Patent Box reduces your corporation tax on innovation profits by up to 60%. But many companies overcomplicate it, miss deadlines, or structure it wrongly from the outset. Here is what you actually need to know.

Table of Contents

- What is the Patent Box?

- Who actually qualifies for Patent Box relief?

- How much tax can you save with Patent Box?

- Why most companies treat Patent Box too simply

- The four-stage calculation explained

- Common Patent Box mistakes that trigger HMRC enquiries

- Should you elect into Patent Box?

- Frequently asked questions

What is the Patent Box?

The Patent Box is a corporation tax relief that allows UK companies to apply a reduced 10% rate of tax to profits that come directly from patents and certain other intellectual property rights. Companies with patents, regulatory data protection certificates, supplementary protection certificates, or plant variety rights can elect to apply this reduced rate instead of paying corporation tax at the full main rate (currently 25%, or 19% for small companies).

The relief applies from 1 April 2013 onwards. The government introduced it to encourage UK companies to keep patent development, manufacturing, and commercialisation onshore. Without Patent Box, a UK company earning £100,000 profit from a patented product typically pays corporation tax at 25% (£25,000 tax). With Patent Box elected, the same profit is taxed at 10% (£10,000 tax). The tax saving is £15,000, but only if the company qualifies and structures the claim correctly.

Who actually qualifies for Patent Box relief?

Any UK company carrying on a trade can elect into Patent Box if it has qualifying IP rights and derives profits from those rights. You do not need to own the patent outright, be a technology company or file patents in multiple jurisdictions.

The practical qualifiers are:

You have qualifying IP. Broadly, this means you own (or have rights to) a granted patent, a patent pending, regulatory data protection (common in pharmaceutical and life sciences), a supplementary protection certificate, or a plant variety right. Trademarks, designs, know-how, and software copyright do not qualify on their own, although software embedded in a patented product may qualify if the patent covers the technical innovation.

You earn profits from that IP. You must derive income from exploiting the patent, whether through selling patented products, licensing patents to others, or providing services based on patented processes. A company that owns patents but does not commercialise them does not benefit from Patent Box.

You are a qualifying company. Most UK-resident companies qualify. A few do not: companies in an early-stage venture capital exemption situation (loss-making), companies within a tax-exempt group, or companies whose only income is exempt income. In practice, this excludes few profitable UK tax-paying companies.

You elect. Patent Box is not automatic. You must make a positive election under s.357A Corporation Tax Act 2010. Once elected, it applies to all your trades and continues indefinitely until you revoke it.

The common mistake here is thinking Patent Box is only for technology firms. Manufacturing companies, life sciences businesses, defence contractors, engineers and industrial process businesses all use it.

If you own a patent that generates profit, you can benefit from Patent Box.

How much tax can you save with Patent Box?

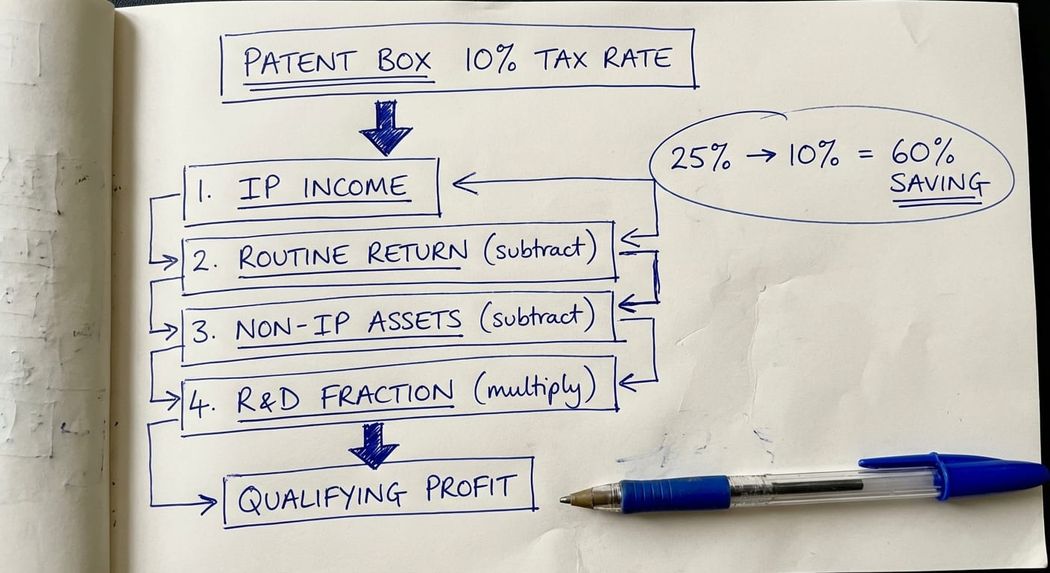

At the headline level, Patent Box reduces your effective tax rate from 25% (current main rate) to 10% on qualifying IP profits. That is a 15 percentage point difference and a 60% reduction in the tax bill on those profits.

In real numbers:

- If your patent generates £500,000 profit a year, the annual tax saving is approximately £75,000 (the difference between 25% tax and 10% tax on £500,000).

- If your IP profits are £50,000, the annual saving is approximately £7,500.

- If your IP profits are £2,000,000, the annual saving is approximately £300,000.

However, the figure is almost never as simple as "10% on total profits." Patent Box applies only to profits attributable to qualifying IP, not to routine business activity. Most companies selling patented products also earn routine profits from standard business operations, logistics, customer service or unpatented components. Only the slice of profit tied directly to the patented innovation qualifies.

This is where most companies get it wrong. They assume Patent Box applies to all profit. It does not.

Why most companies treat Patent Box too simply

The commonest error is submitting a Patent Box claim that ignores the qualifying profit calculation entirely. The company calculates total profit, assumes it all derives from the patent, and claims 10% tax on everything. HMRC flags this immediately.

Patent Box requires a structured four-stage calculation:

- Identify relevant IP income. Which profits come from exploiting the patent, as distinct from other business income?

- Remove the routine return. What profit would the company earn on this product even without the patent? This is "routine return" and is not eligible.

- Deduct non-IP assets. If the profit is attributable to branding, customer relationships, or other marketing assets rather than the patent itself, those profits do not qualify.

- Apply the R&D fraction. Only a proportion of remaining profits can qualify, based on the company's own R&D expenditure versus acquired IP or outsourced development.

Each step requires judgment and evidence. Companies that skip this and claim the full profit is qualifying get challenged.

The second error is missing the Patent Box election deadline or treating Patent Box as optional. You must elect into Patent Box by filing your corporation tax return for the year in which you want relief to apply, or by amending an earlier return within the normal time limits. Election is not automatic, cannot be made retroactively after the deadline, and once made is binding for all subsequent years unless revoked.

The third error is conflating Patent Box with R&D tax relief. They are different schemes. A company can claim both: R&D tax relief on qualifying development expenditure and Patent Box on qualifying profits from the resulting patent. Many companies claim R&D relief but do not claim Patent Box, missing 10+ years of potential savings once a product is commercialised.

The four-stage calculation explained

Stage 1: Relevant IP Income

Patent Box only applies to profits that derive from exploiting qualifying IP. You must identify which of your company's income streams come from the patent and which do not.

Example: You manufacture specialised manufacturing equipment and hold a patent on the core mechanism. You sell the patented equipment at £100,000 per unit. You also sell spare parts and provide maintenance contracts. The income from selling the whole unit includes the patented profit, but the spare parts income may not. Your first task is to separate these streams.

HMRC guidance says you must do this at a granular level. If you have multiple product lines, multiple patents, or licensing income, you identify separate "streams" of income tied to each IP right.

Stage 2: Remove Routine Return

Once you have identified IP income, you remove what HMRC calls the "routine return" — the profit the company would earn on this income even without the patent.

The routine return is not based on industry benchmarks or gross margin comparisons. Under CTA10/s357BJ, it is calculated using a statutory formula: 10% of specified costs allocated to each IP income sub-stream. These specified costs (called "routine deductions") are costs such as wages, premises and materials that any business would incur to generate the income, regardless of whether it held any IP. The routine return is simply 10% of those costs. The 10% rate is fixed in legislation and applies across all sectors.

What is contentious with HMRC is how you identify and allocate those routine costs between IP and non-IP income streams. Companies that ignore the routine return entirely - effectively claiming that 100% of their IP income is excess return attributable to the patent - will be challenged.

Stage 3: Deduct Non-IP Asset Profit

The remaining profit must be adjusted downward if it is attributable to non-IP assets: brand value, customer relationships, manufacturing scale, distribution networks, or market position.

Example: You hold a patent on a pharmaceutical formulation, but your profit also reflects the strength of your distribution network and brand reputation in the market. HMRC will say that part of your profit is attributable to brand and distribution, not to the patent alone. You must deduct this.

In many cases, this figure is small or zero. But in consumer goods, luxury products, or high-brand sectors, it can be significant.

Stage 4: R&D Fraction

This is the most technical step. You calculate a fraction:

R&D Fraction = (Your qualifying in-house and unconnected subcontractor R&D expenditure × 1.3) / (Your qualifying in-house and unconnected subcontractor R&D + Connected party R&D costs + Acquisition costs)

The numerator is uplifted by 30% to reward companies that keep R&D in-house or use unconnected subcontractors. This fraction is applied to the remaining qualifying profit. It ensures that only the proportion of profit arising from your own R&D (and unconnected subcontracted R&D) gets the Patent Box benefit. If you acquired the IP or paid connected parties to develop it, the profit attributable to those costs is taxed at the main rate, not Patent Box rate.

Example: You acquired a patent from another company for £500,000. You developed enhancements to that patent at a cost of £100,000 using in-house staff. Your R&D fraction is (100,000 × 1.3) / (100,000 + 500,000) = 130,000 / 600,000 = 0.2167 or roughly 21.67%. So only 21.67% of your qualifying profit gets Patent Box relief. The rest is taxed at the main rate.

This step captures the economic reality: if you have bought in the innovation, you should not get the same tax benefit as a company that developed it from scratch.

Common Patent Box mistakes that trigger HMRC enquiries

Mistake 1: Missing the Patent Box election deadline.

Patent Box is not automatic. You must make a positive election under s357A CTA 2010, and the latest you can do so is within 12 months of the fixed filing date of the return for the first accounting period you want it to apply. The election can be made in the return itself, or via an amendment to the return, provided the amendment is within that 12-month window.

Once the window closes, there is no provision for a late election and no route through SP05/01. The election is not a claim made annually; it is a one-off notice that applies to all trades and all subsequent accounting periods until revoked.

Many companies miss the deadline because they assume they can add Patent Box later. They can, but only while the amendment window is still open. Make sure your accountant diarises the election deadline alongside the filing deadline.

Mistake 2: Failing to segment income streams.

A company with multiple patents or multiple product lines must identify separate income streams and compute Patent Box separately for each. Some accountants compute a blended figure across all products. This will be challenged because HMRC expects stream-by-stream evidence.

Mistake 3: Claiming the entire profit is qualifying.

The most common challenge. The company submits a return claiming that 100% of trading profit qualifies for Patent Box. HMRC responds: "You have a manufacturing operation, a supply chain, customer service and a distribution network. What percentage of profit is genuinely from the patent alone?" The company usually has no answer, the computation is disallowed, and penalties apply.

Always compute and document the routine return. Use benchmarking data or industry comparative figures.

Mistake 4: Treating Patent Box as an R&D credit.

Patent Box and R&D tax relief are different reliefs for different stages of the business lifecycle. R&D relief is claimed on qualifying expenditure during the development phase. Patent Box is claimed on profits once commercialisation has started. Some companies claim both on the same profit, which is not allowed. Make sure your accountant distinguishes the two schemes.

Mistake 5: Misunderstanding how patent pending claims work.

You cannot reduce your tax payments while a patent application is pending. Instead, you track the profits from exploiting the invention during the pending period (for up to six years), and if the patent is granted, you claim the accumulated relief in the tax return for the year of grant via an election under s357BM CTA 2010. Earlier year returns are not amended; the relief is given entirely in the year of grant. If the patent application is rejected, no s357BM election can be made, so no Patent Box benefit ever arises for that product line and no earlier returns need unwinding. Many companies misunderstand this and either claim relief prematurely during the pending period, or fail to track profits ready for the year of grant.

Mistake 6: Missing the nexus adjustment for acquired technology.

If you have acquired any part of the IP (through purchase, licensing, or inbound acquisition of R&D), the R&D fraction applies. Many companies fail to calculate this fraction correctly, or simply forget to apply it. This is a high-risk area for enquiries because the tax saving can be substantial.

Should you elect into Patent Box?

Not every company should elect into Patent Box, even if they qualify. The calculation and ongoing compliance burden can be substantial. You should consider Patent Box if:

- Your patent-derived profit is significant. If patent income is less than 5% of overall profit, the admin burden may outweigh the saving. If it is 20% or more, Patent Box is worth investigating seriously.

- You have stable, identifiable IP profit streams. If your business is complex, with multiple patents, blended products or changing IP arrangements, Patent Box becomes harder to compute reliably. You need clear separation between IP and non-IP income.

- Your company expects ongoing profit from the patent. Patent Box is a long-term relief. If the patent will expire, be replaced or the product will be discontinued in a few years, you might not recover the cost of establishing the claim. Plan for the medium term at least.

- You have documented your R&D expenditure. The R&D fraction requires evidence of your qualifying R&D costs. If you have not tracked this, reconstructing it is time-consuming and often inaccurate. If you have good R&D records, this is easier.

- You can separate patent profit from routine profit with confidence. If your profit margins are hard to split or subject to significant judgment, Patent Box becomes audit risk. Clear, evidence-based splits reduce risk.

If you elect into Patent Box and later decide it is too complex or too risky, you can revoke the election. The revocation takes effect from the beginning of the accounting period in which you notify HMRC. You cannot cherry-pick years.

Frequently Asked Questions

Q: Can I claim Patent Box on software-based innovations?

A: Only if the software is protected by a qualifying patent and the patent covers the technical innovation, not just the code itself. Software copyright alone does not qualify. If you hold a patent covering a novel software algorithm or process, then profits from that patented software can qualify. The relevant income must derive from the patented innovation, not from generic software development.

Q: Do I need to own the patent outright, or can I license it?

A: You can claim Patent Box on licensed IP as long as you hold exclusive rights to the licence. If you are a licensee with rights to sublicense or to develop improvements, you may qualify. If you are paying a royalty to the licensor, your profit will be reduced by that royalty before the Patent Box computation applies, which reduces the benefit. Holding the patent outright gives you the largest benefit; licensing it in gives you a smaller benefit.

Q: If HMRC opens an enquiry into my Patent Box claim, what should I expect?

A: HMRC will ask to see the evidence supporting each step of the calculation: what profits derive from the patent, how you defined routine return, whether non-IP assets have been deducted and your R&D expenditure records. They will question how you separated profit streams and whether comparable company data supports your routine return assumption. If you are missing documentation, risk of adjustment is high. If your computation is sound and well-evidenced, HMRC often accepts it or negotiates a minor downward adjustment.

Q: Can I claim Patent Box retroactively if I did not elect when I should have?

A: No. Patent Box is optional and you must make the election within the time limit for amending your corporate tax return. For recent years, this is usually within 12 months of the filing date. If you have missed the deadline, you cannot go back and claim it. This is why accountants recommend reviewing Patent Box entitlement every year; missing one year is lost relief forever.

Q: What if my product line is phased out or the patent expires - does Patent Box stop automatically?

A: Patent Box relief applies to qualifying IP income in each accounting period. If the patent expires or the product is discontinued, there is no qualifying income from that source in future periods, so Patent Box relief naturally ceases for that stream. You do not need to formally revoke the overall election unless you want to stop claiming it entirely.

Q: Does Patent Box interact with R&D tax relief, and can I claim both?

A: Yes, you can claim both schemes on the same company. R&D tax relief is claimed on qualifying development expenditure (during the innovation phase). Patent Box is claimed on qualifying profits from the resulting patent (during the commercialisation phase). They apply at different times to different profit stages, so there is no overlap. However, ensure your accounting clearly distinguishes the two schemes to avoid HMRC confusion.

Q: If I am in a group of companies, can multiple group members claim Patent Box on the same patent?

A: Yes, provided each company meets the "active ownership" condition. To qualify, a group company must perform significant management activity in relation to the IP, not simply hold the legal title while another company does the work. If Company A owns the patent but Company B (in the same group) manufactures and sells the product under a licence, Company B can claim Patent Box if it manages the IP rights or performs further R&D on them. Different group members can also claim Patent Box on different products or patents. Group structures trigger additional rules around active ownership and transfer pricing, so specialist advice is recommended for multinational or complex group structures.

What To Do Next

Patent Box can deliver substantial tax savings, but only if you plan and compute it correctly from the outset. The most common route to HMRC enquiry is oversimplified claims that ignore the four-stage profit calculation.

If you hold patents and have not examined Patent Box relief, a short benchmarking exercise is worth doing: identify your patent-derived income, sketch out what proportion might be qualifying profit, and establish whether the relief is material. If the saving is more than a few thousand pounds a year, specialist input is justified.

If you are already claiming Patent Box and have not reviewed the calculation recently, a second opinion is prudent. HMRC enquiries into Patent Box can be expensive to defend if the computation lacks evidence or clarity.

If HMRC enquires into Patent Box, you will need to provide evidence for every step of the calculation. Having that evidence assembled and auditable from day one is the best defence.

If you are structuring a company acquisition or licensing IP from another group company, Patent Box planning should be part of the deal structure conversation. Getting the R&D fraction and profit allocation right at the transaction stage saves years of dispute later.

For complex Patent Box computations, group structure situations, or defence of an HMRC enquiry, specialist input is worth the cost. Patent Box disputes and computations are often worth referring to a specialist rather than attempting to navigate alone.

Questions about Patent Box relief for your company? Contact Steve Livingston LLB FCA to discuss your specific situation.