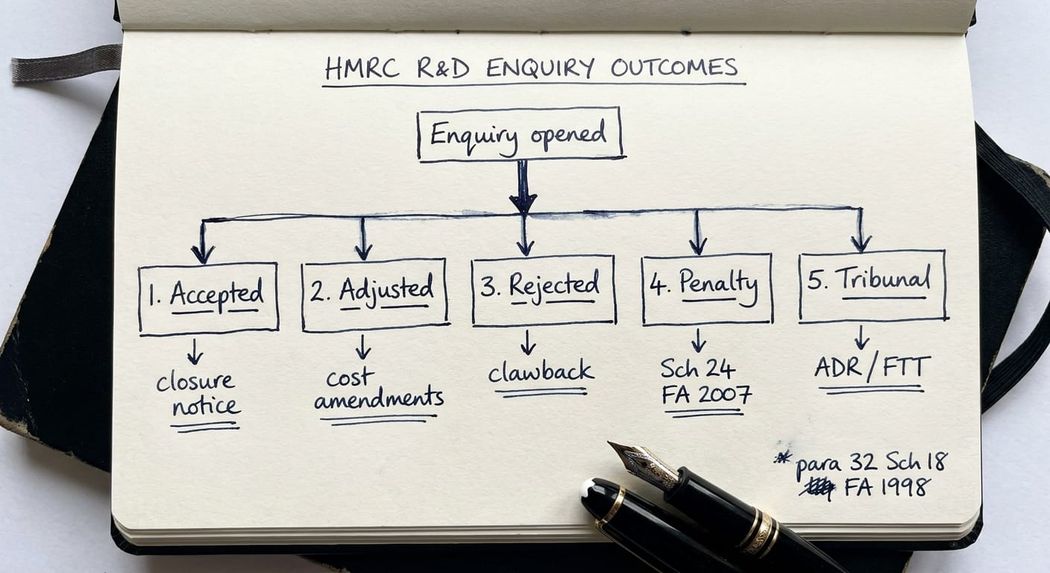

An HMRC R&D enquiry outcome usually falls into one of five categories.

- the claim is accepted broadly as filed,

- accepted with cost adjustments,

- reduced materially in scope,

- rejected in full with clawback of any repayment,

- or rejected with a Schedule 24 FA 2007 penalty.

A small number of cases escalate to statutory review, Alternative Dispute Resolution or the First-tier Tribunal. Which of these outcomes you land on depends on the quality of the original claim, the quality of your response to HMRC, and whether you have specialist representation on the file. In my experience, the outcome is decided within the first three exchanges with HMRC, not at the end.

Table of Contents

- Why the possible HMRC R&D enquiry outcome matters from day one

- The five typical HMRC R&D enquiry outcomes

- Outcome 1: Claim accepted broadly as filed

- Outcome 2: Claim accepted with cost adjustments

- Outcome 3: Claim reduced materially or rejected in full

- Outcome 4: Rejection with Schedule 24 FA 2007 penalties

- Outcome 5: Escalation to statutory review, ADR or tribunal

- What actually drives the outcome

- Frequently asked questions about HMRC R&D enquiry outcomes

Why the possible HMRC R&D enquiry outcome matters from day one

When an enquiry letter lands, the company and its adviser tend to focus on answering the immediate questions. That is natural, and it is the right short-term move. The framework set out in how to respond to an HMRC R&D enquiry letter covers that first step in detail.

The longer-term question, though, is where the enquiry ends. HMRC has been clear since 2024 that it is moving from volume-driven campaign enquiries to more targeted reviews on higher-value and more complex claims. That change does not make enquiries easier. It makes them more precise. When an enquiry is opened now, it is increasingly because HMRC has identified a specific concern in the claim, which means the realistic range of outcomes has narrowed from "explain and close" to something more demanding.

Knowing the range of outcomes available, and what decides between them, lets the company and its adviser shape their strategy on day one rather than discover the destination three letters in.

The five typical HMRC R&D enquiry outcomes

Most R&D enquiries close on one of five outcomes. The categories below are the ones I see consistently in practice. They map onto HMRC's own internal decision framework and onto the statutory tools HMRC uses to give effect to a conclusion.

The five outcomes are

(1) claim accepted broadly as filed,

(2) claim accepted with specific cost adjustments,

(3) claim materially reduced or rejected in full,

(4) rejection combined with a Schedule 24 FA 2007 penalty, and

(5) escalation to statutory review, Alternative Dispute Resolution (ADR) or the First-tier Tribunal.

A very small population of cases sit outside this framework because HMRC has invited the company into Code of Practice 9 on suspicion of deliberate conduct. Those cases are rare and follow a separate process.

Outcome 1: Claim accepted broadly as filed

The best outcome is that HMRC reads the response, tests the supporting file against the Additional Information Form and the technical narrative, and closes the enquiry with no adjustment. This usually happens where the claim was well constructed in the first place, the competent professional is clearly identifiable, the cost build reconciles to the general ledger, and the response answers the questions asked without introducing new material.

"Accepted" does not always mean a silent close. HMRC will often issue a closing letter confirming it has completed its compliance check and is not making amendments under paragraph 32 of Schedule 18 to the Finance Act 1998. That closing letter is the only positive record of the enquiry conclusion.

Outcome 2: Claim accepted with cost adjustments

The next most common outcome is acceptance with specific cost adjustments. HMRC agrees that qualifying R&D took place but takes issue with particular expenditure entries. Typical adjustments now centre on staff cost apportionments, externally provided worker (EPW) arrangements under the reformed scheme, subcontracted R&D where connection or purpose is ambiguous, consumable items (e.g. under s.1126 CTA 2009 that were incorporated into a product sold to a customer), and overseas expenditure with new restrictions for periods beginning on or after 1 April 2024.

The result is often a revised claim value agreed by correspondence, followed by an amendment to the CT600 under paragraph 34 Schedule 18 FA 1998. If the claim was a payable credit, HMRC will clawback the overpaid element. Interest runs on the overpayment from the date of receipt. HMRC may also seek penalties.

Outcome 3: Claim reduced materially or rejected in full

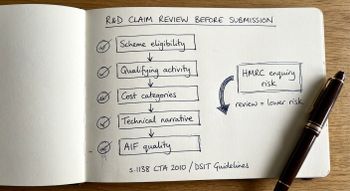

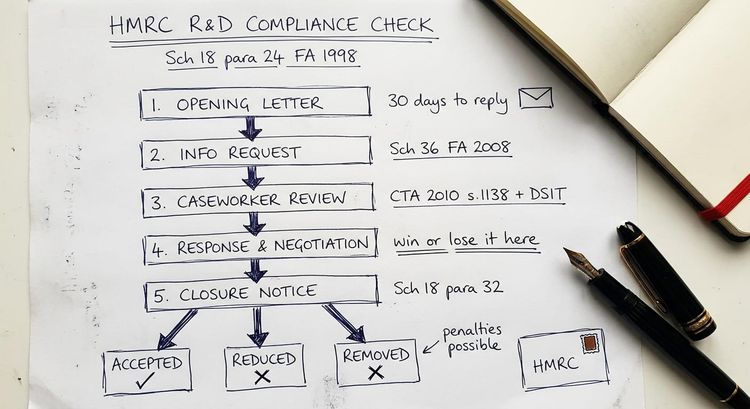

A more serious outcome is material reduction or full rejection. HMRC can reach this outcome on any of three grounds. Either the project does not meet the s.1138 CTA 2010 definition of R&D read with the DSIT Guidelines (2023), or the cost build cannot be evidenced, or the claimant fails a scheme-level condition (scheme eligibility, pre-notification under para 83EA Schedule 18 FA 1998, AIF validity).

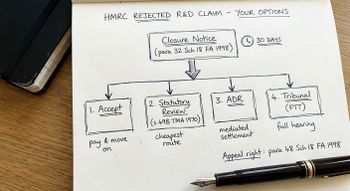

Where HMRC concludes the claim fails in full, it issues a closure notice under paragraph 32 Schedule 18 FA 1998 reducing the claim to nil, recovers any payable credit, and updates the corporation tax position. Interest runs on the recovered amount. The company has thirty days to accept the closure notice or to request a statutory review or appeal to the First-tier Tribunal.

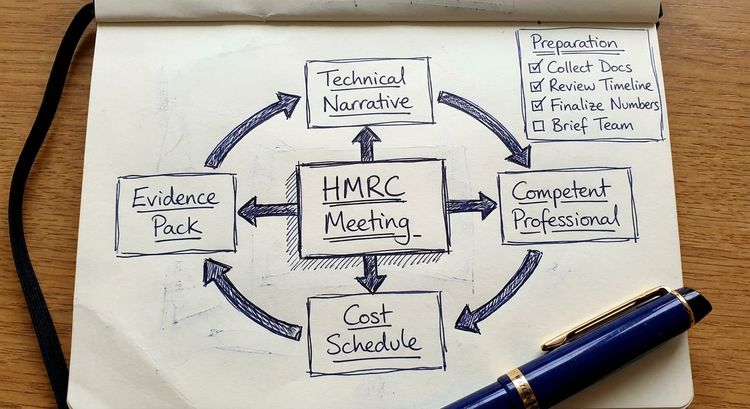

In my experience, the difference between a full rejection and a partial acceptance is often decided by whether the company can produce a credible competent professional who answers HMRC's questions fluently, and whether the technical narrative stands up when read against publicly available information about the product.

Outcome 4: Rejection with Schedule 24 FA 2007 penalties

Where HMRC concludes the claim contained an inaccuracy, it can charge a penalty under Schedule 24 FA 2007 in addition to recovering the claim. The behaviour determines the penalty range. A careless inaccuracy attracts a penalty of up to 30% of the potential lost revenue. Deliberate but not concealed is up to 70%. Deliberate and concealed is up to 100%. Reductions for disclosure, cooperation and quality of disclosure follow the published penalty reduction tables.

HMRC has been more willing to consider Schedule 24 penalties on R&D since 2023, and the trend has continued through 2025 and into 2026. The penalty is not automatic and has to be assessed separately, which means the company gets an opportunity to respond before the penalty is finalised. Quality of response here matters enormously because it determines whether the claim sits in the "careless" or "deliberate" range.

Where HMRC alleges deliberate conduct, the professional exposure for the adviser who prepared the claim can be material. Firms that have never dealt with a deliberate behaviour allegation are often caught out by how quickly HMRC can move from a technical disagreement to a conduct point.

Outcome 5: Escalation to statutory review, ADR or tribunal

If the company does not accept the closure notice, three escalation routes are available.

- A statutory review by an HMRC officer not involved in the case is available on request under s.49B TMA 1970.

- Alternative Dispute Resolution (ADR) uses a trained HMRC mediator to broker a settlement before litigation.

- Appeal to the First-tier Tribunal (Tax Chamber) is the formal litigation route under s.31 TMA 1970.

Tribunal proceedings take twelve to twenty-four months from notice of appeal to decision. Costs are recoverable only in narrow categories in the First-tier Tribunal standard category. Most enquiries never reach this stage, and the prospect of escalation is often what drives a sensible settlement at review or ADR.

What actually drives the outcome

Four factors decide the outcome more reliably than the content of any single HMRC letter.

- the quality of the original claim pack. Strong claims survive enquiry. Weak claims do not, regardless of how the response is handled. Pre-submission review is the cheapest risk control available.

- the first substantive response to HMRC. HMRC forms an internal view of the claim within the first two exchanges. If the response concedes key points early or contradicts the AIF, the outcome is usually set.

- whether a competent professional can be produced and can speak to the project fluently. A professional who answers in marketing language almost always loses the technical point.

- whether the company has specialist representation. Enquiry defence is a specialist discipline. The adviser who prepared the claim is not always the right person to defend it, particularly where HMRC has raised conduct questions.

Key takeaway: HMRC R&D enquiry outcomes usually fall into five categories. The outcome is decided early, not at the end, and the factors that decide it are the quality of the original claim, the quality of the first substantive response, and whether a credible competent professional and specialist defence adviser are in place on the file.

Frequently asked questions about HMRC R&D enquiry outcomes

What are the typical HMRC R&D enquiry outcomes?

Typical HMRC R&D enquiry outcomes are (1) acceptance of the claim as filed, (2) acceptance with specific cost adjustments, (3) material reduction or full rejection on the basis that the claim fails the qualifying activity or expenditure tests, (4) rejection combined with a Schedule 24 FA 2007 penalty, and (5) escalation to statutory review, Alternative Dispute Resolution or the First-tier Tribunal.

How long does an HMRC R&D enquiry take to reach an outcome?

Most enquiries close within three to eighteen months from the opening letter. Simple cost-only enquiries can close within two to six months. Enquiries that escalate to ADR or tribunal can take two to three years from opening letter to final outcome.

Can an HMRC R&D enquiry end without any adjustment to the claim?

Yes. A well-constructed claim supported by a competent professional, a clear technical narrative and a reconciled cost file will often close with no adjustment. HMRC issues a closure notice under paragraph 32 Schedule 18 FA 1998 confirming the compliance check is complete and no amendment is being made.

Will HMRC always charge a penalty if they reject an R&D claim?

No. A penalty under Schedule 24 FA 2007 requires an inaccuracy in a return and a level of culpable behaviour (careless, deliberate, or deliberate and concealed). HMRC can reject a claim without charging a penalty where the error was made despite reasonable care. The penalty is assessed separately from the rejection and the company is entitled to respond before it is finalised.

What happens if we do not accept the HMRC R&D enquiry outcome?

Three routes are available. A statutory review by an independent HMRC officer is available on request under s.49B TMA 1970. Alternative Dispute Resolution uses a trained HMRC mediator. A formal appeal to the First-tier Tribunal (Tax Chamber) is the litigation route. These routes can be used in sequence and each has its own deadlines and procedural rules.

Does HMRC ever concede at the end of an R&D enquiry?

Yes. Where a competent professional gives a compelling technical account, or where the cost build is fully evidenced against the original books, HMRC will drop or narrow its challenge. A structured response with supporting evidence produced at the right point is the most reliable way to produce a concession.

Does the outcome depend on the adviser who prepared the claim?

In part. The quality of the original claim matters, and the record of the preparer will come up if HMRC alleges careless or deliberate conduct. The defence adviser also matters. Specialist enquiry defence experience is the single best predictor of a good outcome, because it informs the tone, structure and sequencing of the response from the first letter.

If an HMRC R&D enquiry letter has already arrived

If HMRC has opened an enquiry into your R&D tax credit claim, the path to a good outcome is set in the first two or three exchanges. The priority is a controlled, evidenced response that anticipates where HMRC is heading and does not concede ground unnecessarily. I act for companies and for accounting firms on behalf of their clients under the R&D tax credit enquiry defence service. Scope and fees are agreed and fixed in advance.

Steve Livingston LLB FCA is the founder of IP Tax Solutions Ltd. He is a former KPMG-trained tax professional and former innovation partner at a top 10 firm. He handles R&D tax credit enquiry defence, pre-submission claim reviews, complex SEIS/EIS structuring, Patent Box and EMI scheme advisory. He can be reached at 0161 961 0096 or stevelivingston@iptaxsolutions.co.uk.