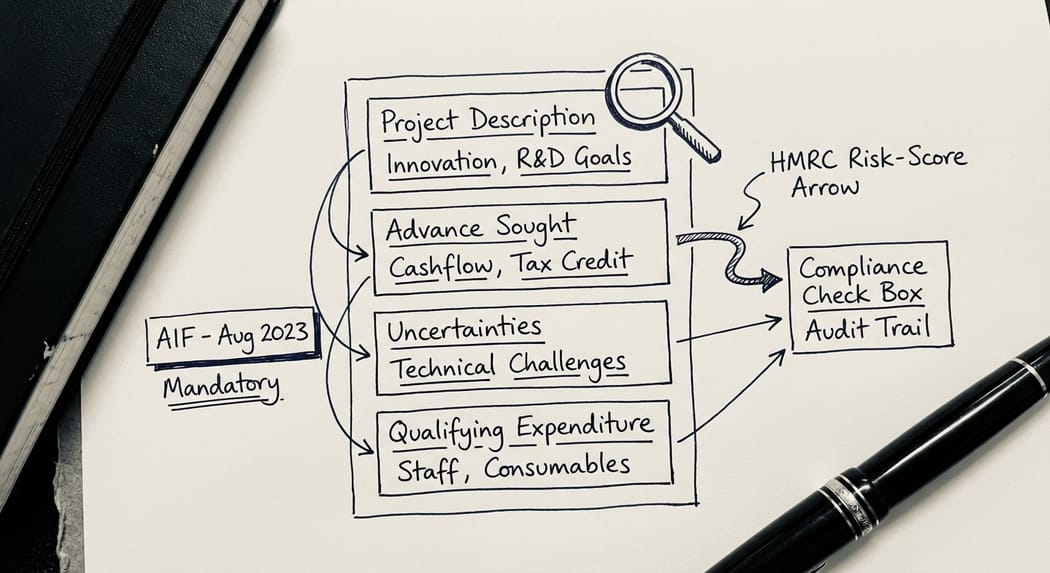

Since August 2023, every company making an R&D tax credit claim must submit an additional information form (AIF) to HMRC before, or at the same time as, filing its corporation tax return. Without it, HMRC will reject the claim.

More significant than the filing requirement, however, is what HMRC does with the AIF once it receives it. The R&D Compliance Centre now uses AIF submissions as the primary basis for risk-scoring claims and selecting which ones to open for enquiry. How you describe your R&D projects in the form may matter more than the numbers in the tax return itself.

This guide explains what the R&D additional information form requires, the mistakes that most commonly attract scrutiny, and how to write project descriptions that will withstand HMRC's review.

What Is the R&D Additional Information Form?

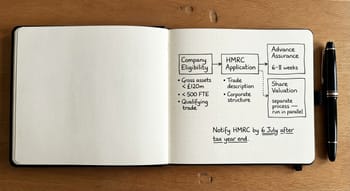

The R&D additional information form was introduced with effect from 8 August 2023. Any claim for R&D relief submitted on or after that date requires a completed AIF, regardless of the accounting period to which it relates.

The form is submitted online through HMRC's Research and Development Additional Information service. It sits outside the corporation tax return process. You do not submit it through the same channel as the CT600.

For accounting periods beginning on or after 1 April 2023, companies that have not claimed R&D relief in any of the three preceding years must also submit a pre-notification to HMRC. This is a separate requirement from the AIF and must be submitted within six months of the end of the accounting period. Missing the pre-notification window means the company loses its right to claim for that period entirely, with no mechanism to extend the deadline.

What Information Does the AIF Require?

The form collects information in three broad areas.

Company and agent details. This covers basic identification: company name, UTR, accounting period, and (if applicable) agent contact information. HMRC cross-references these against the corporate tax record.

Project descriptions. This is the most consequential section and the one where errors are most damaging. You must describe each R&D project in enough detail for HMRC to assess whether the work meets the statutory definition of qualifying R&D under the DSIT Guidelines (2023). Where there are three projects or fewer, all must be described individually. Where there are four or more projects, the company must describe sufficient projects to collectively cover at least 50 per cent of total qualifying expenditure, describing at least three projects. If more than ten projects would be needed to reach 50 per cent coverage, the ten with the highest qualifying expenditure must be described.

For each project, the form asks you to explain: the scientific or technological advance you sought, the scientific or technological uncertainties you encountered, and how you attempted to resolve those uncertainties. These three questions map directly onto the DSIT Guidelines test and onto the statutory definition in the Corporation Tax Act 2009.

Qualifying expenditure. You must provide a split of the total qualifying expenditure by category: staff costs, consumables, software, contracted-out R&D, externally provided workers, and payments to volunteers in clinical trials. The merged scheme form introduced from 1 April 2024 includes data licences and cloud computing as separate expenditure categories, reflecting their status as qualifying costs for accounting periods beginning on or after 1 April 2023. The numbers you enter here are checked against the amounts claimed in the CT return.

Why the Project Description Matters So Much

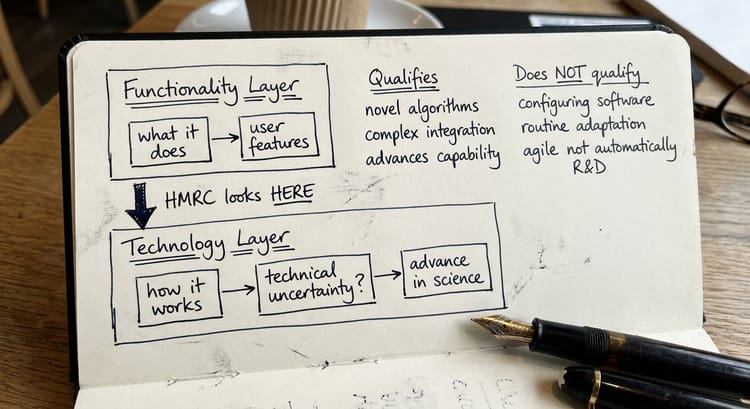

HMRC's R&D Compliance Centre reviews AIF submissions against the DSIT Guidelines test. The test has two limbs: the work must seek a scientific or technological advance, meaning it extends overall knowledge or capability rather than applying existing knowledge to a new commercial context; and it must involve resolving a scientific or technological uncertainty, something not known whether in general or to your specific team.

A description focused on the commercial output tells HMRC nothing about whether the work qualifies. "We built a new customer-facing platform" describes a product. "We sought to develop a real-time load-balancing algorithm capable of processing concurrent requests within sub-100ms latency, using an approach whose performance characteristics under dynamic load were not determinable without experimental work" describes R&D.

The compliance reviewers ask one question: would a competent professional in this field have known the answer at the outset? If the description does not surface a credible technical uncertainty, the claim is flagged for further review.

Key takeaway: The project description in the AIF is your first and most important line of defence. It creates the permanent record of what you said your R&D was when you filed. Everything in any subsequent enquiry is measured against it.

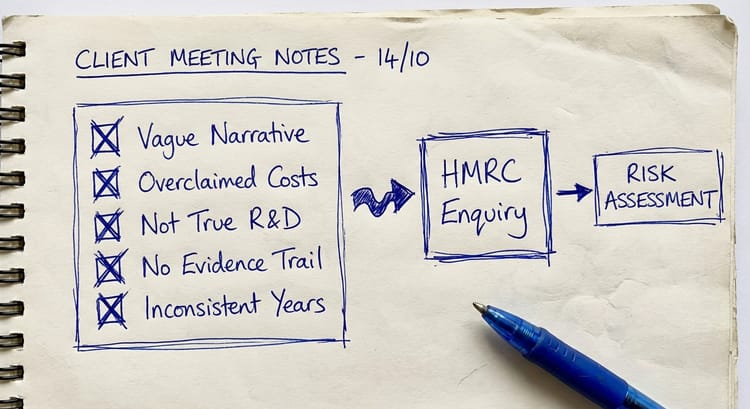

The Most Common AIF Mistakes That Trigger Enquiries

In our experience reviewing AIF submissions across a wide range of sectors, the following patterns account for the majority of avoidable compliance challenges.

Describing the product rather than the R&D process. This is the single most prevalent error. The AIF asks about the scientific or technological work, not the commercial project. Developing a novel product is not, in itself, R&D. The qualifying activity is the process of resolving specific technical uncertainties within that development. Every sentence of the project description should relate to the technical problem, not the commercial outcome.

Vague uncertainty statements. "We were not sure if the system would work as intended" does not constitute a qualifying uncertainty. The uncertainty must be grounded in specific technical parameters. What precisely was unknown? What was the technical reason it was unknown? Could a competent professional in the field have predicted the outcome without experimental work?

Boilerplate descriptions. HMRC has been transparent that it identifies claims where near-identical project descriptions are used across multiple companies, with only the company name and product substituted. Advisers who apply this approach are creating serious risk for their clients. A compliance review that finds generic template language will treat this as a signal of a poorly substantiated claim.

Incorrect expenditure categorisation. The transition to the merged scheme from 1 April 2024 introduced data and cloud computing as new qualifying categories, but only where those costs are used directly in qualifying R&D activity. Including them without proper analysis of whether they meet the qualifying conditions is a recurring source of HMRC challenge.

Missing the pre-notification for new claimants. The six-month window is unforgiving. Companies returning to R&D claims after a three-year break are particularly vulnerable because the requirement may not be on their advisers' radar. Miss the deadline, and the entitlement to claim for that period is lost.

How HMRC Uses the AIF to Score Claims for Enquiry

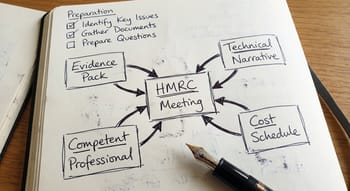

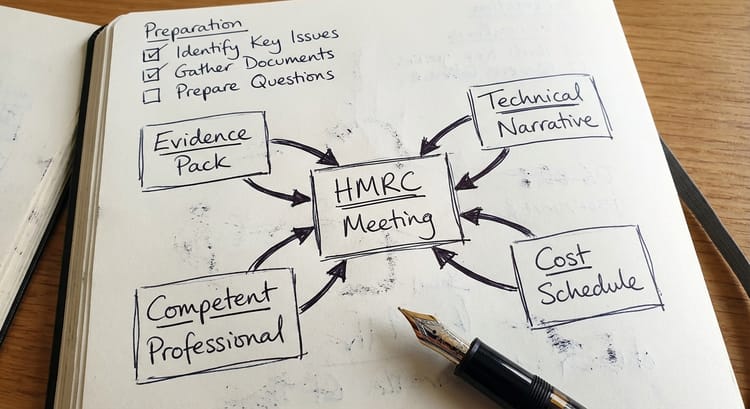

HMRC has been explicit that the AIF supports its compliance programme. The R&D Compliance Centre was established specifically to review claim quality, and AIF content is its primary tool for identifying cases that warrant closer examination. Compliance reviewers work through a structured assessment: does the project description identify a genuine scientific or technological advance? Is the uncertainty credible and specific? Are the qualifying costs consistent with the described activity?

Claims that score poorly on these dimensions attract an information request under Schedule 36, Finance Act 2008. That request typically asks for contemporaneous project records, technical reports, staff timesheets and additional explanation of the uncertainties described in the AIF. Where HMRC concludes that the claim was made on an inaccurate basis, the consequences extend beyond disallowance of the relief. In cases where the inaccuracy is judged to be deliberate, HMRC has raised fraud allegations in R&D claims, with penalties and (in serious cases) criminal referrals following.

The form also creates a contemporaneous record. If HMRC later opens an enquiry, the AIF description is the starting position. Inconsistencies between the AIF, the technical report and project documentation are a significant vulnerability at that stage.

Writing a Project Description That Will Withstand Scrutiny

The clearest test of whether a project description is adequate is whether it could stand alone as evidence of qualifying activity, without reference to anything else. A compliance reviewer should be able to read the description, understand what was technically uncertain, understand what was tried, and reach a defensible conclusion about whether the work qualifies.

These principles apply consistently to well-written AIF descriptions.

Write in first person and make specific claims.

"We sought to determine whether [specific technical outcome] could be achieved using [approach] under [conditions]" is more defensible than "the project involved advanced technical development work."

Address the DSIT Guidelines tests explicitly. The form structure follows the advance and uncertainty tests. Your descriptions should address each in turn: what advance were you seeking, and why was it uncertain whether you could achieve it?

Name the technical disciplines involved. Reference the specific technical expertise in the project descriptions too. Claims where qualified engineers, scientists, or software architects are clearly identified carry more credibility than those described only in headcount terms.

Document the resolution process, including failures. The work does not need to have succeeded to qualify. The AIF asks how you attempted to resolve the uncertainty, not whether you succeeded. Including failed approaches and pivots in methodology often strengthens a description. HMRC expects genuine R&D to involve iteration, not a straight line from problem to solution.

FAQ: R&D Additional Information Form

What is the R&D additional information form?

The R&D additional information form is a mandatory submission that companies must make to HMRC before or when filing a corporation tax return claiming R&D relief. It requires a description of qualifying R&D projects, including the scientific or technological advance sought and the uncertainties encountered, together with a breakdown of qualifying expenditure by category.

When did the AIF become mandatory?

The AIF became mandatory for claims submitted on or after 8 August 2023, following the Finance (No. 2) Act 2023. This applies to all claims regardless of the accounting period to which they relate.

How do I submit the R&D additional information form?

Through HMRC's Research and Development Additional Information service online. It is a separate submission from the CT600 and must be completed before the corporation tax return is filed.

What happens if an R&D claim is filed without the AIF?

HMRC will reject the claim. The AIF is a statutory condition of relief, not supplementary documentation. Without it, no R&D relief can be granted for that period.

Can HMRC use the AIF to open an enquiry?

Yes. The R&D Compliance Centre reviews AIF submissions and uses the project descriptions and expenditure data to score claims for compliance risk. A poor-quality or inconsistent AIF increases the likelihood of HMRC opening a formal compliance check.

What is a pre-notification for R&D, and how does it differ from the AIF?

These are two separate requirements. The pre-notification applies only to new claimants, or those who have not claimed in the previous three years, and must be submitted within six months of the end of the accounting period (special rules apply where a previous claim was filed via an amended return). Missing it means the company loses its entitlement to claim for that year entirely. The AIF is a separate requirement that applies to all claimants at the point of filing.

How detailed does the AIF project description need to be?

Sufficient for HMRC to assess whether the work meets the statutory definition: a scientific or technological advance secured through resolving a scientific or technological uncertainty. Generic, product-focused, or boilerplate descriptions do not meet this standard. Specificity about the technical uncertainty, the approaches tried, and the outcome is what HMRC looks for.

What to Do If HMRC Questions Your AIF

An information request focused on your R&D additional information form is not an accusation, but it is a signal that the claim needs to be defended with precision. The position you set out at the information-gathering stage shapes the entire subsequent process. Concessions made early, or explanations given without full consideration of the statutory framework, can be difficult to recover from.

If you need help completing an R&D additional information form, or if HMRC has already raised questions about an existing claim, IP Tax Solutions works exclusively on innovation tax matters. Contact us to discuss your position.