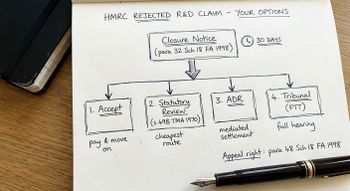

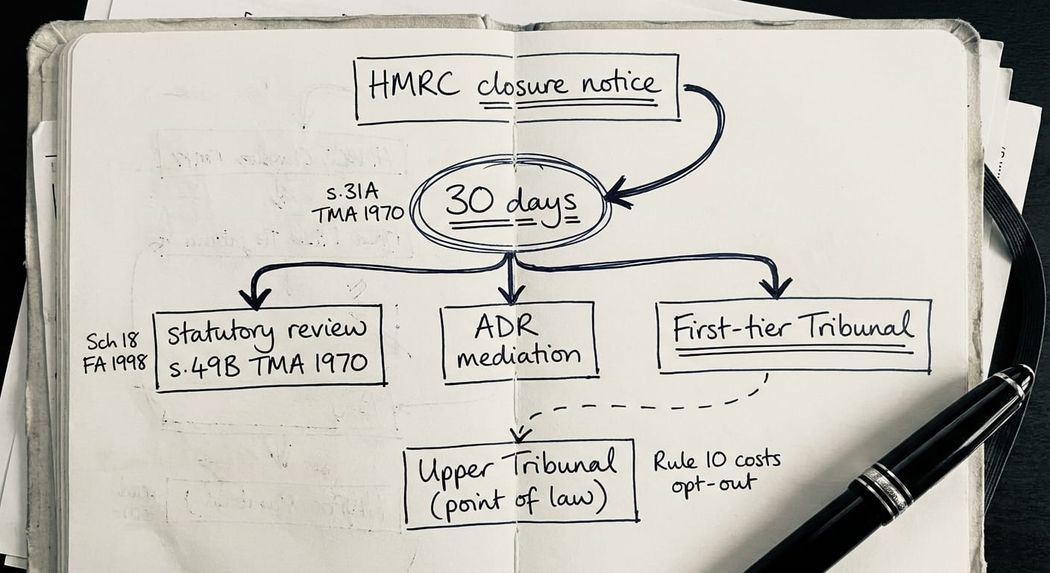

To appeal an HMRC R&D tax credit decision, the company must give notice of appeal to HMRC in writing within 30 days of the closure notice or assessment. From there, three escalation routes run in parallel: a statutory review under s.49B TMA 1970, Alternative Dispute Resolution (ADR) and notification of the appeal to the First-tier Tribunal (Tax Chamber) under s.49D TMA 1970. The appeal right against an amendment made by closure notice sits in paragraph 34 of Schedule 18 FA 1998, which imports the TMA 1970 appeal machinery into the Corporation Tax regime. The 30-day clock controls everything. If it is missed, the only remaining route is to apply for a late appeal, and HMRC does not have to accept one.

Table of Contents

- When do you have an HMRC R&D tax credit decision to appeal?

- Step 1: Lodge the appeal with HMRC within 30 days

- Step 2: Decide between statutory review, ADR, or tribunal

- Step 3: Run a statutory review if the error is legal or procedural

- Step 4: Use ADR where the dispute has stopped moving

- Step 5: Notify the First-tier Tribunal within 30 days of review conclusion

- Step 6: Run the tribunal process itself

- What if you missed the 30-day deadline?

- Frequently asked questions about appealing an HMRC R&D tax credit decision

When do you have an HMRC R&D tax credit decision to appeal?

The right of appeal does not begin when HMRC first signals disagreement. It begins when HMRC issues a decision document that the legislation recognises as appealable. In the Corporation Tax R&D context, that is almost always a closure notice under paragraph 32 of Schedule 18 FA 1998, amending the company's self-assessment to reduce or remove the R&D relief originally claimed. It can also be a discovery assessment under paragraph 41 of Schedule 18 FA 1998, a determination of a penalty under Schedule 24 FA 2007, or a revised decision following an earlier review.

Before the closure notice lands, the company is still inside the enquiry. The right answer during that phase is engagement, not escalation. The framework for how to respond to an HMRC R&D enquiry letter is about evidence gathering, technical narrative work, and structured correspondence, and it is designed to prevent the file reaching the closure notice stage at all. Once the closure notice arrives, the conversation shifts from prevention to procedure.

An appeal also differs from acceptance of an offer. HMRC sometimes closes enquiries by contract settlement under s.54 TMA 1970, where the company agrees a figure in writing and the matter closes without a closure notice. A s.54 agreement is not appealable in the ordinary sense because the right of appeal is settled by the agreement itself. Decide deliberately before signing anything under s.54, because the appeal route closes at the same moment.

Step 1: Lodge the appeal with HMRC within 30 days

The first procedural step after a closure notice is to give notice of appeal to HMRC. The appeal is made to HMRC first, not to the tribunal. Section 31A TMA 1970, as imported into the Corporation Tax regime through paragraph 34 of Schedule 18 FA 1998, sets the deadline at 30 days from the date of the closure notice or assessment. The appeal should be in writing, identify the decision being appealed, and set out the grounds of appeal at an appropriate level of detail.

Two practical points matter at this stage.

- The grounds of appeal do not have to be fully developed at the point of lodging. HMRC expects a statement of the main legal and factual grounds, not a finished legal submission.

- The appeal can be lodged before deciding whether to request a statutory review, apply for ADR, or take the matter straight to the First-tier Tribunal. The appeal itself preserves the company's position. The next strategic decision is which of the three routes to run.

It is also worth knowing that lodging the appeal does not automatically postpone the payment of the tax charged by the closure notice. A separate application for postponement of tax under s.55 TMA 1970 is required. In R&D cases, where a payable credit has been clawed back, the practical payment effect of the closure notice can be significant, and the s.55 postponement application should be made alongside the appeal.

Step 2: Decide between statutory review, ADR, or tribunal

Once the appeal is lodged, the company has three procedural routes available. Under s.49A TMA 1970, HMRC may offer a review, or the company may request one under s.49B. Alternative Dispute Resolution is a separate administrative process offered by HMRC. Under s.49D, the company may notify the appeal to the First-tier Tribunal at any time, subject to the rules on when review offers are outstanding.

Key takeaway: The three routes are not mutually exclusive. A statutory review can sit in front of a tribunal appeal. ADR can run alongside an appeal that has already been notified to the tribunal. The sequencing matters because each route shapes the evidence HMRC will accept at the next stage, and the wrong order can narrow the options that remain.

In my experience, the choice is driven by the nature of the disagreement. If the caseworker has made a clear error of law or misapplied the DSIT Guidelines, a statutory review often resolves the matter quickly and cheaply. If both sides have reached entrenched positions on technical judgement, ADR frequently unlocks movement that neither written correspondence nor tribunal litigation would achieve in the same timescale. If the disagreement is genuinely about how the law applies to the facts and the amount in dispute justifies the cost, the tribunal is the right forum.

Step 3: Run a statutory review if the error is legal or procedural

The statutory review is the first escalation route and the cheapest. Under s.49B TMA 1970, the company can ask HMRC for an independent review by an officer who has not previously been involved in the case. The request must be made within 30 days of the date HMRC notifies the company of the appealable decision. The review itself is carried out by a review officer who has not been previously involved in the case, and is usually completed within 45 days of the review period starting, although extensions by agreement are common.

The statutory review has no tribunal fees, no formal pleadings and no witness evidence. The company submits a written case summarising the technical and legal basis on which the closure notice should be withdrawn or modified. HMRC submits its own case. The reviewing officer reads both and writes a conclusion.

Statutory reviews are most useful where the original caseworker has overlooked evidence that was on the file, has misapplied statutory definitions in s.1138 CTA 2010 or the DSIT Guidelines (which have the force of law through CIRD81910), or has relied on a process point that does not hold up on inspection.

A review is less useful where the disagreement is a matter of pure technical judgement on which reasonable specialists might differ. Reviewing officers are reluctant to substitute their own evaluation for that of the original team on contested technical matters, because that is not what a review is designed to do. If the review upholds the closure notice, the company has a further 30 days from the date of the review conclusion to notify the appeal to the First-tier Tribunal under s.49G TMA 1970.

Step 4: Use ADR where the dispute has stopped moving

Alternative Dispute Resolution uses a trained HMRC mediator, separate from the compliance team, to broker a negotiated outcome. ADR is a non-statutory process but HMRC has published guidance on when it will accept a case. It is particularly suited to R&D disputes where the parties have retreated to written positions, where a shared understanding of the technical facts is the missing piece, or where the tribunal is a poor fit for what is genuinely a communication problem.

ADR is not a soft option. The mediator does not decide the issue, does not make legal findings, and does not substitute for the evidence process. The company still has to bring the technical and financial case, and HMRC still has to justify its position. What ADR does is create a structured day, usually facilitated by video conference in current practice, where both sides can be tested by a neutral voice and can move from entrenched positions without losing face.

Applications can be made at most stages of the dispute, including after the appeal has been notified to the tribunal but before the hearing. If ADR produces a settlement, the outcome is recorded in a written agreement that usually takes effect as a s.54 TMA 1970 contract settlement. If it does not, the matter returns to the tribunal track with no prejudice to either side's position.

Step 5: Notify the First-tier Tribunal within 30 days of review conclusion

If the statutory review upholds the closure notice, the company must notify the appeal to the First-tier Tribunal within 30 days of the date of the review conclusion, under s.49G TMA 1970. If the company has not taken up the review offer, the appeal can be notified to the tribunal at any time after lodging with HMRC, subject to the procedural windows in s.49D and s.49H TMA 1970.

Notification to the tribunal is made on form T240, or through the online tribunal appeal service. The form records the decision being appealed, the amount in dispute, and the grounds of appeal. The procedural rules are the Tribunal Procedure (First-tier Tribunal) (Tax Chamber) Rules 2009 (SI 2009/273). At this stage the tribunal will classify the case as default paper, basic, standard or complex. R&D tax credit appeals are almost always allocated to the standard or complex category, because the technical issues and the quantum involved justify full procedural treatment.

The two procedural diaries diverge materially from this point. Standard category cases move faster and with lighter procedural burden, but still involve lists of documents, witness statements and a hearing. Complex category cases follow rules closer to High Court procedure, including disclosure, expert evidence where appropriate, and costs on the loser-pays basis unless the company opts out of the costs regime under rule 10(1)(c) of the 2009 Rules. The opt-out decision should be made deliberately, early, and with advice, because it is binary and difficult to reverse.

Step 6: Run the tribunal process itself

The tribunal process itself follows a predictable sequence. HMRC serves its statement of case. The company serves a reply. Both sides produce lists of documents and exchange witness statements. The hearing is usually held at the First-tier Tribunal (Tax Chamber) venue closest to the company's registered office. Judgments are handed down in writing, usually within three months of the hearing, and are published on the Tribunals Service website.

The most common grounds on which R&D appeals succeed at tribunal are:

- that the work does in fact meet the s.1138 CTA 2010 definition and the DSIT Guidelines once the evidence is tested,

- that HMRC's reasoning relies on factual assumptions that do not survive cross-examination. The recent case law, including Tills Plus, Stage One Creative Services, Get Onbord, Strictly Money and the LR R&D LLP decision, shows the tribunal engaging closely with the technical substance and not simply deferring to HMRC's view. That pattern is useful to the company that has prepared properly.

Appeals from the First-tier Tribunal lie to the Upper Tribunal (Tax and Chancery Chamber), but only on a point of law and with permission. In practice, the First-tier Tribunal is the forum in which the R&D technical and factual case is won or lost.

What if you missed the 30-day deadline?

Missing the 30-day deadline is not fatal in every case but it narrows the options sharply. Under s.49 TMA 1970, HMRC may accept a late notice of appeal if the company had a reasonable excuse for the delay and acted without unreasonable delay once the excuse ended. If HMRC refuses, the company can apply to the First-tier Tribunal to admit a late appeal. The tribunal's discretion is exercised against the factors identified in Martland v HMRC [2018] UKUT 178 (TCC): the length of the delay, the reasons for it, and the consequences for both sides.

The tribunal looks carefully at whether the company took prompt advice once the closure notice was received, whether the delay was caused by administrative confusion rather than inattention, and whether admitting the late appeal would prejudice HMRC. Applications are not guaranteed to succeed, and a late appeal is always harder than a timely one. The best protection is operational: if a closure notice lands, put a diary entry for 21 days and another for 28 days, and get the appeal drafted and lodged inside those two markers.

If you are preparing to appeal an HMRC R&D tax credit decision, the work on the appeal itself, the statutory review case, the ADR application and the tribunal pleadings are all connected. Getting them right needs specialist R&D tax credit enquiry defence experience and a clear view of how the three routes interact in practice. If you want to talk through a specific case, contact Steve Livingston FCA at IP Tax Solutions on 0161 961 0096 or at stevelivingston@iptaxsolutions.co.uk.

Frequently asked questions about appealing an HMRC R&D tax credit decision

What is the time limit to appeal an HMRC R&D tax credit decision?

The time limit to appeal an HMRC R&D tax credit decision is 30 days from the date of the closure notice or assessment. Section 31A TMA 1970, imported through paragraph 34 of Schedule 18 FA 1998, sets the deadline. A late appeal can only be made with HMRC's agreement or with the permission of the First-tier Tribunal under s.49 TMA 1970, and neither is guaranteed.

What is the difference between a statutory review and a tribunal appeal?

A statutory review is an internal HMRC process under s.49B TMA 1970 in which an officer who has not been previously involved in the case reviews the decision. It has no tribunal fees and no formal procedural rules. A tribunal appeal is a judicial process before an independent First-tier Tribunal judge, governed by the Tribunal Procedure Rules 2009. The review is cheaper and faster but narrower in what it can re-open. The tribunal can consider the full factual and legal case.

Can I use ADR to appeal an HMRC R&D tax credit decision?

Yes. Alternative Dispute Resolution is available at most stages of an R&D tax credit dispute, including after the appeal has been notified to the tribunal. ADR is not a substitute for the appeal itself, because the mediator does not decide the issue, but it is frequently effective where both sides have stopped moving and a neutral facilitator can unlock a settlement.

How long does it take to appeal an HMRC R&D tax credit decision at tribunal?

First-tier Tribunal appeals in the standard category typically take 12 to 24 months from notification to hearing, and a further 1 to 3 months for the written judgment. Complex category appeals can take 18 to 30 months because of disclosure, expert evidence, and larger case management timetables. ADR and statutory review are materially faster. The statutory review is usually concluded within 45 days of the review period starting.

Do I need a barrister to appeal an HMRC R&D tax credit decision?

You do not need a barrister to appear before the First-tier Tribunal. Companies can be represented by their tax adviser, solicitor, or any other person. In complex category R&D appeals, instructing counsel at or before the hearing stage is often the right choice because the tribunal is used to oral advocacy and the company's case will be stronger for it. The decision is usually made with the tax adviser conducting the litigation strategy and counsel brought in for specific advocacy work.

What happens if I lose the appeal at the First-tier Tribunal?

If the First-tier Tribunal decides against the company, the closure notice stands, the tax and any payable credit becomes due with interest under s.87A TMA 1970, and any penalty assessment takes effect unless separately appealed. The company can apply for permission to appeal to the Upper Tribunal (Tax and Chancery Chamber), but only on a point of law. Permission is first sought from the First-tier Tribunal and can be renewed before the Upper Tribunal if refused.

Can HMRC appeal if I win?

Yes. HMRC can apply for permission to appeal to the Upper Tribunal against a First-tier Tribunal decision in favour of the company, on the same basis (point of law, permission needed). In practice, HMRC appeals selectively, usually where the First-tier Tribunal decision has implications beyond the individual case. A well-reasoned First-tier Tribunal judgment, firmly grounded in the evidence, is the best protection against a successful HMRC onward appeal.

This is a highly complex technical area so none of the above should be interpreted as professional advice.