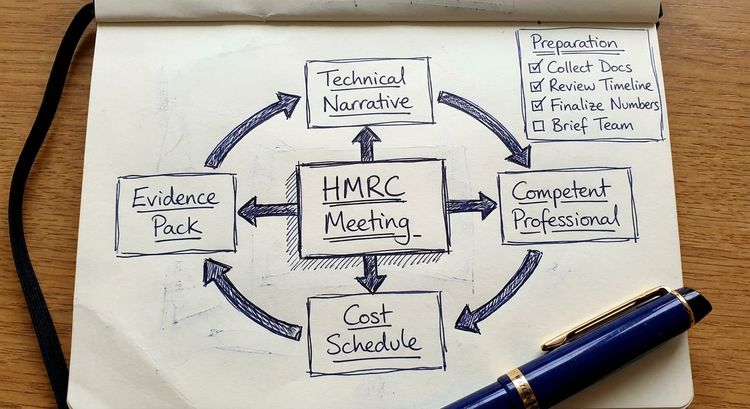

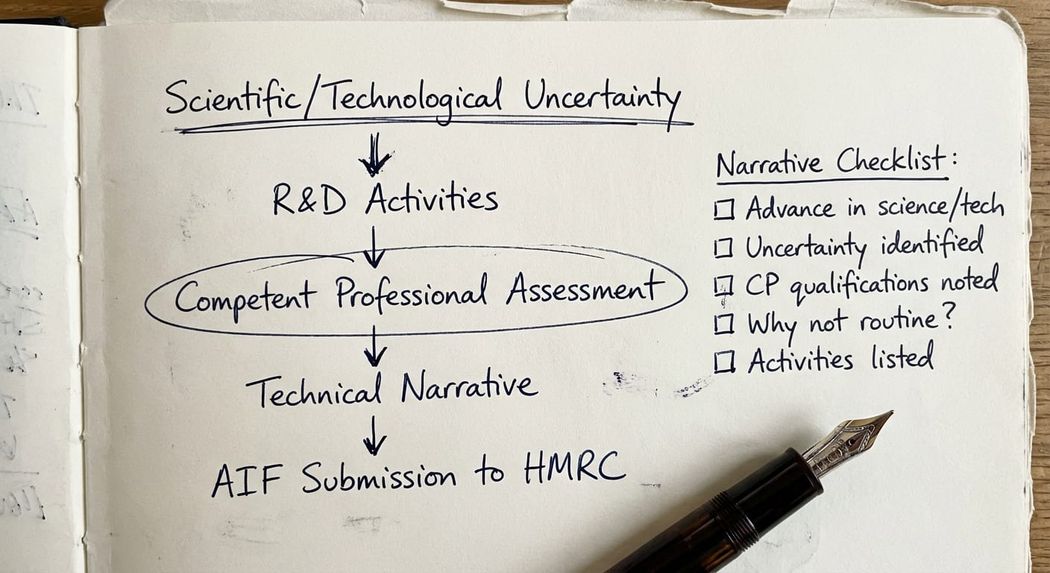

The R&D technical narrative is the document in which a competent professional explains what scientific or technological uncertainty your company was trying to resolve, why that uncertainty existed and how your activities addressed it. Without a credible narrative, your claim has no foundation. HMRC will treat a thin or generic one as grounds to open an enquiry or reduce your claim to zero.

Contents

- What is an R&D technical narrative?

- Why does HMRC require a technical narrative?

- What must a technical narrative contain?

- Who is a competent professional?

- How does the technical narrative connect to the Additional Information Form?

- What does a weak technical narrative look like?

- What happens when HMRC challenges your narrative?

- FAQs: R&D technical narratives

- How I can help

What is an R&D technical narrative?

An R&D technical narrative is a written explanation of the qualifying R&D activities in your claim. It is the document that answers HMRC's core question: was your company genuinely seeking to advance science or technology by resolving an uncertainty that a competent professional could not readily resolve?

The narrative is not a business case. It is not a project plan. It is not a description of what your product does. It is a technical argument, written by someone with the relevant expertise, explaining why your work met the legal definition of R&D for UK tax purposes under s.1138 CTA 2010 and the DSIT Guidelines (2023).

Most enquiries I see start because the narrative fails this test. Either the uncertainty is described in commercial rather than scientific terms, the competent professional is not clearly identified, or the activities described are routine development work dressed up as R&D. HMRC's officers are increasingly sophisticated and they recognise every version of those failures.

Why does HMRC require a technical narrative?

HMRC requires a technical narrative because the R&D tax relief regime is self-assessed. Unlike many tax reliefs, there is no pre-approval process for most claims. A company files its claim with its Corporation Tax return and HMRC relies on the information provided to decide whether to accept or investigate it.

From 8 August 2023, all companies must submit an Additional Information Form (AIF) before their claim. The AIF requires a description of the R&D, identification of the competent professional and an explanation of the uncertainty being resolved. The AIF is, in effect, a formalised version of what the technical narrative should already contain. If you do not submit the AIF, your claim is invalid.

HMRC uses the narrative to make three assessments:

- Whether the claimed work falls within the statutory definition of R&D (an advance in overall knowledge or capability in science or technology, not just within the company).

- Whether the uncertainty was genuine and not readily resolvable by a competent professional working in the field.

- Whether the activities described actually addressed that uncertainty, rather than being ancillary commercial activities.

A narrative that passes all three tests will usually result in HMRC accepting the claim. A narrative that fails any one of them is likely to trigger further scrutiny.

What must a technical narrative contain?

The HMRC Guidelines for Compliance (GfC3, published August 2023) set out what HMRC expects. A credible technical narrative should cover the following, for each project included in the claim:

The advance being sought. What new or appreciably improved process, product, device, or service was being developed? The advance must be in overall scientific or technological knowledge, not merely in the company's own capability. A project that results in something new to your business but readily achievable by others in the field does not qualify.

The specific uncertainty. What was the scientific or technological uncertainty? The uncertainty must be something a competent professional in the field could not readily resolve using existing knowledge. HMRC's guidance is clear that commercial risk, budget constraints, or business-specific challenges do not constitute scientific or technological uncertainty.

Why the uncertainty was not readily resolvable. This is the section most narratives get wrong. It is not enough to say "we didn't know how to do it." You must explain why the answer was not available or deducible from existing published knowledge in the field. This requires the competent professional to demonstrate genuine field knowledge.

The activities undertaken to resolve the uncertainty. What specifically did your team do? Testing, iteration, experimentation, analysis, design, prototyping. Activities that do not directly contribute to resolving the uncertainty (market research, financial planning, routine project management) are not qualifying R&D and should not appear in the narrative.

The outcome. R&D does not need to succeed. What matters is whether the work was directed at resolving the uncertainty. A failed project can still produce a valid claim if the activities were properly directed.

The competent professional's assessment. The opinion should explain the professional's relevant qualifications and experience and confirm that in their view the work represented a genuine attempt to achieve a scientific or technological advance beyond what was readily deducible in the field.

Who is a competent professional?

The concept of the competent professional runs throughout the DSIT Guidelines and HMRC's compliance guidance. Getting this right matters more than most advisers tell their clients.

A competent professional is someone with sufficient knowledge and experience in the relevant field of science or technology to judge whether the advance being sought was genuine and non-trivial and whether the uncertainty could not readily be resolved using existing knowledge in that field.

HMRC's guidance is explicit on one point that trips up many claimants. Having worked in an industry, or having an intelligent interest in a subject, is not enough. The professional must have expertise in the specific area of science or technology being claimed. A managing director who has run an engineering company for 30 years may well be a competent professional in his firm's specialist engineering domain. A director who commissioned IT development but has no background in software engineering is not.

The competent professional does not have to be employed by the company. An external technical expert, a university academic, or a senior contractor with the right expertise will all qualify, provided their credentials are documented in the file.

HMRC has reduced claims to zero in cases where the person identified as the competent professional lacked the relevant expertise. This is not a technicality. It goes to the heart of whether the claim can be supported at all.

How does the technical narrative connect to the Additional Information Form?

The AIF is the mandatory submission that must reach HMRC before your Corporation Tax return is filed. It is a structured form, but it draws directly on the substance of your technical narrative.

The AIF requires, per project:

- A description of the R&D (the advance sought and the uncertainty)

- The main field of science or technology

- The name, role and employer of the competent professional

- A description of the directly qualifying activities

- An explanation of the uncertainty and why it was not readily resolvable

If your technical narrative has been prepared properly, completing the AIF should be a straightforward exercise in transposing information. If the AIF is hard to complete, that is usually a sign that the underlying narrative is not yet fit for purpose.

The AIF itself must reach HMRC on or before the day the Corporation Tax return containing the R&D claim is delivered. Separately, companies that are new claimants, or have not claimed in the three preceding accounting periods, must submit a claim notification form (CNF) within six months of the end of the accounting period. The CNF is a pre-notification of intention to claim, not the AIF. Missing the CNF deadline is fatal to the claim for that year and there is no extension.

What does a weak technical narrative look like?

In my experience reviewing claims that have come under HMRC scrutiny, the weakest narratives share common characteristics.

Generic uncertainty language. Phrases like "we faced technical challenges" or "there was uncertainty around the best approach" tell HMRC nothing. A competent professional should be able to state the specific scientific or technological question that required resolution.

Confusion between commercial and technical uncertainty. Building a new product is not R&D if the technology is known. Entering a new market is not R&D. Customising existing software to client requirements is not R&D. The narrative must identify a genuine gap in overall knowledge or capability, not a gap in the company's own knowledge.

Competent professional in name only. Where the narrative identifies a competent professional but their stated qualifications or role do not match the claimed expertise, HMRC will challenge both the professional's opinion and the validity of the claim.

Activities that bleed into non-qualifying work. Routine testing, deployment, documentation and support are not R&D. A narrative that blurs the line between development work and qualifying R&D will result in HMRC querying the cost apportionment, or rejecting the technical argument entirely.

No reference to existing knowledge in the field. The competent professional should be able to point to what was already known and explain precisely where the project ventured beyond that. Without this, the narrative cannot demonstrate that the advance was in overall knowledge or capability rather than merely in the company's own understanding.

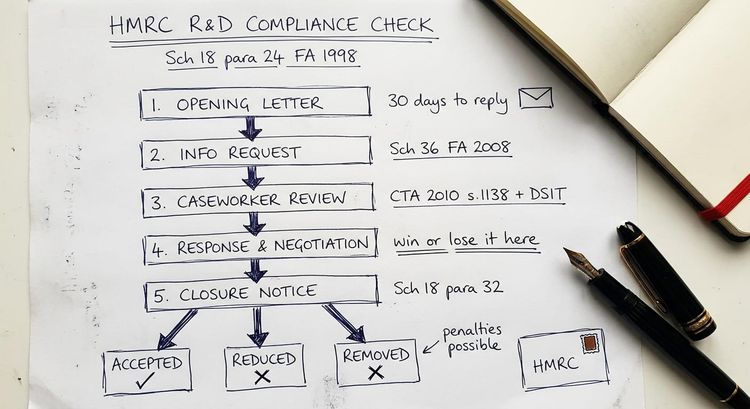

What happens when HMRC challenges your narrative?

If HMRC opens an enquiry into your R&D claim, the technical narrative is the first document it will examine. You will receive a formal enquiry notice, typically requesting the technical details of each project, the competent professional's credentials and the evidence base for the activities claimed.

At this point, the strength of your original narrative either protects you or creates problems. A well-constructed narrative, backed by contemporaneous evidence (project notes, test logs, email threads, design documents, git commits, lab records), gives you a solid foundation to defend the claim. A thin narrative with no supporting evidence forces you into a position where you are reconstructing the argument after the fact, which is a much weaker position.

If you have received an HMRC enquiry letter about your R&D claim, the article on how to respond to an HMRC R&D enquiry letter covers the process in detail.

HMRC's enquiries can result in the claim being accepted, reduced, or disallowed in full. In serious cases, HMRC may allege that the claim was fraudulent or negligent. The outcome depends heavily on the quality of the technical evidence and the calibre of the professional handling the defence.

Key takeaway: The technical narrative is not a formality. It is the legal argument that your R&D activities meet the statutory definition. A claim with a robust narrative, a properly qualified competent professional and contemporaneous evidence stands up to HMRC scrutiny. A claim without those things is vulnerable from the day it is filed.

FAQs: R&D technical narratives

What is an R&D technical narrative?

An R&D technical narrative is a written document explaining the scientific or technological uncertainty your company was resolving through its R&D activities, why that uncertainty existed and how your activities addressed it. It is the core technical argument supporting your R&D tax relief or expenditure credit claim.

Does HMRC require a technical narrative for every R&D claim?

HMRC requires a description of the R&D activities, the uncertainty and the competent professional as part of the mandatory Additional Information Form (AIF), which must be submitted before your Corporation Tax return for all claims from August 2023. In practice this means every claim requires a technical narrative. Claims filed without a supporting AIF are invalid.

Who should write the R&D technical narrative?

The narrative should be written or validated by a competent professional in the relevant field of science or technology. This must be someone with genuine expertise in the specific technical domain, not simply a senior manager or the company's accountant. The adviser preparing the claim should work with the technical team to draft the narrative, but the substance of the technical argument must come from someone who can speak as a competent professional in the field.

How long should an R&D technical narrative be?

There is no prescribed length, but the narrative must be sufficient to address each required element for each qualifying project. In practice, a well-written narrative for a moderately complex project runs to two to five pages per project. Brevity that leaves gaps in the technical argument is far more damaging than length.

Can I submit an R&D claim without a technical narrative?

From August 2023, a claim without a supporting AIF (which requires technical narrative content) is invalid as a matter of law. Before that date, HMRC could still open an enquiry and disallow a claim that lacked a credible technical narrative. The AIF requirement formalised an expectation that already existed in practice.

What happens if my R&D technical narrative is challenged by HMRC?

HMRC will issue formal information requests and may request a meeting to discuss the technical content of the claim. If the narrative is weak or the evidence does not support it, HMRC may reduce or disallow the claim. A specialist adviser can assess the strength of your position, engage with HMRC on the technical arguments and decide whether to defend the claim, negotiate a reduction, or appeal to the First-tier Tribunal.

Can a narrative be improved after HMRC opens an enquiry?

You cannot substitute a new narrative for the one submitted with the claim. However, you can provide additional evidence and explanation in response to HMRC's queries. The quality of the original narrative determines how much room you have to manoeuvre. A claim with no narrative is in a fundamentally different and much weaker position than one with a genuine, if imperfect, technical argument.

How I can help

If your R&D claim is under HMRC scrutiny, or if you want an independent review of your technical narrative before submission, I can assess the strength of your position and advise on what needs to be done.

I am Steve Livingston FCA, founder of IP Tax Solutions. I have 25 years in innovation tax, including KPMG training and a tax partnership at a Top 10 firm. I have successfully defended R&D claims against HMRC, including cases involving fraud allegations and I work directly with the accountants, CFOs and directors handling these situations.

If you are dealing with an active enquiry, the first step is to understand where your narrative is vulnerable. You can read more about the enquiry defence process on the R&D tax credit defence page, or contact me directly to discuss your specific situation.

Steve Livingston FCA

IP Tax Solutions Ltd

Tel: 0161 961 0096

stevelivingston@iptaxsolutions.co.uk