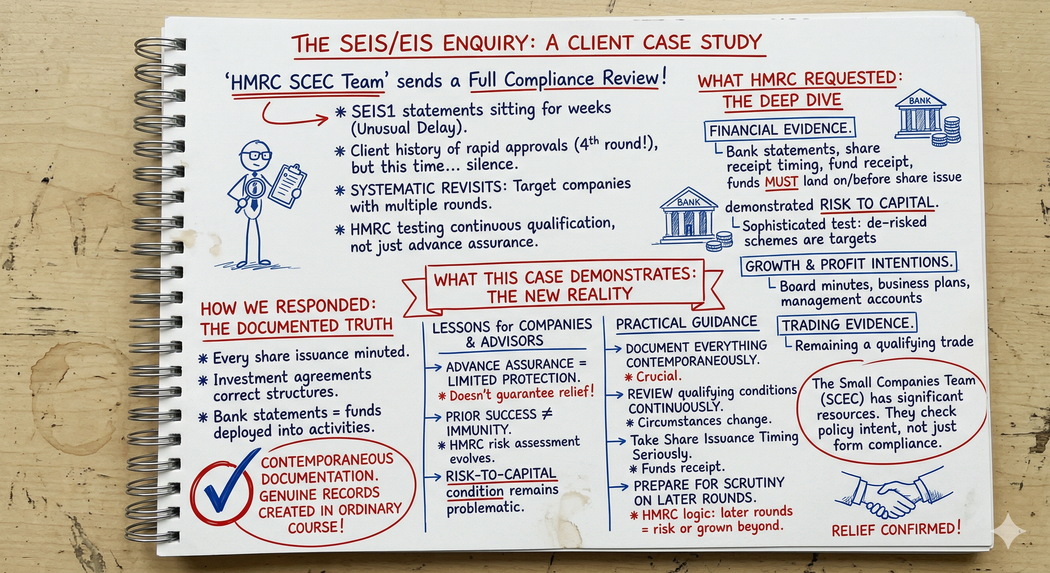

When a letter from HMRC's Small Companies Enterprise Centre (the specialist HMRC team that deals with SEIS & EIS) landed in our inbox, we knew exactly what was coming.

The SEIS1 compliance statements had been sitting with HMRC for weeks. For this client - on their fourth SEIS investment round, with advance assurance, and a history of 24-48 hour approvals - the unusual delay told us everything we needed to know.

HMRC was conducting a full compliance review.

This wasn't a random audit. The extended SCEC HMRC Team has been systematically revisiting companies that have raised multiple SEIS/EIS rounds, particularly where significant amounts have been deployed. They're testing whether companies continue to satisfy the qualifying conditions throughout their life, not just at the point of advance assurance.

What HMRC Requested

The enquiry letter was thorough:

Financial evidence: Bank statements demonstrating the receipt and issue of shares from investment funds, with particular attention to timing. HMRC wanted to verify that funds were injected on or just before each relevant SEIS share issue.

Risk to capital demonstration: Detailed explanation of how the company still satisfied the risk-to-capital condition. This is crucial - HMRC has become increasingly sophisticated in identifying companies that may have de-risked to the point where the relief no longer applies.

Growth and profit intentions: Evidence that the company maintained genuine intentions to grow and generate profit. Board minutes, business plans, management accounts and strategic documentation all came under scrutiny.

Trading evidence: Confirmation that the company remained a qualifying trade throughout the relevant period, with particular focus on any activities that might constitute excluded trades.

The implicit question underlying all of this: did the company genuinely qualify for SEIS relief, or had circumstances changed materially since advance assurance was granted?

How We Responded

We had everything documented:

- Every share issuance had been properly minuted.

- Investment agreements were complete and evidenced the correct share structures.

- Bank statements showed clear deployment of funds into qualifying activities.

- Board minutes demonstrated ongoing growth intentions and commercial decision-making consistent with a risk-taking enterprise.

Crucially, we had contemporaneous documentation. Not documents created after the fact to satisfy HMRC, but genuine business records created in the ordinary course of the company's activities.

HMRC processed all compliance statements as originally filed. No amendments, no denials, no withdrawal of relief.

What This Case Demonstrates:

Advance Assurance Provides Limited Protection

Advance assurance is HMRC's initial view that the company will likely be a qualifying company when it issues shares. It does not guarantee that relief will ultimately be available.

HMRC explicitly retains the right to review qualifying conditions when compliance statements are filed. In practice, this means the real test comes 12-18 months after the shares are issued, when Form SEIS1 or EIS1 is submitted.

Companies with advance assurance can - and increasingly are - facing substantive enquiries at the compliance statement stage.

Prior Success Offers No Immunity

Our client had successfully claimed SEIS relief three times previously. Each round had been processed quickly, with no questions asked.

This fourth round triggered a full enquiry.

HMRC's risk assessment evolves. As companies mature, raise additional capital, and scale their operations, they naturally move closer to the boundaries of what constitutes a qualifying company. Multiple SEIS/EIS rounds can themselves trigger additional scrutiny - HMRC wants to ensure companies haven't outgrown the relief while continuing to claim it.

The Risk-to-Capital Test Remains Problematic

The risk-to-capital condition, introduced in 2018, continues to generate the most enquiries. HMRC views this as their strongest weapon against "capital preservation" schemes disguised as qualifying investments.

In practice, HMRC examines:

- Whether the company has sufficient assets relative to investment received

- Whether downside protection exists through security, guarantees, or agreements

- Whether the business model genuinely involves risk of loss

- Whether management decisions demonstrate profit-seeking rather than capital preservation

Companies that have received multiple investment rounds need to be particularly careful. As they mature, build asset bases and de-risk operationally, they can inadvertently fail the risk-to-capital test even if their underlying business model remains unchanged.

Practical Guidance for Companies and Their Advisors:

Document Everything Contemporaneously

The single most important factor in defending HMRC enquiries is contemporaneous documentation. Board minutes, investment agreements, business plans and financial records created at the time carry infinitely more weight than documents created retrospectively.

If HMRC believes documentation has been created to justify a claim after the fact, they will discount it entirely.

Review Qualifying Conditions Continuously

Don't assume that qualifying at the point of share issuance means qualifying throughout the three-year period. Circumstances change. Business models evolve. Companies that qualified at incorporation may no longer qualify 18 months later.

Regular reviews - particularly before filing compliance statements - can identify issues while there's still time to address them.

Take Share Issuance Timing Seriously

The precise timing on which shares are issued matter enormously.

Issued too early i.e. the cash landing post share issue, can invalidate the qualifying status.

Issued too late and it can look like a loan to equity conversion (which is not allowable, unless structured as an ASA).

Prepare for Scrutiny on Later Rounds

Repeat SEIS/EIS compliance certificates might receive minimal scrutiny, particularly for clearly qualifying companies with advance assurance. Later rounds face heightened review.

HMRC's logic: if you're still raising SEIS/EIS capital three or four years after incorporation, either your business model has problems (risk to capital) or you've grown beyond qualifying status (gross assets, employee numbers and/or the independence condition).

The Broader Context

HMRC's approach to SEIS and EIS has tightened considerably since 2018. The Small Companies Enterprise Team has been significantly resourced, and their technical capability is arguably amongst the strongest across HMRC.

They're moving beyond simple compliance checks toward substantive reviews of whether companies genuinely satisfy the policy intent behind the reliefs. Companies that treat SEIS/EIS as a routine tax planning exercise - rather than genuine risk capital for qualifying activities - are increasingly exposed.

This creates real risk for companies that have claimed relief in good faith but without rigorous attention to ongoing qualifying conditions.

Conclusion

Our client's case had a positive outcome because everything was documented correctly from day one. But the enquiry itself - unexpected, given their history - demonstrates the evolving risk environment. It also causes stress for the founders and investors alike.

Companies raising SEIS/EIS investment need to approach compliance with the assumption that HMRC will review everything when statements are filed. Advance assurance helps, but it's not conclusive. Prior success helps, but it's not immunity.

The companies that survive these enquiries are the ones that treated SEIS/EIS compliance as an ongoing obligation, not a one-time exercise.

If your company has raised material SEIS or EIS investment - particularly across multiple rounds - the time to ensure everything is bulletproof is before HMRC opens the file. Reach out for assistance.

IP Tax Solutions specialises in defending SEIS and EIS structures against HMRC enquiry. With deep experience handling complex compliance cases, we help companies and their investors protect substantial tax reliefs that HMRC increasingly challenges.