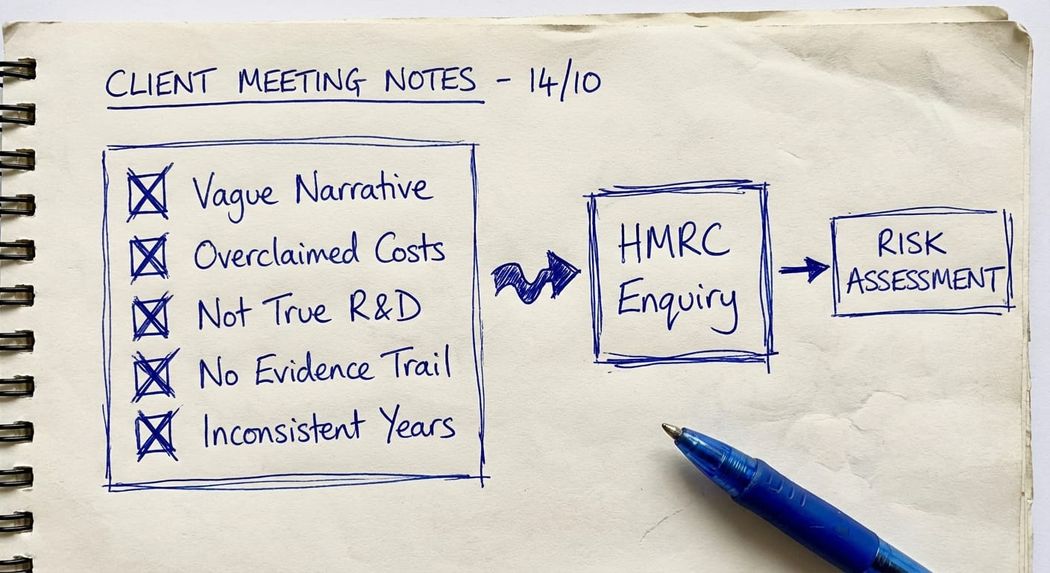

Every year, HMRC opens thousands of compliance checks into R&D tax credit claims. Some are random. The majority are not. The triggers vary, but the underlying causes are often the same: claims that are poorly constructed, inadequately evidenced, or built on a flawed understanding of what actually qualifies as R&D. Understanding the most common R&D tax credit claim mistakes is the first step toward not making them.

For a detailed look at what specifically causes HMRC to select a claim for scrutiny, see our article on what triggers an HMRC R&D enquiry. This article focuses on the underlying errors that make claims vulnerable in the first place.

1. The Technical Narrative Describes What Was Built, Not How Uncertainty Was Resolved

This is the most common mistake we see, and the hardest to fix retrospectively.

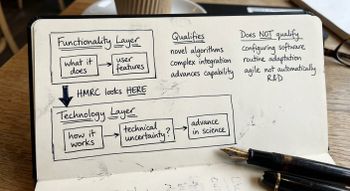

The technical narrative is the document (or section of the CT600 additional information form) where the company explains why its work qualifies as R&D. Many narratives describe the product or system that was developed, written in the style of a product brochure: what it does, what it delivers, who benefits from it.

HMRC does not want to know what you built. HMRC wants to know what scientific or technological uncertainty existed, what the current state of knowledge was before the project began, what specific investigations were conducted to resolve that uncertainty, and what advance in knowledge resulted.

The DSIT Guidelines 2023 (which replaced the BEIS Guidelines and set out the criteria HMRC uses to assess qualifying R&D under s.1138 CTA 2010) require that the work seeks to achieve an advance in overall knowledge or capability in a field of science or technology, not merely a company-specific improvement. A narrative that cannot articulate the baseline and the uncertainty will not satisfy this test.

In our experience, narratives prepared by non-specialist advisors or by the company itself without proper technical input are often competent descriptions of the project but poor explanations of the qualifying R&D. That gap is what HMRC exploits.

2. Staff Costs Are Claimed Without Proper Apportionment

Staff costs are typically the largest element of any R&D claim. They are also the element HMRC can most easily verify by cross-referencing the claim against PAYE records and company accounts.

Problems we regularly identify include:

Director time claimed at implausible percentages. A director running a ten-person company who also leads sales, manages client relationships, handles administration, and sits on the board cannot spend 90% of their time on qualifying R&D. Claims that show this draw immediate scrutiny.

No time recording to support the apportionment. HMRC will ask for contemporaneous evidence of how the qualifying percentages were arrived at. A spreadsheet prepared at the time of making the claim, working backwards from a desired figure, is not contemporaneous evidence.

Including indirect support activities that exceed what is permitted. Under the merged scheme introduced by Finance Act 2024, and under the prior SME scheme, there are specific rules about which support activities qualify and to what extent. Qualifying indirect activities (QIAs) must be directly connected to and support work that itself qualifies as R&D.

Payroll inconsistencies. If the claim includes a salary figure for an employee that does not reconcile with their PAYE record or P60, HMRC will ask why. This is a basic cross-check that is frequently overlooked.

3. Routine Development, Adaptation, and Integration Are Treated as R&D

The definition of R&D in s.1138 CTA 2010 is strict. It requires scientific or technological uncertainty: a situation where a competent professional working in the field would not know whether something is scientifically or technologically possible, or how to achieve it.

Work that does not involve that uncertainty does not qualify, regardless of how technically complex or commercially important it is.

In practice, we see claims that include:

- Adapting or configuring existing software for a new client or market context

- Integrating two established systems using standard APIs

- Applying known techniques to a new sector without any element of genuine uncertainty

- Performing acceptance testing, quality assurance, and validation activities

- Making iterative improvements to an existing product where the improvement is commercially motivated but technically straightforward

None of these activities qualify under the DSIT Guidelines 2023. Including them in a claim does not just risk those costs being disallowed: it raises questions about the integrity of the rest of the claim.

4. Subcontractor Costs Are Included Without Checking the Rules

The rules governing subcontractor costs have changed significantly and vary depending on which scheme applies.

Under the merged scheme (Finance Act 2024), a company can claim for the qualifying element of contractor payments where the company is the one that initiates and bears the cost of its own R&D project, contracting out elements of that work to third parties. The "contracted-out R&D" provisions in the merged scheme mean that the entity that commissions and initiates the R&D (the "customer" or "decision-maker") can claim for qualifying contractor payments, while the entity that performs R&D under commission (the "contractor") can generally no longer claim for that work. An exception applies where the customer is an irrelievable client, for example a company or person not within the charge to UK corporation tax.

Under the former SME scheme, payments to unconnected subcontractors were restricted to 65% of the amount paid. For connected subcontractors, the claimable amount was restricted to the lower of the amount paid and the subcontractor's own relevant expenditure incurred on the qualifying R&D activities. This second restriction was frequently overlooked in group structures where one entity employed the R&D staff and recharged costs at a premium to an operating company making the claim.

Connected party structures in particular require careful analysis before any claim is submitted.

5. There Is No Contemporaneous Evidence to Support the Claim

R&D tax credit claims can be submitted up to two years after the end of the accounting period to which they relate. This means a company might be making a claim for work carried out three years ago, long after projects have concluded, teams have changed, and records have been tidied up or discarded.

When HMRC opens a compliance check, one of the first requests is for contemporaneous project records: project plans, meeting notes, technical reports, test logs, version control histories, internal communications, and similar documentation. If this documentation does not exist, or exists only in summary form prepared after the event, the claim is extremely difficult to defend.

The absence of contemporaneous records does not automatically mean the R&D did not happen. But it makes it very difficult to demonstrate that it did, and HMRC will draw adverse inferences from the gap.

The solution is straightforward in principle and often neglected in practice: keep records as the work progresses. This is especially important for software development claims, where the R&D content of a project can be contested and the boundary between qualifying and non-qualifying work shifts as the project develops.

6. The Claim Is Inconsistent With Prior Years or Company Circumstances

HMRC reviews R&D claims in the context of a company's full tax history. Year-on-year inconsistencies are a consistent trigger for compliance checks.

Examples we have seen include:

- A company that claimed no R&D in Years 1 and 2 but then claimed 40% of total costs as qualifying R&D in Year 3, with no explanation of why the R&D activity appeared suddenly

- A company whose claim showed a significant increase in qualifying staff costs without any corresponding increase in headcount or payroll

- A company whose technical narrative described entirely different projects to those referenced in prior-year claims, without acknowledging that the earlier projects had concluded

- A company claiming R&D credits in a sector where HMRC had identified widespread non-compliance, with a claim size disproportionate to its turnover and staff count

None of these situations automatically indicate fraud or error. But each of them creates an anomaly that HMRC will want explained, and that explanation needs to be prepared with care.

7. The Claim Is Prepared Without Adequate Specialist Input

R&D tax credits are a specialist area. The technical assessment of what qualifies requires both scientific or engineering knowledge (to assess whether genuine uncertainty exists) and tax knowledge (to map the qualifying work to the cost categories and scheme rules). Very few advisors hold both.

Claims prepared solely by generalist accountants, or solely by technology consultants without tax expertise, frequently contain errors in one dimension or the other. Claims prepared by non-specialist R&D boutiques using generic templates are often technically accurate in structure but thin on the specific analysis that survives HMRC scrutiny.

In our experience, the claims that hold up under enquiry are those where the technical narrative was written or reviewed by someone with direct technical knowledge of the field, and where the costs were quantified by someone who understood the statutory scheme.

What Happens If HMRC Finds Mistakes in Your Claim

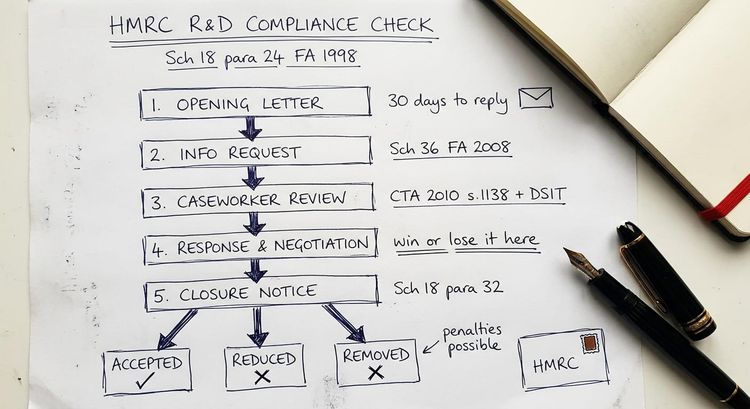

If HMRC opens a compliance check and identifies errors, the consequences depend on how significant the errors are and whether HMRC considers them to reflect careless or deliberate behaviour.

At minimum, the overclaimed relief will be repaid with interest. A penalty will typically follow, calculated as a percentage of the tax at stake, with the rate depending on whether the behaviour was careless, deliberate, or concealed.

For larger claims or where HMRC suspects deliberate overclaiming, the enquiry can escalate significantly. Understanding how long an HMRC R&D enquiry takes is important context here: a serious enquiry can run for 18 months or more and consume significant management time and cost.

If you have already received an opening letter, the approach from that point is covered in our guide on how to respond to an HMRC R&D enquiry letter.

Key takeaway: The most common R&D tax credit claim mistakes are not obscure technical errors. They are failures of process: narratives written without adequate technical analysis, costs apportioned without adequate records, and qualifying criteria applied without adequate understanding of the DSIT Guidelines. Most can be avoided with proper preparation and the right specialist input before the claim is submitted.

Frequently Asked Questions

What are the most common mistakes in R&D tax credit claims?

The most common mistakes are: a technical narrative that describes project outputs rather than the resolution of scientific or technological uncertainty; overclaimed or poorly apportioned staff costs; including routine development work that does not meet the DSIT Guidelines 2023 definition of qualifying R&D; subcontractor costs claimed outside the applicable scheme rules; and no contemporaneous documentation to support the claim if HMRC enquires.

Why does HMRC open an enquiry into an R&D claim?

HMRC selects claims for compliance checks based on a range of risk indicators including claim size relative to company turnover, year-on-year inconsistencies in qualifying expenditure, industries with known compliance problems, and intelligence from third parties. Claims that contain R&D tax credit claim mistakes, even unintentional ones, increase the risk of selection because they often produce the statistical anomalies that trigger HMRC's risk assessment process.

What is the DSIT definition of qualifying R&D?

The DSIT Guidelines 2023 define qualifying R&D as work that seeks to achieve an advance in overall knowledge or capability in a field of science or technology, and involves the resolution of scientific or technological uncertainty. The uncertainty must be one that a competent professional working in the field could not resolve without investigation. The guidelines replaced the previous BEIS Guidelines and are the document HMRC uses when assessing claims under s.1138 CTA 2010.

Can I fix mistakes in an R&D claim after it has been submitted?

Yes, in most cases. A company can submit an amended return to correct errors in a submitted R&D claim, provided the amendment is made within the statutory time limit (normally two years from the end of the accounting period). If HMRC has already opened a compliance check, any errors should be disclosed promptly, as voluntary disclosure is treated more favourably when calculating penalties than errors discovered by HMRC independently.

How does HMRC spot overclaimed staff costs in R&D claims?

HMRC cross-references the staff costs claimed in an R&D relief claim against PAYE records, company accounts, and the additional information submitted with the CT600. A director whose salary is £80,000 but who is claimed to spend 95% of their time on qualifying R&D, in a company with significant non-R&D turnover, will draw scrutiny. HMRC also looks at whether the qualifying percentages are consistent with the nature and scale of the business.

What evidence do I need to support an R&D tax credit claim?

The most important evidence is contemporaneous: records created at the time the R&D was being carried out. This includes project plans, technical meeting notes, test logs, version control records, internal technical reports, and email chains where technical problems and solutions were discussed. Evidence prepared retrospectively to support a claim is materially weaker and significantly harder to defend under enquiry.

Does including non-qualifying work in a claim always result in a penalty?

Not automatically. HMRC's penalty regime distinguishes between careless errors (which attract lower penalties, sometimes suspended) and deliberate or concealed behaviour (which attracts higher penalties of up to 100% of the tax). Where a company genuinely believed work qualified, took reasonable steps to assess this, and the error reflects a borderline judgment rather than wilful overclaiming, the penalty position is more favourable. The key is to demonstrate that the claim was prepared with reasonable care.

How to Protect Your Claim Before It Is Submitted

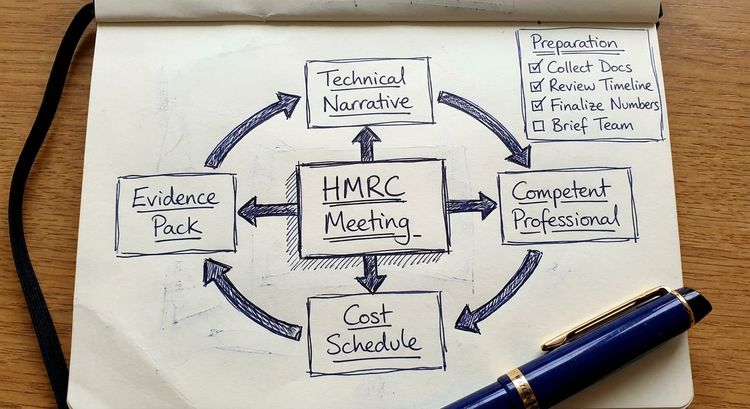

The most cost-effective time to address R&D tax credit claim mistakes is before the claim goes in. A pre-submission review by a specialist who understands both the technical and statutory requirements can identify the weaknesses that HMRC will focus on and address them while there is still time to do so.

At IP Tax Solutions, we work with companies and their accountants to review claims before submission, strengthen technical narratives, and ensure that qualifying costs are correctly identified and evidenced. If your claim is already under enquiry, we also provide R&D tax credit defence across all stages of the HMRC compliance process.

To discuss a review of your R&D claim, contact Steve Livingston directly via the contact page.