The EIS financial health requirement under s.180B ITA 2007 is one of the least understood conditions in the Enterprise Investment Scheme. If a company was "in difficulty" at the point its shares were issued, every investor who subscribed loses their 30% income tax relief. The condition is assessed at a single moment in time and cannot be cured retrospectively.

Table of Contents

- What is the EIS financial health requirement?

- What does "in difficulty" actually mean?

- When does the financial health test apply?

- What happens to investors if the requirement is breached?

- How does HMRC assess your balance sheet?

- Can you argue the position with HMRC?

- When should you take specialist advice?

- Frequently asked questions

What is the EIS financial health requirement?

The EIS financial health requirement is a statutory condition at s.180B ITA 2007. It requires the issuing company to be "not in difficulty" at the beginning of Period B, which is the date the shares are issued to investors.

It applies to every EIS share issue. The insolvency-based test (Test 1) applies to all companies at all times. In practice, however, Test 1 is rarely the concern for a company closing an EIS round in the normal way: the test is applied at the date of issue, at which point the subscription monies have been received as part of the same transaction. That cash injection is on the balance sheet at the relevant moment, and in most cases it is precisely what prevents the company from being insolvent. The residual risk from Test 1 arises only where a company is so deeply insolvent that even the EIS proceeds cannot cure it at the date of issue, or where there is a timing mismatch between shares being allotted and cash being received.

The accumulated losses test (Test 2) is the test that causes most problems in practice, and it only applies once a company has moved beyond its initial investing period: broadly, 7 years from first commercial sale for most companies, and 10 years for knowledge-intensive companies. Within that period, a company cannot fail on accumulated losses alone. A company that does fail either test cannot issue qualifying EIS shares on that date, and any EIS1 compliance statement filed in respect of that issue will be invalidated if HMRC later discovers the breach.

The requirement was inserted by Finance (No.3) Act 2010, Sch 2, para 1(4), and has applied to all shares issued on or after 6 April 2011. It reflects post-financial-crisis state aid rules designed to prevent public subsidy flowing to companies that should, in economic terms, be exiting the market rather than raising growth capital.

In my experience, this is the EIS condition most often overlooked in advance assurance applications and the one that creates the most serious problems when HMRC raises it years after investment.

What does "in difficulty" actually mean?

The phrase "in difficulty" is not defined in the primary legislation. Section 180B(3) ITA 2007 directs advisors and HMRC to the Community Guidelines on State Aid for Rescuing and Restructuring Firms in Difficulty (originally 2004/C 244/02 and now assessed against the 2014 Guidelines, 2014/C 249/01, as those had effect in the UK immediately before 31 December 2020). HMRC's internal manual at VCM13040 confirms these 2014 guidelines now govern the assessment.

In practice, HMRC applies a two-part test:

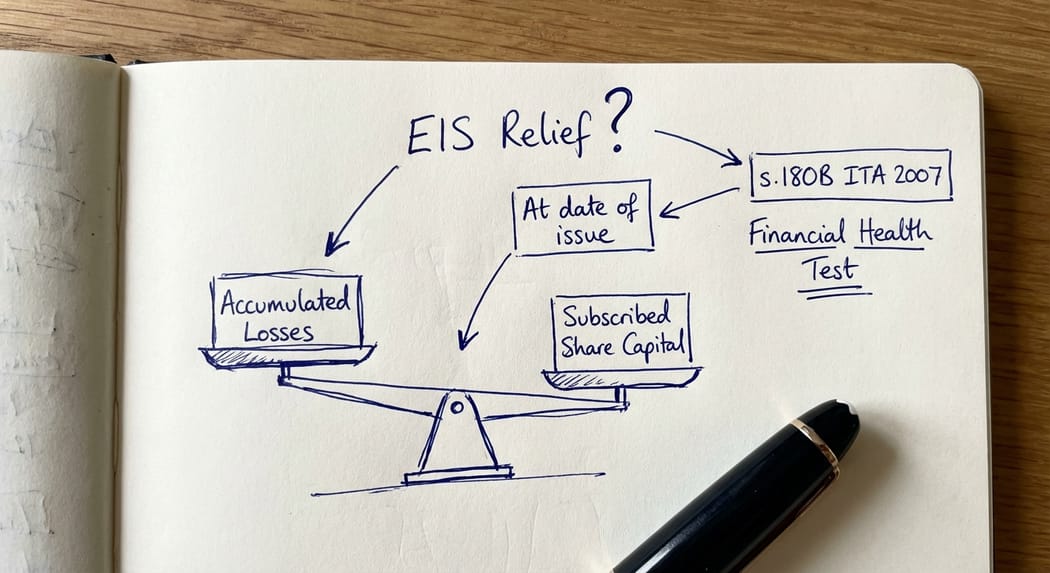

Test 1 (insolvency-based): A company is "in difficulty" if it meets the Insolvency Act 1986 standard: it is unable to pay its debts as they fall due, or its assets are less than its liabilities when contingent and prospective obligations are included.

Test 2 (loss accumulation): A company is also treated as being in difficulty if its accumulated losses exceed half of its subscribed share capital. For this purpose, "subscribed share capital" means the total amount subscribed by shareholders: nominal share capital and share premium combined, as shown in the company's accounts. The test fails when accumulated losses are more than 50% of that total. This test does not apply during the company's "initial investing period" as defined at s.175A ITA 2007: broadly, 7 years from the date of first commercial sale for most companies, and 10 years for knowledge-intensive companies. Within that period, HMRC can only challenge financial health on Test 1. Once a company moves beyond the initial investing period, Test 2 is also engaged.

The second test is where founders and advisors most commonly fall short. A company in its eighth or ninth year (outside the initial investing period), that raised £2 million across earlier rounds and has now accumulated £1.1 million in losses, fails Test 2: the losses exceed half of the total subscribed capital. The company is not insolvent. Its investors are not worried. But on the financial health test, it is "in difficulty."

When does the financial health test apply?

The test is applied at a single point in time: the beginning of Period B, which is the date the shares are issued (s.159 ITA 2007). It is not a continuing obligation. A company that fails the test on the date of issue cannot cure the defect by improving its balance sheet afterwards.

This creates a practical problem. EIS share issues rarely happen on a single day. In a funding round, shares may be issued on different dates to different investors. If the company's financial position changes materially between the first and last issue date, different tranches within the same round may be treated differently.

The timing issue also matters for advance assurance. HMRC grants advance assurance based on the company's position at the time of the application. Advance assurance is not binding if, by the time shares are actually issued, the company's financial position has deteriorated. A company that secured advance assurance six months before closing a round should reassess its balance sheet position at the date of issue, not rely on figures that may now be stale.

What happens to investors if the requirement is breached?

If HMRC determines that the financial health requirement was not met at the date of issue, the consequences are serious:

The financial health requirement is assessed as a snapshot at the date of each specific share issue. It is not a condition that reaches back and affects earlier investors. If a company issued EIS shares in a seed round three years ago and those shares were issued at a date when the financial health requirement was met, those investors are unaffected by a subsequent round where the test was failed. The question asked in every case is: was this company in difficulty at the date these specific shares were issued?

Only the investors who subscribed in the issue where the requirement was not met are at risk. Every investor in that share issue is in principle exposed to withdrawal of their 30% EIS income tax relief. Because the financial health requirement was not met at the date of that specific issue, those shares were never qualifying EIS shares and the relief was never validly obtained. Relief is withdrawn under the standard withdrawal provisions in Chapter 6 of Part 5 ITA 2007. HMRC raises a Special Assessment against each investor under s.235 ITA 2007, requiring repayment of the income tax relief originally claimed, together with interest running from the date of the original claim. HMRC's ability to do so is subject to enquiry time limits: four years from the end of the relevant tax year for innocent error, six years for careless conduct, and twenty years for deliberate conduct. Filing an EIS1 compliance statement in respect of a share issue that did not meet the financial health requirement is likely to be treated as at least careless, giving HMRC a six-year window at minimum. The three-year minimum holding period is a separate matter: it governs when an investor can dispose of their shares without losing relief for other reasons, and has no bearing on HMRC's right to withdraw relief on financial health grounds.

EIS capital gains deferral relief also falls away. If any investor had used the EIS shares to defer a capital gain, that gain crystallises.

SEIS-to-EIS conversion does not insulate against this. Companies that ran a SEIS round followed by an EIS round need to ensure the financial health requirement was met at the date the EIS shares were issued, not the SEIS shares.

The compliance statement (EIS1) that the company submitted to HMRC when issuing the EIS3 certificates to investors becomes misleading. Companies should be aware that making a compliance statement when conditions are not met creates its own risks under the disclosure and penalty regime.

In cases where HMRC raises this after several years, the amounts involved can be material. If a company raised £1 million in EIS shares and 10 investors each subscribed £100,000 (claiming £30,000 of tax relief each at the 30% EIS rate), the aggregate claw-back across all investors is £300,000 in income tax, plus interest from the date of the original claims.

Responding to an HMRC compliance check of this kind involves many of the same processes as responding to an HMRC compliance check on any other innovation tax matter: assembling contemporaneous evidence, engaging HMRC through formal correspondence, and building a technical case around the balance sheet position at the exact date of issue.

How does HMRC assess your balance sheet?

HMRC starts from the most recent filed accounts at the date of the share issue. This is typically the last statutory accounts on Companies House, which may be six to eighteen months old by the time a later funding round closes. HMRC will also consider management accounts if they are available.

HMRC's guidance at VCM13040 was updated in August 2023 to confirm a more flexible approach. The updated guidance makes clear that HMRC will consider reasonable adjustments to the accounts figures, reflecting the particular circumstances of the company at the date of the relevant share issue, provided those adjustments are consistent with UK GAAP. The filed accounts are therefore a starting point, not the final word.

The most commonly argued adjustment in practice is R&D capitalisation. Where R&D costs have been expensed through the profit and loss account but could properly have been capitalised as an intangible asset under UK GAAP, reconstructing the accounts on that basis reduces accumulated losses and may bring the company back within the threshold. Intercompany loans or balances that distort the net asset position of the issuing entity may also be adjusted.

Beyond the balance sheet figures themselves, the August 2023 update confirms that HMRC will look at a company's particular financial circumstances, including its ability to maintain its activity in the short or medium term. A company that is marginal on the numbers but can demonstrate it has the resources to continue trading has a stronger position than the raw figures might suggest. Evidence supporting this could include confirmed grant awards, binding co-investor commitments or a demonstrable revenue pipeline.

Key takeaway: HMRC's updated guidance gives more room to argue the position than a strict reading of the numbers might suggest. But the burden of proof sits with the company, and "we had a healthy cash position" is not the same as "we met the statutory test."

Can you argue the position with HMRC?

Yes, and in my experience, HMRC's initial position on financial health is often more aggressive than the eventual outcome once a detailed technical response is prepared.

I have successfully defended a company that was initially rejected for EIS advance assurance as it was outside its initial investment period and HMRC invoked the second test (accumulated losses - accumulated losses exceed half of its subscribed share capital). We resolved the issue by rebuilding the balance sheet for the R&D costs that had been expensed combined with more recent favourable management accounts.

The first step is to reconstruct the balance sheet position at the exact date of issue, not the date of the most recent accounts. This requires a careful review of all assets and liabilities, including:

- Cash held at the date of issue (verified from bank statements)

- Trade debtors, including accrued income that had been earned but not invoiced

- Trade creditors and accruals, including liabilities that had crystallised but not yet been invoiced

- Any material asset additions or disposals between the accounts date and the issue date

- Intercompany balances, and whether they were genuine liabilities or were subject to informal subordination arrangements

The second step is to consider what reasonable adjustments are available under HMRC's updated guidance at VCM13040 (updated August 2023). HMRC will consider any reasonable adjustment to the accounts figures reflecting the particular circumstances of the company at the date of issue, provided it is consistent with UK GAAP. The most frequently argued adjustment is R&D capitalisation: costs expensed through the profit and loss account that could properly have been capitalised under UK GAAP are treated as an asset rather than a charge against profits, reducing accumulated losses. The updated guidance also confirms that HMRC will look at the company's ability to maintain its activity in the short or medium term, which opens the door to a broader range of supporting evidence beyond the balance sheet numbers alone.

The third step is to engage with HMRC on the applicable guidelines, and in particular on whether Test 2 is properly in play at all. The state aid framework that underpins HMRC's approach at VCM13040 includes a carve-out for companies within their "initial investing period" as defined at s.175A ITA 2007: 7 years from first commercial sale for most companies, 10 years for knowledge-intensive companies. During that period, Test 2 does not apply; HMRC can only challenge financial health on the insolvency-based Test 1. A company that is loss-making but solvent, and that is within its initial investing period, cannot be treated as "in difficulty" on accumulated losses alone.

It is also worth noting that HMRC's approach to this condition has evolved. Early HMRC guidance indicated that a company's ability to attract investment from outside investors was itself evidence that it was not in financial difficulty. That approach was subsequently withdrawn. HMRC now applies the full framework set out in the 2014 Guidelines. The shift means that historic advance assurance letters issued under the earlier, more relaxed approach provide no protection if the same company's financial position is scrutinised under the current standard.

None of this is straightforward. HMRC case workers dealing with EIS compliance are generally experienced, and a poorly structured response can harden their position rather than open a negotiation. Cases that involve multiple investors, material amounts of relief, and disputed balance sheet positions benefit from specialist handling.

When should you take specialist advice?

Take advice before the share issue, not after. The financial health requirement is binary: either the company met it on the date of issue or it did not. If it did not, the only defence is either to argue that HMRC's technical analysis is wrong, or to seek a pragmatic settlement on the amount of relief at stake. Neither of these is a comfortable position.

Advisors should be reviewing their clients' balance sheets before signing off on an EIS1 compliance statement. If the company is outside its initial investing period and accumulated losses are approaching or have exceeded half of total subscribed capital (nominal share capital plus share premium), the financial health test must be worked through in full before, not after, the compliance statement is filed.

If HMRC has already opened a compliance check into an EIS issue and raised financial health as a concern, you need technical assistance before responding. HMRC's initial opening position in these cases often seeks to withdraw all relief. The final outcome, with specialist representation, is often more nuanced.

HMRC is increasingly active across all innovation tax reliefs. The approach it takes to HMRC enquiry defence cases in EIS mirrors the escalation seen in R&D enquiries over recent years, and the amounts of relief at stake in EIS cases can be just as significant.

If you are dealing with an HMRC challenge to EIS relief on financial health grounds, or you need a review of an upcoming EIS share issue before the compliance statement is filed, contact me for a no-obligation conversation.

Frequently asked questions

What is the EIS financial health requirement?

The EIS financial health requirement is a statutory condition at s.180B ITA 2007 requiring the issuing company to be "not in difficulty" at the date its shares are issued. A company is "in difficulty" if it meets the insolvency standard under the Insolvency Act 1986 (Test 1), or, for companies outside their initial investing period under s.175A ITA 2007 (broadly 7 years from first commercial sale), if accumulated losses exceed half of total subscribed share capital (meaning nominal share capital plus share premium combined) (Test 2). Both tests are assessed at the exact date the EIS shares are issued to investors.

Does the financial health requirement apply to SEIS as well as EIS?

The specific financial health requirement at s.180B ITA 2007 is an EIS condition only. SEIS is governed by Part 5A ITA 2007 and has different qualifying conditions. However, SEIS companies should be aware that the separate risk-to-capital condition (VCM8500) and the trading requirement both place restrictions on companies in financial distress.

My company is loss-making. Does that mean it fails the EIS financial health test?

Not automatically. A company within its initial investing period (broadly, 7 years from first commercial sale) cannot fail Test 2 at all. Even outside that period, the test only fails if accumulated losses exceed half of total subscribed share capital (nominal share capital plus share premium). A company that has raised £2 million in equity across its EIS rounds does not fail Test 2 until losses exceed £1 million. HMRC's guidance at VCM13040 (updated August 2023) also allows for reasonable adjustments to the accounts figures, reflecting the particular circumstances of the company at the date of issue, provided those adjustments are consistent with UK GAAP. R&D costs that were expensed but could have been capitalised under UK GAAP are the most commonly argued adjustment and can bring accumulated losses back below the threshold. The analysis requires a precise reconstruction of the balance sheet at the date the shares were issued, not the date of the most recent statutory accounts.

Can HMRC raise the financial health requirement years after the share issue?

Yes. HMRC can open a compliance check into an EIS issue at any time before the four-year enquiry window closes (or longer in cases involving incomplete disclosure). In practice, HMRC often identifies financial health concerns when reviewing an EIS Advance Assurance application, an EIS1 compliance statement or when a company enters administration after having issued EIS shares.

What is subscribed share capital for the purposes of the financial health test?

For Test 2, "subscribed share capital" means the total amount subscribed by shareholders: nominal share capital and share premium combined, as shown in the company's accounts. It is not limited to the nominal (par) value of shares.

This matters significantly in practice. Many EIS companies issue shares at a substantial premium to nominal value. A company that has issued 1,000,000 shares at a penny nominal value but at £1 per share has nominal share capital of £10,000 and share premium of £990,000. Its total subscribed share capital for Test 2 purposes is £1,000,000. The test fails when accumulated losses exceed £500,000, not when they exceed £5,000.

The threshold for Test 2 is therefore calibrated to the total equity raised, not the nominal share capital figure that appears on the face of the balance sheet. A company with significant accumulated losses but also significant equity raised across multiple rounds will need a careful calculation before any new EIS compliance statement is filed.

VCM13040 should be consulted for any live case involving a company that has reached the end of its initial investing period, given the potential for HMRC's published approach to be updated.

Does EIS advance assurance protect investors if the financial health requirement is later found to have been breached?

No. HMRC advance assurance is not a guarantee that EIS relief will be available. It confirms only that, on the information provided at the time of the application, HMRC has no reason to object to EIS eligibility. If the company's financial position deteriorates between the advance assurance application and the actual share issue, or if the balance sheet information in the application was incomplete, advance assurance provides no protection.

What happens to capital gains deferral if EIS relief is withdrawn on financial health grounds?

If EIS income tax relief is withdrawn because the financial health requirement was not met, EIS capital gains deferral relief under Schedule 5B TCGA 1992 also falls away. Any capital gain that was deferred by the original EIS investment becomes chargeable in the year the deferral relief is revoked.

Take specialist advice before the compliance statement is filed

The financial health requirement is not a box-ticking exercise. It requires a precise analysis of the company's balance sheet at a specific moment in time, and the burden of demonstrating compliance falls on the company, not on HMRC.

If you are advising a company that is about to issue EIS shares and there is any question about its accumulated losses relative to subscribed share capital, the time to address that question is before the shares are issued. After the issue, the options narrow considerably.

If HMRC has already raised concerns, a structured technical response is essential. I have represented clients through HMRC compliance checks across EIS, SEIS, R&D and Patent Box, and the financial health challenge is one where early, precise engagement with HMRC generally produces better outcomes than an extended correspondence battle.

To discuss a specific EIS financial health question, call me on 0161 961 0096 or email stevelivingston@iptaxsolutions.co.uk.

Steve Livingston LLB FCA is the founder of IP Tax Solutions Ltd, a specialist innovation tax advisory firm. Former KPMG and former tax partner at Crowe. 25 years in innovation tax advisory and HMRC dispute resolution.