If you are trying to work out whether your company falls under the SME scheme or RDEC for R&D tax credits, the answer depends heavily on when your accounting period began. The April 2024 reforms changed the landscape fundamentally.

For accounting periods beginning on or after 1 April 2024, there is effectively one main scheme for most companies: the new merged RDEC. The old SME vs RDEC distinction has been replaced by a different question: does your company qualify for ERIS, the enhanced route for R&D-intensive SMEs? This guide sets out the current position, explains the historical rules for any periods still in play, and gives you a framework for working out where your company sits.

The Old Framework: SME Scheme vs RDEC Before April 2024

Before April 2024, UK companies claimed R&D tax relief under one of two schemes depending on company size.

Small and medium-sized enterprises claimed under the SME scheme, which provided an enhanced deduction against trading profits. For accounting periods beginning before 1 April 2023, the additional deduction was 130%, meaning that for every £100 of qualifying expenditure, the company deducted £230 in calculating its trading profits. If the company was loss-making, it could surrender losses for a payable tax credit at 14.5%.

The rules tightened from 1 April 2023. The additional deduction was reduced to 86% (giving enhanced expenditure of 186%), and the payable credit rate was cut to 10% for most SMEs. A higher 14.5% rate was preserved for R&D-intensive SMEs with qualifying R&D expenditure representing at least 40% of total relevant expenditure.

Large companies used the Research and Development Expenditure Credit (RDEC), which worked differently. Instead of an enhanced deduction, the company received a taxable credit calculated as a percentage of qualifying expenditure. The old RDEC rate reached 20% from 1 April 2023. The credit was treated as deemed trading income, which meant it was subject to corporation tax, producing a net effective benefit below the headline rate.

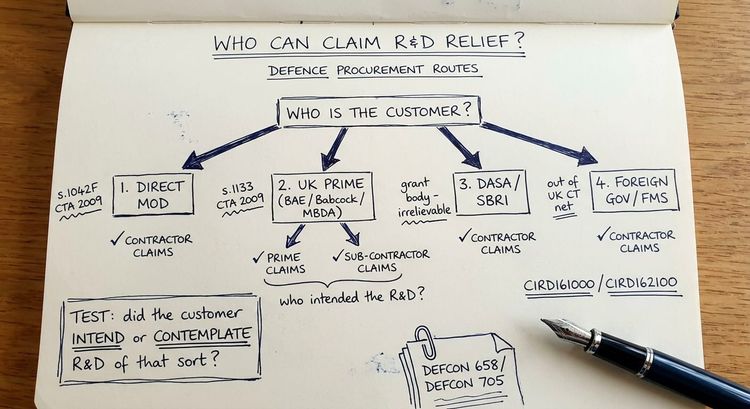

Companies needed to know which bracket they fell into. The SME definition (applying the EU thresholds adopted into UK law) is a company with fewer than 500 employees and either annual turnover not exceeding EUR 100 million or a balance sheet total not exceeding EUR 86 million. Partner and linked enterprises must be aggregated, which catches many group companies out.

What Changed in April 2024: The Merged Scheme

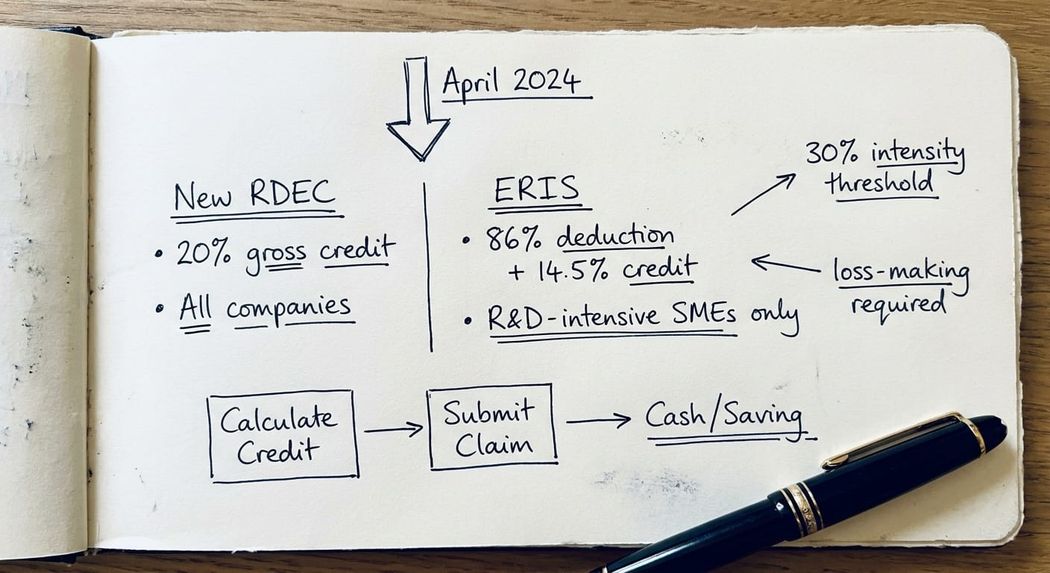

Finance Act 2024 abolished the old RDEC scheme in Chapter 6A of Part 3 CTA 2009 and replaced it with a new merged scheme RDEC, contained in Chapter 1A of Part 13 CTA 2009, with effect for accounting periods beginning on or after 1 April 2024. This was confirmed by SI 2024/286.

The key change: for accounting periods beginning on or after 1 April 2024, the new merged RDEC applies to companies of all sizes. There is no longer a separate SME scheme for most claimants. The old distinction between SME and large company treatment has been collapsed into a single set of rules.

The one exception is ERIS (Enhanced R&D Intensive Support). For qualifying loss-making R&D-intensive SMEs, a separate route continues under a modified Chapter 2 of Part 13 CTA 2009. This is the successor to the old SME scheme, but with important restrictions.

New RDEC: How It Works and What It Delivers

Under the new merged RDEC, the gross credit rate is 20% of qualifying expenditure (for non-ring-fence trades) under CTA09/S1042G. This credit is treated as taxable trading income of the company in the period for which the claim is made.

The practical cash value depends on the company's tax position. For a company paying corporation tax at the main rate of 25%, the net benefit after tax is approximately 15p for every £1 of qualifying R&D spend. For a company within the small profits bracket (19% rate), the net benefit is approximately 16.2p per £1.

The calculation follows a series of payment steps. Loss-making companies can still receive a cash payment via those steps, though the effective rate is subject to a notional tax restriction at step 2, which is set at a lower rate for small profit-makers and loss-makers under the new rules.

One important point: the new RDEC is only available to companies with a trade chargeable to UK corporation tax. Pre-trading companies and certain ineligible companies cannot claim under this route.

ERIS: The Enhanced Route for R&D-Intensive SMEs

ERIS sits outside the merged RDEC. It continues the SME-style calculation for companies that meet all of the following conditions for an accounting period beginning on or after 1 April 2024:

- The company must be an SME (under the existing size definition). It must be loss-making on a tax-adjusted basis before the ERIS additional deduction is taken. And it must meet the R&D intensity condition: qualifying R&D expenditure must represent at least 30% of total relevant expenditure, calculated across the claimant and any connected companies.

- The ERIS rates are an additional deduction of 86% and a payable tax credit of 14.5% (CTA09/S1044(8) and CTA09/S1058(1)(a)). The tax credit under ERIS is not taxable income, in contrast to the new RDEC.

- The practical cash value of ERIS for a qualifying loss-making SME is materially higher than under the new RDEC. A company surrendering the full enhanced expenditure of 186% for a credit at 14.5% can achieve a cash benefit of up to approximately 27p per £1 of qualifying R&D spend, before the PAYE cap and any reduction for other income.

- The intensity threshold was deliberately set lower than the previous 40% threshold under the old SME scheme. The intention was to allow a wider range of genuinely R&D-intensive SMEs to access the more generous route.

Key takeaway: From April 2024, most companies claim under the new merged RDEC at 20% gross. Loss-making SMEs with R&D intensity of 30% or above have a separate route via ERIS, which preserves the higher credit rates. The choice between them is not discretionary: the legislation determines which applies.

Which Scheme Applies to Your Company?

The decision framework for accounting periods beginning on or after 1 April 2024 is as follows.

- Start with company size. If the company is large (500 or more employees, or over the turnover or balance sheet thresholds), it falls into the new merged RDEC. There is no alternative route.

- If the company is an SME, the starting point is also the new merged RDEC. ERIS is the exception, not the default. To access ERIS, the SME must additionally be loss-making (on a tax-adjusted basis, before the ERIS additional deduction) and must meet the 30% R&D intensity condition. The intensity calculation includes connected companies.

- Group structures require particular care. Where an SME is part of a group, the SME size test applies at group level, and the intensity calculation in CTA09/S1045ZA aggregates R&D expenditure and total expenditure across connected companies. This can affect both whether the company qualifies as an SME and whether it clears the intensity threshold.

- ERIS also includes a grace year provision. A company that claimed under ERIS or the old SME scheme in its last 12-month accounting period, and met the intensity condition for that period, can continue to claim ERIS even if it falls below 30% in the current period. This prevents a single year of reduced R&D activity from excluding an otherwise qualifying company, provided the prior year position is properly documented.

The Cash Value: Running the Numbers

It is worth being precise about what these schemes deliver in cash terms, because the headline rates are frequently misread.

Under the new RDEC, the 20% gross credit is reduced by the applicable corporation tax rate. For a company at the 25% main rate, the net benefit is 20% multiplied by (1 minus 25%) = 15%. On £500,000 of qualifying R&D expenditure, the net cash value is approximately £75,000.

Under ERIS, the calculation differs. The additional deduction of 86% produces enhanced expenditure of 186%. A loss-making company can surrender losses of up to 186% of qualifying expenditure for a credit at 14.5%. On £500,000 of qualifying R&D expenditure, the maximum credit is £500,000 multiplied by 186% multiplied by 14.5% = £134,850. This credit is not taxable.

The ERIS route is materially more valuable for qualifying companies. The difference between approximately £75,000 and approximately £135,000 on the same expenditure base is significant and justifies careful analysis of whether the intensity condition is actually met.

Common Mistakes When Claiming Under These Schemes

One of the most common errors we see is claiming ERIS without verifying the loss-making condition. The loss must exist before the ERIS additional deduction is applied. A company that is only loss-making because of the additional deduction itself does not satisfy the condition.

A second common error is failing to aggregate R&D intensity across connected companies. The intensity calculation under CTA09/S1045ZA runs across the whole connected group. An SME with a profitable sister company may find its intensity ratio diluted below the 30% threshold when the connected company's total expenditure is included.

Third, companies with accounting periods straddling April 2024 need specific advice on the transitional provisions at CIRD165000. These affect how contracted-out R&D and subcontractor expenditure is treated across the changeover, and getting them wrong can invalidate part of a claim.

Fourth, claiming under the wrong scheme for pre-April 2024 periods remains a live risk, particularly as HMRC is actively reviewing historical claims. If HMRC raises an enquiry into an R&D tax credit claim, scheme eligibility is one of the first areas examined. A claim submitted under the SME scheme when the company did not meet the size definition, or a claim to the R&D-intensive rate without evidence of the 40% threshold being met, is precisely the kind of issue that generates a formal challenge.

For companies managing a live HMRC challenge, specialist representation matters. Our R&D tax credit defence service covers scheme eligibility disputes alongside technical narrative and expenditure challenges.

Frequently Asked Questions

What is the difference between the SME scheme and RDEC for R&D tax credits?

Under the pre-April 2024 rules, SMEs (companies with fewer than 500 employees and within the turnover or balance sheet thresholds) claimed under the SME scheme, which gave an enhanced deduction of up to 130% on qualifying expenditure and a payable credit of up to 14.5%. Larger companies used RDEC, a taxable credit scheme. From April 2024, most companies now claim under the new merged RDEC regardless of size. The SME vs RDEC split has been replaced by the question of whether the company qualifies for ERIS.

What is the new RDEC rate from April 2024?

The new merged RDEC rate is 20% for non-ring-fence trades in accounting periods beginning on or after 1 April 2024 (CTA09/S1042G). The credit is treated as taxable trading income, so the net cash benefit after corporation tax is approximately 15p per £1 of qualifying R&D expenditure for a company paying at the 25% main rate.

Does my company still use the SME scheme after April 2024?

For most SMEs, no. The new merged RDEC applies to companies of all sizes from April 2024. The exception is ERIS, which is available only to loss-making SMEs with qualifying R&D expenditure representing at least 30% of total relevant expenditure. If your company does not meet both the loss-making and intensity conditions, it falls into the new merged RDEC.

What is ERIS and who qualifies for it?

ERIS (Enhanced R&D Intensive Support) is a continuation of the SME-style relief introduced by Finance Act 2024. It applies to companies that are SMEs, are loss-making on a tax-adjusted basis before the ERIS additional deduction, and meet the 30% R&D intensity condition calculated across the company and any connected companies. The rates are an 86% additional deduction and a 14.5% payable tax credit. The credit is not taxable income.

Is the RDEC credit taxable?

The new merged RDEC credit is treated as taxable trading income of the company in the period claimed (CTA09/S1042H). The ERIS payable tax credit is not taxable. This distinction is important when comparing the effective cash value of each route and should be reflected in any tax computation.

Can a company claim under both RDEC and ERIS?

A company may in principle be eligible for both schemes in a period, but it cannot claim under more than one scheme for the same qualifying expenditure (CTA09/S1040). In practice, if a company meets the ERIS conditions, it will normally elect for ERIS on the relevant expenditure given the higher effective value. RDEC would then apply to any remaining qualifying expenditure outside the ERIS claim.

What is the R&D intensity threshold for ERIS?

For accounting periods beginning on or after 1 April 2024, a company must have qualifying R&D expenditure representing at least 30% of its total relevant expenditure to meet the R&D intensity condition (CTA09/S1045ZA). The calculation aggregates expenditure across the claimant and all connected companies. For the final accounting period under the old SME scheme (periods ending on or after 1 April 2023 and beginning before 1 April 2024), the threshold was 40%.

Next Steps

The April 2024 reforms changed which scheme applies to every R&D-claiming company in the UK. Whether you are reviewing a historical claim, preparing a new submission, or dealing with an HMRC challenge based on scheme eligibility, the starting point is a clear analysis of the framework above.

If your company's position is not straightforward, particularly where group structures, the intensity calculation, or pre-April 2024 transitional periods are involved, we would be glad to review it. Contact Steve Livingston at IP Tax Solutions for a confidential discussion about your company's R&D tax credit position.

This is a highly complex technical area so none of the above should be interpreted as professional advice.