HMRC fraud allegations arising from R&D claims prepared by third parties are one of the most serious and misunderstood situations in UK tax. If your accountant or a specialist firm prepared your claim and HMRC is now using words like "fraud", "deliberate inaccuracy", or "dishonest" in its correspondence, you need specialist defence advice immediately. This is not a situation to manage through your existing accountant.

Contents

- What does HMRC mean when it alleges fraud in an R&D claim?

- Why does this happen when the accountant prepared the claim?

- What is the difference between fraud, carelessness, and genuine error?

- What should you do immediately?

- How does defence work when a third party prepared the claim?

- What penalties are you actually facing?

- What does this kind of case look like in practice?

- Frequently asked questions

What does HMRC mean when it alleges fraud in an R&D claim?

HMRC uses specific statutory language when it believes a tax return contains an inaccuracy. Under Schedule 24 Finance Act 2007, HMRC distinguishes between three categories: a careless inaccuracy, a deliberate inaccuracy, and a deliberate and concealed inaccuracy. In everyday language, the last two are what most people would call fraud.

When HMRC says a claim is "fraudulent", it is typically asserting that the inaccuracy in your Corporation Tax return was deliberate. This matters because the penalties attached to deliberate inaccuracies are significantly higher than those for careless errors, and HMRC has wider investigative powers when fraud is in scope.

It is important to understand that HMRC applies this label to the company's return, not necessarily to any individual within the company. Whether the conduct of the person who prepared the claim can be attributed to you as the director or company is a separate and critical question that your specialist needs to address from the outset.

Why does this happen when the accountant prepared the claim?

Between 2018 and 2023, a large number of R&D claims were submitted by firms operating as volume claim specialists. These firms, sometimes called claim factories, prepared tens of thousands of claims and typically charged a percentage fee based on the tax relief obtained.

In many cases, the technical content of these claims was overstated. Projects were included that did not meet the DSIT (formerly BEIS) guidelines for qualifying R&D activity (the standard applicable under s.1138 CTA 2010). Cost categories were stretched. Some narratives were generic, written to a template rather than to the specific facts of the company.

The company director often signed the Corporation Tax return without a detailed understanding of exactly what had been claimed, or how the qualifying expenditure had been calculated. HMRC is now challenging many of these claims and, in the most serious cases, is characterising the inaccuracies as deliberate.

This is a difficult position. You trusted a specialist to handle this. You signed a return in good faith. And yet you now find yourself facing a fraud allegation on a claim you may not have fully understood at the time.

What is the difference between fraud, carelessness, and genuine error?

Under Schedule 24 FA 2007, the three categories carry different penalty ranges.

A careless inaccuracy arises where the taxpayer failed to take reasonable care. The standard penalty is 0-30% of the tax understated (known as the Potential Lost Revenue). For R&D claims, carelessness is the appropriate characterisation where the company made a genuine mistake in applying the rules, even if it relied on a professional.

A deliberate inaccuracy is where HMRC believes the taxpayer knew the return was wrong. The standard penalty is 20-70% of the Potential Lost Revenue for a deliberate but unconcealed inaccuracy, rising to 30-100% where HMRC considers the inaccuracy to have been concealed.

The key battleground in most R&D fraud allegation cases is whether the inaccuracy was careless or deliberate. This is a factual question, not just a legal one, and it turns largely on what you knew, what you were told, what you asked, and what the preparer represented to you. A tribunal case decided in 2024, H&H Contract Scaffolding Ltd v HMRC [2024] UKFTT 151 (TC), confirmed that a failed R&D claim does not automatically warrant a carelessness penalty, let alone a fraud characterisation. The company in that case had taken reasonable care and the tribunal found the penalty charge was not warranted. The Tribunal specifically found that the company was not even careless, because it had selected a seemingly reputable specialist and provided them with accurate information. This proves that the 'reliance on a professional' defence is still a powerful tool against HMRC penalties.

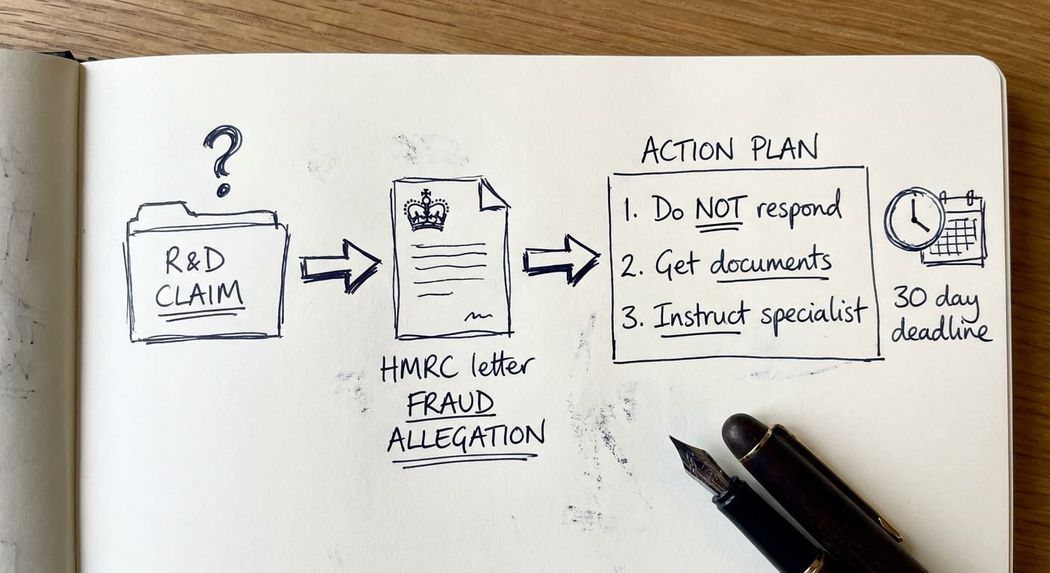

What should you do immediately?

The first thing to do is to avoid responding to HMRC directly without specialist input.

If you have received an HMRC enquiry letter about your R&D claim, the worst thing you can do is send a detailed written response before you understand the legal framework. Anything you say in correspondence becomes part of the record. Poorly worded responses, or responses that make unnecessary concessions, can make a difficult situation significantly worse.

The second thing to do is to obtain the complete documentation that was submitted to HMRC. This means the Corporation Tax return, the computation, the R&D schedule within the return, and the supporting technical narrative or report that accompanied it. You need to understand exactly what was claimed before you can respond to anything.

The third step is to instruct a specialist who has experience defending fraud allegations in R&D cases. This is not the same as your existing accountant, even if they are competent in general tax work. R&D tax credit defence requires a specific understanding of HMRC's enquiry procedures, the relevant penalty legislation, and how to present the facts to minimise exposure.

How does defence work when a third party prepared the claim?

When a claim factory or third-party specialist prepared your R&D claim, the defence strategy typically has two phases.

The first phase is establishing the facts. This means reviewing every project included in the claim against the DSIT guidelines and understanding, honestly, which projects genuinely qualify and which do not. This is not about making a new case to HMRC from scratch. It is about understanding the actual strength of your position before you engage.

The second phase is addressing the penalty question separately from the tax question. Even if HMRC is right that some expenditure does not qualify, that does not mean a fraud penalty is justified. To sustain a deliberate inaccuracy charge, HMRC must demonstrate that you, as the taxpayer, knew the return was wrong when you signed it. If you relied on the professional judgement of a firm that held itself out as a specialist, that reliance is directly relevant to the carelessness versus deliberate distinction.

In my experience, many of these cases settle in the careless range or below, once the full facts of the engagement between the company and the claim preparer are properly documented and presented. The engagement letter, the instructions you gave, the questions you asked, what you were told about qualifying expenditure, and the representations made to you in the claim report all become important evidence.

What penalties are you actually facing?

The tax exposure depends on how much of the claim HMRC successfully challenges. If the full claim is unwound, the company owes the relief back, plus interest from the original payment date.

The penalty exposure depends on the inaccuracy category:

- Careless, unprompted disclosure: 0-30% of Potential Lost Revenue

- Careless, prompted disclosure: 15-30% of Potential Lost Revenue

- Deliberate, unprompted disclosure: 20-70% of Potential Lost Revenue

- Deliberate, prompted disclosure: 35-70% of Potential Lost Revenue

- Deliberate and concealed, unprompted: 30-100% of Potential Lost Revenue

- Deliberate and concealed, prompted: 50-100% of Potential Lost Revenue

HMRC has the ability to reduce penalties significantly for disclosure, co-operation, and giving access to records. A key part of any defence strategy is managing the behaviour mitigation to minimise whatever penalty applies.

It is also worth understanding that HMRC sometimes raises fraud allegations as a starting position in negotiation, not because it has strong evidence to sustain them at tribunal. This does not mean you should ignore the allegation. It means you should engage from a position of knowledge, not fear.

Key takeaway: A fraud allegation from HMRC is not a finding. It is a starting position. With the right evidence and specialist representation, the characterisation of many of these cases can be moved from deliberate to careless, with a material reduction in penalty exposure.

Frequently asked questions

What does HMRC mean by a fraudulent R&D claim?

HMRC uses this term to describe a deliberate inaccuracy under Schedule 24 Finance Act 2007. It means HMRC believes the person who submitted the return knew it was wrong. A fraudulent allegation is not the same as a criminal prosecution, though in the most serious cases HMRC has the power to refer matters to the Crown Prosecution Service. The vast majority of R&D fraud allegation cases are resolved through civil settlement, not criminal proceedings.

My accountant filed the claim without telling me the details. Am I still liable?

As the director who signed the Corporation Tax return, you are the taxpayer for these purposes. However, your knowledge at the time you signed is central to whether any inaccuracy was deliberate or careless. If you signed in reliance on a professional's advice and had no reason to suspect the claim was wrong, that supports a careless rather than deliberate characterisation, which carries lower penalties.

Can I argue that HMRC should pursue the claim factory, not me?

The R&D claim is part of your Corporation Tax return. HMRC's enforcement action is against the company as taxpayer. If you believe the claim factory misrepresented the position to you, you may have a separate civil claim against that firm, but that does not resolve your liability to HMRC. Both tracks need to be considered.

What if the claim factory has gone into liquidation?

This is an increasingly common situation. The insolvency of the claim preparer does not affect your HMRC exposure. It does, however, affect your ability to recover losses from them and may limit the evidence available about how the claim was prepared. This makes it more important, not less, to obtain any documentation you hold about the original engagement.

How long does HMRC have to open an enquiry into an R&D claim?

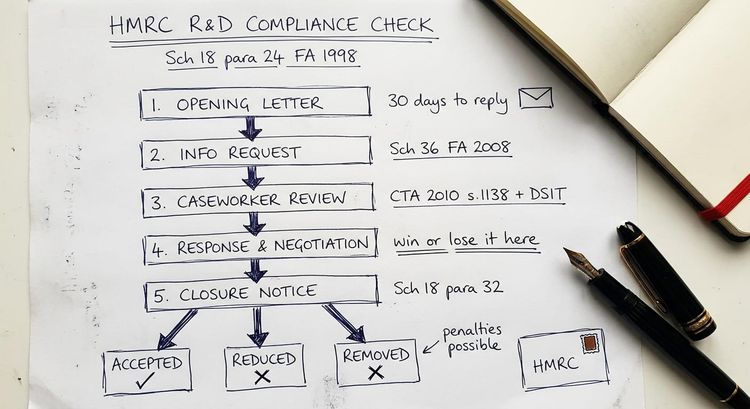

HMRC has one year from the filing date to open a standard enquiry into a Corporation Tax return under Schedule 18, paragraph 24, Finance Act 1998 (longer if filed via amended return). For discovery assessments, where HMRC identifies an inaccuracy after the enquiry window has closed, the time limit extends to six years for careless errors and twenty years for deliberate ones. This is why HMRC's categorisation of the inaccuracy matters so much.

Should I use the same accountant who filed the original claim to defend it?

In most cases, no. Your existing accountant has a conflict of interest. If the claim they prepared is now under challenge, they have a personal interest in its defence that may not align with yours. A specialist who was not involved in the original claim will assess the position objectively and advise you on its genuine merits.

What is the first thing I should do if I receive an HMRC fraud allegation letter?

Do not respond to HMRC directly. Telephone a specialist immediately. The response window in an HMRC enquiry is typically 30 days, but extensions are available in most cases. Use that time to gather documentation and take proper advice before committing anything to writing.

What to do next

If you have received HMRC correspondence alleging fraud or deliberate inaccuracy in your R&D claim, I can review your position and advise on the options. I have represented clients in exactly this situation, including cases where the original claim was prepared by third-party specialists who have since ceased trading.

Contact me at stevelivingston@iptaxsolutions.co.uk or call 0161 961 0096 for an initial discussion. There is no charge for an initial call.

Steve Livingston LLB FCA is the founder of IP Tax Solutions, a specialist innovation tax advisory firm. Former KPMG and former partner at Top 10 firm. 20+ years defending innovation tax claims against HMRC.

This is a highly complex technical area so none of the above should be interpreted as professional advice.