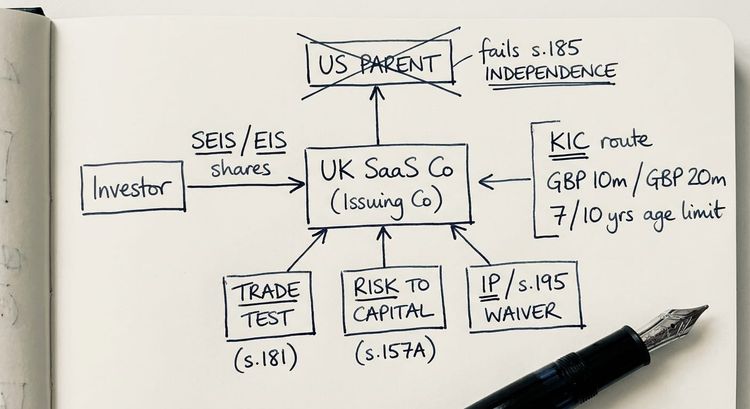

No. A US-incorporated parent company cannot raise EIS investment through a UK subsidiary. EIS relief is only available on shares issued by a company that has a UK permanent establishment of its own and satisfies the independence test in s.185 ITA 2007. Controlling a UK subsidiary does not give the US parent a UK permanent establishment (s.191A(8) ITA 2007), and the UK subsidiary itself cannot act as the EIS issuer because it is a 51% subsidiary of the US parent. The workable routes are for the US parent to establish a genuine UK branch, for the group to insert a new UK holding company at the top, or for a fresh UK trading company to take on the business.

Table of Contents

- Why this question keeps coming up

- What does EIS require the issuing company to prove?

- Does controlling a UK subsidiary give the US parent a UK permanent establishment?

- Can the UK subsidiary issue EIS shares directly?

- What structures actually work for US-incorporated founders?

- What tax planning points come up in practice?

- Frequently asked questions about US parent EIS UK subsidiary structures

Why this question keeps coming up

Founders arrive at this question almost always having built a US-incorporated parent (frequently a Delaware C-Corp) with a genuine UK operating subsidiary. The team is in London, the engineering happens in Manchester, wages are paid in £ sterling. A UK angel round comes together, the angels ask about EIS (Enterprise Investment Scheme), and the obvious thought follows: the UK subsidiary is a UK company, so it must be able to issue EIS-qualifying shares.

I see this pattern in pre-seed deals led by UK angel networks and in corporate finance pitches for cross-border SaaS companies. The assumption is almost always wrong. The cost of learning that after the round has closed is measured in months of restructuring work and, in the worst cases, UK investors losing the reliefs they had been told they would receive.

What does EIS require the issuing company to prove?

EIS relief attaches to shares issued by a company that satisfies a long list of conditions in Part 5 of ITA 2007. For the cross-border parent-subsidiary question, three of those conditions are decisive.

- The UK permanent establishment requirement in s.180A ITA 2007. The issuing company must have a UK permanent establishment throughout Period B (broadly, the date of issue to the third anniversary of issue). This is the compliance window the investor's relief depends on.

- The meaning of permanent establishment in s.191A ITA 2007. A company has a UK permanent establishment if (and only if) it has a fixed place of business in the UK through which its business is wholly or partly carried on, or an agent acting on its behalf habitually exercises authority in the UK to conclude contracts for the company.

- The control and independence requirement in s.185 ITA 2007. The issuing company must not at any time during Period B be a 51% subsidiary of another company or under the control of another company. There is a narrow exception for qualifying subsidiaries of the issuing company, but that works in the opposite direction (issuing company down to subsidiary), not up.

Those three conditions together close the door on the structure founders most commonly propose.

Does controlling a UK subsidiary give the US parent a UK permanent establishment?

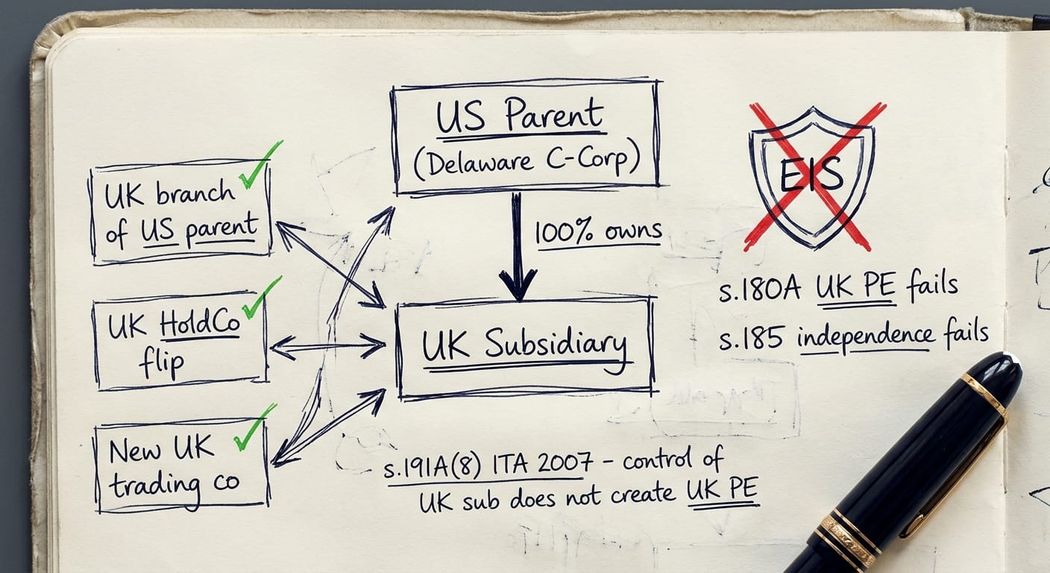

No. This is the specific trap most advisers miss. Section 191A(8) ITA 2007 is explicit: a company is not regarded as having a UK permanent establishment "by reason of the fact that it controls a company that" is UK-resident or carries on business in the UK. So if the US parent owns 100% of a UK operating subsidiary, that fact alone does not give the US parent a UK permanent establishment.

To have a UK permanent establishment in its own right, the US parent must independently satisfy the test in s.191A(2). That means a fixed place of business in the UK (an office, branch, place of management) through which the US parent itself carries on business, or a UK-based agent with habitual contracting authority for the US parent. Having a UK subsidiary that runs its own activities, under its own directors, in its own offices, does not do the job for the parent.

This is the same permanent establishment concept used more widely in UK corporation tax and in tax treaty analysis. For EIS purposes, s.191A is the specific definition that governs, and s.191A(8) is the provision that catches out almost every founder who tries to argue the US parent has a UK PE through its subsidiary.

Can the UK subsidiary issue EIS shares directly?

Also no. The UK subsidiary fails the independence element of the s.185 control and independence requirement because it is a 51% subsidiary of the US parent. A 51% subsidiary cannot be the EIS issuing company.

This block is complete and it cannot be fixed by structuring inside the same group. You cannot carve out the UK subsidiary, give the US parent a preferred share class with limited rights, or attempt to fragment control so that s.185 is somehow satisfied. The statute tests the actual ownership position during Period B, and any arrangements under which control could arise are caught by s.185(1)(b) and (2)(b). Any scheme whose main purpose (or one of its main purposes) is to obtain EIS relief is separately at risk under the EIS-specific anti-avoidance rules.

There is no route to keeping the US parent above the UK subsidiary and having the UK subsidiary issue EIS-qualifying shares. This is the hardest fact for founders to accept because the existing structure usually reflects years of US legal work, investor expectations, and option scheme arrangements that cannot easily be unwound.

What structures actually work for US-incorporated founders?

Three routes typically come into focus when I advise US-incorporated founders who want UK EIS investment.

Route 1: The US parent establishes its own UK branch. The US parent independently sets up a fixed place of business in the UK, with a place of management, employees acting for the parent, and business carried on through that branch. This satisfies s.191A(2) for the US parent itself, so the parent meets the s.180A UK PE requirement. The parent can then issue EIS-qualifying shares. It still has to satisfy every other EIS condition (independence, control, gross assets, qualifying trade, risk-to-capital, trading requirement, age limit), which is a substantial checklist for an established US corporation.

Route 2: Insert a UK holding company (UK HoldCo flip). A newly incorporated UK company becomes the new top of the group, existing shareholders exchange their US parent shares for UK HoldCo shares, and the UK HoldCo issues the EIS round. The US corporation becomes a subsidiary of the UK HoldCo. This is common but mechanically complex. It requires US tax analysis (Section 367, PFIC risk, possible gain recognition), UK analysis on the share-for-share exchange (TCGA 1992 s.135), and HMRC advance assurance for the new holding company.

Route 3: Incorporate a new UK trading company and move the business. In some cases the cleanest answer is a fresh UK company that acquires the trade and assets. The new UK company is genuinely independent, has no US parent above it, and satisfies s.185 on day one. The downside is real commercial displacement: trade, employment contracts, IP, customer contracts and the cap table all move.

Each route has significant US and UK tax consequences that need to be modelled before documents are drafted.

What tax planning points come up in practice?

Several recurring issues deserve highlighting when the structure is designed.

The risk-to-capital condition in s.157A ITA 2007 looks at whether the investment is a genuine growth-intent investment rather than a tax-motivated reorganisation. A structure that exists primarily to unlock EIS relief for US-incorporated founders will attract close HMRC scrutiny on risk-to-capital, and the commercial narrative needs to stand up.

US founders frequently trigger PFIC (Passive Foreign Investment Company) exposure for their US co-shareholders if the UK HoldCo holds mostly investments or cash after the round. This is a US tax problem rather than a UK one, but UK advisers should spot it because it can kill the willingness of US shareholders to support the flip.

Finally, if HMRC later challenges the EIS status after investors have claimed relief, the investors (not the company) suffer the loss of relief and the interest on the clawback. The company bears no direct tax cost from a failed EIS status, but it carries a serious commercial and reputational cost. This is why pre-round structure diligence matters and why I recommend advance assurance on anything cross-border.

Key takeaway: A US-incorporated parent company cannot use a UK subsidiary as an EIS issuing vehicle. The only workable routes involve the US parent establishing a genuine UK permanent establishment of its own, inserting a UK holding company at the top of the group, or incorporating a new UK trading company. All three have significant US and UK tax consequences that need to be modelled before any restructuring begins.

Frequently asked questions about US parent EIS UK subsidiary structures

Can a US parent company qualify for EIS if it opens a small UK office?

Only if the UK office is a genuine fixed place of business of the US parent itself, through which the US parent's business is wholly or partly carried on. A representative office carrying on only preparatory or auxiliary activities (see s.191A(4) and (5) ITA 2007) does not meet the test. The UK branch needs substance: a place of management, decision-making for the parent and real business activity belonging to the parent rather than the UK subsidiary.

Does a US parent with a UK subsidiary automatically have a UK permanent establishment?

No. Section 191A(8) ITA 2007 explicitly provides that a company is not regarded as having a UK permanent establishment by reason of the fact that it controls a UK-resident or UK-trading company. The US parent must independently establish a UK permanent establishment of its own under s.191A(2).

Can we restructure the UK subsidiary to become the EIS issuer?

The UK subsidiary cannot act as the EIS issuer while the US parent remains as its 51% or controlling owner, because s.185 ITA 2007 bars the issuing company from being a 51% subsidiary or under the control of another company. Restructuring therefore means either removing the US parent from the top of the group (a UK HoldCo flip) or moving the business to a new UK company.

What is a UK HoldCo flip and does it need HMRC advance assurance?

A UK HoldCo flip is a share-for-share exchange where a newly incorporated UK company acquires the existing US parent. The US parent becomes a subsidiary of the UK HoldCo, which then issues the EIS round. The UK mechanics rely on TCGA 1992 s.135. The US side needs careful analysis of Section 367 and PFIC risk. Advance assurance from HMRC is strongly advisable and typically takes four to eight weeks. The flip must be completed before the EIS share issue, not afterwards.

Can SEIS work instead of EIS for a US-incorporated founder group?

The same UK permanent establishment and independence conditions apply to SEIS . The answer is the same. A US-incorporated parent with a UK subsidiary cannot use the UK subsidiary as an SEIS issuer, and the US parent itself is unlikely to fit SEIS in practice because of the gross assets limit (£350,000), the three-year company age limit, and the trade limit. SEIS is a harder fit in cross-border structures than EIS.

How long does a UK HoldCo flip take in practice?

From the decision to restructure to a signed EIS round, I plan for six to twelve weeks in a clean case. The time is driven by the US tax analysis, the share-for-share documentation, HMRC advance assurance turnaround, and investor due diligence. Founders who try to compress the flip into two weeks almost always end up with gaps in the compliance record that cause problems later.

Talk to a specialist before you restructure

If you are a US-incorporated founder with a UK operating subsidiary and a UK angel round in view, the structure decision has to come first and the fundraising timetable second. Getting the EIS-qualifying entity right is the foundation every later step rests on. If UK angels have already subscribed on a structure that does not work for EIS, the position is usually recoverable only if it is caught early.

I advise founders, corporate finance teams, and lawyers on S-EIS structures, advance assurance applications for restructured groups and post-issue defence of SEIS/EIS status under HMRC challenge. If you are working through this right now, I am happy to take a first look on a call and give you a direct view on whether the structure you are planning will actually work.

Steve Livingston LLB FCA is the founder of IP Tax Solutions Ltd. He is a former KPMG-trained tax professional and former tax partner at Crowe UK. He handles R&D tax credit enquiry defence, HMRC compliance challenges, complex SEIS/EIS structuring, Patent Box computation and EMI scheme advisory. He can be reached at 0161 961 0096 or stevelivingston@iptaxsolutions.co.uk.

This is a highly complex technical area so none of the above should be interpreted as professional advice.