When Should an Accountant Refer Complex Innovation Tax Work to a Specialist?

The short answer: If your client faces an HMRC enquiry into R&D, a rejected SEIS/EIS advance assurance, subcontracted R&D with overseas elements or disputes over what qualifies under the R&D merged scheme, they need a specialist.

You can advise on routine claims and basic SEIS structure. But defence work, hard-to-classify costs, and HMRC disputes fall outside most general practice capability. The earlier you refer, the easier it is to recover the position.

What This Article Covers

- What accountants handle well (and shouldn't over-reach)

- Red flag issues that signal specialist referral

- When HMRC makes referral mandatory

- What a specialist does that a generalist cannot

- How referral arrangements work

- Timing: the cost of waiting

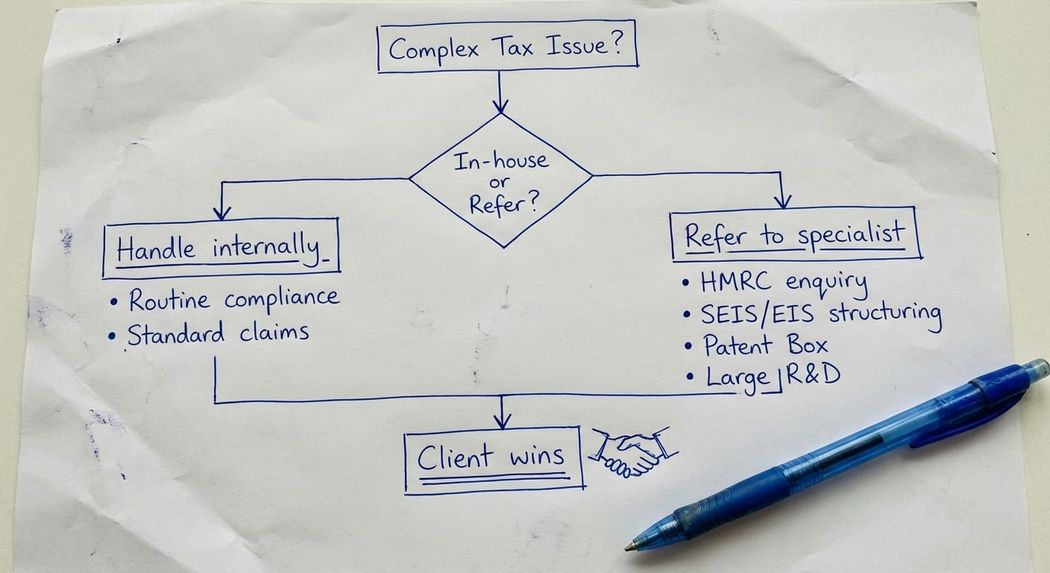

What Most Accountants Can Handle Alone

Straightforward R&D claims under the merged scheme. If a software developer or manufacturer is describing genuine R&D work, keeps decent records, the costs are clean and there's no HMRC attention, your team can prepare a solid claim. You know how to:

- Identify qualifying and non-qualifying activities (staffing, software, cloud, consumables)

- Apply the R&D intensity test correctly

- Calculate both the enhanced deduction (86% for SMEs) and RDEC credit rates

- Flag connected-party EPW and contractor rules

- Complete the Claim Notification Form (CNF) within the 6-month deadline

Your value here is control, cost and continuity of records. A clean claim that passes the first read is worth preparing in-house.

Basic SEIS advance assurance structuring. You can advise on the headline conditions: trading company, newly incorporated, active business test, financial health. If the structure is plain (single investor, no connected persons), you can prepare an application and take it through HMRC.

Initial consultancy on Patent Box. You understand the nexus approach and can identify straightforward cases where one patent covers one product line. Where the patent portfolio is simple and the numerator and denominator are clear, you can advise.

Non-dispute SEIS/EIS compliance statements. Where the company is thriving, no HMRC involvement and the investor structure is uncomplicated, a compliance statement is within reach.

Red Flags: When to Refer Immediately

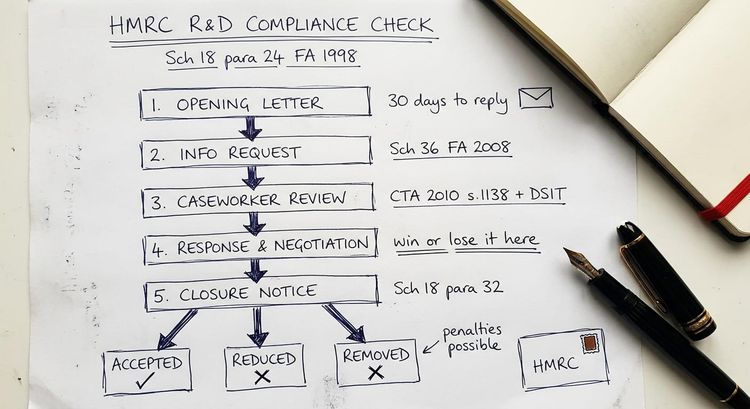

1. HMRC has opened an enquiry into R&D, SEIS/EIS or Patent Box

This is the point of no return. HMRC moves slowly, asks strategic questions, and tests your evidence under pressure. You need someone on your side who:

- Has defended claims to tribunal (not negotiated; defended)

- Understands HMRC's assessment logic and what they are really testing

- Can sit across the table from an HMRC enquiry officer and push back on weak reasoning

- Knows which documents move the needle and which are noise

If HMRC has sent a letter or opened a formal enquiry, your response will make or break the claim outcome. How you respond to the enquiry letter matters far more than how it was prepared.

Refer now. A specialist can co-advise you on the claim's foundation and help you hold the line during the enquiry. Your alternative is learning HMRC's playbook at the client's expense.

2. HMRC has alleged fraud or negligence in an R&D claim

Fraud allegations change the ballgame entirely. HMRC applies different standards of proof, different discovery rules, and different penalties. The claim is no longer "is the cost qualifying?" but "did the advisor know better?" and "is there a pattern of aggressive positions?"

A specialist who has handled fraud-allegation cases will:

- Understand the distinction between errors-of-law (defensible) and false claims (not)

- Know when to concede early to avoid penalty uplift and when to fight

- Prepare evidence packs that answer HMRC's real concern (was the advisor complicit?)

Do not attempt this alone. Refer within days of seeing the letter.

3. The R&D claim involves subcontracted work, overseas elements, or group R&D

Subcontractor rules, externally provided workers (EPWs), and overseas R&D carry strict conditions (ss. 1133-1136 CTA 2009). If any of these apply, the claim is medium-to-high risk:

- Subcontracted R&D: You must prove the contractor's underlying costs and apply a 65% cap unless connected-party rules shift the test. Most practices underestimate this burden.

- Overseas R&D: Work done abroad only qualifies if it would be wholly unreasonable for your company to replicate the necessary conditions in the UK or Northern Ireland (s. 1138A). HMRC tests this heavily. You need evidence of why the work had to be elsewhere, not just "that's where we have people".

- Group R&D: If company A funds R&D in company B or a sister company, you must distinguish payment (which qualifies) from participation (which tests benefit). Most accountants assume "they paid the invoice, so they get the relief". Often wrong.

Refer the moment you see any of these. The cost of a specialist's input up-front (a few hundred pounds) is trivial against the cost of a wrong position (entire claim disallowed plus penalties).

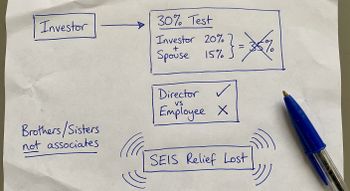

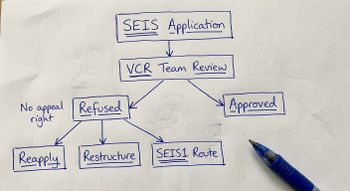

4. SEIS advance assurance has been rejected, or you suspect it will be

HMRC's advance assurance decisions are notoriously difficult to predict. If you've had a rejection, the application either missed a condition or HMRC found a reason to deny relief (e.g., connected persons, financial health failure, trading company status).

A specialist in SEIS advance assurance rejections will:

- Decode HMRC's reasoning and identify which condition actually failed

- Propose a restructure that cures the defect without losing tax benefits

- Reapply with a stronger, more detailed submission

If you're unsure your application will succeed, refer before submitting. HMRC's silence is not approval; rejection is costly and forces clients to restructure later.

5. The claim mixes R&D relief with other reliefs (film, video games, theatres, etc.)

Claims cannot overlap. If a company claims R&D relief and also qualifies for a theatre relief or video games relief, there are strict anti-overlap rules (s. 1040ZA CTA 2009). Mistakes here can void the entire R&D position and trigger penalty investigations.

Refer any claim that touches multiple relief regimes.

6. Patent Box: the group structure is complex or there is a licensing dispute

Patent Box computation relies on the nexus approach and clear tracing of qualifying income to the patent. If there are multiple patents, multiple product lines, cross-licensing, or disputes with related parties over who owns what, you are in specialist territory.

Refer before you calculate. A wrong nexus calculation can trigger a sustained HMRC enquiry.

7. The client has received prior HMRC enquiries or corrections on R&D or SEIS/EIS

If HMRC has challenged this client before, they are high-risk for future enquiry. HMRC's systems flag repeat claimants. Your file must be defensible from day one. A specialist review before claim submission can head off a second enquiry.

What a Specialist Does That a Generalist Cannot

Judgment under uncertainty. A specialist has seen 100+ claims, 20+ enquiries, and 5+ tribunal cases. They can tell you whether a cost that sits on the borderline will hold up under HMRC scrutiny. That judgment is worth thousands to a client facing an enquiry.

Tactical negotiation with HMRC. HMRC enquiry officers follow a playbook. A specialist knows the playbook. They know when to provide a document that moves HMRC toward settlement and when to hold firm. Generalists often over-disclose or assume all information must be volunteered.

Technical narrative and evidence packaging. Most practitioners know R&D relief mechanically. Few can write a narrative that threads the needle between "credible basis" and "technical certainty". A good narrative answers HMRC's unstated question before they ask it.

Group and cross-border structuring. If your client has overseas subsidiaries, parent-company R&D funding, or complex group IP ownership, the interactions between R&D relief, transfer pricing, and IP regimes require specialist knowledge.

How Referral Arrangements Work

You refer the client to a specialist for a specific piece of work. That work might be:

- Co-advice: Specialist reviews your draft claim and advises on risk; you amend and submit

- Full advisory: Specialist takes the lead on claim preparation; you remain on the file for continuity

- Defence: Client faces an HMRC enquiry; specialist takes over the response

- Second opinion: Client wants independent reassurance before submitting a claim you've prepared

- Restructure advice: SEIS/EIS application failed; specialist proposes restructure options

Most specialists charge by the hour or as a fixed fee for the scope. It is not a referral to a different firm for the whole engagement; it is a spot engagement with a specialist while you remain the relationship manager.

The handoff is smooth. You brief the specialist on what you've done, what the client's concerns are, and what outcome you're aiming for. The specialist delivers advice or a revised claim back to you. You integrate that into your work and own the final filing.

What the Cost of Waiting Looks Like

Claim submitted without specialist input. Cost: £1,000 to £3,000 in fees (your time or a junior's). Risk: borderline claim without disciplined evidence backing. Outcome: HMRC enquiry, 18-24 month delay, reputational risk if you have to concede mid-enquiry.

Claim challenged by HMRC. Cost: specialist defence engagement (£5,000 to £25,000+) plus internal rework, client stress, potential partial or full disallowance. Timeline: 2-3 years.

Specialist input before submission. Cost: £1,500 to £7,500 in specialist fees. Outcome: claim submitted with defensible structure, narrative, and evidence. HMRC enquiry risk drops by 60-70%. If enquiry happens, timeline to resolution is 12-18 months and outcome is typically favourable.

The math is simple: a few hundred pounds of specialist input before submission saves multiples of that in enquiry costs and risk.

Red Flags in Your Own Practice

Signs you are at risk of over-reaching:

- You are preparing multiple R&D claims per year without sending any to a specialist for review.

- A claim involves overseas R&D, subcontractors, or group structures and you haven't discussed it with a specialist.

- You have never looked up s. 1128 (externally provided workers definition) or s. 1133 (contractor rules) in the statute.

- You are not maintaining a rolling risk-grade of each client's R&D claims (low/medium/high).

- You don't have an internal checklist for CNF deadlines, AIF deadlines, or PCRT sign-offs.

If any of these apply, now is the time to build a referral protocol. HMRC's scrutiny of R&D claims is tightening. The Professional Conduct in Relation to Taxation (PCRT) standard now requires advisors to have a "credible basis" for positions. That standard is tighter than "not obviously wrong". You need to be confident, and confidence comes from specialist input.

When Should You Start the Referral Conversation?

Early is almost always better. The moment you see a claim that sits outside routine territory, mention it to the client: "This looks like we should get a specialist's eyes on this. It will cost an extra £2,000 but it will de-risk the claim significantly."

Most clients will accept. Those who push back ("it's just standard R&D") often later regret that decision when HMRC arrives.

How to Find and Vet a Specialist

Look for:

- Explicit enquiry defence experience (not just "we advise on R&D")

- References from other accountants (not just satisfied end-clients)

- A willingness to co-advise (joint letters, client meetings) rather than siloing the work

- Clear fee models and realistic timeline expectations

Ask:

- Have you defended an R&D claim to tribunal?

- How many HMRC enquiries have you settled in the last two years?

- Do you co-advise with accountants, or do you take full engagement?

- Can you provide a reference from another accountant who has referred work?

A good specialist wants accountants as referral partners. They know the referral flow is a mutual benefit. They will invest time in understanding your practice and your clients.

Frequently Asked Questions

Q: Can't I just hire a junior accountant to handle the more complex stuff in-house?

Not safely. Complexity in R&D claims comes from judgment, not volume. A junior can execute a schedule or populate a form. They cannot tell you whether a claim will survive HMRC scrutiny or what evidence is material. That judgment comes from experience. Your client is better served by a one-off specialist input than by a junior's guess.

Q: If I refer a client to a specialist, won't they poach the client from me?

Rarely, if you frame the referral correctly. Position it as: "We handle your accounts and general tax. For this specialist area, we bring in an expert." The client sees you as the coordinator and gatekeeper. A good specialist reinforces that. If the specialist tries to poach the client, they are not a good referral partner.

Q: What's a reasonable fee for a specialist to charge for reviewing a claim before submission?

Typically £1,500 to £3,500 for a medium-complexity claim. Some specialists offer fixed-fee review packages. Get a quote upfront and agree scope. For defence work (HMRC enquiry), expect £5,000 to £20,000+ depending on length and complexity.

Q: Do I lose credibility if I refer every complex claim to a specialist?

The opposite. You gain credibility because you are honest about the limits of your knowledge and you are protecting your client. Partners respect peers who know what they don't know and act accordingly.

Q: What if the specialist disagrees with my position on the claim?

That is a valuable moment. You get an independent technical view. If the specialist thinks you're right, you have confidence. If they disagree, you have time to adjust before HMRC sees it. Disagreement is not failure. It is early-warning risk management.

Q: Can a specialist review my work after I've submitted the claim to HMRC?

Yes, but it is more expensive and less effective. HMRC's first request will often probe the weak points. A specialist reviewing post-submission has less flexibility to reshape the narrative or evidence. If you've already filed, a specialist can help you respond to AIF or enquiry letters.

Q: How do I know if a claim needs a specialist review?

Use this test: Would you be comfortable defending this claim in front of an HMRC enquiry officer if you had to do it tomorrow? If the answer is "I'm not sure" or "I'd need to research", refer it.

The Bottom Line

Accountants are the gateway to innovation tax work. You see the clients, you prepare the accounts, you file the returns. But you are not specialists in R&D defence, SEIS/EIS structuring, or Patent Box computation. Nor should you be; it is not your practice.

Your value to clients is knowing when to refer, finding the right specialist, and staying in control of the relationship. Early referral on a complex claim can save tens of thousands of pounds in enquiry costs and reputational damage.

The firms that thrive are the ones that build referral partnerships. You become the trusted advisor who manages your clients' tax affairs comprehensively, bringing in specialists where needed, and protecting your clients' positions before HMRC ever arrives.

If you are managing innovation tax clients without a referral network, now is the time to build one.

Next Steps

If you are handling an R&D claim, SEIS/EIS application, or Patent Box case that sits outside your comfort zone, talk to a specialist before submission. The conversation is free, the input is invaluable, and the cost is modest against the risk.

To discuss a specific client matter or explore a referral arrangement, contact Steve Livingston FCA at IP Tax Solutions.

Resources and Related Reading

- How to Respond to an HMRC R&D Tax Credit Enquiry Letter

- SEIS Advance Assurance Rejected - What To Do Next

- R&D Tax Credit Defence - What It Is and When You Need It

- Professional Conduct in Relation to Taxation (PCRT) - UK tax profession standard

- CTA 2009 Part 13 - R&D Relief Legislation