An HMRC R&D compliance check is a formal HMRC review of your company's Research and Development tax credit claim. HMRC writes to your company, asks for evidence that your work qualified and that the costs were correct, reviews your reply, and then closes the check by accepting the claim, reducing it, or removing it. Penalties can follow if HMRC finds an error. I am Steve Livingston FCA, and I have defended R&D claims through HMRC compliance checks for over 25 years.

Contents

- What is an HMRC R&D compliance check?

- Why has HMRC checked so many R&D claims since 2022?

- What are the stages of an HMRC R&D compliance check?

- What does HMRC ask for during a compliance check?

- How long does an HMRC R&D compliance check take?

- What are the possible outcomes?

- When should you bring in a specialist?

- Frequently asked questions

- About Steve Livingston FCA

What is an HMRC R&D compliance check?

An HMRC R&D compliance check is the formal process HMRC uses to examine a Research and Development tax credit claim after it has been submitted. It is opened under paragraph 24 of Schedule 18 to the Finance Act 1998, which gives HMRC the power to enquire into a company tax return.

"Compliance check" and "enquiry" describe the same legal process. HMRC tends to use "compliance check" in its letters. The check can look at the whole return or just the R&D claim within it.

Receiving a compliance check letter does not mean HMRC has decided your claim is wrong. It means HMRC wants to see the evidence behind it. A well-evidenced claim, presented clearly, can come through a compliance check without any adjustment.

Why has HMRC checked so many R&D claims since 2022?

HMRC scaled up R&D compliance activity sharply from 2022 onwards, after estimating that a significant proportion of SME R&D claims contained error or were not compliant. It built a dedicated volume compliance team and began checking a far higher share of claims than ever before.

This is why the HMRC R&D compliance check became a routine business risk rather than a rare event. Many of the claims pulled into checks were genuine. The volume approach catches valid claims alongside weak ones, because selection is driven by risk indicators in the data, not by a prior decision that the claim is false.

In my experience, the companies that struggle most are not necessarily the ones doing 'dubious qualifying work'. They are often the ones whose genuine R&D was poorly documented, often by a volume claim provider who has since moved on. The HMRC R&D compliance check tests evidence, and thin evidence is the real exposure.

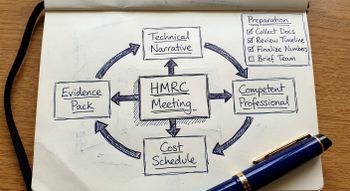

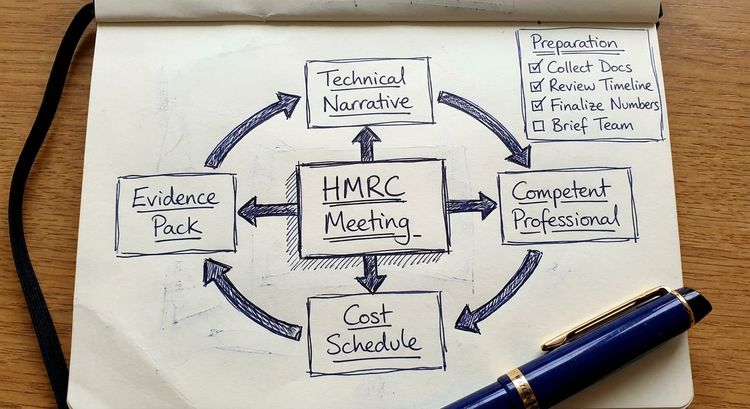

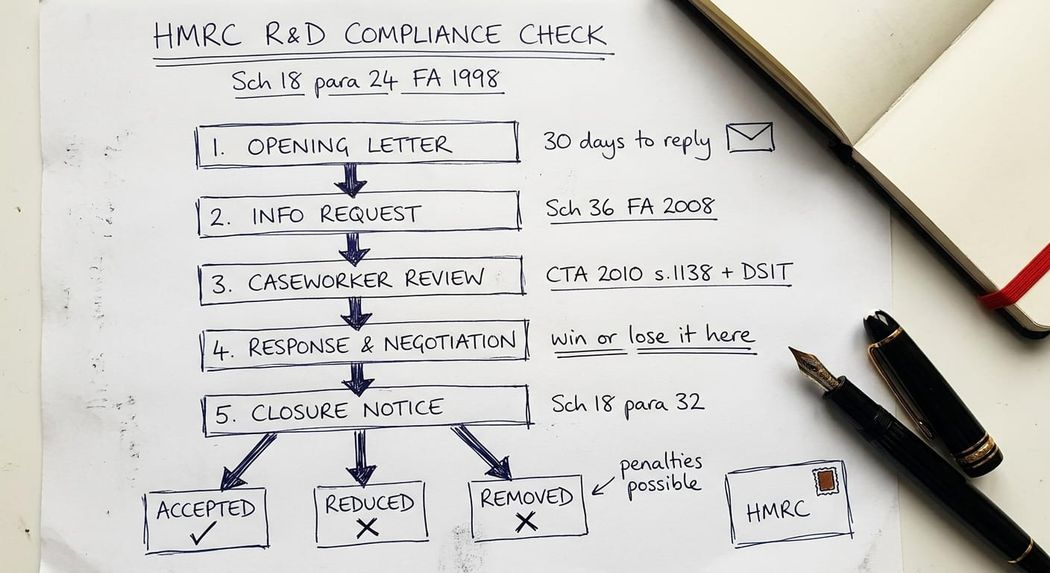

What are the stages of an HMRC R&D compliance check?

A typical HMRC R&D compliance check moves through five broad stages.

Stage 1: The opening letter. HMRC writes to your company's registered office stating that it is checking the R&D claim for a specified accounting period. The letter sets out questions and usually gives 30 days to respond.

Stage 2: The information request. HMRC asks for the documents and explanations behind the claim. If a request is not met, HMRC can issue a formal information notice under Schedule 36 to the Finance Act 2008.

Stage 3: Caseworker review. The HMRC caseworker reviews your response against the statutory definition of R&D in section 1138 of the Corporation Tax Act 2010 and the DSIT guidelines. Further questions, or a request for a meeting or site visit, often follow.

Stage 4: Response and negotiation. You answer the follow-up points. Where there is genuine disagreement, this stage can run through several rounds of correspondence. It is the stage where the technical argument is won or lost.

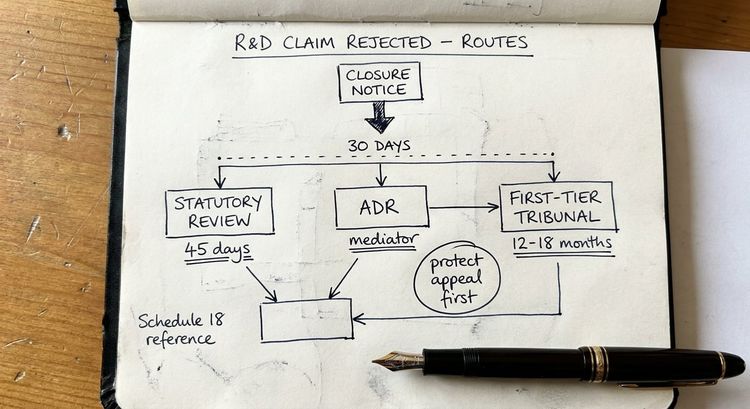

Stage 5: The closure notice. HMRC issues a closure notice under paragraph 32 of Schedule 18 to the Finance Act 1998, stating its conclusion and any amendment to your return. You can appeal a closure notice amendment under paragraph 34.

If you want a detailed walkthrough of the first reply, see my guide on how to respond to an HMRC R&D enquiry letter.

What does HMRC ask for during a compliance check?

HMRC's caseworkers are trying to establish two things: whether your work qualified as R&D, and whether the costs you claimed were correct.

On the technical side, HMRC will test your claim against the statutory test. Was there a genuine scientific or technological uncertainty? Could a competent professional have resolved it readily using publicly available knowledge? Was there an advance in the field, not just an advance for your business?

On the financial side, HMRC checks whether staff costs are correctly apportioned between R&D and non-R&D work, whether subcontractor and externally provided worker costs are eligible, and whether consumables and software costs link directly to qualifying projects.

HMRC's own Guidelines for Compliance (GfC3) confirm that, during an R&D compliance check, HMRC may ask to see relevant documents, visit your site, examine prototypes, and talk to employees. Documents commonly requested include project plans, drawings, test results, meeting minutes, and email exchanges. Contemporaneous records carry far more weight than explanations written after the event.

How long does an HMRC R&D compliance check take?

Most R&D compliance checks take between three and twelve months. The single biggest variable is the quality of the first response.

A straightforward check, met with a clear and well-evidenced reply, can sometimes be resolved in a single round of correspondence, in as little as six to eight weeks. A check where the opening response was weak, late, or incomplete can run well beyond twelve months, because each gap generates a new round of questions.

If the matter cannot be agreed and proceeds to Alternative Dispute Resolution or the First-tier Tribunal, add several more months. The way to keep a compliance check short is to make the first response complete, accurate, and framed in the language of the legislation.

What are the possible outcomes?

Key takeaway: An HMRC R&D compliance check does not have a single predetermined ending. The outcome is shaped by the strength of your evidence and how well your case is argued, which is why the response stage matters more than the opening letter.

There are four broad outcomes. HMRC may accept the claim in full and close the check with no amendment. HMRC may agree a reduced figure, where part of the claim is accepted and part is not. HMRC may reject the claim entirely, removing the relief and issuing an amendment for the tax due. Or the matter may remain in dispute and move to statutory review, Alternative Dispute Resolution, or the Tribunal.

Where HMRC concludes there was an error, penalties under Schedule 24 to the Finance Act 2007 can apply. These run from nil, where reasonable care was taken, up to 100% of the tax at stake for deliberate behaviour. A genuine error disclosed voluntarily, before HMRC finds it, usually attracts a much lower penalty than the same error uncovered by the caseworker.

If your claim has already been paid and is then reduced, the difference becomes Corporation Tax payable. For a smaller company that has spent the credit, that can be a serious cash flow event, which is why it is worth understanding your exposure early.

When should you bring in a specialist?

Not every compliance check needs specialist representation. A minor administrative query on a well-documented claim can often be handled in-house or by your accountant.

You should consider a specialist where the claim value is material, where HMRC is challenging whether your activities qualify as R&D at all, where the letter refers to error, fraud, or comes from HMRC's Fraud Investigation Service, where your claim was prepared by a volume provider without proper project-level narratives, or where you lack contemporaneous records. You should also consider it where your accountant has not handled R&D compliance checks before. There is no criticism in that. It is a specialist field, and HMRC's caseworkers do it full time.

A specialist reviews the claim and the letter, identifies the weak points before HMRC does, frames the technical and financial arguments correctly, manages the correspondence and any meeting, and knows when to concede a point and when to hold firm. I have taken claims through compliance checks where HMRC alleged the work was routine and we closed the check with no amendment. I have also advised clients to correct genuine errors voluntarily, which reduced their penalty exposure significantly. Knowing which path fits a given case is the judgement that experience buys. You can read more about specialist R&D enquiry defence and how I work.

Frequently asked questions

What is the difference between an HMRC R&D compliance check and an enquiry?

There is no legal difference. Both refer to HMRC examining your tax return under paragraph 24 of Schedule 18 to the Finance Act 1998. HMRC generally uses "compliance check" in correspondence, but your rights and the process are the same whichever term appears in the letter.

Does an HMRC R&D compliance check mean my claim is fraudulent?

No. A compliance check is a request to see evidence, not an accusation. HMRC selects many claims using risk indicators in the data, and genuine, well-founded claims are regularly pulled into checks. The check tests your evidence. If your work qualified and you can show it, the check should close without an adjustment.

How far back can HMRC open an R&D compliance check?

HMRC can normally open a compliance check into a company tax return within twelve months of the date the return was delivered (longer, if the claim was filed via an amended return). Where HMRC suspects a loss of tax through carelessness or deliberate behaviour, it can assess earlier periods through a discovery assessment, going back up to six years for carelessness and twenty years for deliberate behaviour.

What happens if I miss the deadline in the compliance check letter?

Tell HMRC promptly and ask for a reasonable extension, which is usually granted if requested early. Simply ignoring the letter is the worst option. HMRC can issue a formal information notice under Schedule 36 to the Finance Act 2008, and an unanswered check can end in an amendment made without your input.

Can I still send HMRC more documentation after the compliance check has started?

Yes. You can provide further evidence throughout the check. Be aware that records created at the time of the project carry more weight than material produced after the claim was filed, and HMRC may question the relevance of late documentation. The strongest position is contemporaneous evidence presented clearly from the outset.

Will an HMRC R&D compliance check affect my future claims?

Not automatically. You can continue to claim R&D relief for later periods while a check is open. However, if HMRC identifies problems in the period under check, it may look more closely at your subsequent claims, so it is worth tightening your record keeping and technical narratives going forward.

Should my original claim provider handle the compliance check?

Consider this carefully. If the claim was prepared poorly, the firm that prepared it has a conflict of interest and may be reluctant to highlight weaknesses in its own work. An independent review of the claim and the letter, before you reply, is often the safer course.

Get specialist help with an HMRC R&D compliance check

An HMRC R&D compliance check is won or lost on the quality of the evidence and the way the technical case is argued, not on the wording of the opening letter. If you have received a compliance check letter, the most useful thing you can do is understand your position before you respond.

I offer a diagnostic call to review the letter and your original claim, assess the strength of your position, and set out your options. If you are an accountant whose client has been selected for a check, I also work with firms on a referral basis, which you can read about on my page for accountants and professional advisers. To discuss a specific case, get in touch.

About Steve Livingston FCA

I am Steve Livingston, a Fellow of the Institute of Chartered Accountants in England and Wales and the founder of IP Tax Solutions. I have spent over 25 years in innovation tax, including training at KPMG and a partnership at a Top 10 UK accounting firm.

I specialise in founder and owner equity tax including R&D compliance checks and enquiry defence, complex SEIS & EIS structuring, Patent Box, equity structuring including EMI scheme issues. I am the specialist that founders, HNWI, accountants, lawyers and corporate finance advisers call when innovation tax gets complicated.