Yes. A company can use SEIS, EIS and EMI in the same company at the same time, because the investor reliefs and the employee option scheme reward different people.

The real work is in the sequencing: grant EMI options before a priced funding round to fix a low exercise price, and keep one clean class of ordinary shares so the investor reliefs are not tainted.

On this page

- Can you run all three in one company?

- How the eligibility gates interact

- Keep one clean class of ordinary shares

- Sequencing the EMI grant around your funding round

- Getting the order right across the company's life

- Two traps that catch founders

- A worked example

- Frequently asked questions

Can you run all three in one company?

SEIS, EIS and EMI are not mutually exclusive, and most growing UK companies I advise end up using at least two of them. SEIS and EIS are investor reliefs. They reward (typically) external individuals who subscribe cash for new shares and take genuine risk with that money. EMI is an employee share option scheme. It rewards the people who work in the business by letting them acquire shares later, usually at a price fixed today.

Because the reliefs benefit different groups, there is no statutory bar on one company running SEIS, EIS and EMI together. The scheme rules sit in different places. The investor reliefs are in Part 5 and Part 5A of the Income Tax Act 2007. EMI lives in Schedule 5 to the Income Tax (Earnings and Pensions) Act 2003. They were designed to work in the same early-stage companies, and in practice they routinely do.

The risk is not whether you can combine them. It is whether you combine them in the right order, with the right share rights, at the right valuations. Get that wrong and you can taint the investors' relief or hand your team a higher exercise price than they needed to pay.

How the eligibility gates interact

Each scheme has its own qualifying gates, and the good news is that they broadly point the same way. A company that qualifies for SEIS or EIS will almost always clear the EMI company conditions, because the EMI gates are massive following the April 2026 updates, allowing companies with up to £120m in gross assets and 500 employees to qualify, far exceeding the venture capital scheme gates.

SEIS is the tightest test. The company must have gross assets of no more than £350,000 immediately before the share issue, fewer than 25 full-time equivalent employees, and a qualifying trade that started no more than three years earlier (s.257HF ITA 2007). Total SEIS raised is capped at £250,000, with 50% income tax relief for investors. EIS is wider: broadly £30m of gross assets (£35m post investment) since 6 April 2026, fewer than 250 employees, and a seven-year age limit from first commercial sale, with 30% income tax relief.

EMI's company conditions include a £250,000 limit on the value of options any one employee can hold (paragraph 5, Schedule 5 ITEPA 2003). The practical point for sequencing is simple. If you have built the cap table to satisfy SEIS and then EIS, you have already done much of the hard part for EMI. The SEIS and EIS advisory work I do almost always front-loads these gates so that the EMI grant later is straightforward.

Keep one clean class of ordinary shares

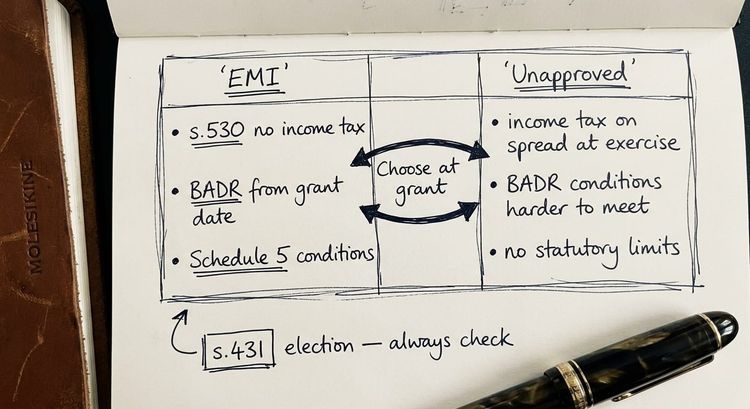

This is where combined structures most often go wrong. SEIS shares must be ordinary, non-redeemable, fully paid in cash, and carry no preferential right to dividends or to assets on a winding up (s.257CA ITA 2007). EIS shares must similarly be full-risk ordinary shares with no preferential rights and no pre-arranged exit (s.173 and s.177 ITA 2007). EMI options must be granted over shares that are ordinary, fully paid and non-redeemable (paragraph 35, Schedule 5 ITEPA 2003).

The cleanest combined structure grants the EMI options over the same ordinary share class the SEIS and EIS investors hold, or over a parallel ordinary class with identical economic rights. The danger comes when a company bolts on growth shares or a separate class with a hurdle or a liquidation preference for management, and the drafting of that waterfall accidentally gives the ordinary shares a preferential position.

A staged liquidation waterfall that pays ordinary shareholders before growth shareholders can create exactly the preferential right that disqualifies the investors' shares from EIS. It mirrors the preferential right HMRC successfully challenged in Flix Innovations Ltd v HMRC, the leading case confirming that any preferential right, however small, disqualifies the shares from EIS. If you are running investor reliefs and an option scheme in one company, the articles have to be read through the SEIS and EIS lens before anyone subscribes.

Sequencing the EMI grant around your funding round

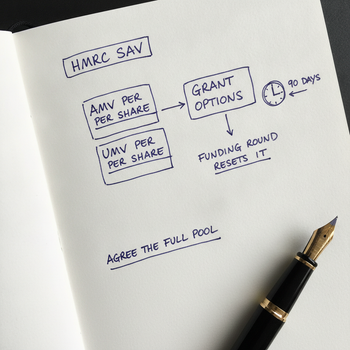

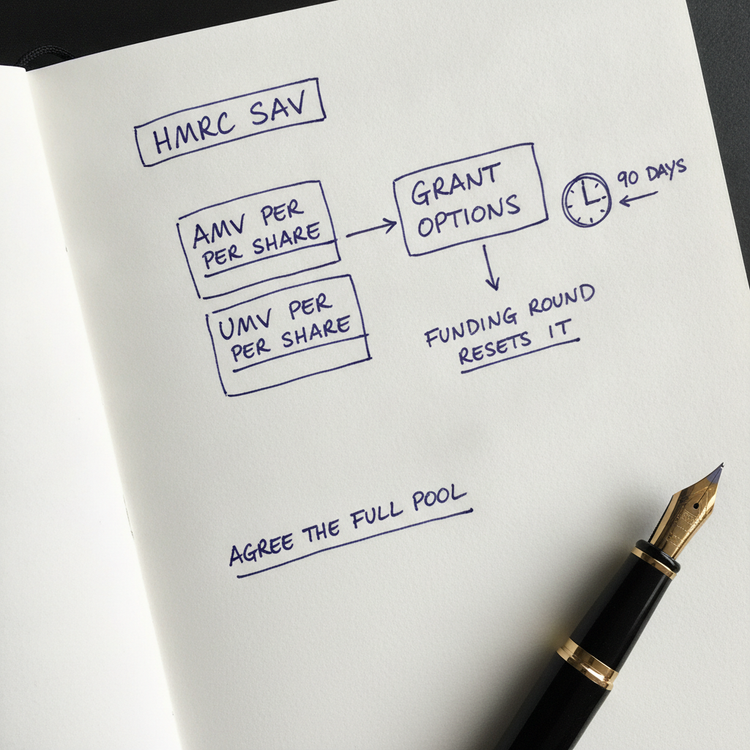

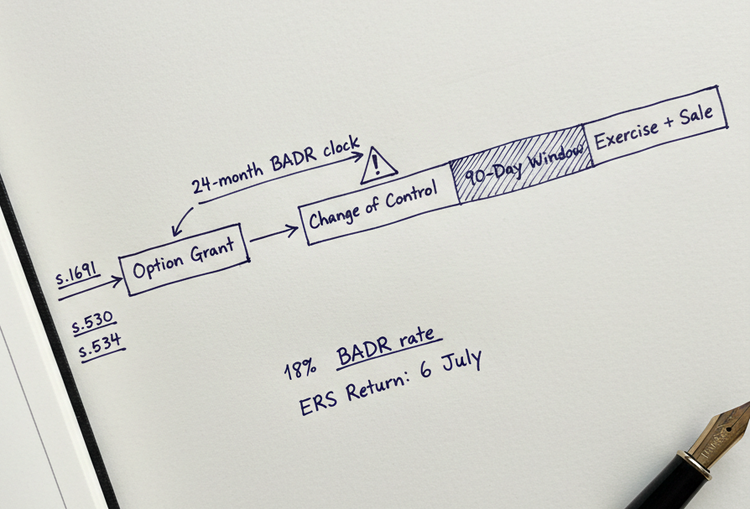

This is the heart of the question, and the part that costs real money if it is mishandled. An EMI grant needs an agreed market value. You submit an actual market value and an unrestricted market value to HMRC Shares and Assets Valuation, and the figure they agree is the market value against which you typically set the exercise price your employees will pay (paragraph 55, Schedule 5 ITEPA 2003).

A priced SEIS or EIS round sets an arm's length price per share. Once that round closes, HMRC will treat the round price as a strong reference point for the value of the ordinary shares. So the order matters. Grant the EMI options, and ideally agree the valuation, before a priced round is in active negotiation. That fixes a lower exercise price for your team while the company is still early. Wait until after a priced EIS round closes and the agreed value rises, which raises the cost for employees to exercise and shrinks their upside.

Key takeaway: The single biggest lever when you combine SEIS, EIS and EMI in the same company is timing the EMI valuation. Get the option grant and the HMRC valuation done before the priced round, not after, and your team locks in a lower exercise price.

There is a limit to this. You cannot ignore a round that is already agreed. If a term sheet is signed and the raise is imminent, HMRC will expect the EMI valuation to reflect it. The window to grant at a genuinely lower value is before the round is on the table, not the day before completion.

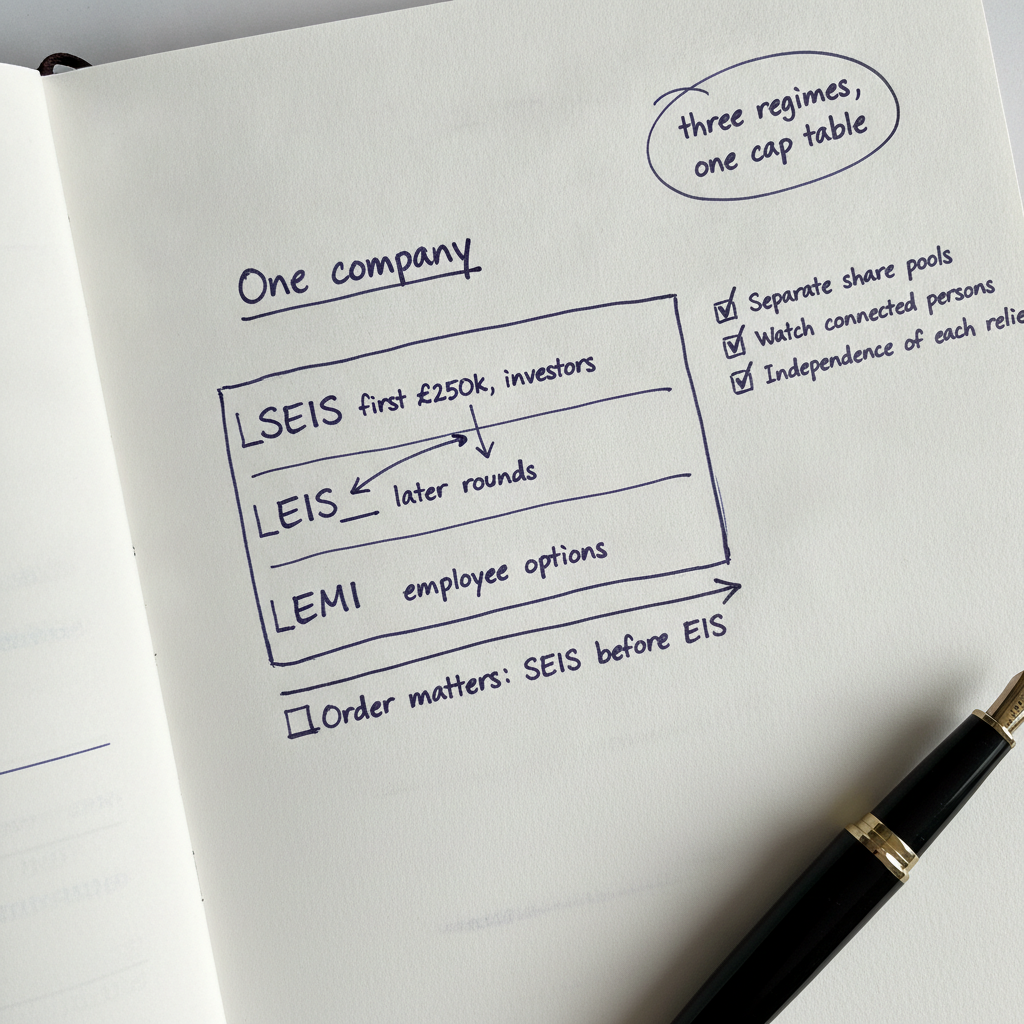

Getting the order right across the company's life

There is a fixed rule that governs the whole sequence: SEIS money must come before any EIS or VCT money. A single pound of EIS investment received before the SEIS shares are issued permanently disqualifies the company from SEIS. So the SEIS round always comes first, then EIS rounds follow.

EMI sits alongside this and does not consume the SEIS or EIS investment limits, because those limits are about money raised for shares, not options granted. A typical order for a founder company looks like this.

- Incorporate and issue subscriber ordinary shares.

- Grant early EMI options while the value is genuinely low, subject to the founder material interest point below.

- Raise the SEIS round.

- Raise EIS rounds.

- Make later EMI grants priced off the most recent round.

The reliefs do not compete for the same allowance, so layering them is about timing and clean paperwork rather than trade-offs, with the valuation interaction above the one point I plan around deliberately.

Two traps that catch founders

- The 30% material interest rule. A founder-director who holds more than 30% of the ordinary share capital cannot be an eligible EMI employee (paragraph 28, Schedule 5 ITEPA 2003), and cannot claim SEIS or EIS relief as an investor either, because the same 30% substantial interest test applies on the investor side (s.257BF ITA 2007 for SEIS, s.170 ITA 2007 for EIS). So a majority founder gets neither relief. Senior hires below 30% can take EMI, and outside investors below 30% can take SEIS or EIS. Usefully, unexercised EMI options do not count toward the 30% material interest test until they are exercised (paragraph 30, Schedule 5 ITEPA 2003), so granting options does not itself tip an employee over the line.

- The receipt of value rules during the investors' three-year holding period. If the company buys back shares within that window, for example from an employee who leaves after exercising EMI options, that can be a receipt of value that reduces or withdraws SEIS or EIS relief for the affected investors (s.257FE ITA 2007 for SEIS, s.213 ITA 2007 for EIS). Leaver buy-backs are common in option schemes, so this collision is easy to miss. Where a leaver needs to be bought out inside the three years, I look at parking the shares or deferring the buy-back rather than letting the company repurchase and quietly damage the investors' relief.

Frequently asked questions

Can you have SEIS, EIS and EMI in the same company?

Yes. There is no rule preventing SEIS, EIS and EMI in the same company. SEIS and EIS reward outside investors who subscribe cash for shares, while EMI rewards employees with share options. The schemes were designed to operate in the same early-stage companies, and the only real constraint is sequencing them correctly.

Should I grant EMI options before or after a funding round?

Grant EMI options before a priced SEIS or EIS round wherever you can. A priced round sets a market value that HMRC will use as a reference point, so granting beforehand fixes a lower exercise price for your team. Once a round is agreed and imminent, the EMI valuation has to reflect it, so the chance to lock in a lower value is gone.

Does an EMI scheme affect SEIS or EIS relief for investors?

Not by itself. EMI options do not use up the SEIS or EIS investment limits, because those limits apply to money raised for shares rather than options granted. The risk to investor relief comes from share buy-backs during the three-year holding period and from preferential share rights, not from the existence of the option scheme.

Can a founder get both EMI and SEIS or EIS relief?

A founder who holds more than 30% of the ordinary share capital can get neither, because the same 30% material interest test bars them from EMI and from claiming SEIS or EIS as an investor. Founders below 30% may qualify for EMI as employees / directors. Outside investors below 30% may qualify for SEIS or EIS.

Do SEIS, EIS and EMI shares all have to be ordinary shares?

In effect, yes. SEIS and EIS shares must be ordinary, full-risk shares with no preferential rights, and EMI options must be over ordinary, fully paid, non-redeemable shares. The cleanest combined structure uses one class of ordinary shares for both the investors and the EMI options, so a separate growth share class does not accidentally create a preference that disqualifies the investor relief.

Which comes first, SEIS or EIS?

SEIS always comes first. If a company receives any EIS or VCT investment before it issues SEIS shares, it is permanently disqualified from SEIS. So the order is SEIS round first, then EIS rounds, with EMI grants layered in around the timing of each priced round.

Getting the sequence right

Combining SEIS, EIS and EMI in one company is not difficult in principle, because the reliefs reward different people and do not compete for the same allowance. What separates a clean structure from an expensive one is the order of events: SEIS before EIS, one clean class of ordinary shares, and the EMI valuation agreed before a priced round rather than after it. Miss the sequencing and you either taint the investors' relief or hand your team a higher exercise price than they should have paid.

If you are setting up an EMI scheme alongside a SEIS or EIS raise, or you are worried a planned buy-back or a growth share class might damage relief that is already in place, get in touch. we will look at the cap table, the articles and the timing together, and tell you the order to do things in.

Schema markup (JSON-LD) for Ghost page-level code injection, not the body

{

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "Can you have SEIS, EIS and EMI in the same company?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Yes. There is no rule preventing SEIS, EIS and EMI in the same company. SEIS and EIS reward outside investors who subscribe cash for shares, while EMI rewards employees with share options. The schemes were designed to operate in the same early-stage companies, and the only real constraint is sequencing them correctly."

}

},

{

"@type": "Question",

"name": "Should I grant EMI options before or after a funding round?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Grant EMI options before a priced SEIS or EIS round wherever you can. A priced round sets a market value that HMRC will use as a reference point, so granting beforehand fixes a lower exercise price for your team. Once a round is agreed and imminent, the EMI valuation has to reflect it, so the chance to lock in a lower value is gone."

}

},

{

"@type": "Question",

"name": "Does an EMI scheme affect SEIS or EIS relief for investors?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Not by itself. EMI options do not use up the SEIS or EIS investment limits, because those limits apply to money raised for shares rather than options granted. The risk to investor relief comes from share buy-backs during the three-year holding period and from preferential share rights, not from the existence of the option scheme."

}

},

{

"@type": "Question",

"name": "Can a founder get both EMI and SEIS or EIS relief?",

"acceptedAnswer": {

"@type": "Answer",

"text": "A founder who holds more than 30% of the ordinary share capital can get neither, because the same 30% material interest test bars them from EMI and from claiming SEIS or EIS as an investor. Founders below 30% may qualify for EMI as employees. Outside investors below 30% may qualify for SEIS or EIS."

}

},

{

"@type": "Question",

"name": "Do SEIS, EIS and EMI shares all have to be ordinary shares?",

"acceptedAnswer": {

"@type": "Answer",

"text": "In effect, yes. SEIS and EIS shares must be ordinary, full-risk shares with no preferential rights, and EMI options must be over ordinary, fully paid, non-redeemable shares. The cleanest combined structure uses one class of ordinary shares for both the investors and the EMI options, so a separate growth share class does not accidentally create a preference that disqualifies the investor relief."

}

},

{

"@type": "Question",

"name": "Which comes first, SEIS or EIS?",

"acceptedAnswer": {

"@type": "Answer",

"text": "SEIS always comes first. If a company receives any EIS or VCT investment before it issues SEIS shares, it is permanently disqualified from SEIS. So the order is SEIS round first, then EIS rounds, with EMI grants layered in around the timing of each priced round."

}

}

]

}

The technical points covered in this post are complex, and this should not be interpreted as professional advice. Please reach out for technical assistance specific to your needs.