Manufacturing companies are among the largest R&D tax credit claimants in the UK, but they are also among the most frequently challenged by HMRC. The line between a qualifying process improvement and routine optimisation is genuinely difficult to draw, and many claims are either too conservative or too broad. This guide sets out what qualifies under the merged scheme, where HMRC focuses its scrutiny, and what documentation a manufacturing claim needs to withstand examination.

Contents

- What is R&D in a manufacturing context?

- What manufacturing activities qualify for R&D tax credits?

- What does NOT qualify as manufacturing R&D?

- How is the merged R&D scheme different for manufacturers?

- How does HMRC approach manufacturing R&D claims?

- What documentation does a manufacturing R&D claim need?

- When should a manufacturing company seek specialist help?

- Frequently asked questions

What is R&D in a manufacturing context?

R&D for UK tax purposes is a corporation tax relief. The operative test is set out in the DSIT Guidelines (2023), which have legal force for accounting periods beginning on or after 1 April 2023.

The core test requires two things: a project seeking an advance in science or technology, pursued through the resolution of scientific or technological uncertainty. Both elements must be present.

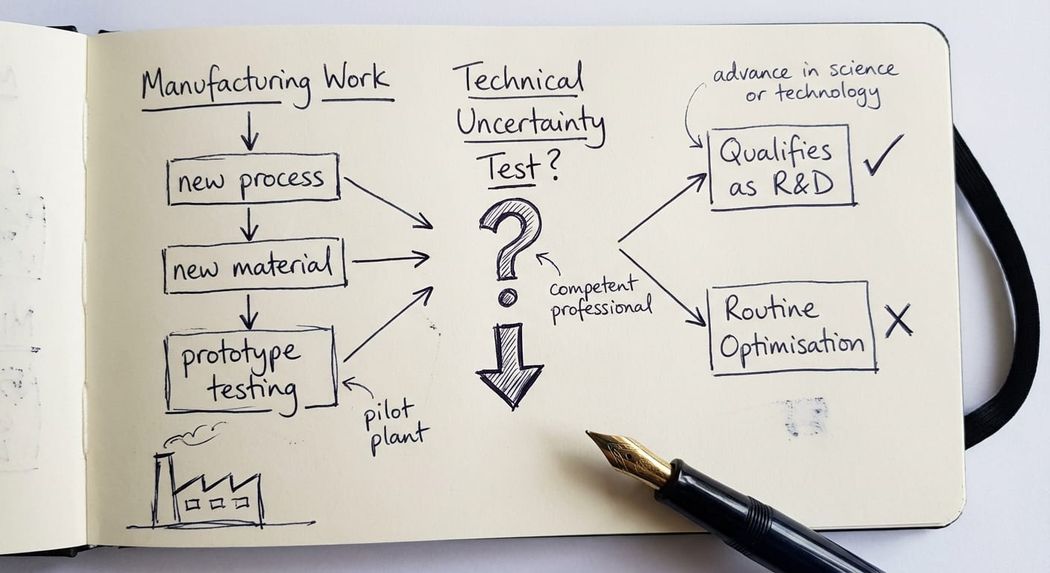

In a manufacturing context, this most commonly arises where a company is trying to develop a new process, a new material, or a new product and the route to achieving the intended outcome is not obvious from existing knowledge. It is not enough that the work is novel to the company. The question is whether the uncertainty exists relative to overall knowledge in the relevant field.

The DSIT guidelines confirm at paragraph 7 that an advance may have "tangible consequences (such as a new or more efficient cleaning product, or a process which generates less waste)". Process-based R&D is explicitly within scope.

What manufacturing activities qualify for R&D tax credits?

New process development. Where a manufacturer is developing a production process that does not yet exist in a form a competent engineer or scientist could implement directly from available knowledge, the design, testing and iteration work can qualify. This includes pilot plant construction: the DSIT guidelines at paragraph 40 confirm that operating a pilot plant while assessing its performance is R&D until the scientific or technological uncertainty has been resolved.

New or appreciably improved materials. Paragraph 9(c) of the DSIT guidelines brings within scope work that makes an appreciable improvement to an existing process, material, device, product or service through scientific or technological changes. The improvement must be genuine and non-trivial, and recognised as such by a competent professional in the field.

Prototype development and testing. Construction and testing of prototypes generally falls within R&D until a prototype with the essential characteristics of the final product has been successfully tested (DSIT guidelines, paragraph 39). In manufacturing, this applies to tooling, moulds and component designs developed to meet technical specifications that required genuine engineering uncertainty to resolve.

System uncertainty in process integration. Paragraph 29 of the DSIT guidelines addresses system uncertainty arising from the complexity of combining elements where the individual components are understood but how they interact is not. A manufacturing company assembling a novel production line from known components may still face genuine technological uncertainty about whether the integrated system will achieve its intended output.

Material science and surface engineering. Work to improve coatings, surface treatments, alloy compositions or material properties can qualify where the outcome was not readily predictable. This is common in aerospace, automotive, and advanced engineering manufacturing.

What does NOT qualify as manufacturing R&D?

Routine process optimisation. Adjusting process parameters within a known framework, using established methods, to improve yield or reduce cycle time is not R&D. The DSIT guidelines at paragraph 14 make clear that optimisations and fine-tuning which do not materially affect the underlying science or technology do not constitute scientific or technological uncertainty.

Implementing existing technology in a new context. A business installing a proven automation system in a new production facility, even if it is the first time that business has used such technology, is not advancing overall knowledge. The question is whether a competent professional in the field could readily achieve the same outcome.

Scaling up a known process. Moving from laboratory scale to full production is generally not R&D once the uncertainty about scalability is resolved. However, where scaling involves genuine uncertainty, for instance whether a reaction will remain stable or a material will retain its properties at production volumes, that uncertainty can itself be a qualifying R&D activity.

Commercial and financial activities. Market testing, product launch planning and administrative work do not qualify, even where directly linked to an R&D project. Paragraph 28 of the DSIT guidelines sets out these exclusions.

How is the merged R&D scheme different for manufacturers?

From accounting periods beginning on or after 1 April 2024, the SME scheme and standalone RDEC were consolidated into a single merged scheme. Most manufacturing companies now claim under this regime.

The credit rate under the merged scheme is 20% of qualifying expenditure (s.1042G CTA 2009). This is an above-the-line credit, brought in as a taxable trading receipt. The net benefit for a profitable company paying corporation tax at 25% is broadly 15% of qualifying expenditure.

The treatment of subcontracted R&D also changed significantly. Under the pre-April 2024 SME rules, a company could claim relief on payments to third-party subcontractors with relatively few restrictions. Under the merged scheme, the rules around connected parties, overseas restrictions, and where economic risk sits are more complex. Manufacturing companies with development work commissioned from third parties should take specific advice on how their expenditure is treated.

How does HMRC approach manufacturing R&D claims?

HMRC has raised the documentary standard substantially. The additional information form (AIF), required for all claims from August 2023, means claims without a properly articulated technical narrative are in a high-risk position from the outset.

In manufacturing, HMRC's common lines of challenge are these. First, the routine objection: HMRC will contend that process improvements described in a claim are routine optimisation rather than R&D. This argument turns almost entirely on how well the technical uncertainty is articulated relative to what a competent professional could have readily deduced.

Second, competent professional identification: the HMRC GfC3 guidance makes clear that a competent professional must have knowledge of the relevant field, awareness of the current state of knowledge, and accumulated relevant experience. A production manager with general engineering experience may not meet the test for a claim involving advanced materials science or novel chemical processes.

Third, project boundary issues: manufacturing claims often include activities that are part of a broader commercial project but do not themselves resolve scientific or technological uncertainty. HMRC focuses on whether the R&D component has been properly separated from routine production expenditure.

If HMRC opens a compliance check on your manufacturing claim, I would recommend reading our guidance on how to respond to an HMRC R&D enquiry letter as a first step in understanding what the process involves.

What documentation does a manufacturing R&D claim need?

The AIF requires you to set out, for each project: the field of science or technology, the advance being sought, the specific uncertainties faced, and why those uncertainties could not be readily resolved by a competent professional.

In a manufacturing context, the documentation should include the following.

- A technical narrative written or approved by a competent professional in the relevant field. This is not a commercial description of the product or process. It must address the scientific or technological uncertainty directly, with reference to the state of knowledge in the field at the time the work was done.

- Records of iterative testing: where a manufacturer conducted multiple trials to resolve process uncertainty, the trial records, test results and evidence of failure and iteration demonstrate that the outcome was not predictable.

- A timeline tracking when each identified uncertainty was encountered and when it was resolved. The DSIT guidelines at paragraphs 33-35 define when R&D begins and ends; the claim should reflect these boundaries.

Cost records allocating staff time, consumables, and subcontractor costs to qualifying activities, separated from production and commercial activities.

When should a manufacturing company seek specialist help?

A manufacturing R&D claim warrants specialist input where: the claim turns on process innovation rather than product development (these are harder to articulate and easier for HMRC to challenge); the competent professional within the business is a production or operations manager without a strong science or engineering academic background; the claim includes significant subcontracted development work; or HMRC has opened an enquiry or issued an information request.

The penalty risk also justifies early specialist involvement. Under the penalty regime introduced alongside the April 2023 reforms, careless or inaccurate claims can attract penalties of 30% or more of the tax benefit claimed. The standard required has risen significantly since 2023.

If you are facing HMRC scrutiny on a manufacturing claim, or want a second opinion before submission, see our R&D tax credit defence service for details of how a specialist review works.

Key takeaway: Manufacturing companies can claim R&D tax credits on process development, material innovation and prototype work, but the claim must rest on a clear articulation of scientific or technological uncertainty. HMRC scrutinises manufacturing claims heavily. A well-prepared technical narrative, with a properly identified competent professional, is not optional. It is the difference between a defensible claim and an exposed one.

Frequently asked questions

Do manufacturing process improvements qualify for R&D tax credits?

Some do and some do not. The test is whether the improvement required resolving scientific or technological uncertainty that was not readily deducible by a competent professional in the field. Routine optimisation and the implementation of established processes will not qualify. Where the manufacturer was working at the boundary of available knowledge, developing a novel reaction pathway or a new joining technique without a known solution, the qualifying R&D can be substantial.

What is a competent professional in a manufacturing R&D claim?

A competent professional is someone with the knowledge, experience, and qualifications to assess whether a scientific or technological advance was being sought and whether genuine uncertainty existed. In manufacturing, this is typically a qualified engineer, materials scientist, or chemist with expertise specific to the project's field. Having worked in manufacturing generally is not sufficient. HMRC's GfC3 guidance specifies that the competent professional must be knowledgeable about the relevant scientific or technological principles, aware of the current state of knowledge in the field and have accumulated experience and a track record in that field.

Can a manufacturing company claim R&D credits for developing new materials?

Yes. Developing a new material, or making an appreciable improvement to an existing material through changes to its scientific or technological characteristics, falls within the definition of qualifying R&D under paragraph 9(c) of the DSIT Guidelines (2023). The improvement must go beyond minor or routine upgrading and must represent something a competent professional in the field would recognise as genuine and non-trivial.

How much can a manufacturing company claim under the merged scheme?

Under the merged scheme, the credit rate is 20% of qualifying R&D expenditure under s.1042G CTA 2009. For a profitable company paying corporation tax at 25%, the net cash benefit is approximately 15% of qualifying expenditure. A loss-making SME that meets the R&D intensive threshold (broadly, qualifying expenditure exceeding 30% of total expenditure) may access a payable credit at a higher effective rate under the separate SME intensive rules, which sit outside the standard merged scheme.

What happens if HMRC challenges our manufacturing R&D claim?

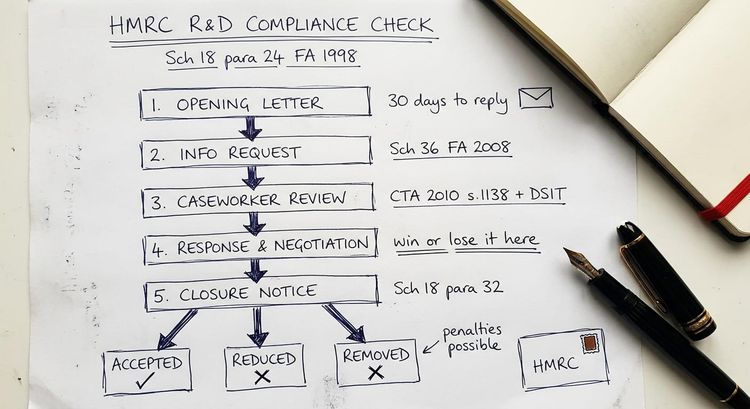

HMRC will open a formal compliance check and issue an information notice requesting supporting documentation. What you submit at this stage shapes the rest of the enquiry. If HMRC's challenge turns on the routine optimisation argument, the response must demonstrate, with reference to the state of knowledge in the relevant field at the time the work was done, why the uncertainty existed. I would recommend instructing a specialist early. Conceding ground at the information stage makes a claim significantly harder to defend at a later point.

What is the merged R&D scheme and does it apply to manufacturing companies?

The merged scheme is the unified R&D relief regime that replaced the pre-April 2024 SME and large company RDEC frameworks for periods beginning on or after 1 April 2024. The vast majority of manufacturing companies, whether SME or large, now claim under this scheme. It operates as an above-the-line credit at 20%, offset against corporation tax liability through the seven-step process in s.1042I.

Can subcontracted R&D work count towards a manufacturing R&D claim?

Under the merged scheme, qualifying expenditure on externally provided workers and subcontracted R&D is included under ss.1042D and 1042E CTA 2009. However, the rules around connected parties, overseas restrictions, and where economic risk sits are materially more complex than the pre-April 2024 SME subcontracting rules. Manufacturing companies commissioning development work from third parties, or acting as a contractor carrying out R&D for a larger customer, should take specific advice on how their expenditure falls within the new rules.

Take the next step

If you are preparing a manufacturing R&D claim, have received an HMRC information request, or want a second opinion before submission, I am happy to have a direct conversation about your position. Contact me at stevelivingston@iptaxsolutions.co.uk or call 0161 961 0096.