If you are a director thinking about subscribing for SEIS or EIS shares in your own company, the first question is not "how much can I put in" but "am I allowed to put in anything at all". The SEIS director connected persons rules sit at the heart of that question, and a surprising number of founders, advisers and even drafting solicitors get them wrong. Get the structuring right and a director investment can sit alongside a full external round without losing a penny of relief. Get it wrong and the entire subscription is disqualified, sometimes years after the cash has gone in.

This is a guide to how the rules actually work, what HMRC looks at, and how to structure a director's investment so it survives both advance assurance and any later HMRC enquiry.

Why the connected persons rules exist (and why they bite directors hardest)

SEIS and EIS are designed to channel risk capital from outside investors into early-stage companies. Parliament's concern, when the schemes were introduced, was that without a "connection" rule directors and existing shareholders would simply route their own money in through the relief and pocket the tax break for capital they would have invested anyway. The legislation deals with that by disqualifying anyone who is too closely linked to the company at the moment the shares are issued.

The rules sit in two places.

- For SEIS, the investor conditions are in s.257BA to s.257BF ITA 2007.

- For EIS, they are in s.163 to s.170 ITA 2007.

The two regimes share the same architecture (an employee test, a director test, and a substantial interest test), but the way each test is calibrated differs. That difference is the source of most of the practical confusion.

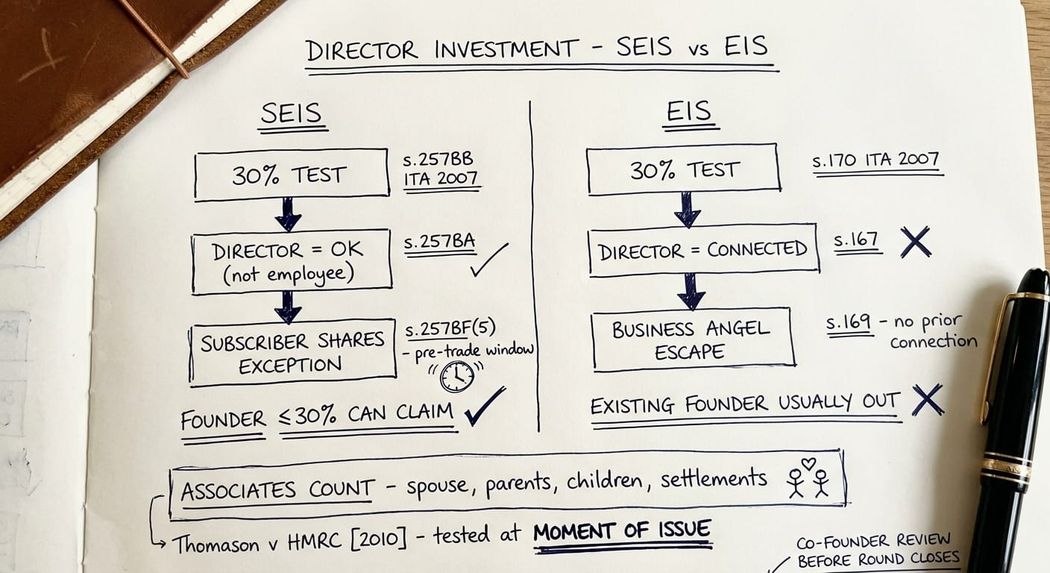

The 30% substantial interest test (the one most founders fail before they begin)

For both schemes, an investor is connected if they (taken together with their associates) directly or indirectly hold, or are entitled to acquire, more than 30% of any of the following: ordinary share capital, issued share capital, voting power, or rights to assets on a winding up. Control under s.995 ITA 2007 is also caught.

Associates count: Spouses, civil partners, lineal ancestors and lineal descendants, business partners and trustees of settlements where the investor is settlor or beneficiary are all attributed under s.253 ITA 2007 (EIS) and s.257HJ ITA 2007 (SEIS). The case of Cook v Billings & Others [2001] STC 16 confirmed that an associate's holding is treated as the investor's own when measuring the threshold.

There is one narrow exception. Under s.257BF(4) ITA 2007, an SEIS investor is not treated as having a substantial interest if at the time of subscription the company has only issued subscriber shares (the formation shares issued at Companies House registration) and has not yet started trading or preparing to trade. That is what allows a single founder to subscribe for SEIS shares immediately after incorporation, even though they own 100% of the issued share capital at that moment, provided no trade has begun. Outside that window the 30% ceiling is hard.

A founder-director who already owns more than 30% of an active trading company cannot subscribe for SEIS or EIS shares in that company at all. There is no Business Angel route, no advance assurance argument and no structuring fix that gets you past the 30% test once the company is trading. The only options are a different shareholder making the investment, or a fresh structure entirely.

SEIS treats directors differently from EIS, and that matters

This is where most advisers slip. Under SEIS, s.257BA ITA 2007 disqualifies an investor who is an employee of the company at any point during period A. Crucially, "an individual holding a directorship is not considered an employee for this purpose". A founder who is a director but holds 30% or less of the share capital can subscribe under SEIS without needing to invoke a Business Angel rule at all. SEIS does not contain an EIS-style director-as-connection test.

Under EIS the position is different: Section 167 ITA 2007 treats a director as connected with the company by virtue of being a director, subject to s.168. Under s.168 ITA 2007 a director is not connected if they receive nothing beyond the "permitted payments" list (reasonable expenses, interest at a reasonable commercial rate on money lent, dividends not exceeding a normal return, market-rate rent, payment for goods at market value, and necessary and reasonable remuneration meeting the s.168(3) conditions). Where the director receives remuneration outside that list, the only escape is the Business Angel route in s.169 ITA 2007, where they must qualify under one of the prior-condition limbs.

The practical consequence is that SEIS director investment is meaningfully easier than EIS director investment. A co-founder who holds, say, 25% of the share capital and sits on the board can subscribe for SEIS shares as part of the SEIS round without any further structuring work. The same founder subscribing under EIS would need to satisfy the Business Angel conditions before any of the relief sticks.

The Business Angel exemption for EIS director investment

Section 169 ITA 2007 carves out a specific class of paid director who can still claim EIS relief notwithstanding the connection. To qualify, the director's only connection with the company must be that they are receiving remuneration as a director, and one of three further conditions must be met:

- At the time the shares are issued, the director had never previously been connected with the company and had not been involved in carrying on the whole or any part of the trade as an owner, director or employee.

- The shares are issued before the termination period of an earlier eligible share issue at which the first condition was satisfied.

- The shares are issued before the termination date of an earlier SEIS-eligible share issue in respect of the same investor.

The first limb is the route most "post-investment director" cases follow. An external investor subscribes for shares as a passive backer, then takes a board seat after the round closes and starts being paid for that role. Provided they were not connected with the company immediately before the share issue, the relief survives. The leading authority on the timing point is Thomason & Ors v HMRC [2010] UKFTT 579 (TC), which confirmed that the connection test is applied at the moment the shares are issued, not retrospectively.

Permitted payments under s.168 ITA 2007 (reasonable expenses, interest at a reasonable commercial rate on money lent, dividends not exceeding a normal rate of return, rent at no more than market value and so on) do not count as remuneration for these purposes. Anything outside that list, including a salary, bonus, consultancy fees or share-based remuneration that is not within the permitted list, brings the director within the connection rule and forces reliance on s.169.

Five director-investment scenarios that come up in practice

In our SEIS and EIS work, the same five fact patterns surface repeatedly. The structuring answer is different in each.

- Scenario 1: Solo founder incorporates a company and holds 100% of the initial subscriber shares. As long as no trade or preparation to trade has begun, HMRC ignores this initial 100% holding. The founder can then subscribe for new SEIS shares alongside external investors, provided the founder's total stake is diluted to 30% or less as a result of that round.

- Scenario 2: Two co-founders, each holding 50% of the issued share capital. Once the company has started trading, neither founder can subscribe for SEIS or EIS personally. The 30% ceiling is breached on day one. New money can come from external angels. The founders themselves are locked out.

- Scenario 3: Four co-founders, each holding 30% or less, all directors, company trading. Each can subscribe for SEIS shares (subject to the £200,000 per tax year investor cap and the company-side £250,000 limit) if they each hold 30% or less. For EIS each would need to clear the Business Angel route in s.169, which they will not satisfy because they are existing trading directors. Result: SEIS works, EIS does not.

- Scenario 4: External investor takes a board seat post-investment and starts being paid. Passes EIS s.169 condition 1 if they had no prior connection. Document the timeline carefully. Get the directorship and the remuneration arrangement signed only after the share issue date.

- Scenario 5: Investor's spouse is already a director or shareholder of the company. Associates are attributed. Treat the spouse's holding as the investor's own. Most of these cases are fatal for SEIS or EIS unless the holdings can be restructured before the share issue, which is rarely commercially possible.

What goes wrong, and how HMRC finds it

The connection rules are tested at advance assurance, at compliance check on the SEIS1/EIS1 statement, and again on any compliance enquiry into the company or the investor. HMRC's Venture Capital Reliefs Team is well practised at spotting paid director arrangements that started before the share issue and were dressed up as having started after. The fact pattern that triggers a query is almost always the same: a board appointment dated post-issue, but minutes, payroll records, contracts of employment or invoices that show the director was already operationally involved.

Where the structuring fails, the consequences are harsh. The investor's relief is withdrawn, often retrospectively across multiple tax years.

Key takeaway: SEIS is markedly more permissive than EIS for director investment. A trading-company founder who holds 30% or less can subscribe for SEIS shares without invoking a Business Angel rule. The same founder cannot get EIS relief unless they fall within s.169 ITA 2007. The 30% test is the one that catches most people early. Get a structural review done before the round closes, not after.

Frequently asked questions

Can a director invest in their own company under SEIS?

Yes, provided they hold 30% or less of the issued share capital, voting rights and assets on winding up at the time the shares are issued (taken together with their associates). Under s.257BA ITA 2007 a director is not treated as an employee for the SEIS investor test, so the directorship itself is not the problem. The 30% substantial interest test in s.257BB ITA 2007 is.

Can a director invest in their own company under EIS?

Only if they fall within the Business Angel exemption in s.169 ITA 2007. That generally means the director must not have been connected with the company before the share issue and must not be receiving remuneration outside the s.168 permitted payments list. Existing founder-directors of trading companies almost never qualify. Different rules apply for EIS reinvestment relief.

What counts as a substantial interest for SEIS or EIS?

More than 30% of the ordinary share capital, the issued share capital, the voting power or the rights to assets on winding up, taken together with associates.

Who counts as an associate for the connected persons test?

Spouses, civil partners, lineal ancestors and lineal descendants, business partners and trustees of settlements where the investor is settlor or beneficiary, under s.253 ITA 2007 (EIS) and s.257HJ ITA 2007 (SEIS). Cook v Billings & Others [2001] STC 16 confirms that associate holdings are attributed when measuring the 30% threshold. Siblings are not associates.

Can I become a paid director after I subscribe for EIS shares and still keep my relief?

Yes, under s.169 ITA 2007 condition 1, provided you had no prior connection with the company and were not involved in carrying on its trade as an owner, director or employee before the share issue. The connection test is applied at the moment the shares are issued (Thomason & Ors v HMRC [2010] UKFTT 579 (TC)). Documentation of the timeline matters.

What is the consequence of getting the SEIS director connected persons rules wrong?

The investor's relief is withdrawn under s.257BB ITA 2007 (SEIS) or s.163 ITA 2007 (EIS), generally retrospectively. Carry-back relief claimed against the prior tax year is also withdrawn. Where a director's investment was part of a wider round, the disqualification is investor-by-investor, not round-wide, but the reputational and adviser-relationship damage tends to spread.

Does the connected persons test apply during the whole holding period or just at issue?

The connection tests apply throughout a specific statutory window called Period A, meaning connection arising mid-period will withdraw relief just as effectively as being connected at the moment of issue.

Period A encompasses the entire lifespan of the investment. For SEIS, it runs from the company’s incorporation until the third anniversary of the share issue. For EIS, it includes a look-back window starting two years before the shares are issued and ends three years after the issue. All connection tests - including the 30% substantial interest test and the employee/director rules - apply continuously across this entire Period A window. (Period B is simply the post-issue portion of Period A).

Where this leaves you

The SEIS director connected persons rules are not impossible to navigate, but they reward early planning and punish late discovery. If you are a founder-director thinking about subscribing for SEIS or EIS shares in your own company, the first step is a structural check against the 30% ceiling and the s.167 / s.257BA director-as-employee tests. If you are an external investor about to take a board seat, the first step is a documented timeline that the HMRC Venture Capital Reliefs Team can satisfy itself with later.

This is a highly complex technical area so none of the above should be interpreted as professional advice.

If you would like a structural review of a director investment before the round closes, or a second opinion on a structure where advance assurance is already in flight, contact Steve Livingston FCA at IP Tax Solutions on stevelivingston@iptaxsolutions.co.uk or 0161 961 0096.