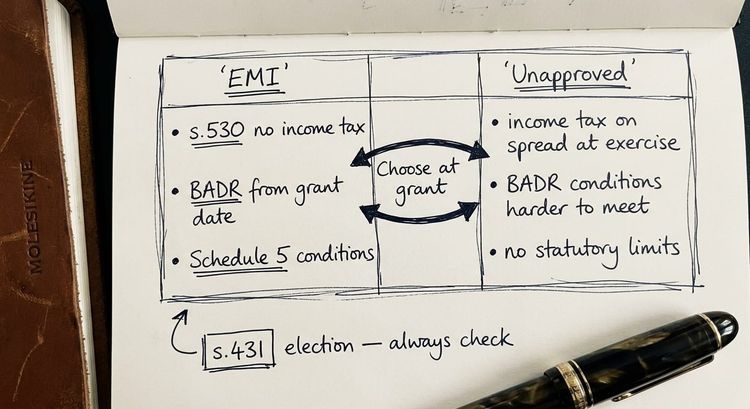

An EMI scheme that is working as intended is one of the most tax-efficient structures available to a UK trading company.

The employee exercises options at the grant-date market value, the growth in share value is taxed as a capital gain rather than income, and Business Asset Disposal Relief (BADR) can apply to reduce the CGT rate to 18% in 2026/27. But those advantages disappear, partially or entirely, if a disqualifying event occurs and the option is not exercised promptly.

Understanding what triggers an EMI disqualifying event, and what the 90-day window actually means in practice, is essential for any company running a scheme.

This article explains different categories of EMI disqualifying event under ITEPA 2003, ss 532-539, the tax consequences of missing the deadline, and the practical steps to take when a complication arises.

What Is a Disqualifying Event in an EMI Scheme?

An EMI disqualifying event is a statutory term for any occurrence that causes an EMI option to lose some or all of its qualifying status under the EMI code in ITEPA 2003, Part 7, Chapter 9.

The events are set out across three sections of the legislation:

- s.534 (company events),

- s.535 (employee events), and

- s.536 (other events).

The combined effect of ss 532-539 determines the tax treatment where an option is exercised after a disqualifying event has occurred.

Critically, a disqualifying event does not automatically destroy the option. The option remains exercisable. What changes is the tax treatment if the employee waits more than 90 days before exercising.

Company-Level Disqualifying Events (s.534 ITEPA 2003)

Section 534 sets out the events at company level that trigger disqualification. These are:

- Change of control. The most commonly encountered trigger in practice. A disqualifying event occurs when the relevant company becomes a 51% subsidiary of another company (s.534(1)(a)), or comes under the control of another company (or that company and a connected person) without becoming a 51% subsidiary (s.534(1)(b)). This is why acquisitions and investment rounds involving a change of control require careful advance planning for EMI option holders.

- Cessation of qualifying trade. If the relevant company ceases to meet the trading activities requirement set out in Schedule 5, paragraphs 13-23 of ITEPA 2003, a disqualifying event occurs (s.534(1)(c)). Companies whose trade evolves, or who add activities that fall into the excluded categories under Schedule 5, risk triggering this.

- Failure to begin a qualifying trade. Where a company was a qualifying company at option grant only because it was preparing to carry on a qualifying trade, and either preparations cease or the initial two-year period ends without the trade commencing, a disqualifying event is treated as occurring under s.534(3)-(5).

One important exception applies under s.534(2): where replacement options are granted on a qualifying takeover (under Schedule 5, paragraph 41), the change of control is not treated as a disqualifying event in relation to the old option.

Employee-Level Disqualifying Events (s.535 ITEPA 2003)

Section 535 covers events arising from the employee's own position. Two triggers apply:

- Ceasing to be an eligible employee. A disqualifying event occurs when the employee ceases to meet the employment requirement in Schedule 5, paragraph 25 (s.535(1)(a)). This means leaving employment. When an option holder resigns, is made redundant, or otherwise ceases to be an employee of the relevant company (or, where applicable, a qualifying group company), a disqualifying event is triggered from that point.

- Breach of the working time commitment. A disqualifying event also occurs when an employee ceases to meet the requirement in Schedule 5, paragraph 26 (s.535(1)(b)). The working time test requires the employee's committed time to equal or exceed 25 hours per week, or if less, 75% of their total working time including self-employment. An additional deemed disqualifying event arises at the end of any tax year where the average reckonable time per week during that year fell below the statutory threshold (s.535(2)).

This second trigger is a trap for part-time workers and those whose work patterns change during the life of the option. Since 6 April 2023, individual working time declarations are no longer required when options are granted, which reduces the administrative burden. However, the working time condition itself remains firmly in place and must be monitored throughout the option's life.

Other Disqualifying Events (s.536 ITEPA 2003)

Section 536 sets out a further category of triggers that are less commonly encountered but highly significant when they arise:

- Variation of option terms. Any variation of the option's terms that either increases the market value of the subject shares, or results in the Schedule 5 requirements no longer being met, is a disqualifying event (s.536(1)(a)). In practice, any proposed amendment to an EMI option agreement must be reviewed against this provision before implementation.

- Alteration of share capital. Alterations to the share capital of the relevant company that affect the value of the option shares and involve the creation, variation or removal of rights or restrictions (under s.537(2)), or that are designed to increase the market value of the option shares for non-commercial reasons (under s.537(3)), can trigger a disqualifying event.

- Conversion of shares. A conversion of the shares to which the option relates into a different class is a disqualifying event under s.536(1)(d), except where the conditions in s.538(2) are met. Those conditions relate to the conversion being a whole-class conversion with the majority of the original class held by third parties, or to the company being employee-controlled by reference to those shares.

- Grant of an exceeding CSOP option. If the employee is granted a relevant CSOP option and the total market value of their unexercised employee options (EMI and CSOP) immediately after the grant exceeds £250,000, a disqualifying event is triggered under s.536(1)(e). This is a less common but important interaction to consider where an employee participates in multiple share schemes.

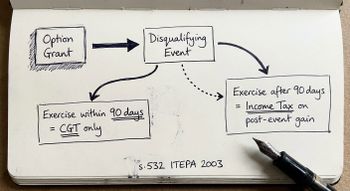

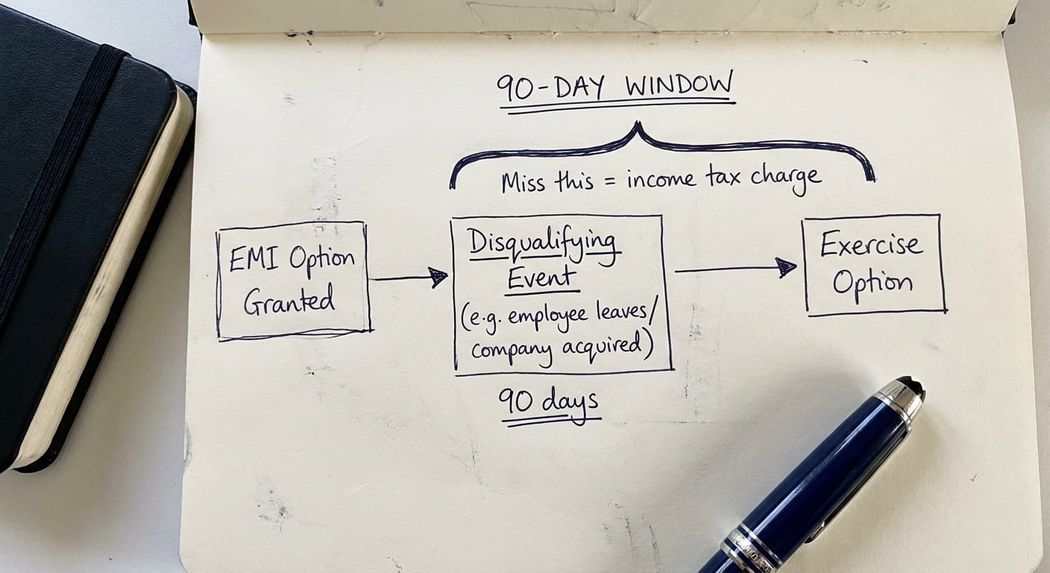

The 90-Day Window: What It Means and Why It Matters

Section 532 ITEPA 2003 is the mechanism that converts a disqualifying event into a tax cost. Where a disqualifying event has occurred and the option is exercised more than 90 days after the date of that event, the beneficial EMI treatment is partially lost.

Specifically, the income tax charge under s.476 applies to the "post-event gain": the amount by which the market value of the shares at the date of exercise exceeds their market value immediately before the disqualifying event (s.532(4), definition of PEG).

Growth in value from the original grant date to the disqualifying event is still taxed under the CGT regime. It is only the post-event growth that becomes subject to income tax.

The 90-day period was extended from 40 days by FA 2013, with effect for disqualifying events occurring on or after 17 July 2013.

In our experience, two practical problems arise with the 90-day window.

- option holders and companies often do not identify the disqualifying event promptly. A change in an employee's working pattern, for example, may not be flagged until the annual review. By that point, the 90-day period may already have passed.

- many exit-based EMI schemes include no provision allowing exercise on a disqualifying event. Where the scheme rules require exercise only on a sale or flotation, the employee may have no mechanism to act within 90 days even if they are aware of the event. This is a drafting point that deserves attention at the scheme design stage.

What Happens If You Miss the 90-Day Window?

If the option is exercised more than 90 days after the disqualifying event, the post-event gain is charged to income tax (and potentially NICs) under s.476. This is in addition to, not instead of, any capital gains treatment on the pre-event growth.

In a scenario where a company is sold a year after an employee left (the disqualifying event), the income tax charge on the post-departure gain can be substantial. The employee's position is no longer equivalent to that of a founding shareholder taxed at capital gains rates throughout. BADR will not apply to the income element. Where the disqualifying event was cessation of employment, the employee's gain will also fail the BADR employment test for the period following departure.

Where HMRC investigates an EMI scheme and identifies that a disqualifying event was not reported or acted upon, the consequences can extend to PAYE and NIC liabilities for the employer. Specialist advice on the full implications is strongly advisable, and in our practice this kind of situation calls for the same structured approach we apply to any complex HMRC challenge. For companies facing broader HMRC scrutiny of their tax arrangements, the considerations are similar to those involved in a formal HMRC enquiry and dispute advisory engagement.

Replacement Options and Takeover Scenarios

Where a company is acquired, replacement options may preserve the EMI benefits of the original grant. The acquiring company must grant replacement options within six months of the takeover (Schedule 5, paragraph 42 ITEPA 2003). The total market value of the new option shares must equal the market value of the original option shares immediately after the replacement is granted.

Where no replacement options are offered, the original options must be exercised within 90 days of the change of control event. In a sale scenario, this is often manageable because the mechanics of the transaction create the liquidity to do so. But it requires the company, its advisers, and the option holders to have the process clearly documented before completion.

HMRC confirmed in Employment Related Securities Bulletin 33 (October 2019) that where replacement EMI options are granted on a company reorganisation involving the exchange of EMI options, a new working time declaration must be signed at grant. This requirement was subsequently relaxed for new declarations from 6 April 2023, but the Bulletin's position on replacement options should be noted for earlier schemes.

Practical Steps When a Disqualifying Event Occurs

If a disqualifying event arises or is suspected, the immediate priority is establishing the date with precision. The 90-day clock runs from that date under s.532(1)(b). The steps that should follow are:

Review the option agreement to confirm whether it permits exercise on a disqualifying event. If it does not, immediate legal and tax advice is needed to assess whether anything can be done.

Notify option holders of the event and the 90-day deadline. There is no statutory obligation to do this, but failure to inform employees creates practical and regulatory risk.

Consider the valuation position. If exercise is to proceed, the current market value of the shares needs to be established to compute both the income element and the capital gains element correctly.

Assess whether the event needs to be reported. EMI options must be reported through the ERS annual return. A disqualifying event, and any subsequent exercise, requires accurate reporting.

Take specialist advice on the PAYE and NIC implications if the option is exercised late. Where income tax applies, the employer may have PAYE obligations depending on the type of shares received.

Key takeaway: A disqualifying event does not end an EMI option, but it starts a 90-day clock. Miss that window, and the growth in value after the event becomes subject to income tax rather than capital gains tax. Early identification and immediate action are essential.

Frequently Asked Questions

What is an EMI disqualifying event?

An EMI disqualifying event is a statutory trigger under ITEPA 2003, ss 533-536 that causes an EMI share option to lose some of its tax-advantaged status. Common examples include the employee leaving the company, the company coming under the control of an acquirer without offering replacement options, and the company ceasing to carry on a qualifying trade. The key consequence is that the option must be exercised within 90 days to preserve the beneficial income tax treatment.

What happens if I exercise my EMI option after 90 days of a disqualifying event?

If you exercise your EMI option more than 90 days after a disqualifying event, the growth in share value between the date of the disqualifying event and the date of exercise is taxed as employment income rather than a capital gain. This can significantly increase the tax cost, particularly where the share value has risen substantially after the triggering event. The pre-event growth remains within the CGT regime.

Does leaving my employer automatically trigger an EMI disqualifying event?

Yes. Ceasing to be an eligible employee under Schedule 5, paragraph 25 of ITEPA 2003 is a disqualifying event under s.535(1)(a). From the date of departure, the 90-day clock begins. If the EMI scheme rules permit exercise on a disqualifying event, leaving employment is therefore the trigger to review your options urgently.

Can a company acquisition trigger a disqualifying event on EMI options?

Yes, in most cases. Where the relevant company becomes a 51% subsidiary of another company, or comes under the control of an acquirer, a disqualifying event occurs under s.534(1)(a)-(b). The exception is where the acquiring company grants replacement EMI options within six months under Schedule 5, paragraph 42. If no replacement options are granted, EMI option holders must exercise within 90 days of the change of control to retain the income tax exemption.

What is the 30% material interest barrier in EMI schemes?

The material interest test in Schedule 5, paragraph 28 of ITEPA 2003 prevents an individual from holding qualifying EMI options if they have a material interest in the company, broadly meaning a shareholding (with associates) of more than 30% of the ordinary share capital or voting rights. This is an eligibility condition at grant and does not operate as a disqualifying event as such, but it can prevent an option from qualifying in the first place where a founder or significant investor also participates in the scheme.

Does a reduction in working hours trigger a disqualifying event?

Potentially yes. If the employee's working time falls below 25 hours per week on the company's business (or below 75% of total working time if that figure is lower), a disqualifying event may arise under s.535(1)(b) or may be treated as occurring at the end of the relevant tax year under s.535(2). Employees whose hours change materially, including those moving to part-time arrangements, should review the position promptly.

Do EMI disqualifying events need to be reported to HMRC?

Yes. Employers must report EMI option grants, exercises, and lapses through the Employment Related Securities (ERS) annual return filed with HMRC. A disqualifying event, and any exercise that takes place after one, must be reflected accurately in that return. Errors or omissions can attract HMRC scrutiny and, depending on the circumstances, result in PAYE and NIC exposure for the employer.

Getting Specialist Advice

EMI disqualifying events are one of those areas where the gap between knowing the rules exist and knowing exactly what to do when they arise in a live situation is significant. The interaction between the 90-day window, the scheme rules, the valuation position, and the reporting obligations creates a set of moving parts that can go wrong quickly.

If a disqualifying event has occurred in your company's EMI scheme, or if you are uncertain whether one may have arisen, I would be glad to review the position with you. I have advised companies through change of control transactions, departure scenarios, and scheme complication issues where specialist guidance was needed at short notice.

Contact me at stevelivingston@iptaxsolutions.co.uk or call 0161 961 0096.