The SEIS connected persons rules are one of the most frequently misunderstood areas in early-stage investment structuring. Most advisors know that SEIS carries significant tax relief for investors. Far fewer have a precise handle on which investors cannot claim that relief because of their relationship to the company, and the specific rules that determine when a stakeholder's associated shareholdings will disqualify a subscription altogether.

This article sets out the SEIS connected persons rules in full, explains how the 30% substantial interest test works in practice, and identifies the restructuring options available when a deal is at risk.

What Are the SEIS Connected Persons Rules?

The SEIS investor eligibility conditions are set out in Chapter 2 of Part 5A of ITA 2007 (ss.257B to 257BF). To qualify for SEIS income tax relief, an investor must satisfy five tests throughout the relevant period. Two of those tests amount to what practitioners commonly call the "connected persons" restrictions:

- The no-employee test (s.257BA ITA 2007): neither the investor nor any of their associates may be employed by the company unless they are also a director.

- The no substantial interest test (s.257BB ITA 2007): neither the investor nor any of their associates may hold, directly or indirectly, more than 30% of the company's ordinary share capital, voting power, rights on a winding up, or overall control.

The no-employee test applies throughout "period B" (the period from share issue to the third anniversary of share issue, as defined in s.257AC ITA 2007). The no-substantial-interest test applies throughout "period A" (the period from incorporation to the third anniversary of share issue). Both tests are tested at the date of share issue, but the no-substantial-interest test must continue to be met throughout period A, while the no-employee test must continue to be met throughout period B.

Breach of either test at the point of issue means no relief arises. Breach after the point of issue means any relief already given is withdrawn.

Who Counts as an Associate Under the SEIS Rules?

The definition of "associate" for SEIS purposes comes from s.257HJ ITA 2007, which cross-refers to s.253 ITA 2007 (the same definition used for EIS).

Associates include:

- The investor's spouse or civil partner

- The investor's parents and remoter ancestors (grandparents, great-grandparents)

- The investor's children and remoter issue (grandchildren, great-grandchildren)

- Business partners of the investor (e.g. LLP partner or a general partner)

- Trustees of a settlement where the investor is the settlor or a beneficiary

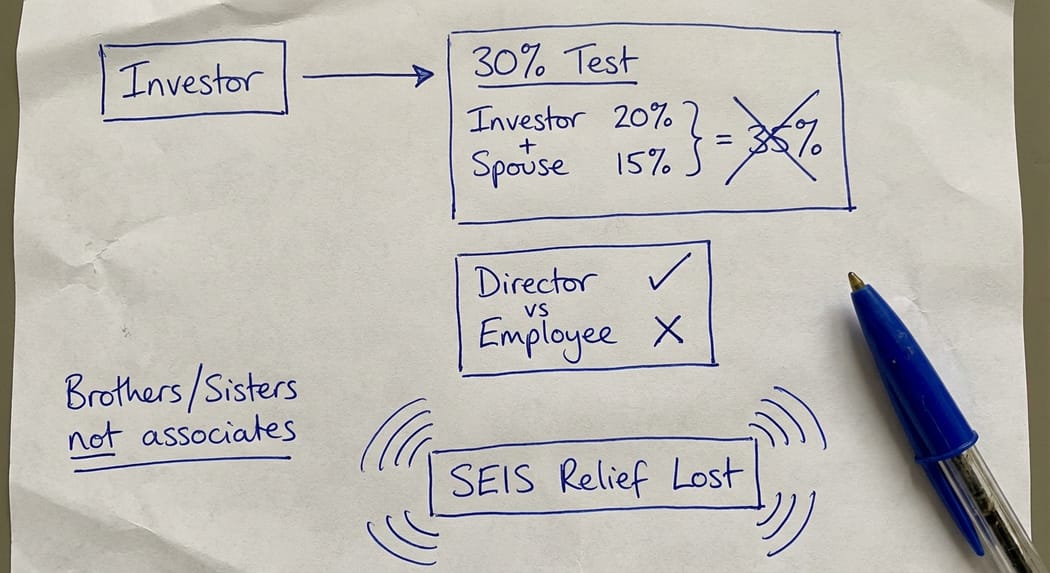

One exclusion that practitioners should know: brothers and sisters are not associates for SEIS (or EIS) purposes. This contrasts with some other tax provisions where siblings are included. A sibling's shareholding does not count toward the 30% test.

The associate aggregation rule operates in both directions. If the investor holds 20% and their spouse holds 15%, the combined holding of 35% takes the investor above the 30% threshold and SEIS relief is not available. It does not matter that the spouse is a separate legal person and subscribed for their shares independently.

The 30% Substantial Interest Test: Where Most SEIS Deals Fail

The test under s.257BB ITA 2007 is the one that causes the most practical problems. The full definition of "substantial interest" in s.257BF ITA 2007 covers any combination of:

- Ordinary or issued share capital

- Voting power

- Rights on a winding up

- Control of the company (per s.995 ITA 2007)

Associates' holdings are aggregated with the investor's own stake. The result is that a family member who received a nominal founder share allocation, or a spouse who holds shares acquired earlier in the company's history, can push an otherwise clean investor over the 30% threshold.

In practice, the trap most commonly arises in two scenarios.

The founder investor scenario. A founder who holds 40% of the company wants to invest alongside outside angels in a SEIS round. The founder would like the income tax relief and CGT exemption that SEIS offers. But the founder's 40% stake (note that this is beyond the stage of initial subscriber shares) means they cannot be a qualifying investor. The outside angels can qualify (subject to their own tests), but the founder cannot, regardless of the amount they invest.

The family stakeholder scenario. An external investor who is not a founder wants to participate in a SEIS round. They hold 15% of the company. Their spouse, who is not involved in the business but received shares at incorporation, holds 18%. Their combined stake is 33%. HMRC will not allow SEIS relief on the investor's subscription, and this will not be apparent unless someone maps out the cap table with associate holdings in mind.

The 30% test is applied to the investor's aggregate holding with associates, not to their individual stake. A clean-looking investor position can fail the test because of a spouse's or parent's shareholding that no one thought to check.

Can an Employee or Director Invest Under SEIS?

The answer depends entirely on the investor's role at the company.

Under s.257BA ITA 2007, an investor who is an employee of the company cannot claim SEIS relief. This applies during period B and includes employees of any qualifying subsidiary. It does not matter how small the employment or how minor the role.

The critical exception is that the employee restriction does not apply if the investor is also a director. A director who happens to receive a salary is not an employee for this purpose. This is a deliberate policy choice: SEIS was designed partly to allow founder-directors to participate in investment rounds alongside outside investors.

The VCM guidance at VCM32020 makes the director definition broad. It includes not only formally appointed directors but also:

- Anyone occupying a position that functions like a directorship, regardless of job title

- Persons whose directions the board habitually follows

- Managers or individuals involved in business management who, whether alone or with associates, own or control at least 20% of ordinary share capital

This last point is significant. A senior employee with a 20%+ stake may well be classified as a director under s.257HJ ITA 2007 (mirroring CTA10/s.452), even if they have no board appointment. That classification could mean they do satisfy the no-employee test. It could also mean their shareholding is relevant to other investors' 30% calculations.

For ordinary employees with no directorship and no meaningful stake, the position is clear: they cannot claim SEIS relief on a subscription made while employed. The solution, if they wish to invest, is to resign from employment before subscribing, or to take on a director appointment that brings them within the director exception.

How Do the SEIS Connected Persons Rules Differ from EIS?

The SEIS and EIS investor conditions are not the same, and treating them as interchangeable is a common source of error.

Under the EIS rules (s.168 ITA 2007), an investor is "connected" to the company if they are an employee, a partner, or a director who receives remuneration or a bonus. An unpaid director (a genuine non-executive director receiving no remuneration) is not connected under EIS.

The SEIS position is different. Under s.257BA ITA 2007, the restriction falls on employees, but a director (paid or unpaid) is expressly excluded. This means a paid founder-director CAN claim SEIS relief on their own subscription, subject to passing the 30% test. Under EIS, that same paid founder-director would be connected and would not qualify.

The 30% test under s.257BB ITA 2007 applies to both SEIS and EIS (for EIS, see the equivalent substantial interest restriction under s.170 ITA 2007). The definition of associates is also broadly similar across both schemes.

The practical consequence is that SEIS tends to be more accessible to founder-directors than EIS. The restriction that bites most frequently under SEIS is the 30% test, not the employee/director distinction.

What Happens When the SEIS Connected Persons Rules Are Breached?

If the investor fails either the no-employee test or the no-substantial-interest test at the date the shares are issued, no SEIS relief arises. The investor holds shares in the company but receives no income tax reduction and no CGT exemption under the SEIS regime.

If the investor qualifies at the date of issue but then breaches the 30% test during period A (for example, by acquiring additional shares that push their aggregate stake above 30%), relief already given is withdrawn in full. The investor faces an additional income tax assessment for the amount of relief originally received. Interest runs from the date of the original claim.

This is set out at VCM36010 and s.257FA ITA 2007.

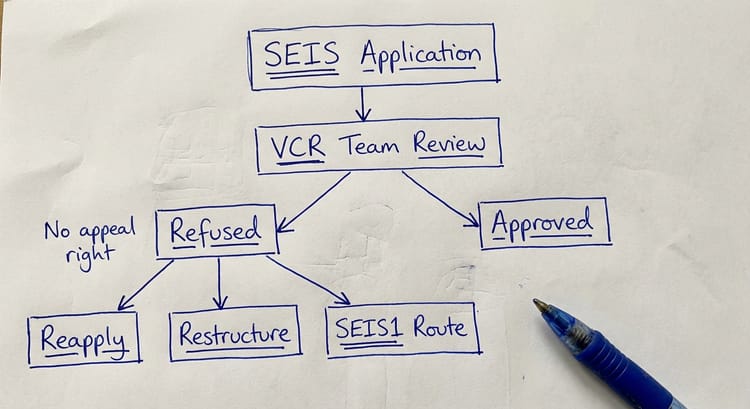

Where connected persons issues are identified at the advance assurance stage, HMRC will simply refuse to confirm eligibility. For more on what to do when HMRC refuses a SEIS advance assurance application and the options available to restructure.

How to Structure Around a Connected Persons Issue

Where a connected persons issue is identified before shares are issued, there are usually solutions. The right approach depends on which test is at risk.

If the investor is an employee only (no directorship): The investor needs to either resign from employment before the share issue date, or take on a director appointment before subscribing. The director appointment must be genuine and not simply a mechanism to circumvent the employee restriction. HMRC is aware of this structure and will scrutinise it if the appointment is immediately followed by a share subscription.

If a founder holds more than 30%: The founder cannot claim SEIS relief. This is not something that can be restructured around without either diluting the founder's stake or accepting that the founder's element of any subscription does not qualify. Outside investors in the same round can still qualify, provided they each satisfy the investor conditions individually.

In all cases, the time to identify and resolve connected persons issues is before shares are issued. Applying for SEIS advance assurance in advance of the round is the best mechanism for surfacing investor eligibility issues. HMRC's Venture Capital Reliefs (VCR) Team will flag concerns about company-level qualification, and while advance assurance does not formally cover individual investor eligibility, the discipline of preparing the application tends to surface cap table issues that would otherwise go unnoticed.

Frequently Asked Questions

What are the SEIS connected persons rules?

The SEIS connected persons rules are two investor eligibility conditions in Chapter 2 of Part 5A of ITA 2007. The first (s.257BA) prevents employees from claiming SEIS relief unless they are also directors. The second (s.257BB) prevents anyone from claiming relief if they, together with their associates, hold more than 30% of the company. Both tests must be met throughout the period following share issue.

Can a company director claim SEIS relief on their own investment?

Yes. Under s.257BA ITA 2007, a director is expressly excluded from the employee restriction. A paid founder-director can subscribe for SEIS shares and claim the income tax relief and CGT exemption, provided their aggregate holding with associates does not exceed 30%. This is one of the key differences between SEIS and EIS, where a paid director is treated as "connected" and therefore excluded.

What happens if an investor holds SEIS shares and then their stake rises above 30%?

If the investor's aggregate holding with associates rises above 30% during the three years following share issue, the SEIS relief already received is withdrawn in full (VCM36010, s.257FA ITA 2007). An additional income tax assessment is raised, and interest runs from the date of the original claim. This is a continuing obligation, not just a test at the point of subscription.

Do brothers and sisters count as associates for SEIS purposes?

No. The definition of "associate" under s.257HJ ITA 2007 (cross-referring to s.253) does not include brothers or sisters. A sibling's shareholding does not count toward the 30% threshold for any investor. This is a notable exception, and one that is sometimes overlooked by advisors who apply the rules less carefully than the legislation requires.

My SEIS advance assurance was refused because of connected persons issues. What should I do?

A refusal on this basis tells you that HMRC has identified an investor eligibility concern, usually relating to the 30% substantial interest test or the employee restriction. Before reapplying, the cap table needs to be reviewed carefully with associate holdings mapped in full. The solution may involve restructuring investor stakes, adjusting the timing of the investment, or, in some cases, accepting that certain investors in the round cannot claim SEIS relief. Getting specialist input before resubmitting is advisable, since HMRC limits correspondence to two rounds after an initial opinion (VCM60270).

How does HMRC know about connected persons issues?

HMRC's Venture Capital Reliefs (VCR) Team reviews advance assurance applications carefully, but it does not have access to the full cap table unless the applicant provides it. Connected persons issues often surface at the compliance statement stage (form SEIS1(VCS)), when HMRC processes investor certificates and cross-references the information provided. Where HMRC finds that a named investor does not meet the eligibility conditions, it will not issue a SEIS3 certificate to that investor, and any relief already claimed is at risk.

Can the connected persons rules be avoided by structuring the investment through a nominee?

No. The legislation operates by reference to the beneficial interest, not the registered holder. A nominee arrangement does not sever the investor's connection to the underlying shares. HMRC's guidance is clear that both direct and indirect holdings count toward the 30% threshold.

What to Do Next

The SEIS connected persons rules are not obscure. They are part of the investor eligibility framework in the primary legislation. But their practical application, particularly the aggregation of associates' stakes, catches experienced advisors more often than it should.

The cost of getting this wrong falls on investors, not advisors. An investor who subscribed in good faith, claimed the income tax relief, and then receives a withdrawal notice faces a recovery assessment on tax they have already spent. That outcome is avoidable if the cap table is reviewed properly before shares are issued.

I advise founders, accountants and corporate finance advisors on SEIS investor eligibility and connected persons structuring issues. If you are preparing a SEIS round and want the cap table reviewed for eligibility issues before shares are issued, or if you are dealing with an existing situation where HMRC has raised connected persons concerns, get in touch. You can also read more about Steve Livingston FCA and the SEIS and EIS work I handle.

For advice on what to do if connected persons issues have already caused HMRC to challenge a claim, see the broader context in HMRC enquiry defence.