Most founders assume that giving shares in the family company to a son or daughter is a simple act of generosity with no tax cost. It is not. Transferring shares to your children is a disposal at market value for Capital Gains Tax, it can trigger an income tax charge under the employment-related securities rules, and it interacts with Business Asset Disposal Relief in ways that change which route is cheapest. Get the sequence right and the tax can be deferred in full. Get it wrong and your child can face an income tax bill on shares they paid nothing for.

This article sets out the three regimes that bite on a family share gift, in the order they need to be considered:

- CGT disposal and s.165 holdover relief,

- ERS family relationship exception, and

- BADR question of whether to defer the gain at all.

Why gifting shares is a disposal at market value

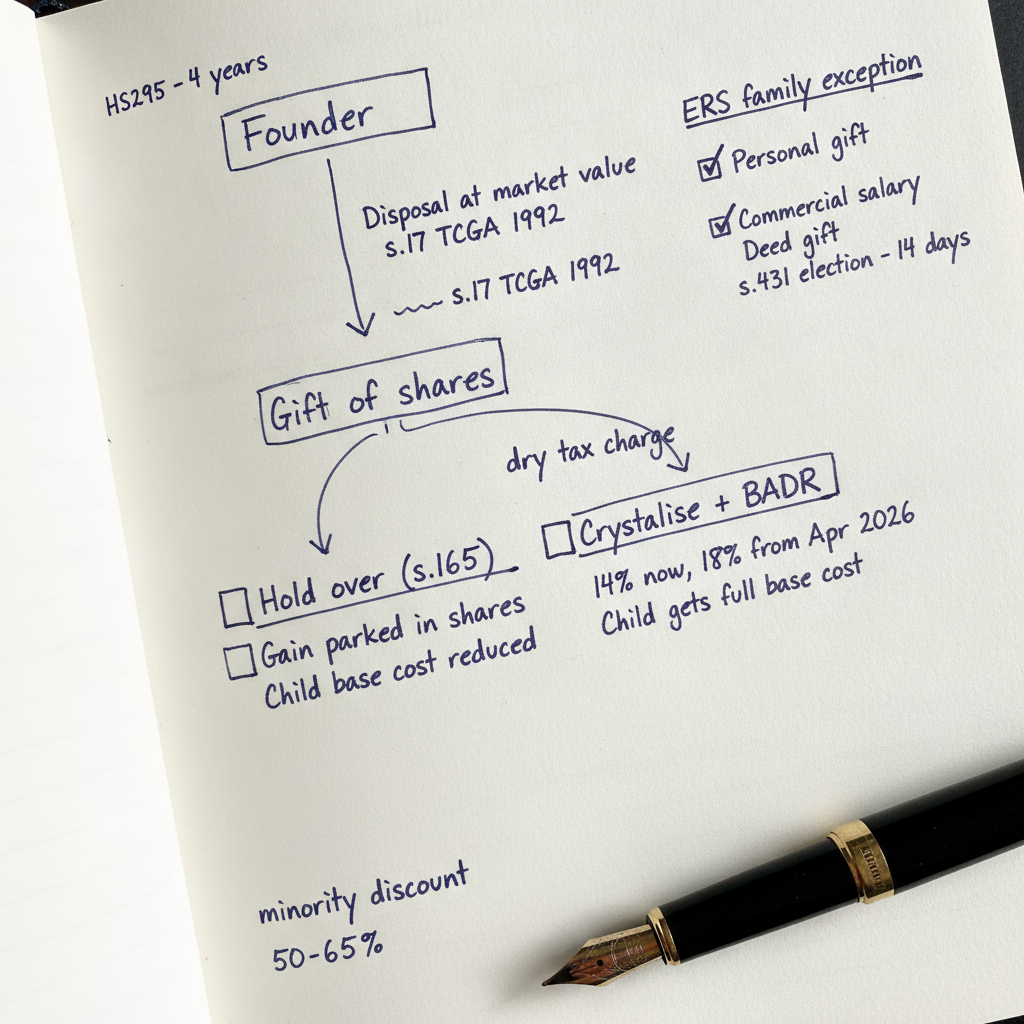

When you give shares to a connected person, you and your child are connected under s.286 TCGA 1992, so the transfer is treated as a disposal at open market value under s.17 TCGA 1992. The fact that no money changes hands is irrelevant.

The gain is calculated as if you had sold the shares for what a hypothetical willing buyer would pay, less your original base cost.

For a founder who subscribed for shares at par and built a profitable company, that gain can be substantial. Capital Gains Tax on shares is now charged at 18% for any part of the gain falling within the basic rate band and 24% above it, following the increases that took effect in late 2024. Without a relief, transferring shares to your children produces a "dry" tax charge: a real CGT liability with no cash proceeds to pay it. That is the problem s.165 is designed to solve.

Section 165 holdover relief: deferring the dry tax charge

Gift Hold-over Relief under s.165 TCGA 1992 allows the gain on a gift of qualifying business assets to be deferred. Shares in a personal trading company qualify, so a gift of shares in your own trading company to your child is within scope of the relief.

The mechanism is a deferral, not an exemption. On a joint election by you (the donor) and your child (the donee), the held-over gain is deducted from your child's base cost. You pay no CGT now. Your child inherits a lower acquisition cost, so the deferred gain crystallises when they eventually sell to a third party.

In effect the gain is 'frozen' inside the shares and carried forward to the next disposal.

Two practical points matter here:

- the company must be a trading company or the holding company of a trading group throughout. If it holds significant investment assets, holdover can be restricted under Sch 7 TCGA 1992.

- Statement of Practice 8/92 allows the claim to proceed without an agreed valuation, provided both parties accept that market value exceeds allowable cost. That said, for any sizeable transfer we recommend a robust valuation, because the same figure underpins the inheritance tax position and any future HMRC challenge.

The claim is made on form HS295, signed jointly, and must be filed within four years of the end of the tax year of the gift.

The ERS trap: when a gift to your child is taxed as employment income

This is the part many advisors miss: if your child works in the business, the transfer falls within the employment-related securities regime in Part 7 ITEPA 2003. The deeming provision in s.421B(3) ITEPA 2003 treats shares made available by an employer, or by a person connected with an employer, as acquired "by reason of employment". On that reading, the difference between market value and what your child pays (£nil, on a gift) could be taxed as general earnings under s.62 ITEPA 2003, with income tax and National Insurance at rates up to 45% plus.

The escape is the exception for opportunities made available "in the normal course of domestic, family or personal relationships". HMRC's guidance at ERSM20220 takes a common-sense view and gives the express example of a father handing shares to his children on retirement, even where the children are employees. So the family gift is usually outside the income tax charge. The exception is a question of fact though, and it can be lost. To keep the gift on the family side of the line:

- Make the gift personally, from you as an individual, rather than having the company issue fresh shares. HMRC is stricter where the company procures the acquisition.

- Pay your child a commercial salary for their actual role. An abnormally low salary lets HMRC argue the shares are a remuneration top-up.

- Keep the gift within the family. Simultaneous gifts to non-family employees weaken the personal relationship motive.

- Document intent. A formal deed of gift referencing the family relationship and your intention to provide for your child independently of their job is strong evidence.

Even where you are confident the exception applies, a protective s.431 election is usually worth signing and retaining personally within 14 days of the acquisition. It fixes the tax position on the unrestricted market value at the date of the gift, so that if HMRC later challenges the family characterisation, there is no further charge on subsequent growth. There is also an ERS reporting dimension: a reportable event normally has to go on the company's ERS annual return, filed online by 6 July following the end of the tax year.

Business Asset Disposal Relief: when crystallising beats holding over

Holdover is not always the right answer. Business Asset Disposal Relief (formerly 'Entrepreneur's Relief') charges qualifying gains at a reduced rate, and that rate has been climbing. BADR was 10% until 5 April 2025, 14% for 2025-26, and has risen to 18% from 6 April 2026, against a lifetime limit that remains at £1 million. As the BADR rate converges with the main 24% rate, the long-term value of the relief shrinks.

That creates a genuine planning choice when transferring shares to your children. If you hold over the gain under s.165, you defer the CGT but your child takes a reduced base cost and may not qualify for BADR on their own eventual sale. If instead you crystallise the gain now, claim BADR at 18% in 2026-27 and use part of your £1 million lifetime limit, you pay tax today but at a historically low rate, and your child takes a full market value base cost. For a founder approaching exit, deliberately crystallising a gain at 18% before April 2027, rather than holding it over into an uncertain future rate, can be the cheaper outcome over the life of the shares. The decision turns on the size of the gain, your remaining BADR allowance, and how soon your child is likely to sell.

Key takeaway: holdover relief and BADR pull in opposite directions. Holdover defers tax but strips your child's base cost and BADR access; crystallising now locks in today's low BADR rate. The right answer depends on the numbers, not the default.

Valuation, minority discounts and timing

The market value at the date of the gift drives every one of these calculations, so the valuation is not an afterthought. HMRC's Shares and Assets Valuation team typically uses a maintainable earnings approach for trading companies, weighting recent years. A recent weak trading year therefore suppresses the valuation, which reduces both the held-over gain and any inheritance tax exposure on the gift.

Gifting a minority stake rather than the whole holding also matters. A minority interest carries no control over dividends or strategy, so a discount of 50% to 65% on the pro-rata value is common for a 20% holding. Transferring shares to your children in tranches, each a minority interest, can move significant equity at a fraction of the headline value. None of this works without a defensible valuation file, and the cap table at Companies House must reconcile to the register of members before any transfer is documented.

The deadlines and elections you must not miss

Four filing points govern a clean family share transfer.

- The s.165 holdover claim goes on form HS295, signed by both parties, within four years of the end of the tax year of the gift.

- A protective s.431 election must be made within 14 days of the acquisition and cannot be made late. It is kept on file and not filed anywhere.

- The ERS annual return, reporting the event, is due online by 6 July after the tax year end.

- If the gift is a potentially exempt transfer for inheritance tax, the seven-year clock starts on the date of the gift, so the date should be recorded precisely.

Frequently asked questions

Do I pay capital gains tax when I gift shares to my children?

Yes, in principle. A gift to a connected person is a disposal at market value under s.17 TCGA 1992, so a chargeable gain arises even though no money changes hands. You can defer the gain by claiming s.165 holdover relief jointly with your child, or you can choose to crystallise it and claim Business Asset Disposal Relief.

How does s.165 holdover relief work on a gift of shares to children?

Holdover relief defers the gain rather than eliminating it. On a joint election, the gain is deducted from your child's base cost, so you pay no CGT now and the deferred gain crystallises when your child later sells. The shares must be in a trading company, and the claim is made on form HS295 within four years of the end of the tax year.

Will my child pay income tax on shares I give them?

Possibly, if they work in the business. The employment-related securities rules in Part 7 ITEPA 2003 can treat the gift as employment income. The family relationship exception at ERSM20220 usually takes a genuine family gift outside the income tax charge, but it must be supported by a commercial salary, a personal gift from you rather than a company issue, and a deed of gift.

Should I file a s.431 election when transferring shares to my children?

In most cases yes, but only as a protective measure. It should not be necessary if HMRC accepts the family gift ERS exemption; however, if HMRC challenges the treatment then a s.431 election could be crucial. A s.431 election fixes the tax charge on the unrestricted market value at the date of acquisition, so any later HMRC challenge cannot reach the subsequent growth in value. It must be signed within 14 days of the acquisition. It is not filed anywhere and should be retained personally and can be produced as evidence if and when necessary.

Is it better to hold over the gain or claim BADR when gifting shares?

It depends on the numbers. Holdover defers the CGT but reduces your child's base cost and may cost them Business Asset Disposal Relief later. Crystallising now lets you claim BADR at 18% in 2025-27 and gives your child a full base cost. For a founder near exit, locking in the lower BADR rate can be cheaper over the life of the shares.

How are the shares valued for a gift to my children?

At open market value on the date of the gift. HMRC generally applies a maintainable earnings basis for trading companies, and a minority holding attracts a discount of 50% to 65% for lack of control. A weak recent trading year suppresses the valuation, which reduces both the CGT gain and the inheritance tax exposure.

Where this leaves you

Succession tax planning involving transferring shares to your children is rarely the no-cost gift it appears to be. The CGT disposal, the ERS deeming provision and the BADR rate change all bite at the same moment, and the cheapest outcome depends on doing them in the right order with the right paperwork. We advise founders and the accounting firms who refer them on exactly this sequencing: when to hold over, when to crystallise, how to protect the ERS position, and how to evidence the valuation. If you are planning a family share transfer, speak to us before you sign anything, or ask your accountant to bring us in through our adviser referral route.