Most startups raising across more than one funding round get the SEIS and EIS sequencing wrong. A misstep can cost investors their tax relief and expose the company to HMRC challenge. This guide sets out how the rules actually work, what has changed in recent years and where the real risks lie.

What is in this guide

- What is the difference between SEIS and EIS in a funding context?

- Does SEIS always have to come before EIS?

- What happened to the 70% spending rule?

- How do the investment limits work across multiple rounds?

- What company conditions change when moving from SEIS to EIS?

- What is a knowledge-intensive company and why does it matter?

- What are the most common structuring mistakes?

- When does HMRC challenge multi-round SEIS and EIS structures?

- FAQ

What is the difference between SEIS and EIS in a funding context?

SEIS (Seed Enterprise Investment Scheme) and EIS (Enterprise Investment Scheme) are not interchangeable. They target different stages of a company's life and impose different conditions. In practice, most early-stage companies raise SEIS first and EIS later - but the transition between the two is governed by rules that are not widely understood even among experienced advisors.

SEIS is designed for very early-stage companies. The company must have been carrying on a qualifying trade for no more than three years (two years for shares issued before 6 April 2023), have gross assets of no more than £350,000 before the investment, and have fewer than 25 full-time equivalent employees. The maximum that can be raised under SEIS is £250,000 in total (raised from £150,000 for shares issued before 6 April 2023). Investors receive 50% income tax relief and a full CGT exemption on gains if they hold for three years.

EIS is less restrictive in terms of company size but has different caps. In terms of tax relief for the investor: investors receive 30% income tax relief plus CGT deferral.

The company must have gross assets below £30 million immediately before the investment (rising to £35 million after the investment) and fewer than 250 full-time equivalent employees. . The annual risk finance investment limit is £10 million in a rolling 12-month period, with an overall lifetime cap of £24 million. The above reflects the new (doubled) limits for gross assets, annual and life-time limits with effect from 6 April 2026.

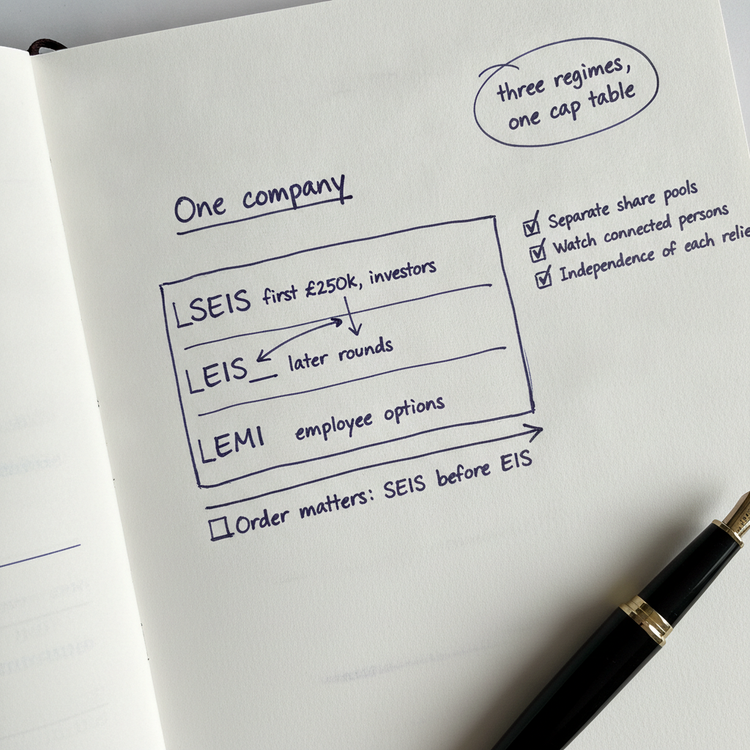

Does SEIS always have to come before EIS?

Yes. This is one of the few bright-line rules in this area, and it derives from s.257DK ITA 2007. A company cannot issue qualifying SEIS shares if it has previously received any EIS investment - meaning a company that has issued shares covered by an EIS1 compliance statement can never subsequently raise SEIS.

The practical consequence is that the sequencing must always be SEIS first, then EIS. There is no mechanism for reversing this order. If a company inadvertently issues EIS shares before completing its SEIS raise - for example, because two investor tranches close in the wrong order - the SEIS eligibility is permanently lost.

It is possible to raise SEIS and EIS in the same investor round, provided the SEIS shares are issued first. The company issues shares up to the £250,000 SEIS limit as SEIS-qualifying shares, then issues further shares as EIS-qualifying shares. Each tranche must meet the conditions of its respective scheme at the date of issue. We recommend allowing one day between share issues to clearly reflect the order of issue timing difference.

What happened to the 70% spending rule?

Many advisors still believe that a company must spend at least 70% of its SEIS funds before it can issue EIS shares. This rule existed under s.173B ITA 2007 but was abolished for shares issued on or after 6 April 2015.

For any EIS share issue today, there is no statutory requirement to have spent a particular proportion of earlier SEIS funding. The VCM guidance (VCM12040) confirms this expressly. A company can issue EIS shares immediately after closing its SEIS round without waiting to deploy the SEIS money, provided all other EIS conditions are met.

This is one of the most persistent myths in early-stage tax structuring. It leads advisors to delay EIS raises unnecessarily, sometimes causing the company to miss the EIS age window or create a timing problem with investor demand.

How do the investment limits work across multiple rounds?

The key limits to monitor across multiple rounds are as follows.

SEIS lifetime cap: £250,000 in total across the life of the company (for shares issued on or after 6 April 2023). This is an absolute ceiling - once reached, no further SEIS raises are possible regardless of how much time has passed.

EIS annual limit: No more than £10 million may be raised in any rolling 12-month period through EIS (and VCT investments count toward this same limit). The rolling 12-month period is calculated from the date each risk finance investment is made - it is not a calendar year.

EIS lifetime limit: Under s.173AA and s.173AB ITA 2007, the company must not have received more than £24 million in total risk finance investments at the date of any EIS issue, and must not exceed that amount during period B (generally three years from the date of EIS share issue). This cumulative figure includes all EIS, SEIS, VCT and approved State aid investments across the company's history.

A company that raised £250,000 in SEIS has already used £250,000 of its lifetime risk finance allowance. Its remaining EIS headroom is £23.75 million (assuming no other risk finance has been received).

For companies raising multiple EIS rounds over several years, tracking the cumulative risk finance position is critical. The compliance statement (EIS1) submitted to HMRC on each round must be consistent with this cumulative position. If the total risk finance exceeds the limits at any point, the affected shares lose EIS qualification.

What company conditions change when moving from SEIS to EIS?

Several conditions apply differently under EIS compared to SEIS, and companies sometimes fail EIS conditions that they easily passed at the SEIS stage.

Gross assets: SEIS requires gross (total) assets below £350,000. EIS permits gross assets up to £30 million before investment (rising to £35 million after investment, from 6 April 2026). A company that has grown significantly between its SEIS round and its first EIS round should verify the gross assets position carefully.

Employee headcount: SEIS requires fewer than 25 full-time equivalent employees. EIS allows up to 249. Most early-stage companies will be well within both limits, but companies that have scaled quickly should check.

Age requirement: EIS imposes a permitted maximum age requirement under s.175A ITA 2007. Standard companies must raise their first EIS investment within 7 years of their first commercial sale. A company that took several years to reach its first commercial sale, then spent further years growing before seeking EIS investment, may find it has already passed this window. If the company has already received a qualifying risk finance investment within the 7-year period, subsequent rounds can continue beyond it, but the first EIS investment must fall within the window (unless it can benefit from one of the narrowly drawn exemptions).

Trading requirement: EIS requires the company to be carrying on a qualifying trade throughout period B - there is no "new qualifying trade" restriction equivalent to SEIS's three-year cap. Companies that have been trading for many years can still qualify for EIS provided the other conditions are met.

Financial health: Both SEIS and EIS require the company to meet the financial health requirement at the date of issue (s.180B and s.257DE ITA 2007). Companies with accumulated losses exceeding half of subscribed share capital may fail this test. In my experience, the financial health condition is the most frequently overlooked condition in later EIS rounds, particularly where the company has been burning cash since its SEIS raise.

What is a knowledge-intensive company and why does it matter?

Companies that qualify as knowledge-intensive companies (KICs) under s.252A ITA 2007 benefit from significantly more generous EIS limits. The annual risk finance limit is £20 million in any rolling 12-month period. The lifetime limit is £40 million. The permitted maximum age window extends to 10 years from first commercial sale rather than seven. These KIC limits also doubled from 6 April 2026.

To qualify as a KIC, the company must meet at least one of two operating costs conditions and at least one of either the innovation condition or the skilled employee condition. The first operating costs condition requires at least 15% of operating costs to have consisted of research and development or innovation expenditure in at least one of the three preceding years. The second operating costs condition requires at least 10% in each of those three years. Either condition independently satisfies the operating costs requirement. The innovation condition requires the company to be creating intellectual property and for it to be reasonable to assume that, within ten years of the share issue, IP exploitation or IP-driven business will form the greater part of the company's business.

For deep technology, biotech, AI and similar companies planning multiple funding rounds, determining whether KIC status applies can be the difference between raising £10 million or £20 million in a single year, and between a 7-year or 10-year investment window. This determination should be made before the first EIS round, not retrospectively.

What are the most common structuring mistakes?

In my practice, I see four mistakes repeated across multi-round structures.

Wrong order. Issuing EIS before SEIS is complete - even inadvertently, through a simultaneous close where EIS investors settle first - permanently blocks any remaining SEIS. This cannot be undone.

Ignoring the age window. Companies assume EIS is available whenever they need it. If the 7-year window has passed (or 10 years for KICs) without a qualifying risk finance investment having been made within it, EIS is no longer available under condition A. Conditions B and C in s.175A can preserve eligibility in limited circumstances, but these are narrowly drawn and require careful analysis.

Failing the financial health test. Companies with loss-making track records and significant accumulated losses may have net liabilities exceeding subscribed share capital by the time they come to raise a later EIS round. The financial health test must be met on the date the shares are issued, and there is limited scope to argue around it once the position is clear.

Share class errors. EIS and SEIS shares must be new ordinary shares carrying no preferential rights (s.173 ITA 2007). Investors who negotiate liquidation preferences, anti-dilution rights or priority dividends may inadvertently create shares that fail the ordinary shares requirement. This is a recurring issue in rounds where legal counsel focused on commercial terms has not engaged with scheme conditions.

When does HMRC challenge multi-round SEIS and EIS structures?

HMRC's compliance activity in the venture capital schemes space has increased significantly since 2022. The most common challenge points in multi-round structures are: the financial health requirement in later rounds, the age condition, and the use of funds requirement where money is not deployed within two years of issue.

HMRC also scrutinises whether the risk-to-capital condition is genuinely met - whether there is a genuine prospect of both capital loss and gain. In structures where investors have preferential protections that substantially reduce their downside risk, HMRC may argue the condition is not satisfied.

If HMRC opens a compliance check on a compliance statement, the consequences can be severe: withdrawal of income tax relief for all investors in that round, loss of CGT exemptions, and potential recovery of relief with interest. Companies that have issued EIS compliance statements across multiple rounds face compounding risk - a finding on one round can prompt scrutiny of others.

Key takeaway: Multi-round SEIS and EIS structures are not difficult to execute, but the margin for error is narrow. The sequencing rules, investment limits and company conditions must be checked at each round. Getting the structure right from the outset is considerably cheaper than defending it later.

Where a compliance check has been opened - or where there is uncertainty about whether past rounds were correctly structured - specialist HMRC enquiry defence advice should be sought before responding to HMRC.

FAQ

Can a company raise SEIS and EIS at the same time?

Yes, provided the SEIS shares are issued before the EIS shares. The company issues shares up to the £250,000 SEIS ceiling as SEIS-qualifying, then issues further shares under EIS. Both tranches must individually meet their respective scheme conditions at the date of issue. We recommend issuing the shares on separate days for completeness.

Is there still a rule that 70% of SEIS money must be spent before EIS can be raised?

No. The 70% spending rule under s.173B ITA 2007 applied only to shares issued before 6 April 2015. It was abolished for all EIS shares issued on or after that date. There is no minimum spending requirement from a prior SEIS raise before EIS can proceed.

How many EIS rounds can a company raise?

There is no limit on the number of rounds, provided the company remains within the annual risk finance limit (£10 million in any rolling 12 months for standard companies, £20 million for knowledge-intensive companies) and the lifetime limit (£24 million or £40 million for KICs). Each round requires a fresh EIS1 compliance statement showing all conditions are met at that date.

What happens if a company fails the financial health test on a later EIS round?

The shares issued in that round cannot qualify for EIS relief. Investors in the affected round cannot claim income tax relief or the CGT benefits. HMRC will not authorise the EIS3 certificates needed for investors to claim. The company may be able to restructure its balance sheet position before the next raise, but relief already missed on a failed round cannot be retrospectively claimed.

Can SEIS investors participate in later EIS rounds?

Yes. An investor who held SEIS shares can also invest in later EIS rounds in the same company. There is no bar on the same individual holding both SEIS and EIS shares. However, the investor must check their connection status - if they have become connected with the company (for example by holding more than 30% of ordinary share capital once all rounds are aggregated) they may not qualify for EIS relief on the later investment.

What is the EIS age limit and can it be extended?

For standard companies, the first EIS investment must be made within 7 years of the company's first commercial sale. For knowledge-intensive companies this extends to 10 years. The window can be preserved beyond the initial period if a qualifying risk finance investment was made within it and subsequent rounds continue in the same qualifying business activity. Extensions outside these parameters are not available.

When should I seek specialist advice on a multi-round SEIS and EIS structure?

Before each round is the right answer, not after. Advance assurance from HMRC is available at both SEIS and EIS stage and provides certainty for investors before they commit. Where a structure involves unusual share classes, complex investor arrangements or a company that is borderline on the age or financial health conditions, specialist review before issue is essential. Fixing a mis-structured round after the event is possible in limited circumstances, but the options narrow considerably once compliance statements have been submitted.

Ready to structure your next round correctly?

If you are preparing a SEIS or EIS raise, planning a transition between the two schemes, or need a second opinion on whether past rounds were correctly structured, I can help. I have worked with companies at every stage of the SEIS/EIS journey, from first-round advance assurance to multi-round compliance reviews and, where necessary, HMRC dispute resolution.

To discuss your specific position, contact me at stevelivingston@iptaxsolutions.co.uk or call 0161 961 0096.