Most software and SaaS founders raising under SEIS or EIS assume the schemes are tech-friendly. They are. But the rules were drafted before SaaS existed in its modern form, and the structuring decisions that look obvious to a software founder are often the same decisions that get advance assurance refused or (worse) surface in a compliance check three years after the cash has been spent.

This guide sets out the SEIS and EIS questions that matter for UK software and SaaS companies in 2026. It is written for founders, CFOs, finance leads and accountants asking whether a particular round qualifies, what to put in the advance assurance application, and where the structuring traps are.

Are software and SaaS companies eligible for SEIS and EIS?

Yes. There is nothing in s.181 ITA 2007 (the trading requirement) or s.192 (excluded activities) that excludes software development or software-as-a-service businesses as a sector. Software trades are mainstream qualifying trades for both Seed Enterprise Investment Scheme and Enterprise Investment Scheme purposes.

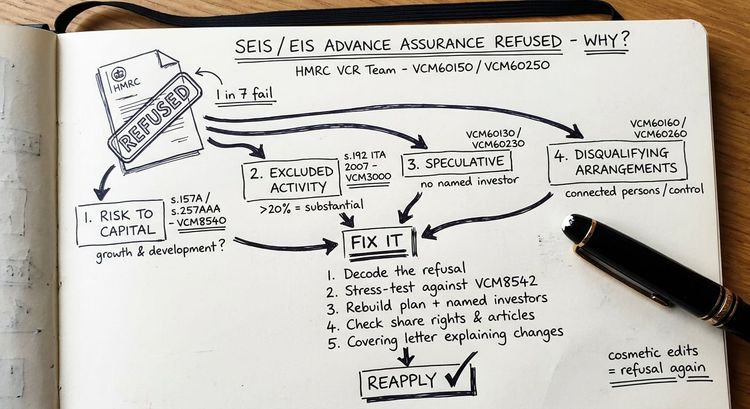

That said, eligibility depends on satisfying every condition in the legislation, and software companies present specific risk areas: how revenue is characterised, where IP is created and held and whether the risk-to-capital condition in s.157A (EIS) or s.257AAA (SEIS) ITA 2007 is genuinely satisfied. Each of these is a live point in HMRC's current Advance Assurance practice.

The trading requirement and excluded activities

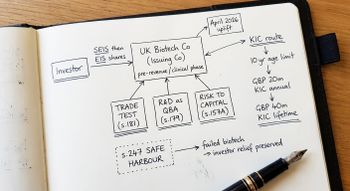

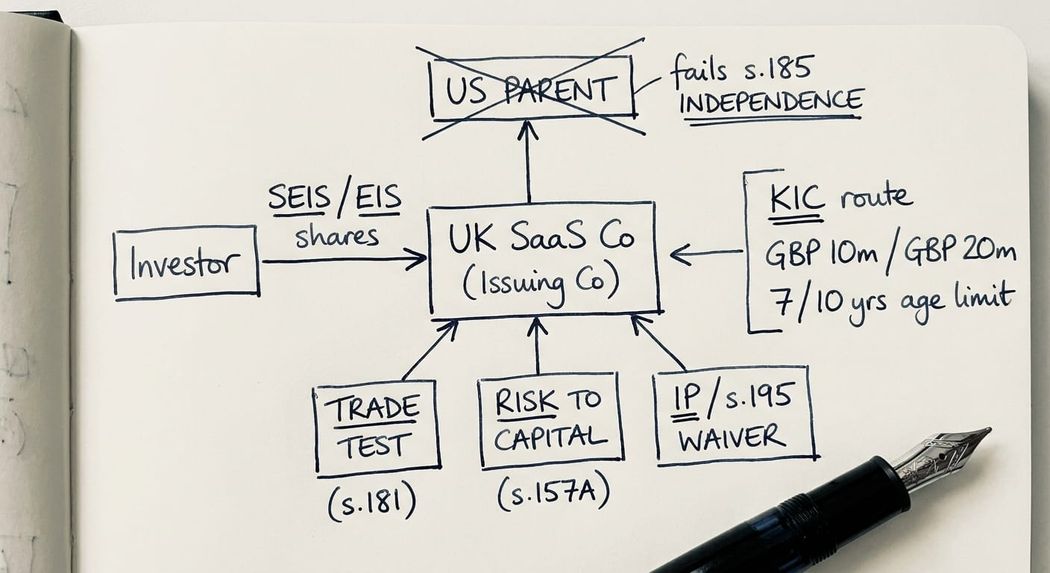

The issuing company must exist wholly, or substantially wholly, for the purpose of carrying on one or more qualifying trades (s.181). A trade is a qualifying trade unless it consists wholly, or substantially, of one of the activities excluded by s.192(1). For software and SaaS, three of the listed exclusions sit close to the line:

Receiving royalties or licence fees (s.192(1)(e)). This is the most-misread exclusion. On a literal reading, a software company licensing software for a fee would fail. The waiver in s.195 ITA 2007 fixes that for most genuine software businesses. The waiver removes the exclusion where the royalties or licence fees are attributable to the exploitation of "relevant intangible assets," meaning intangible assets where the issuing company (or a qualifying subsidiary throughout the creation period) created the whole or the greater part by value. So a UK SaaS company that built its own platform clears the test. A UK company that licenses-in IP from a foreign group, purchases / repackages it, and licenses it on does not.

Other financial activities (s.192(1)(c)). FinTech businesses sit closest to this exclusion. The HMRC manual at VCM3040 distinguishes regulated lending and underwriting (excluded) from regulated advisory and intermediary activity (not excluded). A SaaS platform that operates as a payments processor or a credit risk intermediary has to evidence which side of the line it sits on, and Financial Conduct Authority status is not a clean proxy.

Dealing in goods other than ordinary wholesale or retail distribution (s.192(1)(b)). This rarely catches pure SaaS. It can catch software companies that bundle hardware, where the hardware element is significant.

The 20% test in VCM3010 is the practical anchor: if excluded activities make up no more than 20% of turnover or capital employed (whichever is more reasonable on the facts), HMRC will normally accept they are not a "substantial part" of the trade.

The risk-to-capital condition for SaaS companies

The risk-to-capital condition in s.157A (EIS) and s.257AAA (SEIS), introduced by Finance Act 2018, requires two things at the date of share issue:

- the company must have objectives to grow and develop its trade over the long term, and

- the investment must carry significant risk of capital loss greater than the net return.

SaaS companies tend to look low-risk to HMRC's reviewing officers in the Venture Capital Reliefs (VCR) team because of three features that recur:

- Contracted recurring revenue: Annual recurring revenue, multi-year enterprise contracts, and high net retention all read as "secured income" on a first read. They are not automatically disqualifying. VCM8542 is explicit that securing future income does not by itself indicate capital preservation. The point matters when recurring revenue is large relative to the raise and the use of funds story does not show genuine reinvestment in product, hiring, and market expansion.

- Light-touch economics: SaaS businesses that outsource development work, have low employees head count (current and projected) and/or appear more 'life-style' oriented will attract scrutiny from HMRC. Aim to be a "full-fat" company with a growing headcount, brand and ambition.

- Capital efficiency at the seed stage: SaaS companies often raise small SEIS rounds against modest valuations and break even fast. That is a commercial strength but a SEIS challenge: the smaller the round and the closer the company is to break-even, the harder it is to argue investor capital is genuinely at risk.

The way to clear the condition is to write the application as if HMRC has read the file before. Show the growth plan, the milestones the cash unlocks, the headcount and revenue trajectory, and the specific commercial risks (technical, market, competitive, regulatory) that could cause investor capital to be lost. The risk-to-capital condition is where most software-company refusals are now decided.

Knowledge-intensive company status: when it matters

A knowledge-intensive company (KIC) is defined in s.252A ITA 2007. KIC status raises the EIS company age limit from 7 to 10 years from first commercial sale, raises the EIS annual investment limit (now £20 million from April 2026, against £10 million for non-KICs), raises the lifetime limit (£40 million against £24 million), and raises the gross employees cap from 250 to 500.

A software company qualifies as a knowledge-intensive company by satisfying two cumulative limbs.

- The operating costs limb requires R&D or innovation spend of at least 15% of operating costs in one of the last three years, or at least 10% in each of the last three years.

- The second limb is met by satisfying either the innovation condition or the skilled employees condition. The innovation condition (s.252A(5)) requires the company to be engaged in creating relevant IP, with that IP (or business resulting from it) reasonably expected to form the greater part of the company's business within ten years. The skilled employees condition (s.252A(8)) requires at least 20% of the FTE workforce to hold a relevant higher education qualification (postgraduate Master’s degree or PhD (equivalent to NVQ Level 7 or above) directly related to the R&D being carried out) and to be engaged directly in R&D or innovation throughout the three years from share issue.

For most UK SaaS companies with active engineering teams, the IP creation condition is met by default. The operating cost test is then the practical question. SaaS founders should run that calculation before assuming KIC status, and document it in the advance assurance file.

Permitted maximum age, pivots, and the SaaS playbook

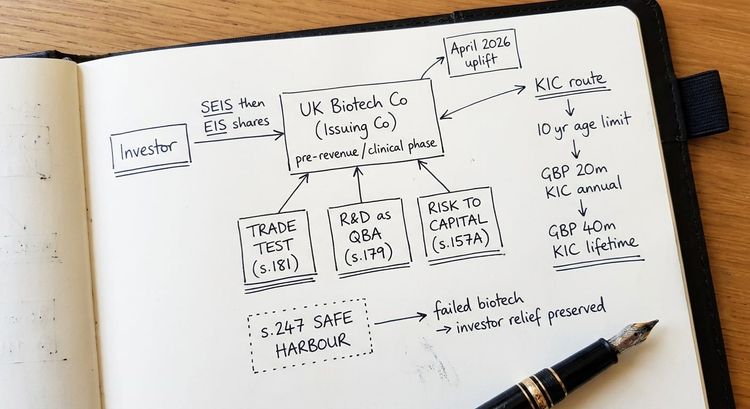

For EIS, the shares must have been issued within seven years of the company's first commercial sale (ten years for KICs), unless the round is a permitted growth investment satisfying s.175A. For SEIS, the trade must be "new" in the sense that no person has carried it on for more than three years before the share issue (s.257HF). Software companies hit two specific points here.

- Pivots: A SaaS company that ran a consumer freemium product for two years and then pivoted into a B2B enterprise SKU is normally treated as carrying on a continuing trade for SEIS purposes if the underlying technology, customer base, or trading apparatus is materially shared. HMRC's view on what counts as a "new trade" is fact-driven and conservative. The defensible position is to document the pivot at the time, evidence the discontinuation of the old trade, and accept that for SEIS the safer route is often to incorporate a new vehicle rather than pivot the existing one (subject to phoenix and TAAR analysis).

- Open-source contributions and prior platforms: Founders often have prior commercial activity through previous companies or sole-trade work. If the same trade was carried on by a different person more than three years before the SEIS issue, SEIS is barred. EIS may still be available, but the seven-year clock runs from the first commercial sale of the trade by any person.

Where SEIS/EIS, R&D and HMRC enquiry risk overlap

Software companies are the single sector most likely to face concurrent challenges across SEIS/EIS, R&D tax credits, and corporation tax compliance. We see three patterns.

- R&D claims that lean on the same software development costs that the SEIS/EIS use-of-funds narrative is selling as growth investment.

- SEIS/EIS investors connecting on directorship terms that breach the connected persons rules in s.166 to s.171.

- And SaaS companies receiving an HMRC enquiry into R&D and answering it in a way that prejudices the SEIS/EIS position. The strategic point is that the documentation is shared. If the R&D narrative says staff time was spent on Project X, the SEIS/EIS file needs to be consistent with that. We have written separately on responding to an HMRC R&D tax credit enquiry letter, and on specialist HMRC enquiry defence where multiple workstreams are open.

The April 2026 changes that affect software fundraising

The April 2026 EIS changes raise the relevant ceilings: annual EIS investment to £10 million (£20 million for KICs), lifetime EIS investment to £24 million (£40 million for KICs), and the gross assets test to £30 million pre-issue and £35 million post-issue. The practical effect for software companies is that growth-stage SaaS businesses that were drifting out of EIS territory are pulled back in, particularly if they qualify as knowledge-intensive. Existing EIS pipelines should be re-modelled against the new caps before the next round is structured.

The single most useful preparation step before submitting an Advance Assurance application for a software or SaaS company is to write the use-of-funds narrative as if HMRC's reviewing officer is sceptical about risk to capital. Every other technical point is easier to land than that one.

Frequently asked questions

Can a SaaS company qualify for SEIS or EIS?

Yes. There is no sector exclusion for SaaS or software businesses. Eligibility depends on the company satisfying the trading requirement, the excluded activities tests, the risk-to-capital condition, the permitted maximum age requirement, and the financial health and independence tests. The risk-to-capital condition is where most software-sector refusals occur in current practice.

Does SaaS recurring revenue breach the risk-to-capital condition?

Not by itself. VCM8542 is explicit that securing future income does not automatically indicate capital preservation. The condition asks whether the investment carries a significant risk of capital loss and whether the company has long-term growth objectives. SaaS recurring revenue must be considered in the context of the use of funds, the growth plan, and the commercial risks that could cause the business to fail.

Are SaaS subscription fees treated as licence fees under s.192(1)(e)?

In most cases, no. SaaS revenue is typically a service supply, not a licence fee. Where contracts are structured as software licences (for example, perpetual or term licences for on-premise software), the s.195 waiver normally protects the position because the issuing company has created the IP. The waiver is the practical line for software companies, and it requires the issuing company (or a qualifying subsidiary throughout the creation period) to have created the whole or greater part of the IP by value.

Does a software company qualify as knowledge-intensive?

Most active software development companies meet the IP creation condition by default. The operating cost test (15% R&D in one of the last three years and 10% in each, or 10% in each of the last three) is the practical question for KIC status. Founders should run the calculation before assuming KIC eligibility and document it in the advance assurance file.

What use-of-funds detail does HMRC want to see for a SaaS round?

Specifics, not categories. Engineering hire numbers and seniority, sales and marketing headcount and channels, infrastructure investment, market entry plan with milestones, and a clear link between the cash and the growth trajectory. "Working capital" as a line item invites a follow-up question on risk to capital.

Does the April 2026 EIS limit increase apply to existing pipelines?

Yes, for shares issued on or after the relevant commencement date. Companies with an active EIS pipeline should re-model the round against the new caps, particularly where KIC status is available, since the lifetime and annual limits are doubled.

What to do next

If you are preparing an Advance Assurance application for a software or SaaS company, the file needs to be built around three points: a clean trade and excluded-activities analysis, a use-of-funds narrative that satisfies the risk-to-capital condition, and an IP and group-structure review that establishes the s.195 waiver and the independence test. We work with software founders and their accountants on advance assurance applications, on Compliance Statement (form SEIS1 / EIS1) preparation, and on enquiry defence where HMRC raises a question after the round has closed. The earlier the structuring review happens in the round, the lower the risk of an avoidable refusal.

The above article covers highly technical and complex tax law and does not constitute professional advice.