Pre-revenue biotech is the sector SEIS and EIS were designed for. It is also the sector where the rules pinch hardest. Long timelines to first sale, high gross-asset draws, mixed funding rounds and a real prospect of failure all push at the edges of the legislation. Get the structure right and your investors keep their tax reliefs through to a successful exit. If the science does not work, they salvage their position through statutory loss relief. Get it wrong and you blow up the cap table.

Contents

- Why SEIS and EIS matter more for biotech than any other sector

- The trade test problem: when R&D rescues a pre-revenue biotech

- Risk to capital for a pre-revenue biotech

- Knowledge-Intensive Company status: the gateway to long-runway biotech funding

- SEIS-then-EIS sequencing in a biotech round

- The April 2026 EIS uplift: what it means for biotech series A and beyond

- If the biotech fails: how investor relief survives liquidation

- Frequently asked questions

Why SEIS and EIS matter more for biotech than any other sector

A loss-making biotech raising under SEIS and EIS sits at the intersection of three features that are not present together in any other sector. Drug discovery and medical device development can run for ten years or more before the first commercial sale. Spend per project is high. The probability of terminal failure is real. Every other class of UK growth company looks tame by comparison.

That risk profile is exactly what the venture capital schemes were built to fund. The income tax relief at 50 per cent (SEIS) or 30 per cent (EIS), the capital gains exemption on disposal, and the sideways loss relief under s.131 ITA 2007 against general income, together produce an investment proposition that mainstream private equity does not match for early-stage UK life sciences. In practice, SEIS and EIS for loss-making biotech is the only retail-friendly product that prices in a 10-year R&D runway with a meaningful probability of zero.

The flipside is that the same features that make biotech a natural fit also stress every gate in the legislation. The trade test, the financial health requirement, the gross assets ceiling, the age limits and the risk-to-capital condition were not written with a 10-year preclinical programme in mind. They were written with a generic two-to-five-year growth company in mind. Biotech founders and their advisers spend most of their time at the edge of those rules.

The trade test problem: when R&D rescues a pre-revenue biotech

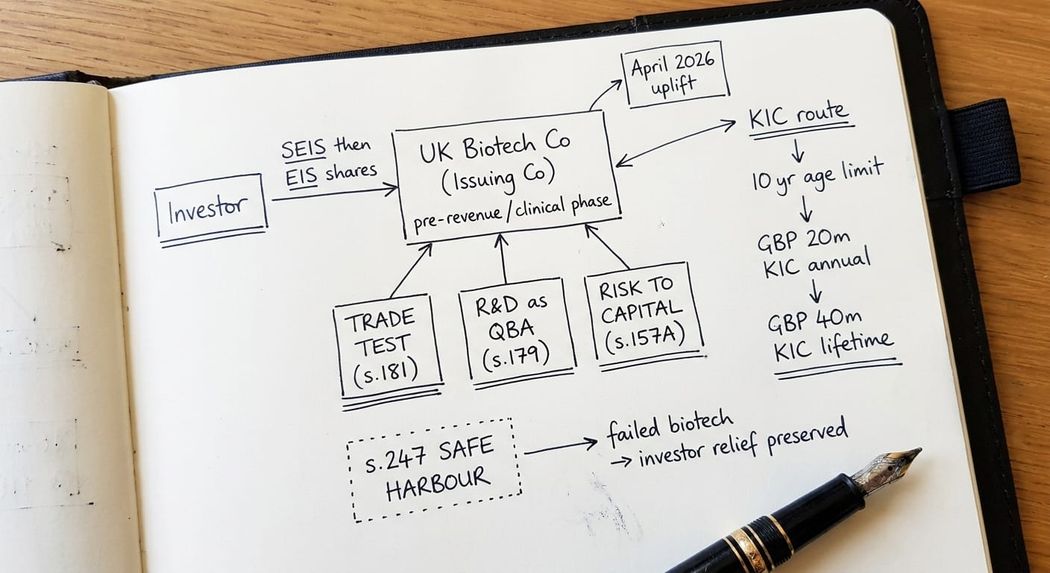

The single biggest technical issue for a loss-making biotech is the trading requirement. The issuing company must exist wholly for the purpose of carrying on a qualifying trade (s.181(2)(a) ITA 2007 for EIS, s.257DA(2)(a) for SEIS). On a literal reading, a company that is years away from a first sale is not trading at all, and would fail.

Section 179 ITA 2007 contains the rescue. A "qualifying business activity" includes (a) carrying on a qualifying trade, (b) preparing to carry on a qualifying trade where that trade commences within two years of the share issue, and (c) carrying on research and development from which it is intended that a qualifying trade will be derived. For a biotech in clinical phase, limb (c) is the workhorse provision. The R&D itself is the qualifying business activity. The company does not need to be open for sales to satisfy the test.

Risk to capital for a pre-revenue biotech

The risk-to-capital condition (s.157A ITA 2007 for EIS, s.257AAA for SEIS, both inserted by Finance Act 2018) requires that the company

- has objectives to grow and develop its trade over the long term, and

- that the investment poses a significant risk of capital loss to the investor of an amount greater than the net return.

For a loss-making biotech the second limb is rarely the issue. A pre-revenue clinical-stage company is, almost by definition, a high-risk-of-capital investment. The first limb is where careful drafting matters. HMRC will look for a credible long-term growth narrative supported by a business plan that identifies measurable growth metrics, including pipeline progression, headcount in scientific functions, IP portfolio development, and clinical milestones. Generic "we plan to expand" language does not satisfy VCM8542.

In our experience the risk-to-capital condition is rarely the cause of refusal for an genuine biotech, but it is increasingly the cause of refusal where the funding structure looks engineered. Convertible loan notes that effectively guarantee returns, redeemable share classes, anti-dilution mechanics that protect the investor from downside, and early exit arrangements are all read as capital-preservation indicators by HMRC's Venture Capital Reliefs (VCR) Team. A biotech advance assurance application that makes the investor feel safe is usually the one that fails.

Knowledge-Intensive Company status: the gateway to long-runway biotech funding

Most biotech companies that survive long enough to matter will need to claim Knowledge-Intensive Company (KIC) status under s.252A ITA 2007. KIC is not a different scheme. It is an enhanced version of EIS that recognises that some sectors, biotech foremost among them, take longer to grow (see section below on size / limits that increased from April 2026).

The KIC qualifying tests are: an operating costs condition (R&D expenditure of at least 15 per cent of total operating costs in one of the last three accounting periods, or at least 10 per cent in each of those three periods), combined with either an innovation condition (the IP being created is expected within ten years to be the main source of business income) or a skilled employee condition (at least 20 per cent of the workforce are skilled employees engaged in R&D and hold a relevant master's or doctoral degree).

For a clinical-stage biotech both routes usually qualify. The operating costs condition is satisfied trivially in most cases, often at 80 per cent or more. The innovation condition is satisfied because the IP estate (compositions of matter, formulations, methods of use) is expected to drive future revenue. The skilled employee condition is satisfied because biotech research teams are dominated by PhD-level scientists.

There is a critical practitioner point for pre-revenue biotech. Under VCM16060, the 10-year initial investing period for a KIC may be measured from the date when annual turnover first reached £200,000, rather than from first commercial sale. For a biotech that has never made a sale, this effectively resets the clock. In combination with the R&D as qualifying business activity rule under s.179, a KIC biotech can continue to raise EIS funds well beyond the point that a non-KIC company in another sector would have aged out.

SEIS-then-EIS sequencing in a biotech round

Most biotech founders understand SEIS and EIS as two stages on the same path. In practice the sequencing rules under s.257DK ITA 2007 (no prior EIS or VCT investment before SEIS shares are issued) and the parallel restriction in the EIS legislation make sequencing the single most common cause of avoidable problems in early biotech rounds.

The basic rule is simple. SEIS shares must be issued BEFORE any EIS or VCT shares. If an EIS investor closes first (often because they have an income tax deadline), the SEIS allocation is lost in full for that round. The amounts at stake are not small: a £250,000 SEIS slice that disappears costs the founder either £125,000 of investor income tax relief or (more commonly) a renegotiated valuation when the SEIS allocation evaporates.

Two structural points help in biotech rounds specifically:

- biotech rounds tend to be large by total size and slow to close, with multiple investor types (angels, family offices, university spinout funds, EIS funds, sometimes corporate venture). The temptation to take EIS commitments alongside SEIS in the same closing is strong. The legislation does not bend. The SEIS issue must complete first, ideally a clear day before the EIS tranche, with a clear paper trail.

- the £250,000 SEIS lifetime cap (s.257DL, post April 2023) is small relative to a biotech raise. Once it is gone it is gone for good. Biotech founders should plan to use it deliberately at the seed stage and then move to EIS proper.

The sister problem is mixed convertible structures. Where SAFEs or advance subscription agreements (ASAs) are used to bridge between SEIS and EIS rounds, the conversion mechanics need to be drafted so that the SEIS shares actually issue first in legal terms. We have seen ASAs drafted with conversion language that, on a careful reading, issues all rounds at the same legal moment, which is fatal for the SEIS slice.

The April 2026 EIS uplift: what it means for biotech series A and beyond

The April 2026 reforms to EIS materially expand the funding ceiling for biotech companies that were previously running out of room. The headline changes are:

- annual company investment cap of £10 million (£20 million for KIC),

- lifetime company cap of £24 million (£40 million for KIC), and

- the gross assets test rising to £30 million pre-issue and £35 million post-issue.

The age limit (7 years standard, 10 years KIC) is unchanged.

For a biotech moving from late seed into series A territory, the practical effect is that EIS becomes a viable component of substantially larger rounds than was previously possible. Pre-April 2026, a £10 million KIC raise was only possible if you used the full £10 million annual KIC limit and had not used it in the prior 12 months. The new £20 million KIC annual cap allows a clean tranche through EIS even where the round also includes non-EIS institutional money.

Three planning consequences flow from the uplift.

- a biotech that was about to age out of EIS at year 7 should reassess KIC eligibility now: the 10-year KIC window combined with the larger gross-assets ceiling means more late-stage clinical companies can stay in scope.

- the gross assets test is the practical gate for biotech with significant capitalised IP, plant or facilities; the new £30 million pre-issue figure changes the answer for a number of companies that were close to the line under the £15 million test.

- the larger limits change the calculus for combined EIS and VC structures: a biotech can now structure a meaningful EIS allocation alongside an institutional anchor without forcing the EIS slice into an awkwardly small minority.

It is worth noting what has not changed. The trade test, the qualifying business activity rules, the financial health requirement, the risk-to-capital condition and the connected persons rules all still apply in their pre-April 2026 form. The April 2026 reforms relax the size limits, not the structural conditions.

Key takeaway: SEIS and EIS for loss-making biotech work because s.179 treats R&D as a qualifying business activity, KIC status extends the funding window to ten years from first commercial sale (or £200k turnover), and the April 2026 uplift accommodates larger rounds. The structural traps are sequencing, financial health at the date of issue and use-of-funds drafting. Get those right and the schemes do exactly what they were designed to do.

If the biotech fails: how investor relief survives liquidation

The hardest conversation in biotech funding is the one about what happens if the science does not work. The good news for investors is that the legislation contains a meaningful safe harbour, and the loss relief regime is genuinely generous when applied correctly.

The starting point is s.182 ITA 2007 for EIS (with the parallel SEIS provision at s.257DB). A company that ceases to meet the qualifying conditions because it is wound up or dissolved for genuine commercial reasons does not trigger withdrawal of investor relief. HMRC's VCM13070 confirms that the usual genuine commercial reason is insolvency or imminent insolvency, which is the typical end-state for a failed biotech that has exhausted cash before reaching commercial viability. Investors who held their shares through to liquidation in those circumstances keep the income tax relief and the CGT exemption.

The second layer is share loss relief under s.131 ITA 2007. EIS investors get this automatically: the attribution of EIS relief makes the shares qualifying shares for s.131 purposes. SEIS investors and EIS investors who could not claim the income tax relief (for example, because they were connected to the company) need to satisfy the qualifying trading company test in s.134 ITA 2007 separately. For a biotech whose R&D is intended to lead to a qualifying trade, the company can usually be shown to be a qualifying trading company even though it never traded in the commercial sense, because R&D as a precursor to a future trade is treated consistently across the venture capital and loss relief regimes.

The mechanic for crystallising the loss is a negligible value claim under s.24(2) TCGA 1992, made while the company still legally exists. The claim is a deemed disposal at £nil value, can be backdated up to two tax years, and the resulting capital loss is then available to set against income for the year of claim or the prior year under s.131. The ordinary income tax cap on reliefs (greater of £50,000 or 25 per cent of adjusted total income) does not apply where EIS or SEIS relief is attributable to the shares.

The arithmetic for a higher-rate (45 per cent) investor on a £100,000 EIS investment that fails is: £30,000 income tax relief on the way in, £70,000 capital loss available for s.131, £31,500 of sideways loss relief, total tax mitigation of £61,500 against an economic loss of £38,500 (38.5 per cent of the original investment). For SEIS the income tax relief on the way in is 50 per cent, producing an even more favourable outcome.

This is the regime that makes biotech investable for sophisticated UK individuals. It is also the regime that depends on the company having satisfied every qualifying condition through to the point of failure. Where compliance has slipped (a missed financial health condition, a borderline trade test, an undisclosed disqualifying event), the whole structure unwinds and the investor faces the full economic loss without statutory mitigation.

Frequently asked questions

Can a loss-making biotech with no sales raise SEIS or EIS money?

Yes. Section 179 ITA 2007 treats carrying on research and development from which a qualifying trade is intended to be derived as a qualifying business activity in its own right. A pre-revenue biotech in IND-enabling, preclinical or clinical-phase R&D will typically satisfy the trade test on this basis, provided the use of funds and business plan are drafted consistently. The company still has to satisfy the financial health requirement (s.257DE for SEIS, equivalent for EIS) at the date of issue.

Does SEIS and EIS biotech eligibility change after April 2026?

The size limits change materially. The annual EIS company cap rises to £10 million (£20 million for KIC), the lifetime cap to £24 million (£40 million for KIC), and the gross assets test to £30 million pre-issue and £35 million post-issue. The structural conditions, including trade test, risk-to-capital, age limits and connected persons rules, are unchanged. SEIS limits (£250,000 lifetime cap, £350,000 gross assets test, 25 FTE limit) are unchanged.

What is a Knowledge-Intensive Company and why does it matter for biotech?

A KIC is an EIS company that meets the operating costs condition (R&D at least 15 per cent of total operating costs in one of the last three years, or 10 per cent in each) plus either an innovation condition or a skilled employee condition. Most clinical-stage biotech companies qualify. KIC status extends the EIS first-investment age limit to 10 years (and can be measured from the date annual turnover first reached £200,000 for a pre-revenue company), raises the headcount limit to 500, and unlocks the higher annual and lifetime company caps.

Why does sequencing matter so much in a biotech SEIS and EIS round?

Section 257DK ITA 2007 disqualifies a company from SEIS if it has previously received any EIS or VCT investment. In a mixed round with both SEIS and EIS investors, the SEIS allocation must complete first, with separate share issues and a clear chronological paper trail. If the EIS investor closes first, often driven by an income tax deadline, the SEIS slice is lost. ASAs and SAFEs need careful drafting so that the deemed legal moment of SEIS issue precedes the EIS issue.

If our biotech fails, do investors lose all their tax reliefs?

Generally not, provided the company is wound up for genuine commercial reasons (s.182 ITA 2007 for EIS, s.257DB for SEIS, and VCM13070). Investors keep the income tax relief and CGT exemption already obtained, and can crystallise the capital loss through a negligible value claim under s.24(2) TCGA 1992. EIS investors automatically have qualifying shares for s.131 share loss relief. SEIS investors and connected EIS investors need to show the company met the qualifying trading company test in s.134 separately, but a biotech in active R&D usually does.

Can a biotech use SEIS or EIS while also claiming R&D tax credits?

Yes. The R&D tax credit regime and the venture capital reliefs operate independently. SEIS and EIS-backed biotech companies regularly claim R&D relief in the same accounting period in which they raise SEIS or EIS funding, subject to the usual restrictions on subsidised expenditure (s.1138 CTA 2009 for the SME scheme as it applied pre-April 2024, and the reformed scheme rules for accounting periods beginning on or after 1 April 2024). We advise on both streams and can sequence the claims to avoid one regime undermining the other.

Do the connected persons rules cause problems for biotech founders investing in their own company?

For SEIS, founders and directors can subscribe for SEIS shares provided they hold no more than a 30 per cent interest (s.257BB read with the substantial interest definition in s.257BF) and meet the other investor conditions in Chapter 2 of Part 5A ITA 2007. SEIS is markedly more permissive than EIS on director investment. For EIS, the position is tighter: a director who is paid is generally treated as connected and ineligible for relief on their own subscription unless the business angel director exception applies. Most biotech founder investments at seed are best structured under SEIS for this reason.

What does HMRC look at most closely on a biotech advance assurance application?

In our experience the four areas are: (1) the use-of-funds narrative and how it maps to qualifying R&D under s.179, (2) the risk-to-capital condition with reference to share rights and any anti-dilution or redemption mechanics, (3) the financial health requirement at the date of intended issue, and (4) the cap table and any connected persons or group structuring. A clean biotech application that addresses all four explicitly tends to clear advance assurance without follow-up correspondence.

Where to take this next

A loss-making biotech should approach SEIS and EIS as a multi-year structural project, not a one-off filing. The decisions made at the seed round, including how the SEIS allocation is sized and used, whether ASAs are deployed, how the use-of-funds story is drafted, and whether the company is on a credible path to KIC status, set the boundaries of every funding round that follows.

We act for UK biotech and life sciences companies on SEIS and EIS structuring, advance assurance applications to HMRC's Venture Capital Reliefs Team, EIS1 and SEIS1 compliance statements, and on enquiry defence where reliefs are challenged. If you are planning a biotech raise in the next twelve months and want a specialist view on whether the structure works, contact Steve Livingston at IP Tax Solutions or visit our SEIS and EIS advisory page.

The above article covers highly technical and complex areas of tax law and it should not be considered to constitute professional advice. Please reach out for technical assistance specific to your circumstances.