When a company wants to incentivise a key person with equity, there are broadly two types of share option available in the UK: the Enterprise Management Incentive (EMI) option and the unapproved share option (sometimes called a non-qualifying option). Most people instinctively reach for EMI, and usually for good reason. But unapproved options have their place, and in some situations they are the only tool that fits. Choosing between EMI vs unapproved options UK advisers and founders face is rarely as simple as "EMI if you can, unapproved if you must."

This article sets out how each structure works, how they are taxed, and how to decide which is right for the person being incentivised and the company doing the incentivising.

What EMI Options Are and Why They Are So Valuable

An Enterprise Management Incentive option is a statutory share option that qualifies under Schedule 5 ITEPA 2003 and is notified to HMRC in accordance with Part 7 of that Schedule. Once the option qualifies, ss.527 to 541 ITEPA 2003 (the EMI code) apply.

The core tax advantage is found in s.530 ITEPA 2003. Where an EMI option is granted at no less than the market value of the shares at the date of grant, the exercise of that option is entirely free of income tax and National Insurance. The employee pays the agreed exercise price, acquires the shares, and any subsequent gain is taxed only when those shares are sold, as a capital gain.

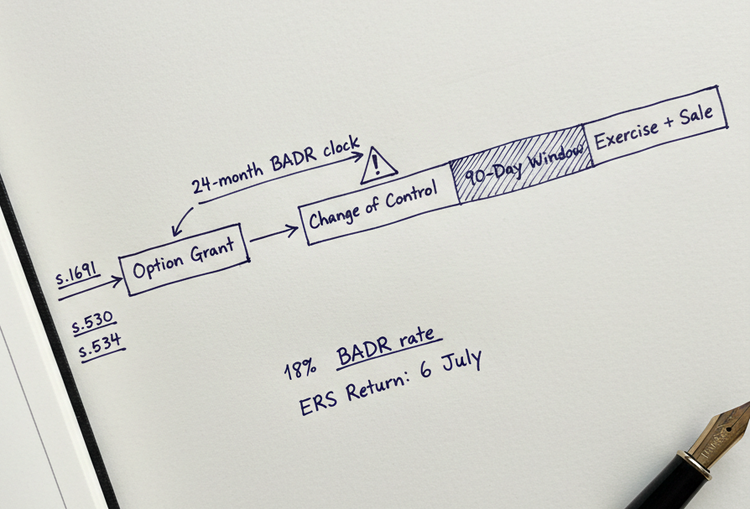

That capital gains treatment comes with a further advantage: Business Asset Disposal Relief (BADR). For qualifying EMI options, the two-year BADR holding period runs from the date the option was granted, not the date the shares were acquired on exercise. An employee who has held an EMI option for two years before a trade sale can, in principle, pay BADR rates on the entire gain, even if they only exercised the option minutes before completion. From 6 April 2026 the BADR rate is 18%, rising from 14%. Without BADR, the standard CGT rate on gains above the basic-rate band is 24%.

On the eligibility side, the Budget 2025 (Finance Act 2025-26) expanded the EMI thresholds significantly, with effect from 6 April 2026. The gross assets limit has increased from £30 million to £120 million, the full-time equivalent headcount limit from 250 to 500, the company-wide pool of unexercised options from £3 million to £6 million in Unrestricted Market Value (UMV), and the maximum option life from 10 to 15 years under s.529 ITEPA 2003. The individual limit of £250,000 UMV per employee is unchanged.

How Unapproved Options Are Taxed

An unapproved option (sometimes called a non-qualifying or non-tax-advantaged option) is simply a contractual right to acquire shares that does not meet, or has not been notified as meeting, the Schedule 5 ITEPA 2003 requirements. There is no statutory framework governing its terms, which is one of the reasons it can be useful.

The tax treatment is materially different from EMI. On exercise of an unapproved option, the spread between the exercise price and the market value of the shares at the date of exercise is treated as employment income under the Part 7 Chapter 5 ITEPA 2003 rules. That spread is charged to income tax (at up to 45%) and, depending on how the option is classified, may also attract employee and employer National Insurance.

After exercise, the employee acquires shares whose base cost for CGT purposes is the market value at the date of exercise (the value already taxed as income). Any further growth from that point to disposal is a capital gain. BADR may still be available, but only under the standard conditions: the employee must hold at least 5% of the ordinary share capital and voting rights, must have been an employee or officer of the company for the preceding two years, and must remain so at the date of disposal. The 5% threshold in particular rules out most employee-level holdings.

The income tax charge on unapproved option exercise can be substantial. On a £500,000 gain at the point of exercise, the difference between EMI and unapproved treatment is potentially £130,000 in income tax and NICs at higher-rate thresholds, before any BADR comparison.

The Section 431A Deeming Provision and When a Manual Election Still Matters

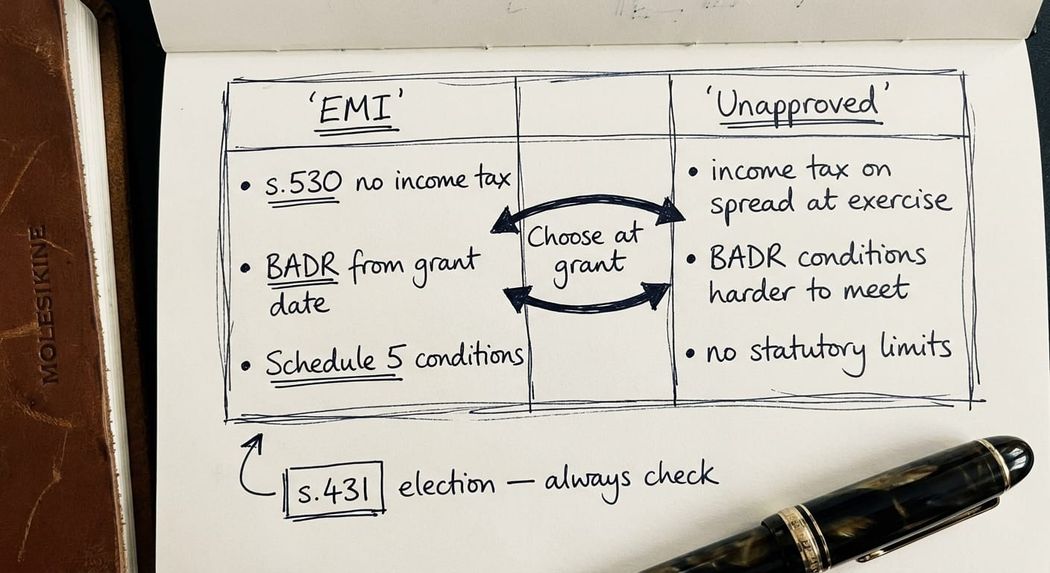

One point that trips up even experienced advisers is the interaction between s.431 ITEPA 2003 elections and EMI options. Under s.431A ITEPA 2003, where a qualifying EMI option is exercised and s.530 relief applies (that is, the exercise price was not less than market value at grant), the employer and employee are treated as having made a joint s.431(1) election. The shares are deemed to be acquired at their unrestricted market value, and the Chapter 2 restricted securities regime is switched off automatically.

In a standard, compliant EMI scheme this is sufficient. A manual s.431 election is technically redundant.

However, there are three situations where s.431A does not apply and a manual election, signed within 14 days of exercise, becomes essential:

Discounted EMI options. Where the exercise price is below market value at grant, s.530 does not apply (relief falls instead under s.531 ITEPA 2003). s.431A is therefore not triggered. Without a manual election, the shares are restricted securities and any post-exercise growth in value above the restricted market value is charged to income tax, not CGT.

Exercise more than 90 days after a disqualifying event. A disqualifying event includes a change of control or the employee dropping below the 25-hour working threshold. If the option is exercised outside the 90-day window, s.530 protection is compromised and the s.431A deemed election is unreliable. A manual election is required.

Failed EMI scheme. Late notification (now the 6 July deadline following the tax year of grant, under FA 2024 s.13, not the old 92-day rule), defective option terms, or independence failures mean the option is treated as unapproved from the outset. At that point, s.431A has no application. If the employee did not sign a manual election within 14 days of exercise and the shares are restricted, the entire post-exercise gain is exposed to income tax as each restriction lifts.

For unapproved options, s.431A does not apply at all. Where the shares being acquired are restricted (which in practice they almost always are in a private company), a manual s.431 election is not optional. It is the mechanism by which future growth is secured as capital gain rather than employment income.

When EMI Is Clearly the Right Choice

EMI is right when:

The employee works at least 25 hours a week for the company (or, if less, at least 75% of their working time). Part-time employees can qualify, but the committed working time test in Schedule 5 paragraph 26 ITEPA 2003 must be satisfied.

The company qualifies. Excluded activities under Schedule 5 paragraph 16 ITEPA 2003 (within the trading activities requirement in Schedule 5 paragraph 13) rule out property development, financial activities, providing legal or accountancy services, farming, and certain other trades. As of 6 April 2026 the company must have no more than 500 full-time equivalent employees and gross assets not exceeding £120 million.

The value of options to be granted to the individual does not breach the £250,000 UMV cap. For senior hires in well-funded companies, this cap is tight and can be reached quickly.

The option terms are fixed and certain. EMI requires the option to specify a number of shares and an exercise price at the date of grant. Formulaic or percentage-based grants do not qualify.

The two-year BADR benefit from grant date is commercially important. For a business heading toward a trade sale within two to five years, the ability to run the BADR clock from grant, not from exercise, is a significant planning advantage.

When Unapproved Options Are the Right (or Only) Tool

Advisers, consultants, and non-executive directors. A person who is not an employee or director of the company (in the HMRC sense) cannot hold an EMI option. Unapproved options for external contributors are taxed as trading income at exercise, not employment income, with VAT implications if the advisor is VAT-registered. The planning is different, but the vehicle is unapproved.

Where the EMI individual limit is breached. A grant worth more than £250,000 UMV cannot be made under EMI. The excess portion must be an unapproved option. This is common in senior hires at well-funded scale-ups where even the post-Budget £6 million company pool is generous but the per-person cap remains the binding constraint.

Where the company does not qualify. Financial services, property, legal, and accountancy businesses cannot grant EMI options. Unapproved options are the only equity incentive vehicle available.

Where option terms need flexibility. EMI requires specific conditions on exercise conditions and prohibits options with wide discretionary triggers. Unapproved options can be structured with more bespoke terms, including performance-linked conditions that would invalidate EMI status.

Where the company is under group control. If the company is a subsidiary under the control of another corporate entity, it cannot grant EMI options to its employees. Unapproved options remain available.

BADR Comparison: The Numbers That Matter

From 6 April 2026 the tax differential between a well-structured EMI exit and an unapproved option exit looks like this, on a £500,000 gain:

EMI option, granted at market value, two-year BADR clock satisfied: £90,000 in CGT (18% BADR rate).

Unapproved option, spread of £500,000 arises at exercise as income: £225,000 in income tax at 45% (higher rate). No CGT on the exercised gain. Further growth taxed as CGT at 24% (or 18% BADR if the 5% test is met, which is unlikely for most employees).

Even where the employee qualifies for BADR on their unapproved options (a high bar), the BADR rate of 18% applies only to the post-exercise capital gain. The exercise gain itself has already been charged to income tax.

The difference on a £500,000 exercise gain alone is £135,000. This is why the choice of vehicle matters and why retrofitting a company's option scheme after the fact, when the company is close to exit, rarely closes that gap.

The Hybrid Structure: EMI Plus Unapproved

In practice, many companies grant both. A senior hire receives a £250,000 UMV EMI option (the statutory maximum) and a further unapproved option for the excess. The EMI element carries the s.430 tax advantages and the BADR from grant. The unapproved element is treated as income at exercise, with a s.431 election signed to protect the post-exercise gain from restricted securities charges.

This is a workable structure but it requires careful documentation. The option agreement must make clear which shares are subject to the qualifying EMI option and which are unapproved. The BADR analysis on the unapproved element needs to be considered at grant, not at the exit, because the 5% shareholding test applies to the total holding, not just the unapproved tranche.

Reliefs Interaction: EMI and SEIS or EIS in the Same Company

Where a company has SEIS or EIS advance assurance, the interaction with the EMI scheme requires careful sequencing. A company that has issued qualifying SEIS or EIS shares can still grant EMI options to its employees. The two reliefs are not mutually exclusive. The independence condition for EMI (Schedule 5 paragraph 9 ITEPA 2003) prohibits control by another company, but institutional SEIS and EIS investors do not take control positions, so the independence condition is generally satisfied.

The issue arises if an existing EMI option holder takes a SEIS or EIS subscription in their own name. For EIS, the investor conditions under s.163 ITA 2007 (the no-connection requirement) prohibit a director of the issuing company from claiming EIS relief. For SEIS, the investor conditions under ss.257BA to 257BE ITA 2007 are structured differently: directors are specifically excluded from the no-employee-investors restriction by s.257BA(2) ITA 2007, but the no-substantial-interest condition in s.257BB ITA 2007 will catch any investor whose combined shareholding and options give rise to a substantial interest in the company. This is a sequencing and structuring question, not a binary incompatibility.

FAQ

What is the main tax difference between EMI and unapproved share options?

EMI options granted at market value are exercised free of income tax and NIC under s.530 ITEPA 2003. The gain from grant to disposal is taxed as a capital gain, potentially at 18% BADR rate where the two-year EMI condition is satisfied. Unapproved options create an income tax charge at exercise on the spread between the exercise price and the market value of the shares at that date, at rates of up to 45%, with NICs also potentially in point.

Can an external adviser or NED receive an EMI option?

No. EMI options can only be granted to employees and directors who satisfy the committed working time test in Schedule 5 paragraph 26 ITEPA 2003. External advisers and non-executive directors who are not employees cannot hold qualifying EMI options. Unapproved options are the appropriate vehicle for non-employees, though the tax treatment is materially different.

Do I still need a s.431 election if I have an EMI option?

In a standard EMI scheme where the option is granted at market value and exercised without any disqualifying event issues, s.431A ITEPA 2003 creates a statutory deemed election. A manual election is technically redundant. However, for discounted options, options exercised late after a disqualifying event, or where there is any risk the scheme has failed, a manual s.431 election within 14 days of exercise remains essential. For unapproved options, s.431A does not apply and a manual election is always required where the shares are restricted securities.

What are the EMI eligibility thresholds after Budget 2025?

From 6 April 2026, the company must have no more than 500 full-time equivalent employees (increased from 250) and gross assets not exceeding £120 million (increased from £30 million). The company-wide pool of unexercised options is now £6 million in UMV (increased from £3 million). The individual cap of £250,000 UMV per employee is unchanged. The maximum option life is now 15 years under s.529 ITEPA 2003 (increased from 10 years).

When does BADR apply to EMI option shares?

For qualifying EMI options, the two-year BADR qualifying period runs from the date the option is granted, not the date the shares are acquired on exercise. This is a significant advantage over unapproved options, where the standard BADR conditions apply: the employee must hold at least 5% of ordinary share capital and voting rights and must have been an employee or officer for the preceding two years. The BADR rate from 6 April 2026 is 18%.

What happens to an EMI option if the scheme fails?

If the option fails to qualify (for example, through late notification past the 6 July deadline, defective option terms, or an independence failure), it is treated as an unapproved option. If the employee has exercised believing the EMI protection applied and did not sign a manual s.431 election, they may face income tax on future growth in value as restrictions lift, in addition to income tax on the exercise spread. This is one of the most serious compliance risks in EMI scheme administration.

Can EMI and unapproved options exist in the same scheme?

Yes. Where the value of shares to be granted to an individual exceeds the £250,000 UMV EMI cap, the excess is typically structured as an unapproved option alongside the qualifying EMI tranche. The two elements carry different tax treatment and must be clearly documented. A s.431 election for the unapproved tranche is essential where the shares are restricted.

Getting the Structure Right

The choice between EMI and unapproved options shapes the entire tax outcome for the person being incentivised. Making that choice at grant, rather than at exit, is what determines whether a £500,000 gain is taxed at 18% or 45%.

If you are reviewing an option scheme, considering a senior hire, or working with a client who has mixed EMI and unapproved option grants, talk to us before the exercise date, not after. We work directly with founders, finance directors, and the accountants who advise them on option scheme design, HMRC valuation negotiations, and compliance across the equity lifecycle.