An R&D tax credit claim review before submission is an independent technical and financial check of a completed claim, completed by a specialist adviser who was not involved in preparing it.

The reviewer re-tests the scheme eligibility, the qualifying activity, the cost categories, the subcontractor and externally provided worker (EPW) rules, the technical narrative and the Additional Information Form (AIF). The purpose is not to reduce the claim. The purpose is to ensure the claim that gets filed would survive an HMRC enquiry.

In my experience, the review costs a small fraction of a successful claim and a tiny fraction of the cost of defending a failed one.

Table of Contents

- Why a pre-submission review exists

- What does a proper R&D claim review before submission actually check?

- Which parts of the claim attract the most HMRC scrutiny?

- What does the review process look like in practice?

- When is it too late to bring in a second pair of eyes?

- How much does a pre-submission R&D claim review cost?

- Frequently asked questions about R&D claim reviews before submission

Why a pre-submission review exists

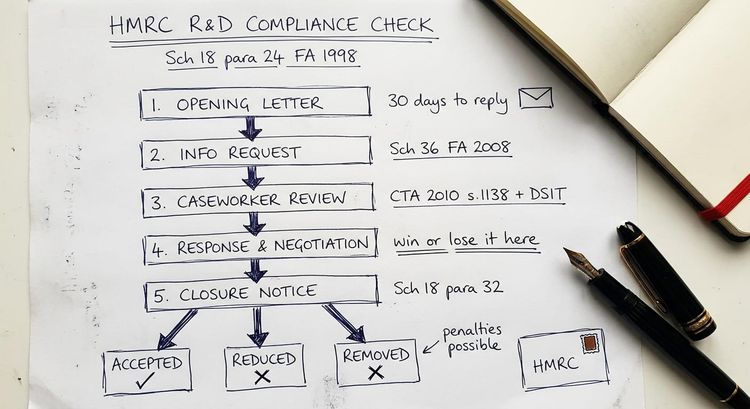

The R&D tax credit enquiry regime has changed shape over the last three years. HMRC's Individual and Small Business Compliance (ISBC) team now opens volume enquiries on small and medium claims, the Fraud Investigation Service picks up the larger or more unusual ones, and the Additional Information Form has turned every claim into a structured dossier that HMRC can triage quickly.

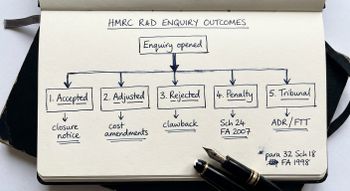

The result is that poor-quality claims now fail at the first line of HMRC review rather than slipping through and being forgotten. A pre-submission R&D claim review exists because the cost of getting the claim wrong has risen. HMRC rejection of a claim, clawback of a repayment, and penalties under Schedule 24 FA 2007 for a careless error are now normal outcomes on claims that would have been accepted quietly five years ago.

The review is an insurance policy and a sense-check. It is carried out by a second, independent specialist. It applies the same technical lens a seasoned HMRC case officer would apply. If it finds a problem, the claim is fixed before it is filed. If it finds no problem, the claim is submitted with supporting documentation that can be produced on demand.

What does a proper R&D claim review before submission actually check?

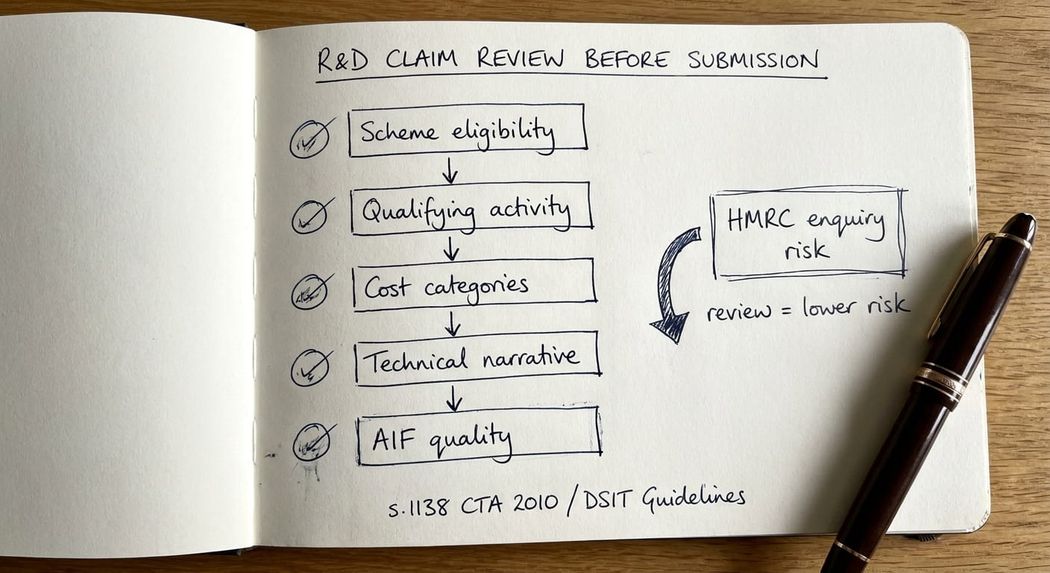

A good pre-submission review is more than a grammar pass over the technical narrative. It re-tests every gate the claim has to pass.

Scheme eligibility comes first.

- Is the company a SME under s.1119 CTA 2010 and the R&D-specific rules in s.1120 CTA 2010, or does it fall into the RDEC/merged scheme population? For periods beginning on or after 1 April 2024, the merged scheme in Part 13 CTA 2009 and the separate ERIS route for R&D intensive loss-making SMEs apply. Most errors I see in scheme selection are caused by missed linked or partner enterprise computations, missed grant funding effects, or subcontract status under the reformed rules.

- Qualifying activity comes next. The project has to pass the s.1138 CTA 2010 definition read together with the DSIT Guidelines (2023), formerly the BIS Guidelines. The review tests whether there is a genuine scientific or technological advance sought, a genuine scientific or technological uncertainty that a competent professional in the field could not readily resolve, and whether the activity ends at the point that uncertainty is resolved. Software claims, bioinformatics, and mechanical engineering projects all attract particular scrutiny on this test.

- Qualifying expenditure is where most money is lost or won. The review re-tests staff cost allocations against contemporaneous evidence, the apportionment of directors' time, the treatment of pension contributions and employer NIC, externally provided workers (including the connected party rules), subcontracted R&D, consumable items and the restrictions for items incorporated into a sold product, and the overseas expenditure restriction introduced for accounting periods beginning on or after 1 April 2024.

- The technical narrative and Additional Information Form are the final stage. The narrative must identify the competent professional, describe the baseline in the field, set out the advance sought, describe the uncertainties, and explain what was done to resolve them. Vague, generic or AI-generated narratives are a leading trigger for enquiries.

Which parts of the claim attract the most HMRC scrutiny?

HMRC's published compliance approach (the Guidelines for Compliance GfC3), the RDCF minutes, and the enquiry patterns I see in my own defence work all point to the same pressure points.

Externally provided workers and subcontractor relationships draw immediate scrutiny, especially if the arrangement is with a connected party or if the counterparty is offshore after April 2024. HMRC tests whether the correct deeming rules have been applied and whether the restricted overseas payments have been properly excluded.

Staff cost allocations are examined closely, particularly for founders and directors whose time is split between R&D and commercial activity. Time records that post-date the claim are treated with scepticism, and retrospective estimates alone will not hold up.

The technical narrative is tested for substance. If the narrative reads like a marketing description of the product rather than a scientific or technological account of the uncertainties faced and the work done to resolve them, the claim is usually opened. HMRC compares the narrative against publicly available information about the company's products, patents and press coverage to check internal consistency.

Pre-notification for new claimants or companies returning after a break is an easy gate to fail. The deadline (six months after the end of the period of account) is absolute, and a missed notification ends the claim before it starts.

A pre-submission review that reaches the same conclusions as a reasonable HMRC case officer gives the company a chance to tighten the weak areas. A review that rubber-stamps the claim without pressure-testing the hard parts is worse than no review, because it adds unearned confidence. Where the review identifies a point that needs specialist defence work, the next step is often a full scoping exercise under the R&D tax credit enquiry defence service rather than submitting the claim as is.

What does the review process look like in practice?

A typical pre-submission review runs in five stages.

- The adviser receives the draft claim pack: the CT600 computation extract, the R&D schedule, the technical narrative, the AIF, supporting time and cost records, the underlying accounts. The review should never be carried out based on the technical narrative alone.

- An internal technical read follows. The reviewer tests the narrative against the DSIT Guidelines, checks internal consistency and flags anything that looks generic, retrofitted or factually thin. A parallel financial read tests the cost build against the evidence file.

- A short technical call with the competent professional inside the business is the most revealing part of the process. Questions are open and specific. What was the state of knowledge in the field at the start of the project? What did the team try first and why did it not work? At what point did the uncertainty end? A competent professional who can answer these questions fluently has almost certainly run a qualifying project. A professional who answers in marketing language or hands over to finance staff usually has not.

- The reviewer then writes a short findings memo. The memo grades the claim (green, amber, red on each gate), identifies fixes before filing, and where necessary recommends removing or reducing specific expenditure categories. If HMRC enquiry risk remains elevated after fixes, the memo says so.

- The final stage is implementation. The original preparer or, where appropriate, a specialist adviser updates the narrative, reworks the cost analysis, and re-files the AIF. The reviewed claim is then submitted.

When is it too late to bring in a second pair of eyes?

Two points in the claim lifecycle really matter. The first is before the claim is submitted, where a review adds value cheaply. The second is after an HMRC enquiry has opened, where the work shifts from review to defence.

If the claim has been filed but no HMRC enquiry has opened, an amendment is still possible within the statutory deadline in paragraph 15 of Schedule 18 to the Finance Act 1998 (broadly, twelve months from the statutory filing date). A review at this point can identify errors that should be corrected by amendment rather than left in place. Voluntary disclosure with a clear technical explanation is almost always better than waiting to be challenged.

If an HMRC enquiry has already opened, a pre-submission review is no longer the right tool. The priority becomes a controlled response to HMRC, starting with the first enquiry letter. The approach I set out in how to respond to an HMRC enquiry letter on an R&D tax credit claim is the right starting point. Trying to perform an internal pre-submission review while an enquiry is live usually creates inconsistencies in the file that HMRC will use against the claim.

How much does a pre-submission R&D claim review cost?

Pre-submission reviews are priced against the size and complexity of the claim, not as a percentage of the benefit. For most SME claims I see, the review fits within a range of £2,500 (plus VAT) to £7,500 (plus VAT). For larger or technically unusual claims, particularly software and merged-scheme cases with significant subcontracted or overseas expenditure, the review can go higher.

Where the review flags issues that need restructuring before filing, the additional work is scoped and priced separately. I quote this openly and do not bundle defence work into the review fee.

For accounting firms who refer the review to me on behalf of their clients, the cost can either be charged directly to the end client (my standard approach) or bundled into the firm's fee (on a disclosed sub-contract basis). Both routes are straightforward commercially, provided the referral is declared and independence is preserved.

Key takeaway: An independent R&D tax credit claim review before submission is a small investment set against the cost of a failed claim, clawback of a repayment and a Schedule 24 FA 2007 penalty. The review re-tests scheme eligibility, qualifying activity, costs, and the technical narrative, and it is most valuable before the claim is filed.

Frequently asked questions about R&D claim reviews before submission

What is an R&D claim review before submission?

It is an independent pre-filing check of a completed R&D tax credit claim by a specialist adviser who was not involved in preparing it. The reviewer re-tests scheme eligibility, qualifying activity, expenditure categories, the technical narrative and the Additional Information Form against the statute (Part 13 CTA 2009, s.1138 CTA 2010), the DSIT Guidelines (2023), and current HMRC compliance practice.

Why would an accountant want an independent second opinion on their client's R&D claim?

Because the cost of getting a claim wrong has risen sharply and because most accounting firms do not run a specialist R&D enquiry defence practice alongside their compliance work. An independent review protects the firm's client and the firm's own file. If HMRC later opens an enquiry, the firm can point to a specialist review on the record. In my experience, referral reviews preserve rather than damage the primary accountant-client relationship.

Will a pre-submission review reduce the R&D claim?

Sometimes. The purpose of the review is not to reduce the claim for its own sake, but to make sure the claim that is filed is defensible. If the review finds that a cost category, a subcontractor arrangement or a project does not meet the statutory test, the correct outcome is to remove it. A claim that survives HMRC scrutiny at a slightly lower value is always better than a higher claim that is rejected in full with penalties.

How long does a pre-submission R&D claim review take?

For a typical SME claim, I plan for five to ten working days from receipt of a complete file. A short technical call with the competent professional is built into the timeline. Larger or merged-scheme claims can take longer, particularly where subcontractor or overseas expenditure analysis is involved.

Can a pre-submission review be done on an R&D claim that has already been filed?

Yes, as long as the statutory amendment window is still open. Paragraph 15 of Schedule 18 to the Finance Act 1998 generally allows amendments within twelve months of the statutory filing date. A review at this point can identify issues that should be corrected by voluntary amendment. If an HMRC enquiry has already opened, the right tool becomes a structured enquiry response rather than a review.

What documents are needed for a pre-submission R&D claim review?

The reviewer needs the draft technical narrative, the Additional Information Form, the R&D cost schedule broken down by category (staff, EPW, subcontracted R&D, consumables, software, data licence and cloud computing costs where applicable), supporting time records, relevant contracts (subcontractor, EPW, consortium, grant), the underlying accounts, the CT600 computation, and the prior year claim and enquiry history if any.

Who should carry out a pre-submission R&D claim review?

Someone who handles R&D tax credit enquiry defence work regularly and is independent of the original preparer. Enquiry defence experience is the single best predictor of a useful review because it tells the reviewer what HMRC actually challenges in practice. A review by someone who has never defended a claim under enquiry is much less useful.

Talk to a specialist before you file

If you are a company finance director preparing an R&D tax credit claim, or an accounting firm partner with a client whose claim feels materially exposed, a pre-submission review is the cheapest risk control available. I carry out pre-submission reviews for companies directly and on referral for accounting firms, and the scope is agreed and fixed in advance.

I advise on R&D tax credit enquiry defence, pre-submission reviews, Additional Information Form quality control, and technical narrative preparation for merged scheme and ERIS claims. If the claim is already in HMRC's hands and a letter has arrived, the starting point is the R&D tax credit enquiry defence service instead.

Steve Livingston FCA is the founder of IP Tax Solutions Ltd. He is a former KPMG-trained tax professional and former tax partner at a Top 10 firm. He handles R&D tax credit enquiry defence, pre-submission claim reviews, complex SEIS/EIS structuring Patent Box computation, and EMI scheme advisory. He can be reached at 0161 961 0096 or stevelivingston@iptaxsolutions.co.uk.