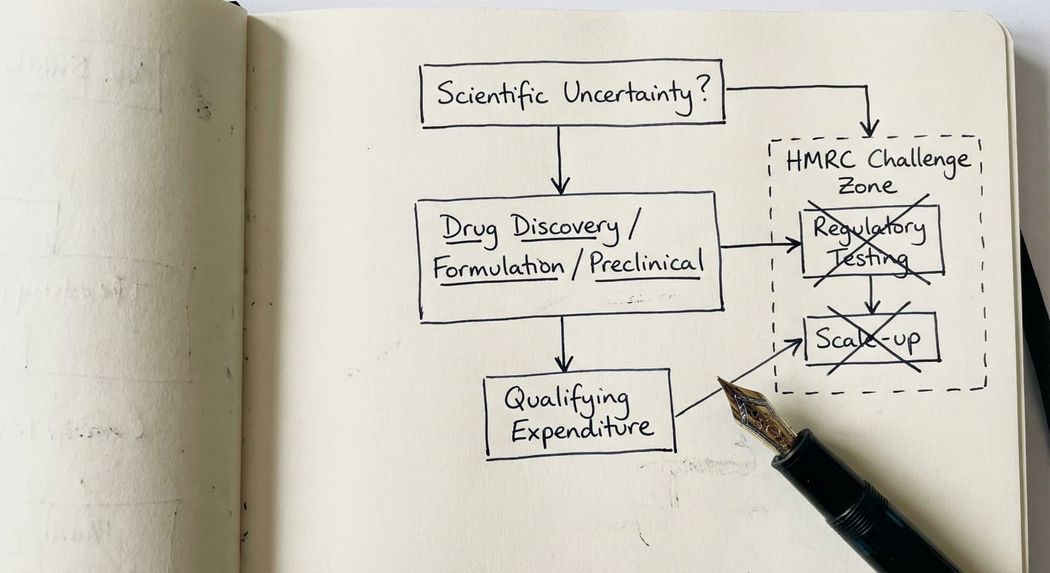

Life sciences and biotech companies carry out genuine scientific research, but that does not mean every activity qualifies for R&D tax credits. The test is specific: there must be a scientific or technological uncertainty that a competent professional in the field cannot readily resolve. Drug discovery, clinical formulation, and novel process development can all qualify. Regulatory testing and manufacturing scale-up usually do not.

What does "R&D" actually mean for a life sciences company?

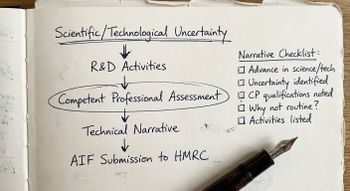

R&D for tax purposes is defined by the DSIT Guidelines (2023) apply to accounting periods beginning after 31 March 2023. For earlier periods, the 2004 guidelines continue to apply.

The core test is straightforward in principle, though demanding in practice: your project must seek to achieve an advance in overall knowledge or capability in a field of science or technology, and there must be genuine scientific or technological uncertainty that a competent professional in the field cannot readily resolve.

Life sciences is explicitly a qualifying field of science. The DSIT Guidelines use pharmaceutical research as an illustrative example at paragraph D1: searching for the molecular structures of possible new drugs, or identifying new uses of existing compounds, constitutes an advance in science or technology. Critically, even where the method used to search (running a computer programme on a particular set of data, for instance) is itself routine, the activity still qualifies if it directly contributes to resolving that scientific or technological uncertainty.

The key point for life sciences companies is this: the scientific complexity of your sector does not automatically make all of your work R&D. The test is applied activity by activity, project by project.

Which life sciences activities qualify for R&D tax credits?

The following types of work commonly qualify in the life sciences sector, provided the specific uncertainty test is met on the facts.

Drug discovery and active compound screening. Searching for new active compounds, identifying new mechanisms of action, or testing novel combinations of known substances to achieve a new or improved therapeutic effect. This sits squarely within the guidelines.

Formulation development. Creating a new pharmaceutical formulation involves genuine scientific uncertainty where existing excipient combinations or delivery mechanisms are not known to achieve the required bioavailability, stability, or patient tolerability. Where a competent professional in the field cannot readily deduce the solution, this work qualifies.

Novel synthesis routes and chemical process development. Developing a new or appreciably improved method for synthesising a known or novel compound, where there is uncertainty about whether the method will achieve the desired yield, purity, or cost efficiency.

Biological assay development and validation. Where developing the assay method itself involves scientific uncertainty rather than the straightforward application of established laboratory procedures.

Preclinical research. Testing novel compounds in vitro and in vivo to assess safety, efficacy, and mechanism of action, where the outcomes cannot be predicted from existing knowledge.

Early-phase clinical development (with important caveats discussed below). Certain Phase I and Phase II activities may qualify where they are directed at resolving scientific or technological uncertainty rather than generating regulatory data about a known outcome.

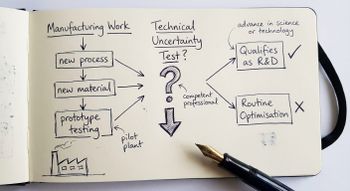

Manufacturing process development for biologics. Bioprocessing and fermentation development, particularly for novel biologics where scale-up from laboratory to production involves genuine technical uncertainty about yield, consistency, or contamination control.

In all cases, the boundary of the qualifying activity must be drawn with care. R&D begins when work to resolve scientific or technological uncertainty starts and ends when that uncertainty is resolved (or work to resolve it ceases). Post-resolution manufacturing, distribution, and commercial activities fall outside the claim.

What does not qualify, and why?

This is where many life sciences claims overreach, and where HMRC challenges arise most frequently.

Regulatory compliance testing. Conducting clinical trials primarily to satisfy EMA or MHRA regulatory requirements does not, of itself, constitute R&D. Where the scientific outcome of a trial is substantially known and the trial is confirming results for a regulatory filing, there is no scientific or technological uncertainty of the kind the guidelines require. HMRC will examine this point carefully.

Standard laboratory procedures applied to new compounds. Applying established analytical methods (HPLC, mass spectrometry, standard toxicology screens) to a new compound, without any scientific uncertainty about the methodology itself, does not qualify. The activity must be directed at resolving uncertainty, not merely generating data.

Manufacturing and scale-up once uncertainty is resolved. The DSIT Guidelines are explicit at paragraph 34: R&D ends when knowledge is codified in a form usable by a competent professional, or when a prototype with all the functional characteristics of the final product is produced. Scaling up a process that is already understood is not R&D.

Post-marketing surveillance and pharmacovigilance. Activities concerned with regulatory post-approval monitoring, patient satisfaction surveys, or commercial acceptance are not R&D.

Minor or routine improvements. The guidelines require an "appreciable improvement" to an existing product or process. Improving tablet palatability by adjusting an existing formulation using known techniques, or reformulating for presentation purposes alone, falls below this threshold.

The consequence of over-claiming is not simply a correction notice. HMRC has the power to open a formal enquiry, disallow the claim with interest and penalties, and in more serious cases to allege negligent or fraudulent misrepresentation. In my experience, life sciences is one of the sectors most likely to face this kind of challenge, precisely because claim values are high and the boundary between qualifying and non-qualifying work is genuinely complex.

How the merged scheme applies to life sciences companies

From accounting periods beginning on or after 1 April 2024, most companies (including SMEs that are not loss-making) claim under the merged scheme, which is based on the RDEC structure at a rate of 20% of qualifying expenditure. This produces a net cash benefit of approximately 16.2% after the credit is taxed at the standard corporation tax rate.

For loss-making SMEs in the life sciences sector, the enhanced R&D intensive support (ERIS) scheme may be available where qualifying R&D expenditure represents at least 30% of total expenditure. The ERIS rate is 27%, producing a net benefit of approximately 21.87% for a 25% rate taxpayer, or a payable credit where the company has no tax liability. Many early-stage biotech and medtech companies fall into this category.

The interaction with grant funding changed materially from 1 April 2024. The subsidised expenditure restriction in the former rules (s.1138 CTA 2009) was repealed by FA 2024, and the conditions for qualifying expenditure under both the merged scheme (ss.1042D-1042F CTA 2009) and ERIS (ss.1052-1053A CTA 2009) do not require expenditure to be unsubsidised. Innovate UK, UKRI, and Horizon Europe grants therefore no longer push grant-funded expenditure out of the claim. This is a significant improvement on the pre-April 2024 SME rules and is particularly relevant for grant-backed life sciences companies, which previously had to split their claims between the SME scheme and RDEC.

Subcontracted R&D arrangements also require careful analysis. Under the merged scheme, the company that bears the financial risk and makes the qualifying decision to undertake R&D is the company entitled to claim. Where a contract research organisation (CRO) is engaged, whether the expenditure qualifies depends on the structure of the contract and who bears the economic risk. This is a live area of HMRC scrutiny.

Why HMRC scrutinises life sciences claims more heavily than other sectors

HMRC has publicly identified large and complex R&D claims as a compliance priority. Life sciences claims attract disproportionate attention for several reasons.

Claim values tend to be high. A mid-size biotech company may have qualifying expenditure of several million pounds in a single accounting period, generating a credit or repayment running into six or seven figures. High-value claims receive proportionally more scrutiny.

The qualifying boundary is genuinely difficult to assess. HMRC compliance officers with R&D portfolios are familiar with common life sciences claim patterns and are increasingly alert to the inclusion of regulatory testing costs, post-resolution manufacturing costs, or costs that cannot be clearly tied to a specific scientific or technological uncertainty.

The technical narrative is often the weakest element of a life sciences claim. In my experience reviewing claims across the sector, the most common failure is not that the underlying work does not qualify, but that the documentation does not articulate the uncertainty at the level of specificity HMRC now expects. The additional information form (AIF) required since 8 August 2023 has raised the bar significantly. HMRC caseworkers use AIF responses to identify claims where the uncertainty description is vague, circular, or inconsistent with the financial data.

If you are concerned that an existing claim may not withstand scrutiny, or if you are already defending an R&D claim against HMRC, taking early specialist advice is almost always the right decision.

How to structure your life sciences R&D claim documentation

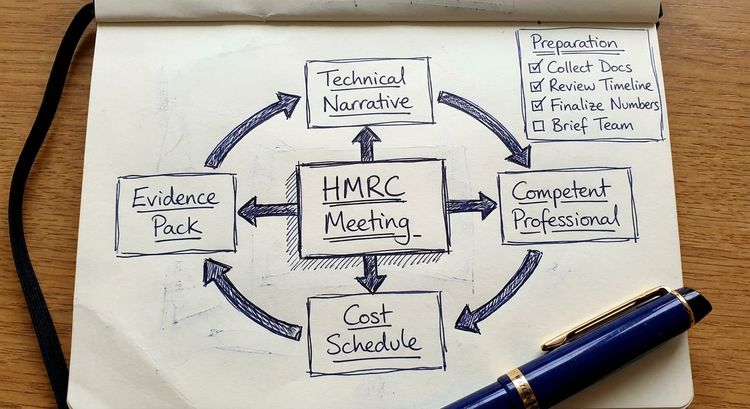

The quality of documentation in a life sciences R&D claim is the difference between a claim that survives HMRC review and one that does not.

For each qualifying project, document the following clearly and consistently.

The scientific or technological uncertainty at the start of the project. This must be stated in terms that a competent professional in the relevant field (not a generalist) would recognise as genuine uncertainty. "We did not know whether compound X would bind to receptor Y with sufficient affinity for therapeutic application" is the right kind of statement. "We were developing a novel drug" is not.

The activities undertaken to resolve that uncertainty. These should be mapped to the stated uncertainty, not described in general terms. If your scientists ran a screening programme, document the approach, the variables being tested, and what was being learned at each stage. If formulation work involved systematic variation of excipient ratios, document the rationale and the specific unknowns being addressed.

When the uncertainty was resolved. R&D ends at a defined point. If a project ran for three years but the technical uncertainty was resolved in year two, the activities in year three need to be considered separately. Documenting the resolution date (or the point at which work ceased) is essential.

Staff time allocation. Laboratory records, project management logs, and timesheet data are all relevant. HMRC expects that staff time attributed to R&D can be substantiated from contemporaneous records, not reconstructed retrospectively from a high-level summary.

The connection between costs and activities. Every line of expenditure in the claim should be traceable to a qualifying activity. Overhead allocations and indirect cost calculations should be documented with a clear methodology.

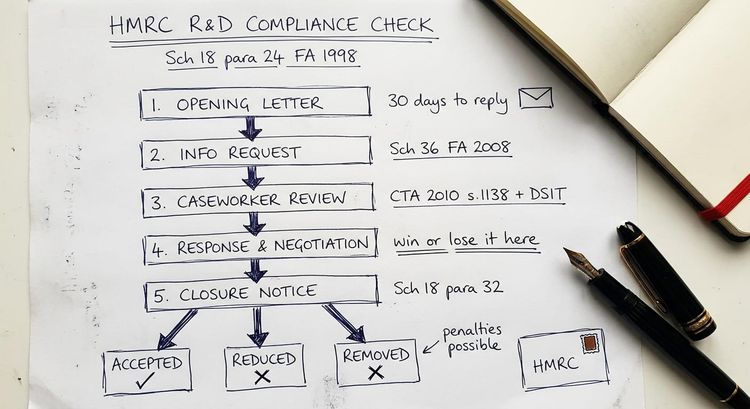

What to do if HMRC opens an enquiry into your life sciences R&D claim

If HMRC opens a formal enquiry (typically by issuing a notice under paragraph 24 Schedule 18 FA 1998 for corporation tax returns), the first step is not to panic. An enquiry is an information-gathering process, not a determination that your claim is wrong.

The enquiry letter will set out a list of questions or information requests. In life sciences cases, these commonly focus on: the basis for including regulatory testing costs; the treatment of costs shared with other projects or group companies; subcontracting arrangements with CROs; and the adequacy of the technical narrative in supporting the claimed uncertainties.

Your response to the initial enquiry letter is the most important document in the process. If your claim was prepared by a volume R&D claim provider, or if your internal accountant prepared it without specialist input, the documentation is likely to need strengthening before you respond. Responding with inadequate documentation accelerates the enquiry toward a disallowance rather than a resolution.

I have represented clients through R&D enquiries in the life sciences sector where the initial HMRC challenge appeared serious but where thorough technical documentation and a structured response led to the claim being accepted in full. Early specialist involvement makes a material difference to the outcome.

Before taking any action in response to an HMRC enquiry letter, read my detailed guidance on how to respond to an HMRC R&D enquiry letter.

Key takeaway: Life sciences R&D tax credits are substantial but technically demanding. The qualifying test is applied activity by activity, not sector by sector. Strong documentation of scientific uncertainty, well-defined project boundaries, and careful treatment of subcontracting and grant funding are the foundations of a defensible claim. If HMRC challenges your claim, early specialist involvement determines the outcome.

Frequently asked questions

Do all clinical trials qualify for R&D tax credits in the UK?

No. Clinical trials do not automatically qualify. The key question is whether the trial is directed at resolving genuine scientific or technological uncertainty (for example, testing a novel compound for the first time in humans, or investigating an unknown mechanism of action) or whether it is primarily generating data to satisfy regulatory requirements for a substantially known outcome. Phase I and early Phase II trials are more likely to qualify; later-stage trials designed to confirm known results for regulatory approval are less likely to do so. Each trial must be assessed on its specific circumstances.

Can a UK biotech company claim R&D tax credits for work done by an overseas CRO?

Under the merged scheme (for accounting periods beginning 1 April 2024 or later), qualifying expenditure on externally provided workers and subcontractors is generally restricted to costs connected with work performed in the UK. There are limited exceptions where the required conditions or specialist facilities genuinely do not exist in the UK. Biotech companies with overseas CRO relationships need to review their claim structure carefully against the new rules, as the pre-April 2024 treatment of overseas subcontracted costs was significantly more permissive.

What is the R&D tax credit rate for a UK life sciences SME?

From 1 April 2024, most SMEs claim under the merged scheme at a 20% credit rate, producing a net cash benefit of approximately 16.2% of qualifying expenditure after tax. Loss-making SMEs with qualifying R&D expenditure representing at least 30% of total expenditure may qualify for the enhanced R&D intensive support (ERIS) scheme at a 27% credit rate. The applicable rate depends on the company's tax position, size, and expenditure profile.

Does Innovate UK or UKRI grant funding affect a life sciences R&D tax credit claim?

For accounting periods beginning on or after 1 April 2024, the subsidised expenditure restriction in the former rules was repealed and the conditions for qualifying expenditure under both the merged scheme and ERIS do not require expenditure to be unsubsidised. Grant funding from Innovate UK, UKRI, Horizon Europe, or other public sources does not reduce qualifying expenditure under either scheme. This is a material change from the pre-April 2024 SME rules, where grant receipts pushed the subsidised portion of expenditure out of the SME claim and into RDEC. The current position is significantly more favourable for grant-backed life sciences companies.

How long does HMRC have to open an enquiry into an R&D tax credit claim?

HMRC has 12 months from the filing date of the company tax return to open a formal enquiry (longer if filed via an amended return). For returns filed late, the window extends accordingly. Beyond the standard enquiry window, HMRC can still raise a discovery assessment where it considers there has been a loss of tax brought about carelessly or deliberately, with time limits extending to 4 years (careless) or 20 years (deliberate) from the end of the relevant accounting period.

What is a "competent professional" in the life sciences context?

Under the DSIT Guidelines, scientific or technological uncertainty is assessed against the knowledge of a competent professional working in the relevant field. In life sciences, this means someone with the appropriate scientific training and practical experience in the specific discipline: a medicinal chemist for compound synthesis, a clinical pharmacologist for trial design, or a bioprocess engineer for production scale-up. The uncertainty must be one that person cannot readily resolve using knowledge that is publicly available or deducible from it.

Can a pre-revenue life sciences startup claim R&D tax credits?

Yes. A company does not need to be profitable or generating revenue to make an R&D tax credit claim. Loss-making companies may receive a payable credit (a cash payment from HMRC) rather than a reduction in a tax liability. The applicable scheme and rate depend on company size, expenditure mix, and whether the ERIS intensity test is met. Many early-stage biotech and medtech companies treat R&D credits as a significant source of non-dilutive cash during their development phase.

Get specialist advice on your life sciences R&D tax credit claim

Life sciences R&D tax credits offer substantial value, but the qualifying rules are applied rigorously and HMRC scrutiny of high-value claims is increasing. Whether you are preparing your first claim, reviewing an existing one before submission, or responding to an HMRC enquiry, specialist input makes a material difference to the outcome.

I am Steve Livingston FCA, founder of IP Tax Solutions. I have 25 years of experience in innovation tax, including a tax partnership at a Top 10 UK firm and a track record of defending complex R&D claims against HMRC challenge, including a case involving fraud allegations where the full claim was successfully defended.

I work with life sciences companies directly, and with the accountants and investors who support them. If you have a claim question or an active HMRC enquiry, contact me at stevelivingston@iptaxsolutions.co.uk or call 0161 961 0096.

This is a highly complex technical area so none of the above should be interpreted as professional advice.