HMRC's refusal of a SEIS advance assurance application is one of the most disorienting moments for an early-stage founder or their adviser. You followed the process, submitted what seemed like a complete application, and HMRC has come back saying it will not give advance assurance.

The question is: what does rejection actually mean, and what can you do next?

This guide sets out why SEIS advance assurance applications are rejected, your options after a refusal, and whether the investment can still proceed.

What SEIS Advance Assurance Is (and What It Isn't)

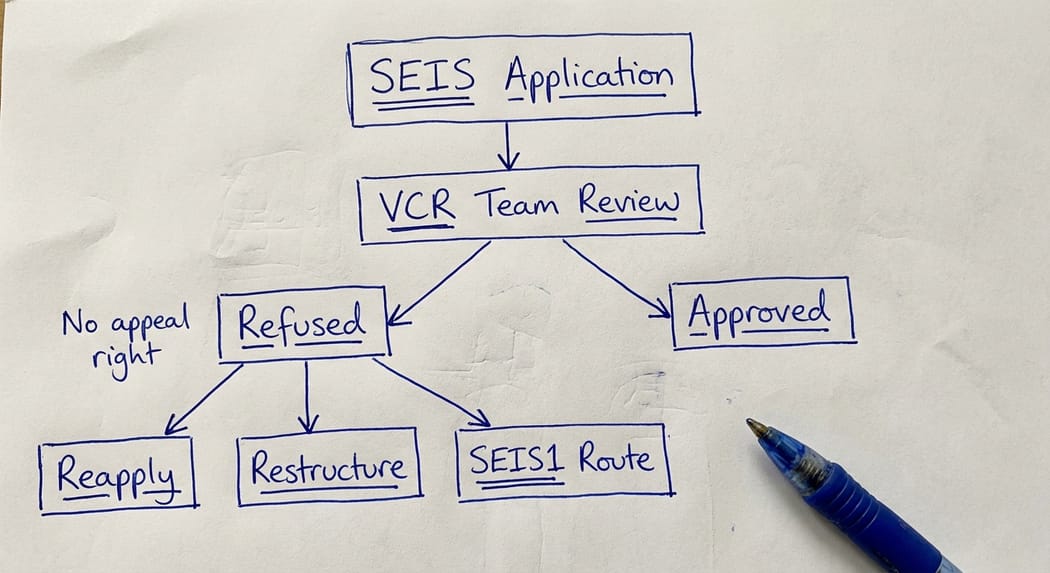

Before addressing rejection, it is worth being clear on what advance assurance actually provides. The service is operated by HMRC's Venture Capital Reliefs (VCR) Team and is, in HMRC's own words, "a non-statutory, discretionary service." There is no right of appeal against a VCR Team decision.

An advance assurance is HMRC's view, at a point in time, that a proposed share issue would qualify for SEIS relief. It is not a guarantee. It does not cover individual investor eligibility. It does not confirm that the company will remain in compliance throughout the three-year holding period. It covers only the specific share issue described in the application.

Obtaining advance assurance is optional. The SEIS legislation (Part 5A of ITA 2007, ss.257A to 257HJ) does not require it. Companies can issue shares and then apply to HMRC for the SEIS1 compliance certificate through the statutory route.

Advance assurance is simply a comfort mechanism, and most investors and angel networks expect to see it before committing funds.

Why HMRC Rejects SEIS Advance Assurance Applications

The VCM guidance at VCM60250 sets out the specific grounds on which HMRC will decline to give advance assurance. The most common in practice are:

The risk-to-capital condition is not satisfied. Under s.257AAA ITA 2007 (inserted by Finance Act 2018), the investment must carry a significant risk that investors will lose more capital than they gain as a return, and the company must have genuine long-term growth objectives. HMRC applies a principles-based test and will refuse assurance where the investment looks like a capital preservation arrangement. Low-risk structures, preference-like investor protections, or business models that generate steady income rather than genuine growth will trigger concern.

The company does not meet the issuing company conditions. The SEIS company conditions in ITA07/s.257D and VCM34000 are tight. For shares issued on or after 6 April 2023, the company must be carrying on a new qualifying trade that started no more than three years before the share issue. Gross assets must not exceed £350,000 immediately before or after the share issue. The company must have 25 or fewer employees. It must not have made a previous EIS, SEIS, or VCT investment.

Disqualifying arrangements. Where the structure suggests the investment will not carry genuine commercial risk (for example, the company pays raised capital to subcontractors before receiving customer payments, or marketing materials describe the investment as lower risk), HMRC will likely refuse (VCM60260).

Insufficient information. HMRC will not give an opinion if the application does not provide enough detail to assess eligibility. Applications without a proper business plan, without named investors (for first-time applicants), or without clear use-of-funds statements will stall or be refused.

Shares already issued. If the company has already issued the shares in question, HMRC will not process an advance assurance application - it defeats the object, "advance" assurance being the key here. The company must instead submit a compliance statement (form SEIS1(VCS) v2.1) through the statutory route.

The Most Common Practical Reasons for Rejection

In practice, the rejections I see most frequently fall into a smaller number of categories.

The trade timing rule. The new qualifying trade must have started within three years of the share issue (two years for shares issued before 6 April 2023). Companies that have been trading quietly for several years before deciding to raise SEIS investment can easily fall foul of this, sometimes without realising it. A pre-trading period, a period of consultancy income, or a predecessor business can all cause problems here.

Risk-to-capital in the structure. HMRC scrutinises term sheets and investment agreements closely. Investor protections that look commercially standard (anti-dilution provisions, preference on exit, repayment terms with limited downside) can undermine the risk-to-capital condition. The VCR Team is experienced at spotting structures that reduce investor exposure to genuine capital loss.

Narrative inconsistency. Applications fail where the business plan, use-of-funds narrative, and Articles of Association tell a slightly different story. HMRC looks across all submitted documents for inconsistencies. A pitch deck suggesting the business is a vehicle for a single contract project rather than a growing trading company will create doubt about the long-term growth requirement under s.257AAA ITA 2007.

Speculative applications. For first-time applicants, HMRC requires named investors and amounts. Applications that cannot demonstrate genuine investor interest, or that list vague investor pools, are likely to receive a refusal or a request for further information that, if not satisfied, leads to closure of the application.

Your Options After a SEIS Advance Assurance Rejection

A refusal is not a final determination that SEIS relief is unavailable. It is important to understand what it does and does not mean.

HMRC's stated position (VCM60250) is that "refusal does not signal HMRC's final position on legislative application." HMRC may still examine the facts when the company submits its compliance statement after shares have been issued. The two decisions are distinct.

That said, a refusal is a meaningful signal. It tells you that HMRC's current view is that the investment either does not meet the conditions or that there is insufficient information to confirm that it does. You have four practical options.

Reapply with a restructured or better-evidenced application. If the refusal was based on insufficient information, a more complete resubmission may succeed. If it was based on a structural issue such as risk-to-capital, restructuring the investment and reapplying may resolve the problem. Note that HMRC engages in no more than two rounds of correspondence after issuing an initial opinion (VCM60270), so each round needs to be well-prepared.

Restructure the investment and the company. Sometimes the refusal identifies a genuine problem that needs to be addressed before shares are issued. This might involve revising the share rights, removing preference-like protections from the term sheet, clarifying the use of funds, or addressing the trade timing issue. Getting this right before issue is considerably easier than trying to fix it after shares have been allotted.

Issue shares without advance assurance and proceed through the statutory compliance route. A company can issue SEIS shares without advance assurance and then submit form SEIS1 to HMRC, which triggers the compliance statement process. This carries risk, particularly for investors who will not know whether their relief is confirmed until HMRC processes the compliance statement. In a situation where advance assurance has been refused, investors need to understand this risk clearly before proceeding.

Take specialist advice before doing anything else. Where HMRC has not given a clear reason for refusal, or where the reason given is technical (such as a risk-to-capital concern), it is worth getting specialist input before deciding on the next step. The wrong response, whether reapplying without addressing the underlying issue or issuing shares on the assumption the compliance statement will be approved, can result in investors losing relief they believed was secure.

A refusal of SEIS advance assurance is not, by itself, a determination that the investment does not qualify. But it is a signal that something in the application or the structure has not satisfied HMRC, and it should be treated seriously.

Can You Proceed Without Advance Assurance?

Yes, but with important caveats. The statutory route, submitting the SEIS1 compliance certificate after shares are issued, is how all SEIS claims ultimately obtain confirmation of investor relief. Advance assurance is a front-end filter, not a requirement.

The difficulty after a refusal is one of investor confidence. Most sophisticated investors, and particularly angel networks and SEIS fund managers, will not invest without advance assurance in place. If advance assurance has been refused and you proceed to issue shares, you should document carefully the basis on which you believe the investment qualifies, and ensure investors understand that HMRC's approval of the compliance statement is not guaranteed.

For companies where advance assurance has been refused on risk-to-capital or structural grounds, proceeding to issue shares without resolving those issues carries real risk that HMRC will also refuse the compliance statement, leaving investors without relief.

When to Get Specialist Help

The advance assurance process is managed by HMRC's specialist VCR Team. The officers handling applications are experienced and apply the guidance carefully. Where an application has been refused, getting a generalist accountant to resubmit the same application with minor changes is unlikely to change the outcome.

In my experience, the cases that turn around after an initial refusal are those where a specialist with genuine SEIS/EIS technical depth reviews the entire proposition, identifies the specific issue (whether structural, factual, or presentational), and rebuilds the application on that basis. That might involve restructuring the share rights, adjusting the use-of-funds narrative, revising the business plan, or, in some cases, advising the founder that the current structure cannot qualify and needs to be rethought before any investment is made.

The same principle applies here as in HMRC enquiry defence more broadly: HMRC's specialist teams have seen every variant of these arguments. An application that does not directly address the reason for refusal will not succeed on a second attempt. If you are facing a SEIS advance assurance refusal, particularly one involving risk-to-capital, connected persons, or trade timing, getting specialist input before the next step is worth the investment.

Frequently Asked Questions

Can I appeal a SEIS advance assurance rejection?

There is no formal appeal mechanism. The advance assurance service is non-statutory and discretionary, and HMRC's guidance (VCM60210) states that no appeal rights are available against VCR Team decisions. The alternatives are to reapply with a revised application, to restructure the investment, or to issue shares and proceed through the statutory compliance route.

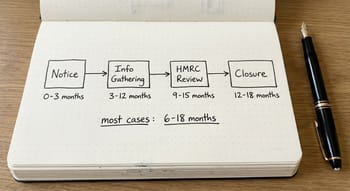

How long does HMRC take to process a SEIS advance assurance application?

HMRC targets 15 working days for standard applications and up to 40 working days for complex cases (VCM60270). In practice, applications involving more complex structures or incomplete information can take longer. HMRC will request further information rather than simply refusing if there are gaps in the submission.

What happens if shares have already been issued before advance assurance was obtained?

HMRC will not process an advance assurance application where the relevant shares have already been issued (VCM60250). The company must instead submit form SEIS1(VCS) directly. This is the compliance statement route and is how SEIS investor certificates are ultimately issued regardless.

Does a SEIS advance assurance refusal mean the company will not qualify for SEIS?

Not necessarily. HMRC's stated position is that a refusal "does not signal HMRC's final position on legislative application" (VCM60250). HMRC may approve the compliance statement even if advance assurance was refused. However, a refusal is a meaningful signal that something in the application or structure concerned HMRC, and it should not be ignored before shares are issued.

What is the risk-to-capital condition and how does it affect SEIS advance assurance applications?

The risk-to-capital condition was introduced by Finance Act 2018 and is codified in s.257AAA ITA 2007. It requires two things: the company must have genuine long-term growth objectives, and the investment must carry a significant risk that investors will lose more capital than they gain as a return. HMRC refuses advance assurance where it considers that the investment is structured to reduce capital risk, such as through preference-like terms, repayment arrangements, or business models that suggest income return rather than growth.

Can I reapply for SEIS advance assurance after a refusal?

Yes. A new application can be submitted if the circumstances have changed, the structure has been revised, or additional information is available. For ongoing correspondence about the same application, HMRC limits itself to two rounds after the initial opinion (VCM60270). A genuinely new application for a revised share issue would be treated as a separate matter.

What information does HMRC require in a SEIS advance assurance application?

The core requirements are set out in VCM60220: a business plan developed for genuine investor engagement (not just for HMRC), details of how funds will be used and how this supports the company's growth, confirmation that shares are ordinary shares without preferential rights, and for first-time applicants, the names and addresses of prospective investors and amounts they intend to invest. Inconsistencies between the business plan, the Articles, and the investment agreement are a common cause of applications stalling or being refused.

What to Do Next

If you have received a SEIS advance assurance refusal, the starting point is to understand precisely why. HMRC should have provided a brief explanation. In my experience, most refusals come down to one of three issues: risk-to-capital concerns in the structure, a trade timing problem, or insufficient information. Each requires a different response, and addressing the wrong issue will not change the outcome.

I advise founders, accountants, and corporate finance advisors on SEIS advance assurance applications and on resolving situations where an initial application has not succeeded. If you are dealing with a refusal and want to understand your options, get in touch or read more about Steve Livingston FCA and the work we do.