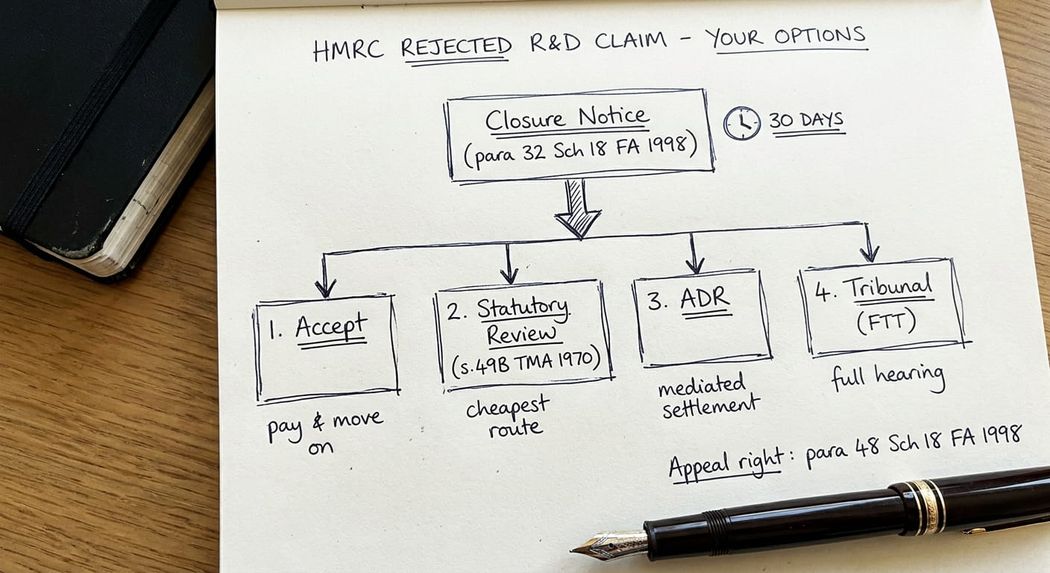

If HMRC has rejected your R&D tax credit claim, four options remain open. You can accept the closure notice and pay any liability. You can request a statutory review under s.49B TMA 1970. You can apply for Alternative Dispute Resolution. Or you can appeal to the First-tier Tribunal (Tax Chamber). Each has its own deadlines, costs, and merits. The right route depends on why HMRC rejected the claim, the strength of the evidence you can now produce, and the commercial exposure on the file. In my experience, the decision needs to be made within days of the closure notice landing, not weeks.

Table of Contents

- What does it mean when HMRC rejects an R&D tax credit claim?

- The four options after rejection

- Option 1: Accept the closure notice

- Option 2: Request a statutory review

- Option 3: Apply for Alternative Dispute Resolution

- Option 4: Appeal to the First-tier Tribunal

- How do you choose the right route?

- Frequently asked questions about an HMRC rejected R&D tax credit claim

What does it mean when HMRC rejects an R&D tax credit claim?

An HMRC rejected R&D tax credit claim is a claim that HMRC has reduced to nil, or materially reduced, at the conclusion of a compliance check. The mechanism is a closure notice issued under paragraph 32 of Schedule 18 to the Finance Act 1998.

The closure notice amends the company's Corporation Tax self-assessment, removes the R&D relief claimed, and recovers any payable credit previously paid to the company. Interest under s.87A TMA 1970 runs from the date the credit was paid.

Most rejections now happen on one of three technical grounds:

- The work does not meet the s.1138 CTA 2010 definition of R&D read together with the BEIS (now DSIT) Guidelines (2023), which have the force of law through CIRD81910.

- Scheme-level failure, for example the pre-notification requirement under CTA 2009 s.1042C/s.1045A being missed, the Additional Information Form being invalid under paragraph 83EA of Schedule 18 FA 1998, or scheme eligibility itself being contested.

- The cost build cannot be reconciled to the general ledger or to the contracts relied on.

If you have not yet reached this stage and HMRC has only opened an enquiry, the approach to how to respond to an HMRC R&D enquiry letter sets out the framework that usually prevents rejection in the first place. Once the closure notice has landed, the conversation changes.

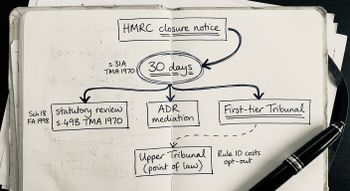

The four options after rejection

The closure notice triggers a 30-day window. Within that window, the company must either accept the notice or take one of three dispute resolution routes. Those three routes are:

- a statutory review,

- Alternative Dispute Resolution (ADR), and

- appeal to the First-tier Tribunal.

These routes are not mutually exclusive. A company can request a statutory review and still appeal to the tribunal if the reviewing officer upholds the amendment. ADR can be run in parallel with an appeal. The sequence matters, though, because each route shapes the evidence HMRC will accept later, and a poorly sequenced escalation often closes off options that would otherwise be available.

Option 1: Accept the closure notice

The first option is to accept HMRC's position. This is not a defeat in every case. Accepting is the right answer where the claim was always going to fail on the technical merits, where the cost exposure is manageable, or where continued engagement would generate legal fees and management time out of proportion to the quantum in dispute.

Acceptance means paying any Corporation Tax liability arising from the amendment, paying back any payable R&D credit already received, and paying interest. Where HMRC has also asserted a Schedule 24 FA 2007 penalty, the penalty assessment is a separate document with its own appeal rights, so accepting the closure notice does not commit the company to accepting any penalty.

One point to watch here: If the company is within the time limits and can identify other qualifying expenditure that was not originally claimed, it may still be possible to file an overlapping amendment under paragraph 15 Schedule 18 FA 1998 to pick up genuine R&D. This is narrow, but it can be deployed successfully where a claim was rejected on scope but the company had a second qualifying project that was never captured.

Option 2: Request a statutory review

The second option is a statutory review. Under s.49B TMA 1970, the company can ask HMRC for an independent review of the decision by an officer who has not previously been involved in the case. The request must be made within 30 days of the closure notice. The review itself is carried out by an officer in HMRC Solicitor's Office and Legal Services (renamed the HMRC Legal Group in January 2025), and usually completes within 45 days, although extensions are common.

The statutory review is the cheapest of the three dispute routes. There are no tribunal fees and no procedural rules to comply with. The company submits a written case summarising the technical and legal basis on which the closure notice should be withdrawn or modified, HMRC submits its own case, and the reviewing officer reads both.

In my experience, statutory reviews succeed where the original caseworker has made a clear legal error, has misapplied the DSIT Guidelines, or has overlooked evidence that was on the file. They rarely succeed where the disagreement is purely one of technical judgement on the facts, because the reviewer is reluctant to substitute their own view for that of the original team on matters of evaluation. The review is worth using as a fast, low-cost filter before committing to tribunal litigation.

If the review upholds the closure notice, the company then has 30 days from the date of the review conclusion to notify an appeal to the First-tier Tribunal.

Option 3: Apply for Alternative Dispute Resolution

The third option is ADR. ADR uses a trained HMRC mediator, separate from the compliance team, to broker a negotiated outcome between the company and HMRC. It is particularly suited to cases where the dispute is as much about communication and framing as it is about law, or where both sides have retreated to entrenched positions and a fresh voice in the room can reset the discussion.

ADR is available at any stage of an enquiry or appeal and does not replace the company's right to a statutory review or tribunal appeal. If ADR fails, those routes remain open. The process is confidential, so anything said in mediation cannot be used against the company later in tribunal.

ADR is most useful on R&D enquiries where the underlying technical case is credible but presentation has been poor, where the competent professional has not yet had the chance to speak to HMRC directly, or where the cost build has been mischaracterised in correspondence. It is less useful where HMRC has made a principled decision on a legal point, because the mediator is not there to override HMRC's view of the law.

Option 4: Appeal to the First-tier Tribunal

The fourth option is a formal appeal. In the Corporation Tax R&D context, the right of appeal against a closure notice is provided by paragraph 34 of Schedule 18 FA 1998. Notice of appeal is given to HMRC within 30 days of the closure notice. The company can then notify the appeal to the First-tier Tribunal (Tax Chamber) at the point of its choosing, subject to the deadlines in the Tribunal Procedure Rules.

A tribunal appeal is a full judicial determination. Evidence is heard, witnesses give oral testimony under cross-examination, and the tribunal applies the statute to the facts as found. The hearing is usually held in public and the decision is published. This last point is important because a published decision creates precedent risk and reputational risk for both sides.

Tribunal proceedings in the First-tier are normally categorised as "standard" for R&D cases, which means costs are not recoverable by either party except where one party has acted unreasonably. The company bears its own legal and expert witness costs regardless of outcome. Full representation on a tribunal hearing including witness preparation and skeleton argument would typically run up significant legal & professional costs (often into six figures), depending on the complexity and the level of cross-examination.

Timing is slower than the other routes. From notice of appeal to final decision is typically 12 to 24 months. Where the amount in dispute is material, this is a period during which interest continues to accrue on any unpaid liability, so the litigation decision has to be weighed against the cost of the delay.

Key takeaway: An HMRC rejected R&D tax credit claim is not the end of the road. Four routes remain open (accept, statutory review, ADR, tribunal), each with different costs, timelines, and prospects. The closure notice starts a 30-day clock, and the quality of the decision made in those 30 days usually determines the outcome more than anything that happens afterwards.

How do you choose the right route?

The choice turns on five questions. I work through them with clients in the first 48 hours after the closure notice lands.

The first question is why HMRC rejected. A rejection on a pure point of law, such as scheme eligibility or the pre-notification requirement, usually belongs in statutory review or tribunal. A rejection on a mix of law and fact, such as the competent professional test, is often better served by ADR. A rejection driven by an evidentiary gap that the company can now close is often resolvable at the review stage if the evidence is credible.

The second question is whether new evidence is available. If the company now holds documents or witness testimony that were not available during the compliance check, that evidence will be more useful in statutory review or ADR than in tribunal, because the tribunal route can raise admissibility arguments if it looks as though the company is running a new case.

The third question is the quantum in dispute relative to legal costs. Where the liability recovered and the penalty assessed run into the hundreds of thousands, tribunal costs become proportionate. Where the exposure is less than £50,000, tribunal is rarely economic even if the company would win on the merits.

The fourth question is whether the company and its advisers are prepared to give evidence under cross-examination. A tribunal hearing places the competent professional in the witness box. If they cannot hold their position under a prepared cross-examination by HMRC's counsel, the claim will usually fall regardless of the technical merits. This is where the quality of pre-litigation preparation matters most.

The fifth question is whether a Schedule 24 FA 2007 penalty has been asserted. Where a deliberate behaviour penalty is on the table, the reputational and director-level exposure can shift the commercial calculus. In those cases, statutory review and ADR are often prioritised precisely because they are confidential and do not produce a published decision.

Frequently asked questions about an HMRC rejected R&D tax credit claim

What does it mean when HMRC rejects an R&D tax credit claim?

An HMRC rejected R&D tax credit claim is a claim that HMRC has reduced to £nil, or materially reduced, by a closure notice issued under paragraph 32 of Schedule 18 FA 1998. The closure notice amends the company's Corporation Tax self-assessment, recovers any payable credit already received, and triggers interest. The company then has 30 days to accept the notice or to start a dispute resolution route.

How long do we have to respond after HMRC rejects an R&D claim?

Thirty days from the date of the closure notice. Within that window, the company must either accept the amendment or request a statutory review, apply for ADR, or give notice of appeal to HMRC. Missing the deadline does not always extinguish the right to appeal, but the tribunal has a discretion to refuse a late appeal and will scrutinise the reasons for delay.

Can we request a statutory review without appealing to tribunal?

Yes. A statutory review is a self-contained process under s.49B TMA 1970. The company does not need to notify a tribunal appeal to request one. If the review upholds the closure notice, a further 30-day window opens during which the company can notify the appeal to the tribunal. Statutory review is typically the first step because it is the cheapest and quickest route.

Is ADR the same as a statutory review?

No. Statutory review is a paper review by a senior HMRC officer who has not previously been involved in the case. ADR uses a trained HMRC mediator to broker a settlement between the company and the compliance team. Statutory review is decision-making, ADR is negotiation. They serve different purposes and can be used in sequence.

What happens to the payable R&D credit we already received?

HMRC will have collected the payable credit through the closure notice. If the original credit was paid in cash, it is recovered as a debt to the Crown and interest runs from the date of original payment. The company can apply to agree time to pay if cash flow is an issue. Any unwound payable credit sits as a Corporation Tax debt on the company's statement of account until it is paid.

Can we bring in a specialist adviser after the closure notice has been issued?

Yes, and in my experience this is the single most common point at which companies switch adviser. A specialist R&D enquiry defence adviser reviews the file, the closure notice, and the correspondence, forms a view on which of the four routes is most appropriate, and takes carriage of the next step. Moving early in the 30-day window is the key to preserving all of the options.

Does rejection by HMRC mean we will also get a penalty?

Not automatically. A Schedule 24 FA 2007 penalty is assessed separately. HMRC has to show an inaccuracy in a return plus a level of culpable behaviour (careless, deliberate, or deliberate and concealed). A company can have its claim rejected without a penalty where the error was made despite reasonable care. Where a penalty is asserted, it has its own 30-day appeal right that runs in parallel to the closure notice appeal.

If your R&D claim has just been rejected

The 30-day window following a closure notice is the period during which the company's options are most open. I act for companies and for accounting firms on behalf of their clients under the specialist R&D tax credit enquiry defence service. The initial review is fixed-fee and produces a recommendation on whether to accept, request statutory review, apply for ADR, or notify an appeal. If you have a closure notice on an R&D tax credit claim, or you can see one coming, it is worth a conversation before the clock runs down.

Steve Livingston FCA is the founder of IP Tax Solutions Ltd. He is a former KPMG-trained tax professional and former tax partner at a Top 10 firm. He handles R&D tax credit enquiry defence, pre-submission claim reviews, complex SEIS/EIS structuring, Patent Box and EMI scheme advisory. He can be reached at 0161 961 0096 or stevelivingston@iptaxsolutions.co.uk.