser can still do the work if HMRC opens an enquiry. Most UK R&D firms are built for volume submission. A smaller number are built to defend what they submit. The difference is invisible until things go wrong, at which point the cost of the wrong choice is not a fee dispute, it is the loss of the claim, a penalty and often an investigation the original adviser has neither the skills nor the stomach to handle. The right R&D tax credit specialist has in-house Chartered Tax Adviser or FCA-level leadership, documented HMRC enquiry outcomes, a willingness to sign the technical narrative in their name, and a fee structure that does not depend on the claim going through.

Table of Contents

- Why the R&D tax credit specialist market has two tiers

- When a company actually needs an R&D tax credit specialist

- The six tests that separate genuine specialists from volume firms

- What specialist R&D tax credit work actually looks like

- When an accountant should refer R&D work to a specialist

- Red flags that should end the conversation

- Frequently asked questions about choosing an R&D tax credit specialist UK

Why the R&D tax credit specialist market has two tiers

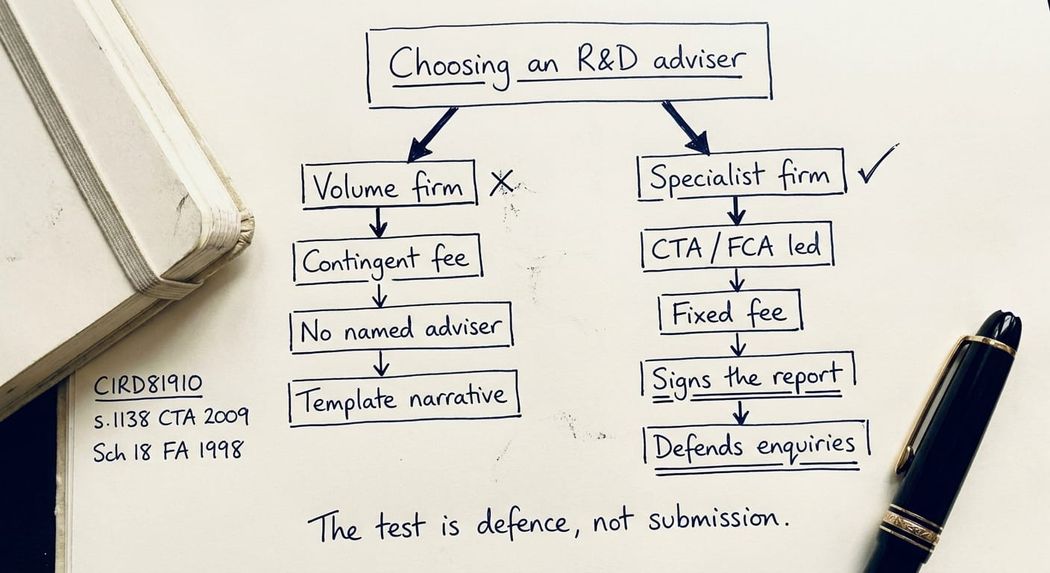

The R&D advisory market splits cleanly into two groups, and most CFOs never see the split until they need the wrong kind of help from the wrong kind of firm.

The first group is the volume submitter. These firms process hundreds or thousands of claims a year on a contingent fee basis, usually between 15% and 30% of the benefit. Their operating model depends on speed at the front end and deflection at the back end. The work is generally competent on straightforward claims and the client experience is polished. When HMRC opens an enquiry, the same firm will usually pass the file back to the client, increase the fee to defend work it has already been paid to produce, or go quiet and let the 30-day clock run.

The second group is the specialist defence firm. These are smaller, almost always led by a Chartered Tax Adviser or a Chartered Accountant with Big Four or equivalent tax background, and built around written technical work designed to withstand scrutiny. Fees are fixed or time-based. The adviser who signs the technical narrative is the same person who will respond to HMRC six months later if the claim is opened up.

Both have a place. A straightforward SME claim for a fifth consecutive year is fine work for a competent volume firm. A first-time claim, a software claim, a claim involving subcontractors or grant funding, or any claim that has already attracted HMRC attention, belongs with a specialist.

When a company actually needs an R&D tax credit specialist

Not every claim needs specialist input. A company is in specialist territory when any of the following apply.

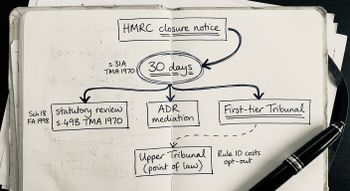

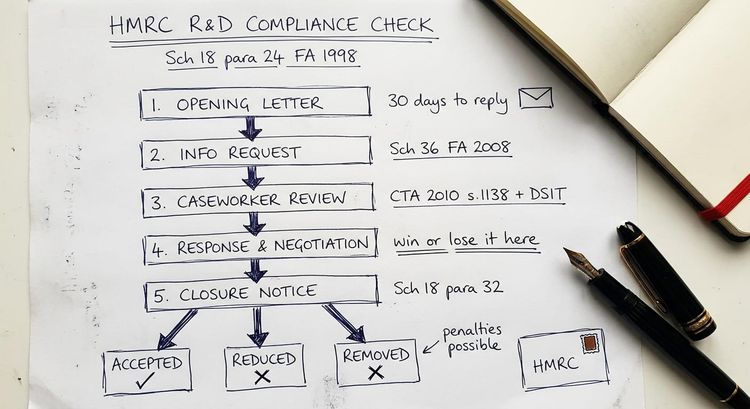

The claim has been opened by HMRC under Schedule 18 FA 1998. Drafting a submission and drafting a response to an information notice are different disciplines. The second requires procedural literacy (paragraph 27, paragraph 32, closure notices, s.49 TMA 1970 review routes) that the volume market rarely carries.

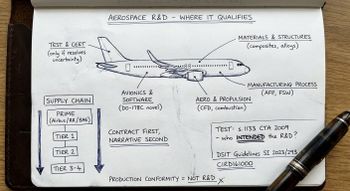

The claim involves software, particularly AI or machine learning. Software remains the leading driver of R&D enquiries and is explicitly called out in CIRD81960 as requiring articulation of baseline, uncertainty, and advance in technological terms, not user-experience terms. A credible software claim today requires an adviser who can read the code, sit with the technical lead, and translate the work into the framework of the DSIT Guidelines at CIRD81910.

The claim involves an overseas element. The April 2024 rules in s.1138A CTA 2009 restrict qualifying subcontracted R&D and externally provided workers to UK-based work, with narrow exceptions. The territorial analysis is judgement, and the judgement is difficult.

The company is claiming under the merged scheme or Enhanced R&D Intensive Support (ERIS). The interaction between scheme eligibility, the intensity test at s.1045ZA CTA 2009, grant-funded project treatment, and PAYE/NIC caps creates computational complexity that volume tooling is not built to handle.

The claim is the company's first. The claim notification regime in s.1142A CTA 2009 has sharp deadlines and a narrow window. Missing it invalidates the claim completely.

The company is in a high-scrutiny sector: life sciences, biotech, fintech, defence, industrial manufacturing with software content. Each draws enquiry rates above the average, and HMRC evaluates each claim against a sector-specific technological baseline.

The 5 tests that separate genuine specialists from volume firms

After fifteen years in R&D advisory, including leading the Crowe UK tax partner practice before founding IP Tax Solutions in 2012, I have settled on six practical tests that reliably distinguish a genuine R&D tax credit specialist UK firm from a volume submitter dressed up as one.

Test one: the person signing the claim also handles the enquiry. Ask for the name of the specific adviser who will prepare the technical narrative and the name of the specific adviser who will handle an HMRC enquiry. If those are different names, or the firm cannot answer, the structure falls apart the moment defence is needed.

Test two: the lead adviser has a Chartered qualification and a verifiable tax background. Chartered Tax Adviser, ACA, FCA, or equivalent. The single best predictor of technical quality is the qualification of the person who signs the report. Check the regulator's register.

Test three: documented enquiry outcomes. Specialist firms can cite the HMRC enquiries they have defended, the outcomes achieved, and the sectors covered, subject to client confidentiality. Volume firms rarely can.

Test four: the fee structure does not depend on the claim being submitted. Contingent fees create a structural incentive to submit weak claims. Fixed fees, or time-based fees with a ceiling, align the adviser with the company. This is the single most reliable signal.

Test five: the firm is willing to turn work away. A specialist will decline a claim that is not credible. A volume firm will not, because its economics depend on throughput. Treat every first conversation that ends in "yes you have a claim" as disqualifying.

Key takeaway: The quality of an R&D tax credit specialist is not tested when the claim is submitted. It is tested when HMRC opens an enquiry, often a year or more later. Choose on the basis of who you want in the room at that moment, not on who has the slickest onboarding.

What specialist R&D tax credit work actually looks like

Specialist advisory looks different from volume submission, and is often slower.

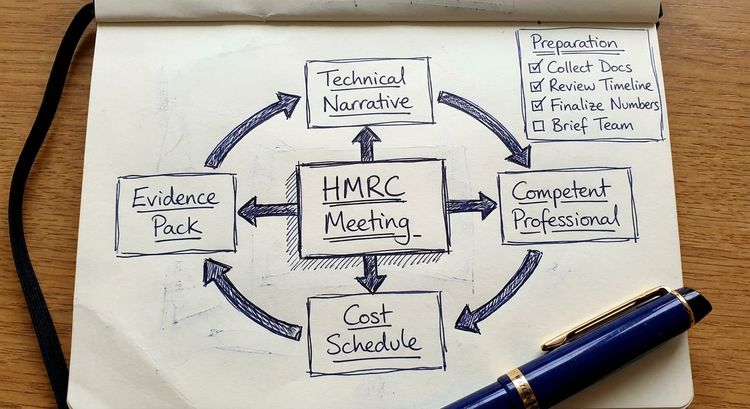

A specialist engagement begins with a scoping review. The adviser reads the prior accounts, the project log, the source code commits or lab notebooks, and any HMRC correspondence on file. The purpose is to map the claim to the statutory definition of R&D at s.1138 CTA 2010 and the computational rules at s.1044 to s.1062 CTA 2009, and to identify weaknesses before they appear in a submission.

The technical narrative is drafted by the person who will sign it, structured around the three statutory tests: technological baseline, scientific or technological uncertainty, and the advance sought. The single most common failure of volume-drafted claims is that they describe business outcomes rather than technological uncertainties. Costing is reconciled on a per-project, per-person basis, at the level required by the Additional Information Form regime introduced in August 2023.

When HMRC opens an enquiry, the same adviser controls the response. The starting point is always to respond to an HMRC R&D enquiry letter inside the 30-day window, with a structured reply that deals with each question individually and ties the answer back to the statute. Where the enquiry escalates, the adviser runs the statutory review, Alternative Dispute Resolution, or First-tier Tribunal process. A specialist who has done this work will have documented R&D tax credit enquiry defence outcomes, including cases where the claim was substantially upheld after HMRC's initial position sought to deny it.

When an accountant should refer R&D work to a specialist

The defensible position for a generalist firm is to handle claims where: the activities are clearly R&D in the statutory sense, the sector is one the firm understands, the quantum is modest, there is no overseas element, no grant funding, and no prior enquiry history. Claims outside that perimeter should be referred to a specialist R&D tax adviser on a transparent basis, with a written scope, a fixed fee, and a clear position on who handles any future enquiry.

Referring out is not a sign of weakness. It is the same judgement accountants make every day on VAT registrations, transfer pricing, and share scheme design. The alternative, which is attempting specialist work on a thin knowledge base and hoping HMRC does not look, has caused a significant proportion of the enquiry volume that has hit the market from 2022 onwards.

Red flags that should end the conversation

- A contingent fee above 25% of the benefit.

- A promise of a specific percentage benefit before the work has been scoped.

- A refusal to name the individual who will sign the report.

- A lead adviser without a Chartered Tax Adviser, FCA, or equivalent qualification.

- A promise to handle any HMRC enquiry at no additional cost (either illusory or priced into every claim).

- No willingness to provide written terms that set out scope, fee basis, enquiry handling, and dispute resolution.

Any one of these should end the conversation.

Frequently asked questions about choosing an R&D tax credit specialist UK

What is an R&D tax credit specialist?

An R&D tax credit specialist is a firm or individual whose practice is concentrated on research and development tax relief under Part 13 CTA 2009 and the related rules in Schedule 18 FA 1998. Genuine specialists include FCA / CTA level leadership, documented HMRC enquiry defence experience and a willingness to sign written technical narratives in their name.

How much should an R&D tax credit specialist charge?

Specialists typically charge fixed or time-based fees, not contingent percentages. A reasonable fixed fee for an SME claim should be possible, depending on complexity. Contingent fees above 25% are a strong signal of a volume-firm model.

Do I need an R&D tax credit specialist if my accountant already prepares my claim?

Not always. If your claim is straightforward, your accountant is experienced in the statute, and there is no enquiry history, a generalist may be adequate. A specialist becomes necessary where the claim involves software, overseas subcontractors, grant funding, high quantum, sector-specific technical uncertainty or any HMRC scrutiny on the file.

What should I look for in an R&D tax credit specialist UK firm?

A named Chartered-qualified lead adviser, documented enquiry outcomes, fixed or time-based fees, a willingness to sign the technical narrative and the Additional Information Form and a written engagement letter that sets out who handles an enquiry and under what fee arrangement.

What is the difference between a volume R&D firm and a specialist?

A volume firm processes thousands of claims a year on contingent fees, with economics that depend on throughput and deflection when scrutiny arises. A specialist processes smaller numbers of claims, charges fixed or time-based fees, is led by Chartered-qualified advisers, and is structured to defend its own work through the full HMRC enquiry and tribunal process.

When should an accountant refer R&D work to a specialist?

When the claim involves software, AI or machine learning, overseas subcontractors, grant-funded projects, the merged scheme or ERIS, a first claim, any prior HMRC scrutiny, or sector-specific complexity the firm does not routinely advise on. Referring out on a transparent basis is compatible with keeping the client relationship.

Closing: the test is defence, not submission

The UK R&D tax credit market is crowded, and much of the volume end is competent at what it does. The problem is that competence at submission is not the same thing as competence at defence, and the difference only becomes visible when HMRC challenges the claim.

If you are choosing now, or your claim has already been opened, the test is simple. Ask for the name of the person who will sign the technical narrative and the name of the person who will respond to HMRC if the file is opened. If those are the same person, and that person is qualified and has the enquiry outcomes to show, you are in the right place. If not, keep looking.

We work with companies and their existing accountants on HMRC R&D enquiry defence and tribunal representation, pre-submission reviews, and specialist narrative drafting. Every engagement is led by a named Chartered-qualified adviser with ex-Big 4 tax partner experience, on fixed or time-based fees, with the enquiry position agreed in writing before any work begins.