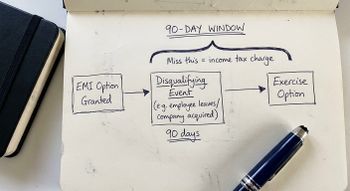

An EMI disqualifying event can cost employees an unexpected income tax bill running to tens of thousands of pounds. The window to act is 90 days. Miss it, and the tax relief that made the scheme worthwhile is gone.

Most companies only discover a disqualifying event has occurred when the damage is already done. A change of control, a shift in an employee's working pattern, or a badly timed amendment to option terms can each trigger one silently.

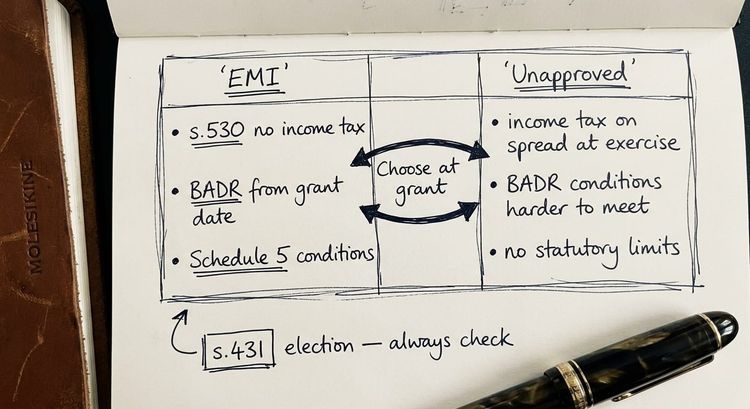

Understanding what constitutes a disqualifying event, and what the consequences are, is essential for any company operating an Enterprise Management Incentives (EMI) scheme.

What Is an EMI Disqualifying Event?

A disqualifying event is any event that causes a qualifying EMI option to lose its tax-advantaged status under ITEPA 2003, ss 532 to 536. When a disqualifying event occurs, the option does not immediately become worthless. However, the employee must exercise it within 90 days of the event to preserve the income tax exemption that makes EMI schemes so attractive.

If the option is exercised after that 90-day window, the "post-event gain" (the growth in share value from just before the disqualifying event to the date of exercise) becomes subject to income tax and National Insurance, rather than capital gains tax. This can be a significant and entirely unexpected charge.

The legislation identifies three categories of disqualifying events: those relating to the company, those relating to the employee, and a further group covering option variations and structural changes.

Company-Level Disqualifying Events

Section 534 ITEPA 2003 sets out the events at company level that trigger a disqualifying event in relation to a qualifying option.

The most common company-level event in practice is a change of control. If the relevant company becomes a 51% subsidiary of another company (s.534(1)(a)), or comes under the control of another company without becoming a 51% subsidiary (s.534(1)(b)), a disqualifying event occurs at the moment control passes. This is exactly the situation that arises in a typical trade sale.

There is an important carve-out: where the acquiring company grants replacement EMI options within six months of the change of control (under Sch 5, paras 39 to 43 ITEPA 2003), the change of control does not cause the original EMI options to fail. If no replacement options are granted, employees must exercise their original options within 90 days of the acquisition to retain their income tax exemption.

The third company-level trigger is where the relevant company ceases to carry on a qualifying trade (s.534(1)(c)). This happens where the company's activities come to consist substantially (broadly, more than 20%) of excluded activities such as dealing in land, financial services, leasing, property development, or operating hotels and care homes. Companies that pivot their business model, or acquire subsidiaries carrying on excluded activities, need to assess the EMI impact before those changes take effect.

Employee-Level Disqualifying Events

Section 535 ITEPA 2003 deals with events at the employee level. Two circumstances trigger a disqualifying event here.

The first is straightforward: when the employee ceases to be employed by the relevant company (or, in a group structure, by any member of the group). Resignation, dismissal and redundancy all bring this about.

The second is less obvious and catches more companies unaware. The working time requirement under Sch 5, para 26 ITEPA 2003 requires the employee to commit at least 25 hours per week, or (if less) 75% of their total working time, to the business of the relevant company. If the employee's actual working time falls below that threshold on average across a tax year, a disqualifying event is treated as occurring at the end of that tax year under s.535(2) ITEPA 2003.

In practice, this catches employees who move to part-time arrangements, take up consultancy work alongside their employment, go on extended unpaid leave, or reduce their hours as part of a flexible working arrangement. HMRC confirmed, by concession, that working time failures caused directly by the Covid-19 pandemic did not trigger disqualifying events. That concession was specific to Covid-19 and does not extend to other reasons for reduced hours.

Other Disqualifying Events: Option Variations and Share Capital Changes

Section 536 ITEPA 2003 catches a further category of events that are disqualifying by virtue of changes to the option itself or to the company's share capital.

Any variation of the terms of the option that either increases the market value of the shares under option, or causes the option to fail the requirements of Schedule 5, is a disqualifying event (s.536(1)(a)). Amending exercise conditions, adjusting performance thresholds, or extending the exercise period in a way that affects value or compliance can all trigger this provision.

Alterations to the share capital of the relevant company that affect share values and cause the Schedule 5 requirements to no longer be met (s.536(1)(b) and (c)) are also disqualifying events. Not all share capital alterations trigger the rule: only those falling within section 537.

A conversion of EMI option shares into a different class of share is also a disqualifying event under s.536(1)(d), unless the conversion falls within the whole-class exception in section 538.

Finally, where the grant of a CSOP option to an employee causes the combined value of unexercised EMI and CSOP options to exceed £250,000, a disqualifying event occurs in relation to the EMI options under s.536(1)(e) read with section 539. Companies operating both EMI and CSOP schemes need to check aggregate option values before each new grant.

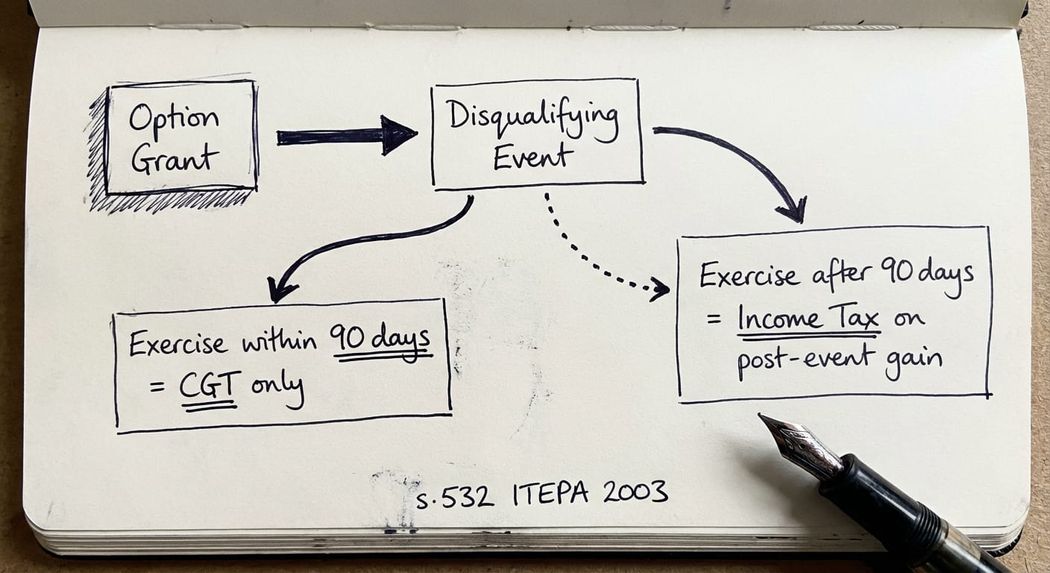

The 90-Day Window: What It Means in Practice

The 90-day window under section 532 ITEPA 2003 is the central mechanism that determines whether a disqualifying event is merely an inconvenience or a significant tax cost.

If the option is exercised within 90 days of the disqualifying event, the full income tax exemption on exercise is preserved. The employee pays CGT on any gains from grant to exercise, typically at Business Asset Disposal Relief rates where available.

If the option is exercised more than 90 days after the disqualifying event, the post-event gain (the growth in share value from the date immediately before the disqualifying event to the date of exercise) is charged to income tax under section 476 ITEPA 2003. This can produce a substantial and unexpected tax charge.

The practical problem is that many EMI scheme rules do not include provisions allowing early exercise in the event of a disqualifying event. Exit-based schemes restrict exercise to the period immediately before a sale or flotation. Where the scheme rules do not permit early exercise, employees cannot act within the 90-day window even if they are aware of it.

Key takeaway: The 90-day window runs from the date the disqualifying event actually occurs, not from the date anyone discovers it. A company that identifies a historic disqualifying event after the fact cannot restart the clock.

What to Do When a Disqualifying Event Occurs

When a disqualifying event occurs, the immediate priorities are to notify affected employees, identify whether the scheme rules permit early exercise, and assess the tax position.

If the event is a change of control on an acquisition, the first question is whether the acquiring company will offer replacement EMI options. Replacement options within six months preserve the qualifying status of the arrangements and avoid the need for early exercise. If replacement options are not going to be granted, employees should be advised to exercise their original options within 90 days of the change of control.

If the event is an employee-level trigger, such as a working time breach, it is worth checking whether the breach is temporary. HMRC takes the position that a disqualifying event occurs at the end of the tax year where the average working time test is failed across that year (s.535(2)). In some circumstances, the employee may still be within the 90-day window at the point the event is identified.

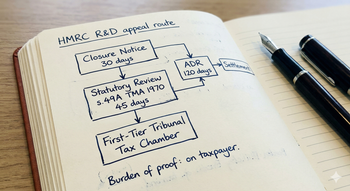

Where HMRC opens an enquiry into the scheme itself, under Sch 5, para 46 ITEPA 2003 (which HMRC may do within 12 months of the notification filing deadline), the same principle that applies in any tax dispute applies here: respond promptly, address the technical points squarely, and take specialist advice before engaging with HMRC enquiry defence.

Frequently Asked Questions

What is an EMI disqualifying event?

An EMI disqualifying event is any event that causes a qualifying EMI option to lose its tax-advantaged status under ITEPA 2003, ss 532 to 536. If the option is not exercised within 90 days of the event, the growth in share value after the event becomes subject to income tax rather than capital gains tax on exercise.

How long do employees have to exercise their EMI options after a disqualifying event?

Employees have 90 days from the date of the disqualifying event to exercise their options and preserve the income tax exemption. This period was extended from 40 days by Finance Act 2013 for disqualifying events occurring on or after 17 July 2013.

Does a company sale always trigger an EMI disqualifying event?

A change of control is a disqualifying event under s.534 ITEPA 2003. However, if the acquiring company grants replacement EMI options within six months of the acquisition (under Sch 5, paras 39 to 43 ITEPA 2003), the change of control does not cause the original options to fail. If no replacement options are offered, employees must exercise their original options within 90 days to retain their income tax exemption.

Can a change in an employee's working hours trigger a disqualifying event?

Yes. The working time requirement under Sch 5, para 26 ITEPA 2003 requires the employee to commit at least 25 hours per week (or 75% of their total working time, if lower) to the business. If the employee's actual working time falls below that threshold on average across a tax year, a disqualifying event is treated as occurring at the end of that tax year under s.535(2). Part-time working, consultancy work alongside employment, and extended unpaid leave are all potential triggers.

What happens if employees cannot exercise their options within 90 days because the scheme rules prevent it?

This is a serious problem for many exit-based EMI schemes, where options can only be exercised on a sale or flotation. If the scheme rules do not include provisions allowing early exercise on a disqualifying event, employees will not be able to act within the 90-day window. The post-event gain will then be subject to income tax on eventual exercise. Companies should review their scheme rules at the outset to confirm that early exercise provisions are in place.

Can HMRC open an enquiry into whether EMI options are qualifying?

Yes. HMRC has the power to open an enquiry into an employer's EMI notification within 12 months of the notification filing deadline under Sch 5, para 46 ITEPA 2003. An enquiry results in a closure notice stating HMRC's decision as to whether the EMI requirements are met. Any adverse notice can be appealed within 30 days.

Is Your EMI Scheme at Risk?

If your company has recently gone through an acquisition, a funding round, a restructuring, or a significant change in employee working arrangements, it is worth reviewing the EMI scheme against the disqualifying event provisions before a problem crystallises.

I work with companies and their advisers on EMI scheme complications, including disqualifying event analysis, replacement option structuring on acquisitions and HMRC enquiries into qualifying company status. If you are concerned about the impact of a recent event on your scheme, get in touch to discuss the position.