Most accounting firms will encounter at least one innovation tax problem each year that sits beyond their in-house capability. An HMRC enquiry into a significant R&D claim, a SEIS structure with connected persons complications, a Patent Box computation for a manufacturing group, an EMI scheme where disqualifying events have occurred. In those cases, the best outcome for everyone (the firm, the client, and the adviser) comes from referring the work to a specialist. Here is how innovation tax referral arrangements work in practice.

Table of Contents

- When should an accounting firm refer innovation tax work?

- What types of innovation tax work are typically referred?

- How does a referral arrangement work in practice?

- Will I lose the client if I refer the work out?

- What about fees and commercial arrangements?

- How should I explain the referral to my client?

- Frequently asked questions

When should an accounting firm refer innovation tax work?

The short answer: when the stakes are high enough and the complexity is deep enough that handling it in-house creates professional risk.

The threshold is not a fixed figure. A £30k R&D claim for a straightforward software company might sit well within a general practice's capability. The same firm facing HMRC fraud allegations on a £400k claim, or a multi-round SEIS structure involving corporate investors and connected persons issues, is in different territory entirely.

The professional risk of getting it wrong goes beyond the immediate tax exposure. Reputational damage, potential complaints, professional indemnity claims, and a damaged client relationship are all real consequences of handling complex innovation tax work without the appropriate depth of technical expertise. Referral is the professional response, not an admission of weakness.

What types of innovation tax work are typically referred?

From my experience working with accounting firms across the UK, the following scenarios are most commonly brought to a specialist via referral.

HMRC enquiries into R&D tax credit claims. This is the most common referral trigger. When HMRC opens a compliance check into an R&D claim, the risk profile of the engagement escalates immediately. If the enquiry involves allegations of fraud or misrepresentation, or if the claim was prepared by a volume factory before your firm took on the client, specialist involvement is usually essential. You can read more about the full scope of R&D tax credit enquiry defence and what that service covers.

Complex SEIS/EIS structures. Connected persons complications, multi-round funding with SEIS and EIS interplay, advance assurance rejections, financial health requirement questions. These issues require detailed knowledge of the Income Tax Act 2007 (s.257AB-s.257HJ for SEIS, s.156-s.257 for EIS) and HMRC practice that most general practitioners do not maintain as a live specialism.

Patent Box computation for non-standard cases. The Patent Box is well-understood in outline, but the computation for companies with multiple patent streams, group licensing arrangements, or mixed IP portfolios is technically demanding. Most firms identify the opportunity and then refer the computation work to a specialist.

EMI scheme complications. Disqualifying events, working time breaches, subsequent changes to employment terms, share valuations under challenge. These problems frequently surface during transactions and require urgent, accurate resolution.

Pre-submission second opinion reviews. Some firms request a specialist review of a significant R&D claim before submission, particularly where the technical narrative is complex or where the client operates in a sector under active HMRC scrutiny. This is a growing area of work.

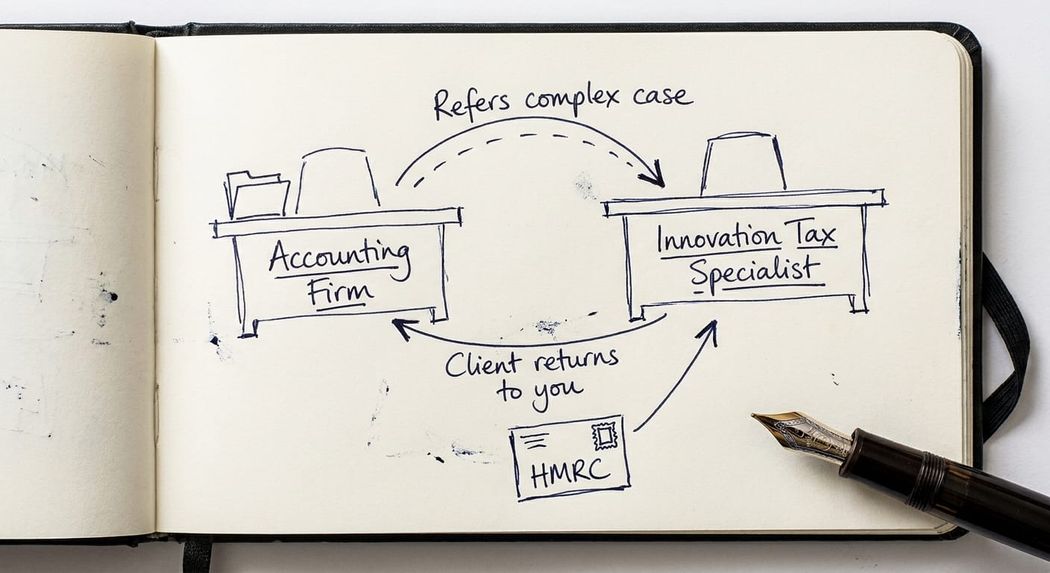

How does a referral arrangement work in practice?

The mechanics are straightforward. The referring firm describes the issue to me, I assess whether I can help, and if I can, we agree the scope of engagement and fee structure directly with the client.

The typical sequence:

- The referring firm contacts me with a brief outline of the issue (by email or phone).

- I confirm whether the matter falls within my specialism and whether I have capacity.

- A three-way introduction is made: the firm, the client, and me.

- I take a direct instruction from the client, documented in a separate engagement letter for the specific matter.

- The referring firm remains the client's general adviser for all other matters throughout.

- On completion, I provide a full written output to both the client and the referring firm (with client consent).

This model keeps the client relationship intact and creates a clean professional structure. The referring firm is not a subcontractor to me, and I am not a subcontractor to the firm. We operate as parallel advisers on the specific matter, with the client informed and consenting throughout.

Will I lose the client if I refer the work out?

This is the most common concern I hear from firms considering a referral. The answer, in practice, is almost always no.

Clients understand specialism. A client who knows their firm cannot handle a serious HMRC fraud allegation in-house, and has been introduced to a specialist with a track record in tribunal-level defence, does not typically interpret that as a failure of service. They interpret it as their accountant looking after them properly.

The risk runs the other way. Firms that try to handle specialist matters beyond their technical depth, and do not achieve a good outcome, are far more likely to lose the client relationship than firms that referred the work and managed the relationship well throughout.

I work hard to keep the referring firm informed and involved throughout any matter I handle on referral. The client returns to their firm for ongoing compliance work. That is the model and, from my experience, it works.

What about fees and commercial arrangements?

I am sometimes asked about referral fees. The position is straightforward: I do not pay referral fees to accounting firms or their staff.

The commercial position is therefore simple. I charge the client a fee for my work. The referring firm continues to charge its own fees for its ongoing work. There is no financial arrangement between us in respect of the referral itself.

Some participants in the innovation tax market operate formal revenue-share "associate" arrangements. I do not participate in those. The client pays me for my advice. That is the entirety of the commercial relationship.

How should I explain the referral to my client?

Position it accurately. This is not "we cannot help you." It is "I have identified the right specialist for this specific problem."

A typical explanation to a client facing an HMRC enquiry might read:

"The HMRC enquiry into your R&D claim requires specialist defence expertise that sits beyond our team's day-to-day work. I have spoken to Steve Livingston at IP Tax Solutions, who specialises in exactly this area and has a strong track record defending R&D claims at enquiry up to tribunal level. I would like to introduce you so he can assess the position and advise on next steps. We will remain your advisers for all other matters."

If the client wants to understand what the enquiry process involves before that conversation, there is a practical guide to responding to an HMRC R&D enquiry letter on this site that may help them prepare for the initial call.

Key takeaway: Referral is not a failure of service. It is a professional judgement that your client's interests are best served by the right combination of advisers. In complex innovation tax matters, that combination almost always includes a specialist.

Frequently asked questions about innovation tax referral arrangements

How do I contact Steve Livingston to discuss a referral?

The quickest route is by email at stevelivingston@iptaxsolutions.co.uk or by phone on 0161 961 0096. A brief description of the issue is helpful but not required. I will confirm within a working day whether I can help and what the most sensible next step would be.

Does IP Tax Solutions work only on referrals from accounting firms?

No. I take direct instructions from clients as well as referrals from accounting firms, lawyers, corporate finance advisers and other professionals. Referral arrangements are a significant part of my practice but not the only route to instruction.

Can I refer innovation tax work in any sector?

Yes. My work covers innovation tax matters across all sectors: software and SaaS, manufacturing, life sciences, engineering, defence, financial services and others. The referral trigger is usually the nature of the problem (HMRC challenge, structural complexity, specialist computation) rather than the industry sector.

What happens if the matter turns out to be straightforward?

I will say so. If I assess a referred matter and conclude it does not require specialist involvement, I will tell the client and the referring firm that clearly. I do not expand instructions beyond what the matter actually requires.

How long does it typically take to resolve an innovation tax referral matter?

It depends entirely on the type of matter. An HMRC R&D enquiry can take anywhere from three months to over two years depending on complexity, HMRC workload, and whether the case proceeds to Alternative Dispute Resolution or tribunal. A Patent Box computation or SEIS advance assurance matter is typically resolved in weeks. I give a realistic timeframe assessment at the outset of every instruction.

Will the client know their accounting firm referred the work out?

Yes, always. I do not accept instructions on a confidential referral basis. The client is informed, consents to the introduction, and engages with me directly. Transparency with the client is a non-negotiable part of how I work.

Do you work with sole practitioner accountants as well as larger firms?

Both. Some of my strongest referral relationships are with sole practitioners and small practices who have built a client base that occasionally generates complex innovation tax work. The size of the referring firm is not the relevant factor; the nature of the client's problem is.

Referring innovation tax work to IP Tax Solutions

If you have a client with an innovation tax problem that has moved beyond your firm's in-house capability, the first step is a short conversation.

Contact me at stevelivingston@iptaxsolutions.co.uk or on 0161 961 0096. Describe the issue briefly and I will confirm within a working day whether I can help and what the next step would be.

There is no obligation in making that initial contact. Most of the firm relationships I have started with a single enquiry about a specific client problem.

Steve Livingston LLB FCA is the founder of IP Tax Solutions Ltd. He is a former KPMG-trained tax professional and former tax partner at a Top 10 firm. He handles R&D tax credit enquiry defence, HMRC compliance challenges, complex SEIS/EIS structuring, Patent Box computation and EMI scheme complications. He can be reached at 0161 961 0096 or stevelivingston@iptaxsolutions.co.uk.